|

시장보고서

상품코드

1851861

알레르기 치료 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Allergy Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

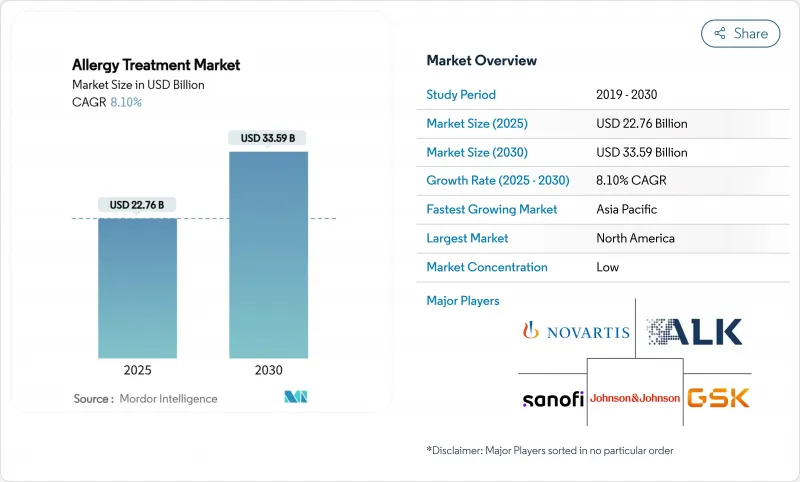

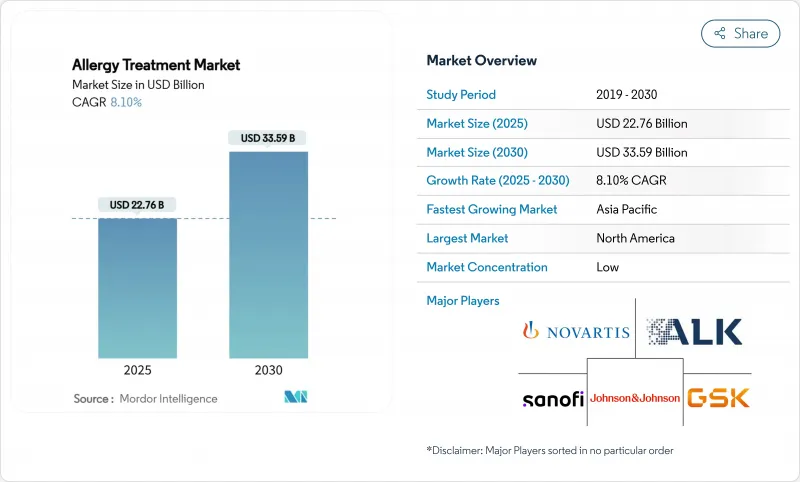

세계의 알레르기 치료 시장 규모는 2025년 227억 6,000만 달러에 이르고, 2030년까지 335억 9,000만 달러로 확대되며, 예측 기간 중 CAGR은 8.10%를 보일 것으로 예측됩니다.

가속하는 질병의 만연, 기후로 인한 알레르겐의 증폭, 획기적인 생물제제가 총체로서 수요를 밀어 올리고 있는 한편, 새로운 디지털 헬스 모델이 액세스와 어드히어런스를 확대하고 있습니다. 오말리주맙이 최초의 다식품 적응을 획득한 이래 경쟁업체 간의 적대관계는 치열해지고 있으며, 주요 제약기업과 민첩한 생명공학기업 모두가 직접 라이벌 관계에 있습니다. 바이오시밀러의 대체를 가속화하는 규제 이니셔티브는 가격 압력을 높이는 동시에 전달 기술, 면역 요법의 개별화, 환자 중심 의료에서의 혁신을 자극하고 있습니다. 지리적 괴리는 여전히 현저합니다. 북미는 생물학적 제제에 대한 지출에서 주도권을 유지하고 있는 반면, 아시아태평양은 도시화의 진전에 의해 감작 수준이 높아지고 있으며, 면역요법의 급속한 보급을 기록하고 있습니다.

세계 알레르기 치료 시장 동향과 통찰

알레르기성 비염과 천식 유병률 상승

급증하는 도시 대기 오염은 산화 스트레스를 촉진하고 면역 반응을 TH2 프로파일로 반전시켜 알레르기 치료 시장에서 처방된 항히스타민제, 류코트리엔 길항제 및 생물학적 제제에 대한 수요를 지원합니다. 베이징에서 델리까지의 대도시에서는 감작률이 50%를 넘고 있으며 미국의 비용 부담은 이미 연간 34억 달러를 넘어섰습니다. 성인의 30%, 소아의 40%가 영향을 받는 비염의 세계적인 확산으로 비염은 유일하게 가장 큰 환자층이며 확실한 수익 기반이 되었습니다.

셀프 메디케이션 및 일반의약품(OTC)에 대한 환자의 선호도 증가

내약성이 높은 2세대 항히스타민 약물과 비강 코르티코스테로이드 약물이 처방약에서 일반의약품(OTC)로 전환되어 소비자의 손에 닿는 범위가 넓어지고 알레르기 치료 시장 전체의 거래량이 증가하고 있습니다. 소매점 선반의 눈에 띄는 위치는 디지털 증상 검사기와 일치하며 가벼운 환자를 자기 관리 케어와 코 막힘 제거제의 조합으로 유도합니다. 특히 북미와 서유럽에서는 지역 약국에서의 진단 대기 시간의 단축이 이 행동을 보다 견고하게 하고 있습니다.

저가 바이오시밀러의 보급이 가속되고 가격 및 이익률이 저하

호환 가능한 오말리주맙과 우스테키누맙의 바이오시밀러는 잇따라 단가를 최대 40% 낮추고 알레르기 치료 시장에서 오리지네이터의 톱 라인 성장을 압박하고 있습니다. 유럽에서는 입찰 제도가 보급을 가속하고, 신흥국에서는 비용 절감이 생물학적 제제에 대한 액세스 입구가 됩니다. 오리지네이터는 프리미엄 포지셔닝을 정당화하기 위해 장치 업그레이드 및 실제 세계 증거 문서를 지원합니다.

부문 분석

비염은 2024년 알레르기 치료 시장 점유율로 41.51%를 차지했으며 세계적인 높은 유병률과 멀티모달 치료 툴킷을 활용하고 있습니다. 시판되는 항히스타민제, 비강 코르티코스테로이드제, SLIT 정제가 치료의 기둥이 되는 한편, 생물학적 제제가 중증인 다감증 환자를 견인하고 있습니다. 계절성 및 연중 알레르기성 질환은 공동으로 광범위한 처방 기반을 유지하며 응급 치료 클래스와 상관없이 기본적인 수요를 보장합니다.

2030년까지 연평균 복합 성장률(CAGR)이 9.65%로 가장 급성장하고 있는 식품 알레르기는 최초의 질환 수식성 생물학적 제제의 승인과 경구 면역요법의 광범위한 파이프라인의 혜택을 받고 있습니다. 성인 발병 알레르기의 역학적 인지에 의해 대상자가 확대되고, 학교 기반의 아나필락시스 프로토콜에 의해 예방적 처방이 확대됩니다. 눈, 피부, 천식 및 기타 틈새 알레르기는 진단 강화와 생물학적 제제의 교차 적응으로 각각 처방 수를 늘리고 있습니다.

항알레르기 약은 유리한 상환, OTC의 융성, 성숙해지고 있는 제네릭 의약품에 지지되어 2024년 알레르기 치료 시장 점유율의 65.53%를 유지했습니다. 2세대 항히스타민제, 외용 코르티코스테로이드제, 류코트리엔 차단제가 안정적인 수익원을 형성하여 신규 카테고리의 가격 변동을 완화하고 있습니다.

면역요법은 2030년까지 CAGR이 10.85%가 될 것으로 예상되며, 이것은 장기적인 비용 효율성에 대한 지불측의 인식과, 재택 SLIT 요법에 대한 환자의 기호의 고조를 반영하고 있습니다. 임상 지침은 복용량과 복용 기간을 표준화하고 변동을 최소화하며 임상의의 신뢰를 높입니다. 피하투여 프로토콜은 고위험 환자에서 최상의 효과를 얻기 위한 표준으로 남아 있는 반면, 생물학적 제제와 SLIT의 병용 전략은 복잡한 다민성에 대응하기 위해 등장하여 알레르기 치료 시장 규모의 제안을 강화하고 있습니다.

지역 분석

북미의 2024년 알레르기 치료 시장 점유율 38.25%는 광범위한 보험 적용, 생물학적 제제의 조기 도입, 전문의 네트워크의 집중에 기인합니다. 미국은 다른 지역에 파급되는 규제상 선편을 붙여 국내 제조업체를 조기 수익과 라이프 사이클 연장의 우위한 입장에 두고 있습니다. 바이오시밀러 의약품의 보급은 대체품에 대한 망설임과 REMS의 제약을 고려하면 여전히 완만하고, 혁신자의 가격 안정성은 유지되고 있습니다.

아시아태평양의 2030년까지 CAGR은 9.85%로 도시화에 따른 감작성의 급증, 가처분 소득 증가, 일부 면역요법을 커버하는 공적 의료보험의 확대가 원동력이 되어 다른 전 지역을 웃돌았습니다. 아토피 집단에서는 먼지벌레 감작율이 90%를 넘어, 지역에 적합한 알레르겐 추출물 수요가 높아져, ALK-Abbello와 Abbott의 제휴와 같은 공동 판매 계약이 촉진됩니다. 모바일 퍼스트 헬스케어의 도입으로 대도시 지역에서 SLIT 원격 치료가 가속화되고 치료 범위가 확대됩니다.

유럽은 보급이 성숙하고 있지만, 바이오시밀러 친화적인 입찰 제도 아래 가격 압축에 직면하고 있습니다. 이 지역은 면역요법의 품질과 부작용 모니터링 표준화를 선도하고 있으며, 지속 가능한 수익성장에 기여하고 있지만, 그 성장은 억제되고 있습니다. 중동 및 아프리카와 남미는 경제와 공급망의 불안정성으로 인해 당면의 견인력이 약해지지만, 전문 의료 인프라가 서서히 개선되어 새로운 비즈니스 기회를 가져오고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 알레르기성 비염 및 천식의 유병률 상승

- 셀프 메디케이션 및 OTC 의약품에 대한 환자 기호 향상

- 신규 치료제 및 생물제제에 대한 투자 증가

- 온라인 재택 SLIT 텔레케어 플랫폼의 확대

- 항-IgE 단클론항체의 상업화

- 기후에 의한 알레르겐 부하 증폭

- 시장 성장 억제요인

- 저가격 바이오시밀러 보급이 진행되어 가격 및 이익률이 저하

- AIT의 장기적 베네핏에 대한 환자 및 HCP의 낮은 인식

- 생물학적 제제와 SLIT 요법에 대한 한정적인 보험 상환

- 천연 알레르겐 추출물 공급망 위험

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 알레르기 유형별

- 눈 알레르기

- 비염

- 천식

- 피부 알레르기

- 식품 알레르기

- 기타 알레르기

- 치료별

- 항알레르기약

- 항히스타민제 - 제1세대

- 항히스타민제 - 제2/제3세대

- 부신피질스테로이드 - 외용약, 흡입약, 전신약

- 울혈 제거제 - 경구제, 점비약

- 류코트리엔 수용체 길항제

- 생물제제 및 mAbs

- 면역요법

- 피하 주사(SCIT)

- 설하 투여(SLIT-정제, 점적)

- 항알레르기약

- 제형별

- 정제 및 캡슐

- 비강 스프레이

- 안약

- 흡입기

- 주사기 및 자동 주사기

- 유통 채널별

- 병원 약국

- 소매 약국 및 드럭스토어

- 온라인 약국

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- ALK-Abello A/S

- AbbVie Inc.

- Allergy Therapeutics plc

- Bausch Health Companies Inc.

- Alembic Pharmaceuticals Ltd.

- F. Hoffmann-La Roche Ltd.

- Nicox SA

- GSK plc

- Johnson & Johnson

- Laboratorios Leti SA

- Novartis AG

- Sanofi SA

- Teva Pharmaceutical Industries

- Merck KGaA

- Stallergenes Greer

- Cipla Ltd.

- AstraZeneca plc

- Pfizer Inc.

- Regeneron Pharmaceuticals

- Bayer AG

제7장 시장 기회와 장래의 전망

JHS 25.11.25The global Allergy treatment market size reached USD 22.76 billion in 2025 and is projected to advance to USD 33.59 billion by 2030, registering an 8.10% CAGR during the forecast period.

Accelerated disease prevalence, climate-driven allergen amplification, and breakthrough biologics are collectively lifting demand, while new digital-health models broaden access and adherence. Competitive intensity has sharpened since omalizumab won the first multi-food indication, drawing both large pharmaceutical firms and nimble biotech entrants into direct rivalry. Regulatory initiatives that speed biosimilar substitution add price pressure yet simultaneously stimulate innovation in delivery technology, immunotherapy personalization, and patient-centric care. Geographic divergence remains pronounced: North America sustains spending leadership on biologics, whereas Asia-Pacific records the fastest uptake of immunotherapy as urbanization deepens sensitization levels.

Global Allergy Treatment Market Trends and Insights

Rising Prevalence of Allergic Rhinitis & Asthma

Surging urban air pollution fuels oxidative stress that flips immune responses toward a TH2 profile, anchoring demand for prescription antihistamines, leukotriene antagonists, and biologics in the Allergy treatment market. Megacities from Beijing to Delhi report sensitization rates exceeding 50%, while cost burdens in the United States already surpass USD 3.4 billion annually. The global scope of rhinitis, affecting up to 30% of adults and 40% of children, makes it the single largest patient pool and a reliable revenue base.

Increasing Patient Preference for Self-Medication & OTC Drugs

Better tolerated second-generation antihistamines and intranasal corticosteroids have migrated from prescription to OTC status, widening consumer reach and lifting overall transaction volumes in the Allergy treatment market. Retail shelf prominence aligns with digital symptom checkers, steering mild sufferers toward self-directed care and decongestant combinations. Short diagnostic wait times in community pharmacies further cement this behavior, especially across North America and Western Europe.

Escalating Uptake of Low-Cost Biosimilars Eroding Price/Margins

Interchangeable omalizumab and a wave of ustekinumab biosimilars cut unit prices by up to 40%, compressing top-line growth for originators within the Allergy treatment market. Europe's tender systems hasten penetration, while emerging economies embrace cost-relief as gateways to biologic access. Originators respond with device upgrades and real-world-evidence dossiers to justify premium positioning.

Other drivers and restraints analyzed in the detailed report include:

- Growing Investments in Novel Therapeutics & Biologics

- Expansion of Online-to-Home SLIT Tele-Care Platforms

- Low Patient & HCP Awareness of AIT Long-Term Benefits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rhinitis contributed 41.51% to the Allergy treatment market share in 2024, capitalizing on its high global prevalence and multi-modal therapy toolkit. Over-the-counter antihistamines, intranasal corticosteroids, and SLIT tablets form the therapeutic spine, while biologics gain traction in severe poly-sensitized cohorts. Seasonal and perennial variants jointly sustain an expansive prescription base, guaranteeing baseline demand regardless of emergent treatment classes.

Food allergy, the fastest-growing segment at 9.65% CAGR to 2030, benefits from the first disease-modifying biologic clearance and a broad pipeline of oral immunotherapy combinations. Epidemiological recognition of adult-onset allergy enlarges eligibility pools, and school-based anaphylaxis protocols amplify prophylactic prescriptions. Eye, skin, asthma, and other niche allergies round out the segment landscape, each adding volume through fortified diagnostic vigilance and cross-indication biologic use.

Anti-allergy drugs maintained 65.53% of the Allergy treatment market share in 2024, bolstered by favorable reimbursement, OTC prominence, and maturing generics. Second-generation antihistamines, topical corticosteroids, and leukotriene blockers together form a stable revenue stream that cushions price swings in novel categories.

Immunotherapy is slated for a 10.85% CAGR through 2030, reflecting payer recognition of long-term cost efficiency and rising patient preference for home-based SLIT regimens. Clinical guidelines standardize dosing and duration, minimizing variability and elevating clinician confidence. Subcutaneous protocols remain the gold standard for maximized efficacy in high-risk patients, while combination biologic-SLIT strategies emerge for complex multi-sensitizations, strengthening the Allergy treatment market size proposition.

The Allergy Treatment Market Report is Segmented by Allergy Type (Eye Allergy, Rhinitis, Asthma, Skin Allergy, Food Allergy, and More), Treatment (Anti-Allergy Drugs and Immunotherapy), Dosage Form (Tablets & Capsules, Nasal Sprays, and More), Distribution Channel (Hospital Pharmacies, Online Pharmacies, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 38.25% Allergy treatment market share in 2024 stems from extensive insurance coverage, early biologic adoption, and concentrated specialist networks. The United States spearheads regulatory firsts that propagate to other regions, positioning domestic manufacturers for early revenues and prolonging lifecycle advantages. Biosimilar penetration remains moderate given substitution hesitancy and REMS constraints, preserving price integrity for innovators.

Asia-Pacific's 9.85% CAGR through 2030 outpaces all other regions, driven by urbanization-linked sensitization surges, rising disposable incomes, and expanded public-health insurance that covers select immunotherapies. House-dust-mite sensitization exceeds 90% in atopic cohorts, steering demand for region-matched allergen extracts and fueling collaborative distribution deals such as ALK-Abbello's tie-up with Abbott. Mobile-first healthcare adoption accelerates SLIT tele-care in metropolitan clusters, broadening therapy reach.

Europe shows mature penetration but faces price compression under biosimilar-friendly tender frameworks. The region leads standardization of immunotherapy quality and pharmacovigilance, contributing to sustainable but restrained revenue growth. Middle East & Africa and South America present emergent opportunities with gradually improving specialty-care infrastructure, though economic and supply-chain volatility temper near-term traction.

- ALK-Abello

- Abbvie

- Allergy Therapeutics plc

- Bausch Health

- Alembic Pharmaceuticals Ltd.

- Roche

- Nicox

- GlaxoSmithKline

- Johnson & Johnson

- Laboratorios Leti S.A.

- Novartis

- Sanofi

- Teva Pharmaceutical Industries

- Merck

- Stallergenes Greer

- Cipla

- AstraZeneca

- Pfizer

- Regeneron Pharmaceuticals

- Bayer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Of Allergic Rhinitis & Asthma

- 4.2.2 Increasing Patient Preference For Self-Medication & OTC Drugs

- 4.2.3 Growing Investments In Novel Therapeutics & Biologics

- 4.2.4 Expansion Of Online-To-Home SLIT Tele-Care Platforms

- 4.2.5 Commercialisation Of Anti-Ige Monoclonal Antibodies

- 4.2.6 Climate-Induced Allergen-Load Amplification

- 4.3 Market Restraints

- 4.3.1 Escalating Uptake Of Low-Cost Biosimilars Eroding Price/Margins

- 4.3.2 Low Patient & HCP Awareness Of AIT Long-Term Benefits

- 4.3.3 Limited Reimbursement For Biologic & SLIT Therapies

- 4.3.4 Supply-Chain Risk For Natural Allergen Extracts

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Allergy Type

- 5.1.1 Eye Allergy

- 5.1.2 Rhinitis

- 5.1.3 Asthma

- 5.1.4 Skin Allergy

- 5.1.5 Food Allergy

- 5.1.6 Other Allergies

- 5.2 By Treatment

- 5.2.1 Anti-Allergy Drugs

- 5.2.1.1 Antihistamines - 1st Gen

- 5.2.1.2 Antihistamines - 2nd/3rd Gen

- 5.2.1.3 Corticosteroids - Topical, Inhaled, Systemic

- 5.2.1.4 Decongestants - Oral, Nasal Spray

- 5.2.1.5 Leukotriene Receptor Antagonists

- 5.2.1.6 Biologics & mAbs

- 5.2.2 Immunotherapy

- 5.2.2.1 Sub-cutaneous (SCIT)

- 5.2.2.2 Sub-lingual (SLIT - Tablets, Drops)

- 5.2.1 Anti-Allergy Drugs

- 5.3 By Dosage Form

- 5.3.1 Tablets & Capsules

- 5.3.2 Nasal Sprays

- 5.3.3 Eye Drops

- 5.3.4 Inhalers

- 5.3.5 Injectables & Auto-injectors

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies & Drug Stores

- 5.4.3 Online Pharmacies

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 ALK-Abello A/S

- 6.3.2 AbbVie Inc.

- 6.3.3 Allergy Therapeutics plc

- 6.3.4 Bausch Health Companies Inc.

- 6.3.5 Alembic Pharmaceuticals Ltd.

- 6.3.6 F. Hoffmann-La Roche Ltd.

- 6.3.7 Nicox SA

- 6.3.8 GSK plc

- 6.3.9 Johnson & Johnson

- 6.3.10 Laboratorios Leti S.A.

- 6.3.11 Novartis AG

- 6.3.12 Sanofi SA

- 6.3.13 Teva Pharmaceutical Industries

- 6.3.14 Merck KGaA

- 6.3.15 Stallergenes Greer

- 6.3.16 Cipla Ltd.

- 6.3.17 AstraZeneca plc

- 6.3.18 Pfizer Inc.

- 6.3.19 Regeneron Pharmaceuticals

- 6.3.20 Bayer AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment