|

시장보고서

상품코드

1851876

엘라스토그래피 이미징 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Elastography Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

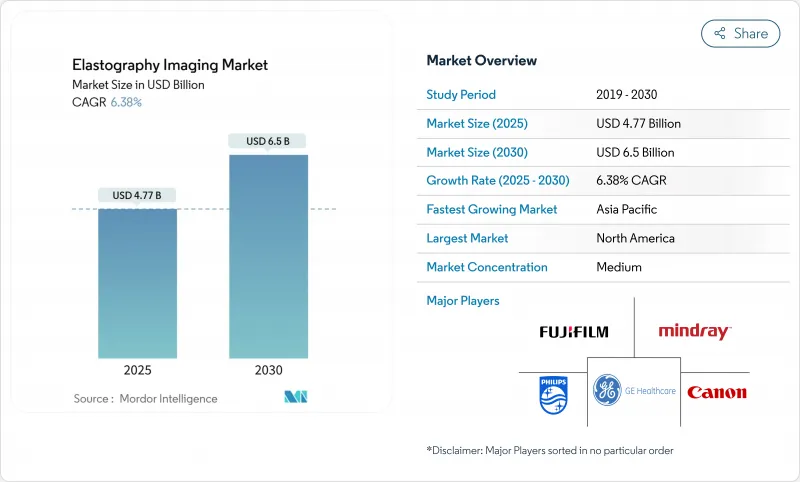

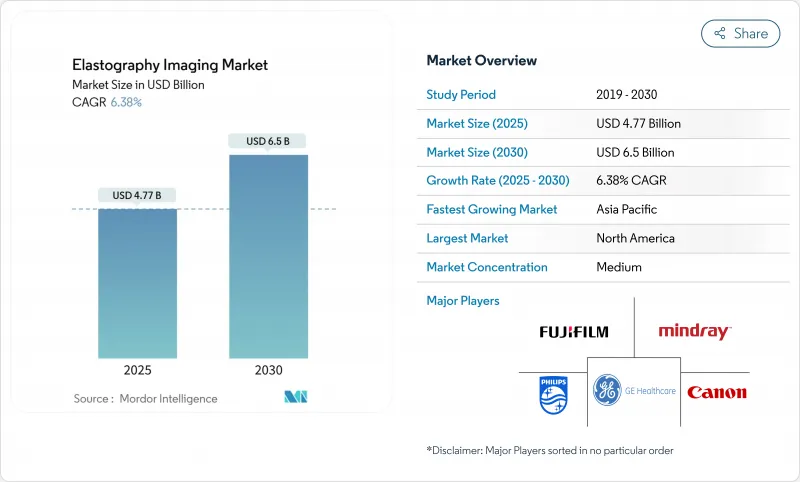

엘라스토그래피 이미징 시장의 2025년 시장 규모는 47억 7,000만 달러로, 2030년에는 65억 달러에 이르고, CAGR 6.38%를 나타낼 것으로 예측되고 있습니다.

비알코올성 지방간염(NASH) 병기 분류의 임상적 검증 증가, 심혈관 및 종양학적 이용 사례 증가, POC(Point-of-Care) 초음파 플랫폼의 왕성한 수요가 성장 궤도를 형성하고 있습니다. 인공지능을 이용한 자동화는 검사 시간이 75%나 단축되어 1차 케어 환경에서의 오퍼레이터 의존의 장벽을 완화합니다. 4,000달러 이하의 가격의 핸드헬드 시아파 프로브가 상업화되어 특히 아시아태평양의 자원이 제한된 시설에서의 접근이 확대되고 있습니다. GE 건강 관리를 통한 Intelligent Ultrasound 인수 등 임상 AI에 중점을 둔 M&A는 하드웨어에서 소프트웨어 주도의 차별화로 축 발을 옮기고 있음을 보여줍니다. 엘라스토그래피 CPT 코드에 대한 불리한 상환 방침과 고주파 피에조 진동자공급 체인 부족이 당면의 발판이 됩니다.

세계의 엘라스토그래피 이미징 시장 동향과 인사이트

만성 질환과 유방암의 이환율 상승

대사 기능 장애와 관련된 지방간 유병률 증가는 일상적인 간경도 측정의 채택을 촉진하고, 2차원 전단파 엘라스토그래피는 14.4kPa의 컷오프 값으로 94%의 정확도를 달성합니다. 초음파 가이드 하에서 감쇠 파라미터와 전단파 데이터를 결합하여 MASLD 환자를 생명을 위협하는 이벤트 위험별로 계층화할 수 있습니다. 유방 엘라스토그래피는 현재 유방 밀도가 높은 경우의 스크리닝을 지원하고 있으며, 62kPa의 임계치로 88%의 감도와 86.7%의 특이도로 악성 미소 석회화를 구별하고 있습니다. 종양과에서의 채용이 증가하고 방사선 치료실에서의 장치 이용이 촉진되고 있습니다. 엘라스토그래피는 생검을 대체하는 비침습적인 검사 방법으로 지지됩니다.

낮은 침습 수술로 이동

전단파 엘라스토그래피는 수리 전에 힘줄 힘줄의 질을 예측하여 외과 의사가 수술 전략을 보다 정확하게 조정할 수 있도록 합니다. 로봇 시스템은 3D ARFI 이미징을 통합하여 다중 파라메트릭 MRI에 필적하는 일치 수준에서 전립선 수술을 안내합니다. AI 확장 엘라스토그래피는 생검 대상을 자동으로 핀 포인트로 식별하여 샘플링 오류와 절차 시간을 단축합니다. 홀로직에 의한 소나타 인수(3억 5,000만 달러)와 같은 전략적인수는 초음파 가이드 하자궁 근종 특이적 저침습 플랫폼의 상업적 매력을 강조합니다. 이 기술의 수술 중 역할은 간에서 근골격계, 부인과 부위로 퍼집니다.

불리한 상환의 틀

메디케어는 CPT76981/76982의 적용 범위를 정의된 만성 간 질환에서 진행된 간 섬유증으로 제한하며, 보다 광범위한 스크리닝 용도를 제한합니다. Aetna는 엘라스토그래피를 간 이외의 용도에서는 임상시험약으로 간주하고 심장병학과 근골격계의 상환을 늦추고 있습니다. 사전 승인 장애물은 관리주기를 늘리고 정기적인 주문을 억제합니다. 심장 엘라스토그래피에 대한 표준 지불이 없기 때문에 지침 승인이 지연되었습니다. 증거 기반 보험 적용 확대가 기대되는 것은 대규모 결과 연구로 비용 절감이 입증된 후입니다.

부문 분석

초음파 엘라스토그래피는 2024년에 62.75%의 매출을 획득했는데, 이는 우수한 워크플로우 통합과 MR 플랫폼에 비해 저비용을 반영하고 있습니다. 이 점유율은 2024년 엘라스토그래피 이미징 시장 규모의 28억 3,000만 달러에 해당합니다. MR 엘라스토그래피는 CAGR 7.35%로 진보하여 섬유증의 병기 분류에 있어서 최고 수준의 정확도에 지지되고 있지만, 도입 비용이 높기 때문에 제3차 의료기관에 한정되어 있습니다. 지속적인 연구개발은 비평면 모니터링을 위한 컨포머블 초음파 일렉트로닉스를 제공하는 반면, AI의 자동화는 오퍼레이터의 스킬 레벨을 넘는 재현성을 향상시킵니다.

MR 엘라스토그래피의 정밀도는 복잡한 간질환 진료에 대한 수요를 지지하고 있지만, 자본 장벽이 있기 때문에 초음파 검사로 일상적인 후속을 실시하고 MR 검사는 불명확한 사례에만 사용한다는 하이브리드 구입 전략에 박차를 가하고 있습니다. 장비 공급업체는 MR 스캔 시간을 줄이고 검사당 비용을 줄이기 위해 AI 재구성을 통합합니다. 임상적인 골드 표준의 지위와 경제적 현실 사이의 균형은 장기적인 모달리티 믹스를 형성합니다.

전단파법은 2024년 매출의 45.71%를 차지하며, 그 양적 우위성과 오퍼레이터의 바이어스의 낮음을 강조했습니다. 변형 엘라스토그래피의 CAGR이 7.81%인 것은 기존 스캐너를 최소한의 비용으로 변환하는 소프트웨어의 업그레이드에 의한 것으로, 이것은 지역 병원에서 설득력 있는 가치 제안입니다. 시어 웨이브의 엘라스토그래피 이미징 시장 점유율은 간 섬유증과 갑상선 결절의 평가에 대한 지침의지지에 의해 강화되었습니다.

일시적 엘라스토그래피는 NASH 모니터링에서 틈새 위치를 차지하며, ARFI는 바늘 배치 중에 실시간 경도 단서를 제공함으로써 인터벤셔널 라디올로지에 이익을 제공합니다. 시어 웨이브와 ARFI를 융합시킨 하이브리드 솔루션이 종양학의 절차 지침을 만족시키기 위해 출현하고 있습니다. 머신러닝 기반 경도 추정을 통한 진단 성능 향상은 기술 유형 간의 경계를 모호하게 유지합니다.

지역 분석

북미가 2024년에 41.25%의 점유율로 매출을 독점했습니다. 간 엘라스토그래피에 대한 호의적인 상환과 신속한 AI 소프트웨어 클리어런스는 수용적인 규제 환경을 형성합니다. 미국에서는 NASH 치료제 개발에 있어서 엘라스토그래피의 엔드포인트를 측정하는 다시설 시험이 개시되어 간 전문의 수요를 지지하고 있습니다.

유럽에서는 국가의 의료 제도가 비용 효과를 중시하고 있기 때문에 안정적인 보급을 유지하고 있습니다. 휴대용 장비는 지역 병원의 총 소유 비용이 낮습니다. 이 지역의 영상 진단 학회는 통일된 프로토콜을 공표하고 있어, 각국간의 비교가능성과 벤더의 중립성을 높이고 있습니다.

아시아태평양의 CAGR은 8.52%로 의료 지출 확대, 당뇨 인구 증가, 저렴한 초음파 칩의 국내 제조가 뒷받침되고 있습니다. 중국의 NMPA는 2024년에 최신 Class III 이미징 가이드라인을 발행해 국내 제품 등록을 가속화하고 국내 경쟁에 박차를 가했습니다. 인도의 POC(Point-of-Care) 프로그램에서는 1차 케어에서 지방간 질환의 스크리닝에 핸드 헬드 엘라스토그래피를 도입하고 있습니다.

중동 및 아프리카에서는 고급 진단 서비스에 투자하는 민간 병원 그룹의 채용이 증가하고 있습니다. 남미에서는 특히 브라질과 아르헨티나에서 공중 보건 캠페인이 비 침습적 간경변 검출을 강조하고 꾸준한 성장을 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성질환과 유방암 증가

- 저침습 수술로의 변화

- 내쉬 관련 간 섬유증의 병기 분류에 있어서 엘라스토그래피 채용

- Ai 대응 POC(Point-of-Care) 초음파 엘라스토그래피

- 로봇 지원 엘라스토그래피 생검 플랫폼

- 핸드헬드 전단파 프로브의 상업 전개

- 시장 성장 억제요인

- 불리한 상환의 틀

- MRI 기반 시스템의 높은 자본 비용

- 재현성을 제한하는 오퍼레이터 의존성

- 고주파 압전 진동자공급 체인 부족

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 모달리티별

- 초음파 엘라스토그래피

- 자기공명 엘라스토그래피

- 기술 유형별

- 변형 엘라스토그래피

- 전단파 엘라스토그래피

- 과도 엘라스토그래피

- 음향 방사력 임펄스(ARFI)

- 이미징 기술별

- 2D 이미징

- 3D/4D 이미징

- 휴대성별

- 카트/트롤리 기반 시스템

- 휴대용/핸드헬드 시스템

- 용도별

- 방사선학

- 심장학

- 비뇨기과학

- 혈관

- 산부인과

- 정형외과 및 근골격계

- 류마티스학

- 물리치료 및 재활의학

- 최종 사용자별

- 병원

- 외래 수술 센터(ASC)

- 진단 영상 센터

- 전문 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Canon Medical Systems Corporation

- Esaote SpA

- Fujifilm Holdings Corporation

- GE HealthCare

- Supersonic Imagine

- Hologic Inc.

- Koninklijke Philips NV

- Mindray Medical International Ltd.

- Resoundant Inc.

- Samsung Medison Co. Ltd.

- Siemens Healthineers AG

- Hitachi Ltd.

- Butterfly Network Inc.

- Clarius Mobile Health Corp.

- Echosens SA

- BK Medical ApS

- Terason Corporation

- Verasonics Inc.

- Shenzhen Wisonic Medical Tech.

- Alpinion Medical Systems

- Ultrasonix Medical Corp.

제7장 시장 기회와 향후 전망

KTH 25.11.17The elastography imaging market is valued at USD 4.77 billion in 2025 and is forecast to reach USD 6.50 billion by 2030, expanding at a 6.38% CAGR.

Growing clinical validation for non-alcoholic steatohepatitis (NASH) staging, rising cardiovascular and oncological use-cases, and strong demand for point-of-care ultrasound platforms are shaping growth trajectories. Artificial-intelligence-enabled automation shortens exam times by as much as 75%, easing the operator-dependency barrier in primary-care settings. Commercially viable handheld shear-wave probes priced below USD 4,000 are widening access in resource-limited facilities, especially across Asia-Pacific. M&A activity focused on clinical AI-such as GE HealthCare's purchase of Intelligent Ultrasound-signals a pivot from hardware to software-led differentiation. Unfavorable reimbursement policies for elastography CPT codes and supply-chain shortages of high-frequency piezo crystals remain near-term restraints.

Global Elastography Imaging Market Trends and Insights

Rising incidence of chronic diseases & breast cancer

Escalating metabolic-dysfunction-associated steatotic liver disease prevalence drives routine liver stiffness measurement adoption, where two-dimensional shear-wave elastography achieves 94% accuracy at a 14.4 kPa cutoff . Combining ultrasound-guided attenuation parameters with shear-wave data stratifies MASLD patients by life-threatening event risk. Breast elastography now supports dense-breast screening, distinguishing malignant microcalcifications with 88% sensitivity and 86.7% specificity at a 62 kPa threshold. Growing oncology adoption bolsters equipment utilization in radiology suites. The dual-organ demand profile solidifies elastography as a preferred non-invasive alternative to biopsy.

Shift toward minimally invasive surgeries

Shear-wave elastography predicts rotator-cuff tendon quality before repair, enabling surgeons to tailor operative strategy more accurately. Robotic systems incorporate 3-D ARFI imaging to guide prostate procedures with agreement levels comparable to multiparametric MRI. AI-enhanced elastography automatically pinpoints biopsy targets, lowering sampling errors and procedure times. Strategic acquisitions, such as Hologic's USD 350 million Sonata buy-out, highlight the commercial appeal of ultrasound-guided, fibroid-specific minimally invasive platforms. The technology's intraoperative role is widening from liver to musculoskeletal and gynecological interventions.

Unfavorable reimbursement frameworks

Medicare restricts CPT 76981/76982 coverage to advanced hepatic fibrosis in defined chronic liver diseases, limiting broader screening uses. Aetna deems elastography investigational outside liver applications, stalling cardiology and musculoskeletal reimbursement. Prior-authorization hurdles lengthen administrative cycles and discourage routine ordering. The absence of standardized payment for cardiac elastography delays guideline endorsements. Evidence-based coverage expansions are