|

시장보고서

상품코드

1910638

육류 포장 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Meat Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

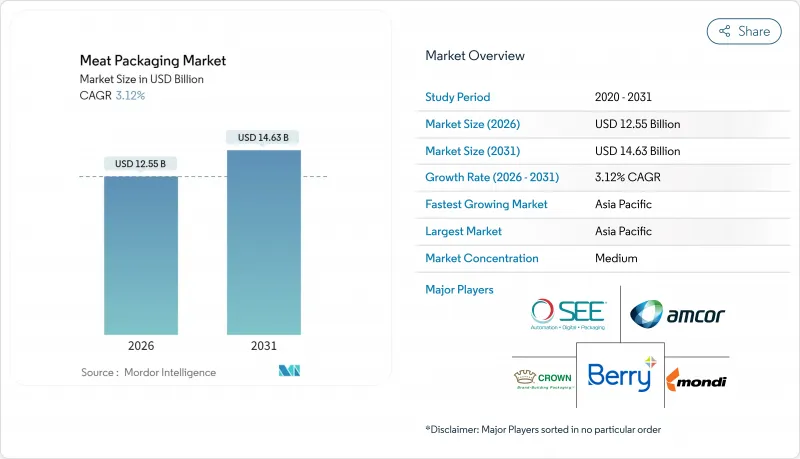

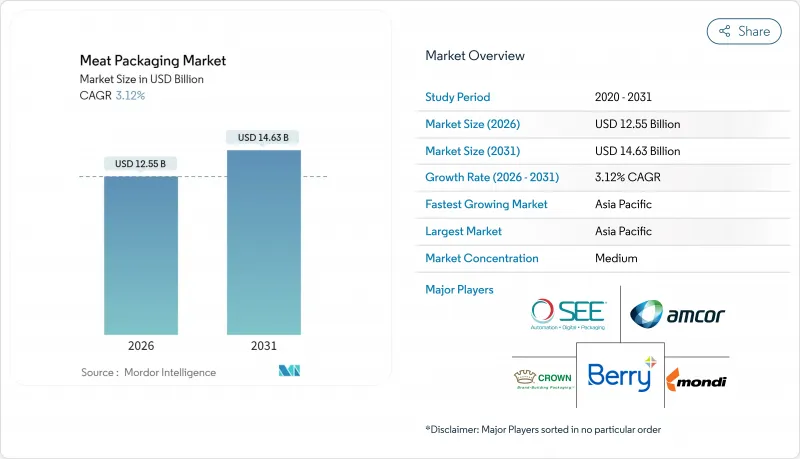

세계의 육류포장 시장 규모는 2026년 125억 5,000만 달러로 추정되며, 2025년 121억 7,000만 달러에서 성장을 이어가고 있습니다. 2031년에는 146억 3,000만 달러에 달할 전망으로, 2026년부터 2031년까지 CAGR 3.12%로 확대될 것으로 예측되고 있습니다.

이 성장은 편의성이 높은 육류 제품 형태에 대한 안정적인 수요, 콜드체인 물류의 보급 확대, 세계 식품 안전 및 지속가능성 규제의 강화를 반영합니다. 소매업체가 장기 보존성과 시각적 소구력 강화를 추진하는 가운데 연질 플라스틱, 조정 분위기 포장, 고배리어 단일 소재가 사양의 주류를 차지하고 있습니다. 아시아태평양이 최대 판매량을 견인하는 한편, 온라인 식료품 및 밀키트 채널이 가장 급속한 증가율을 기록하고 있습니다. 플라스틱 폐기물 규제, 원료 가격 변동, 대체 단백질의 상승이 이익률 전망을 억제하고, 생산자는 재생 가능 필름, 자동화, 스마트 포장 기술에 대한 노력을 촉진하고 있습니다.

세계의 육류 포장 시장 동향과 통찰

편의성과 즉시 섭취가 가능한 육류 제품에 대한 수요

부가가치 육류 제품의 소비자 채용률은 2016년 37%에서 2022년 67%로 상승하여 가공업자를 매장에서의 취급을 최소화하면서 색상과 식감을 유지하는 케이스 레이디 형식으로 이끌고 있습니다. Tyson Fresh Meats는 첨단 배리어 필름을 통한 유통 효율화와 보존 기간 연장을 목적으로 하는 '범용 케이스 레디 프로그램'을 시작했습니다. 시간 제한이 있는 도시 지역의 구매자는 빠른 조리를 가능하게 하는 패키지에 대해 프리미엄 가격을 받아들입니다. 조리된 식품의 성장은 맛과 영양소를 보호하는 고압 처리(HPP) 및 가스 대체 포장(MAP) 시스템에 대한 수요를 가속화하고 있습니다. 이러한 동향은 성숙 도시와 신흥 도시 모두에서 고기 포장 시장의 지속적인 수량 증가를 강화하고 있습니다.

조직화된 소매 및 콜드체인 물류 확대

중국의 편의점 매출은 2023년 전년 대비 10.8% 증가한 4,248억 위안에 이르렀으며, 신선식품이 성장을 견인했습니다. Yueshi Robot 등 신흥기업은 -30℃ 환경에서 가동하는 자율주행 지게차를 도입하여 냉동유통 거점의 효율화를 도모하고 있습니다. 2035년까지 562억 달러에 달할 것으로 예상된 상업용 냉동 설비에 대한 투자 확대에 따라 저온 스트레스를 견디면서 산소 침입을 최소화하는 포장이 요구되고 있습니다. 소매업체는 선반 보충의 신속화를 위해 표준화된 형상을 요구하고 있어 컨버터는 대량 생산 라인에 적응한 플렉서블 파우치나 열성형 트레이의 개발을 추진하고 있습니다. 이러한 동향은 조직화된 소매업이 육류 포장 시장의 장기적인 성장 요인임을 확고히 하고 있습니다.

항균성 및 나노복합 필름의 채용

항균성 나노 복합체는 육류 표면에서 직접 미생물의 성장을 억제하고 보존 기간을 연장하고 보존제에 대한 의존도를 줄입니다. 천연 추출물을 배합한 하이드로겔 캐리어는 식품 안전성을 유지하면서 박테리아 수를 줄이는 효과를 보여줍니다. 북미 및 유럽에서의 파일럿 라인은 상업화를 위한 생산 규모의 확대를 추진하고 있습니다. 이와 같은 필름을 투명한 MAP(가스 치환 포장) 덮개와 조합함으로써 시너지 효과가 생겨 냉장 케이스에서 중요한 능동적 보호와 제품 가시성을 모두 실현합니다.

부문 분석

2025년 시점에서 플렉서블 플라스틱은 불규칙한 형상에 대한 적합성과 우수한 인쇄 적성으로 인해 육류 포장 시장의 41.32%를 차지했습니다. 생분해성 필름은 여전히 틈새 시장이면서 퇴비화 가능 또는 재활용 가능한 솔루션을 규제 당국이 권장하는 가운데 6.85%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 금속 캔과 알루미늄 포일은 멸균이 필요한 고급 퍼티와 장기 보존 제품에서 여전히 필수적입니다. 항균성 나노복합재 층이 플렉서블 웹에 도입되어, 배리어 성능에 더해 능동적인 세균 억제 효과를 제공합니다. 수지 및 코팅 기술의 지속적인 혁신으로 가공업자는 천공 저항성을 유지하면서 두께를 줄일 수 있으며 연포장 비용 경쟁력을 유지합니다.

PET나 PP 경질 트레이는 적재성을 중시하는 슬라이스 제품용이지만, 재료 질량이 많기 때문에 지속가능성의 관점에서 과제가 있습니다. 발포 트레이는 재활용 분류를 용이하게 하는 투명한 단일 PET 트레이로 시장을 양도하고 있습니다. 금속 트레이는 뛰어난 기밀성으로 인해 수출용 콘비프와 런천 미트에서 여전히 사용되지만 무게와 비용은 성장 장벽이 되었습니다. 전반적으로 브랜드가 지속가능성과 상품 진열 요구를 양립시키는 동안 유연한 솔루션은 육류 포장 시장을 주도할 것입니다.

2025년 시점에서 신선 및 냉동 제품이 육류 포장 시장의 53.25%를 차지했습니다. 이것은 슈퍼마켓에서 시각적으로 매력적이고 누설 방지 기능을 갖추고 있으며, 여러 날의 보존 기간을 견디는 트레이와 겹침 포장에 대한 수요에 의해 지원되었습니다. 신흥국에서의 콜드체인망 확대에 따라 성장은 견조하게 추이하고 있습니다. 델리 슬라이스에서 상온 보존 가능한 육포에 이르는 즉시 섭취 라인은 편리성을 중시하는 라이프 스타일을 배경으로 CAGR 5.32%로 확대됩니다. 이러한 형태에는 고산소 및 고습기 배리어성, 전자레인지 대응 씰, 소비자 친화적인 개봉성이 요구되어 박리식 뚜껑이나 분량 관리 기술에 혁신을 촉진하고 있습니다.

가공육 제품은 안정적인 점유율을 유지하고 있지만, 건강 동향이 높아짐에 따라, 보다 저지방 부위나 식물성 대체품에 수요 이동을 볼 수 있습니다. 포장의 개량점으로서는 재봉 가능한 지퍼나 진공 스킨 포장이 주목받고 있어, 식감을 돋보이게 하면서 공기의 모임을 최소한으로 억제합니다. 범주를 불문하고 열화 위험을 표시하는 스마트 인디케이터에 대한 수요가 높아지고 있어, 혼잡한 진열 선반에서의 차별화를 강화해, 소비자의 육제품 포장 시장에의 신뢰를 높이고 있습니다.

지역별 분석

아시아태평양은 2025년 육류 포장 시장 규모의 33.40%를 차지했으며 중국의 연간 약 1억톤의 육류 소비량과 소매업의 현대화가 이를 지원하고 있습니다. 2031년까지 예상되는 지역 CAGR 4.56%는 베이징에서 방갈로르에 이르는 도시화와 콜드체인 거점에 대한 투자를 반영합니다. 중국의 온라인 소고기 구매 점유율은 44%를 넘어 택배 네트워크용으로 설계된 전자상거래 대응 포장의 급속한 보급을 보여줍니다. 인도의 슈퍼마켓은 냉동 식품 매장을 확대하고 MAP 및 VSP(진공 스킨 포장) 솔루션의 적용 기반을 넓히고 있습니다. 동남아시아의 편의점 체인도 이에 따라 습윤 기후를 견디는 표준화된 파우치 형식을 채용하고 있습니다.

북미에서는 높은 1인당 육류 소비량과 성숙한 소매 인프라가 시너지 효과를 발휘합니다. 성장의 원동력은 기술 도입에 있으며 블록체인 추적 시스템, 항균 필름, 자동화 대응 봉지 기계 등을 들 수 있습니다. 규제 검토를 계기로 단일 소재 배리어 필름의 시험 도입이 진행되고, 특히 캐나다의 대형 체인에서 현저합니다. 유럽은 순환형 경제에 대한 적합성에서 주도적 입장에 있어 컨버터 기업에 대해 재생 가능한 PE 및 PP 구조나 종이 섬유 하이브리드로의 전환을 추진하고 있습니다. 산소 장벽과 재생 가능성의 두 목표를 달성하는 포장 회사는 EU 식료품점에서 우선 공급업체로서의 지위를 받았습니다.

남미에서는 브라질 수출 지향 가공업자로부터 대양 횡단 수송을 견디는 견고한 포장에 대한 안정적인 수요를 볼 수 있습니다. 높은 배리어성 파우치, 엠보싱 가공 진공 봉투, 강인한 골판지 외장이 표준 사양이 되고 있습니다. 중동 및 아프리카에서는 보급 상황에 편차가 보이고 걸프 국가의 소매업체는 고급 MAP 포장 스테이크를 지정하는 한편, 많은 아프리카 시장에서는 여전히 정육점 용지에 의존하고 있습니다. 콜드체인 부족이 보급을 제한하지만, 인프라 투자와 퀵커머스의 시험 도입에 의해 단계적인 보급이 진행될 전망입니다. 이러한 각 지역별 동향이 모여, 다층적인 성장 경로가 형성되어 세계의 육류 포장 시장을 확대시키고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 편의성과 RTE 육류 제품에 대한 수요

- 조직화된 소매업과 콜드체인 물류 확대

- 보존 기간 연장과 식품 안전 규제

- 지속가능성을 중시한 고배리어 단일 소재로 이행

- 항균성 및 나노복합 필름의 채용(주목도 낮음)

- 블록체인을 활용한 추적 가능성과 변조 방지 포맷(주목도 낮음)

- 시장 성장 억제요인

- 플라스틱 폐기물 규제와 재활용 가능성의 과제

- 변동하는 폴리머 및 금속 원료 가격

- 일회용 포장세 및 EPR(확대 생산자 책임) 비용

- 대체 단백질의 성장에 의한 붉은 고기 수요 감소(주목도 낮음)

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 팬데믹의 영향 분석 및 회복 분석

제5장 시장 규모와 성장 예측

- 소재 유형별

- 플라스틱

- 플렉서블 파우치

- 가방

- 필름 및 포장재

- 기타 플렉서블

- 경질 트레이 및 용기

- 기타(경질 용기)

- 플렉서블 파우치

- 금속

- 알루미늄

- 철강

- 기타 금속

- 플라스틱

- 고기유형별

- 신선 및 냉동

- 가공품

- Ready-to-eat

- 포장 기술별

- 가스 치환 포장(MAP)

- 진공 스킨 포장(VSP)

- 능동적 및 지능적 포장

- 식용 및 생분해성 필름

- 최종 사용자 채널별

- 소매(슈퍼마켓 및 하이퍼마켓)

- 외식산업 및 HORECA

- 온라인 식료품 및 밀키트

- 육류 가공업자 및 포장업자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향과 발전

- 시장 점유율 분석

- 기업 프로파일

- Amcor plc

- Sealed Air Corporation

- Berry Global Group Inc.

- Mondi plc

- Crown Holdings Inc.

- Coveris Management GmbH

- Winpak Ltd.

- Smurfit Kappa Group plc

- Viscofan SA

- Sonoco Products Company

- Huhtamaki Oyj

- DS Smith plc

- WestRock Company

- Graphic Packaging Holding Company

- Tetra Pak International SA

- Klockner Pentaplast GmbH

- Constantia Flexibles GmbH

- Cascades Inc.

- Innovia Films Ltd.

- LINPAC Packaging Ltd.

제7장 시장 기회와 미래 전망

SHW 26.01.26Meat packaging market size in 2026 is estimated at USD 12.55 billion, growing from 2025 value of USD 12.17 billion with 2031 projections showing USD 14.63 billion, growing at 3.12% CAGR over 2026-2031.

Growth reflects steady demand for convenience meat formats, widening adoption of cold-chain logistics, and tightening global food-safety and sustainability rules. Flexible plastics, modified-atmosphere formats, and high-barrier mono-materials dominate specifications as retailers push longer shelf life and stronger visual appeal. Asia-Pacific drives the largest volumes, while online grocery and meal-kit channels record the fastest incremental gains. Plastic-waste regulation, raw-material volatility, and the rise of alternative proteins temper margin outlooks, encouraging producers to pursue recyclable films, automation, and smart-packaging innovations.

Global Meat Packaging Market Trends and Insights

Demand for Convenience and Ready-to-Eat Meat Products

Consumer adoption of value-added meat rose from 37% to 67% between 2016 and 2022, pushing processors toward case-ready formats that minimise in-store handling while preserving colour and texture. Tyson Fresh Meats launched its Universal Case Ready Program to streamline distribution and extend shelf life via advanced barrier films. Urban shoppers, pressed for time, accept premium price points for packs enabling rapid meal preparation. Growth in fresh-prepared foods accelerates demand for high-pressure processing and modified-atmosphere systems that safeguard taste and nutrients. These dynamics reinforce sustained volume gains for the meat packaging market in both mature and emerging cities.

Expansion of Organized Retail and Cold-Chain Logistics

Convenience-store sales in China climbed to CNY 424.8 billion in 2023, up 10.8% year on year, with fresh foods steering the rise. Start-ups such as Yueshi Robot are deploying autonomous forklifts operating at -30 °C, lifting efficiency in frozen distribution nodes. Broader commercial-refrigeration investment, projected to reach USD 56.2 billion by 2035, requires packaging that resists low-temperature stress while keeping oxygen ingress minimal. Retailers also demand standardised shapes to speed shelf replenishment, steering converters toward flexible pouches and thermoformed trays adapted for high-volume lines. These trends cement organised retail as a long-run catalyst for the meat packaging market.

Adoption of Antimicrobial/Nanocomposite Films

Antimicrobial nanocomposites inhibit microbial growth directly on the meat surface, extending shelf life and lowering reliance on preservatives. Hydrogel carriers infused with natural extracts show efficacy in lowering bacterial counts while remaining food-safe. Pilot lines in North America and Europe are scaling production for commercial launch. Synergies arise when such films are paired with transparent MAP lids, offering both active protection and product visibility critical for refrigerated cases.

Other drivers and restraints analyzed in the detailed report include:

- Shelf-Life Extension and Food-Safety Regulations

- Sustainability-Led Shift to High-Barrier Mono-Materials

- Blockchain-Enabled Traceability and Tamper-Evident Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexible plastics held 41.32% of the meat packaging market in 2025, propelled by conformance to irregular cuts and excellent printability. Biodegradable films, though still niche, record a 6.85% CAGR as regulators favour compostable or recyclable solutions. Metal cans and foil remain vital for premium pate and long-life products requiring sterilisation. Antimicrobial nanocomposite layers are entering flexible webs, offering active bacterial suppression alongside barrier performance. Continuous resin and coating innovation allows converters to downgrade gauge while maintaining puncture resistance, keeping flexible packs cost-competitive.

Rigid trays, often PET or PP, serve sliced products where stackability matters, but face sustainability scrutiny for their higher material mass. Foam trays are losing ground to clear mono-PET variants that ease recyclability sorting. Metal options endure in export-grade corned beef and luncheon meat thanks to superior hermetic integrity, yet their growth is limited by weight and cost. Overall, flexible solutions will keep leading the meat packaging market as brands balance sustainability with merchandising demands.

Fresh and frozen products generated 53.25% of the meat packaging market size in 2025, backed by supermarket demand for visually appealing, leak-proof trays and overwraps that endure multi-day shelf life. Growth remains healthy as cold-chain coverage widens in emerging economies. Ready-to-eat lines, from deli slices to shelf-stable jerky, grow at 5.32% CAGR as lifestyles favour convenience. These formats need high-oxygen and moisture barriers, microwave-safe seals, and consumer-friendly openings, spurring innovation in peelable lidding and portion control.

Processed meats enjoy steady share, though health trends shift some volume toward leaner cuts and plant alternatives. Packaging upgrades focus on resealable zippers and vacuum skin formats that highlight texture while minimising air pockets. Across categories, demand converges toward smart indicators that display spoilage risk, reinforcing differentiation in crowded cases and boosting shopper confidence in the meat packaging market.

The Meat Packaging Market Report is Segmented by Material Type (Plastic, Metal), Meat Type (Fresh and Frozen, Processed, Ready-To-Eat), Packaging Technology (Modified Atmosphere Packaging (MAP), Vacuum Skin Packaging, and More ), End-User Channel (Retail, Foodservice, Online Grocery, Meat Processors), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 33.40% of the meat packaging market size in 2025, underpinned by China's near-100 million-ton meat consumption and vigorous retail modernisation. Regional CAGR of 4.56% through 2031 reflects urbanisation and investment in cold-chain nodes from Beijing to Bangalore. China's online beef purchases surpassed 44% share, signalling rapid uptake of e-commerce friendly packs designed for parcel networks. Indian supermarkets multiply freezer aisles, widening the addressable base for MAP and VSP solutions. Southeast Asian convenience chains follow suit, embracing standardised pouch formats that withstand humid climates.

North America combines high per-capita meat intake with mature retail infrastructure. Growth stems from technology adoption: blockchain tracing, antimicrobial films, and automation-ready baggers. Regulatory reviews spur trials of monomaterial barrier films, especially in Canada's major chains. Europe leads in circular-economy compliance, pushing converters toward recyclable PE/PP structures and paper-fibre hybrids. Packaging firms that meet both oxygen-barrier and recyclability targets unlock preferred supplier status with EU grocers.

South America sees steady demand from Brazil's export-oriented processors that need robust packs for transoceanic shipping. High-barrier pouches, embossed vacuum bags, and strong corrugated outers are standard. Middle East & Africa exhibit uneven penetration; Gulf retailers specify premium MAP steaks, while many African markets still rely on butcher paper. Cold-chain gaps limit adoption but infrastructure investments and quick-commerce pilots point to gradual uptake. Together, these geographic dynamics foster multi-speed growth paths that expand the global meat packaging market.

- Amcor plc

- Sealed Air Corporation

- Berry Global Group Inc.

- Mondi plc

- Crown Holdings Inc.

- Coveris Management GmbH

- Winpak Ltd.

- Smurfit Kappa Group plc

- Viscofan S.A.

- Sonoco Products Company

- Huhtamaki Oyj

- DS Smith plc

- WestRock Company

- Graphic Packaging Holding Company

- Tetra Pak International S.A.

- Klockner Pentaplast GmbH

- Constantia Flexibles GmbH

- Cascades Inc.

- Innovia Films Ltd.

- LINPAC Packaging Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for convenience and RTE meat products

- 4.2.2 Expansion of organized retail and cold-chain logistics

- 4.2.3 Shelf-life extension and food?safety regulations

- 4.2.4 Sustainability-led shift to high-barrier mono-materials

- 4.2.5 Adoption of antimicrobial / nanocomposite films (under-radar)

- 4.2.6 Blockchain-enabled traceability and tamper-evident formats (under-radar)

- 4.3 Market Restraints

- 4.3.1 Plastic-waste regulations and recyclability challenges

- 4.3.2 Volatile polymer and metal input prices

- 4.3.3 Single-use-packaging taxes and EPR fees

- 4.3.4 Growth of alternative proteins reducing red-meat demand (under-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pandemic Impact and Recovery Analysis

5 MARKET SIZE and GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastic

- 5.1.1.1 Flexible Pouches

- 5.1.1.1.1 Bags

- 5.1.1.1.2 Films and Wraps

- 5.1.1.1.3 Other Flexible

- 5.1.1.2 Rigid Trays and Containers

- 5.1.1.2.1 Other Rigid

- 5.1.1.1 Flexible Pouches

- 5.1.2 Metal

- 5.1.2.1 Aluminium

- 5.1.2.2 Steel

- 5.1.2.3 Other Metals

- 5.1.1 Plastic

- 5.2 By Meat Type

- 5.2.1 Fresh and Frozen

- 5.2.2 Processed

- 5.2.3 Ready-to-Eat

- 5.3 By Packaging Technology

- 5.3.1 Modified Atmosphere Packaging (MAP)

- 5.3.2 Vacuum Skin Packaging (VSP)

- 5.3.3 Active and Intelligent Packaging

- 5.3.4 Edible and Biodegradable Films

- 5.4 By End-user Channel

- 5.4.1 Retail (Supermarkets / Hypermarkets)

- 5.4.2 Food-service / HORECA

- 5.4.3 Online Grocery and Meal-kit

- 5.4.4 Meat Processors / Packers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Sealed Air Corporation

- 6.4.3 Berry Global Group Inc.

- 6.4.4 Mondi plc

- 6.4.5 Crown Holdings Inc.

- 6.4.6 Coveris Management GmbH

- 6.4.7 Winpak Ltd.

- 6.4.8 Smurfit Kappa Group plc

- 6.4.9 Viscofan S.A.

- 6.4.10 Sonoco Products Company

- 6.4.11 Huhtamaki Oyj

- 6.4.12 DS Smith plc

- 6.4.13 WestRock Company

- 6.4.14 Graphic Packaging Holding Company

- 6.4.15 Tetra Pak International S.A.

- 6.4.16 Klockner Pentaplast GmbH

- 6.4.17 Constantia Flexibles GmbH

- 6.4.18 Cascades Inc.

- 6.4.19 Innovia Films Ltd.

- 6.4.20 LINPAC Packaging Ltd.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment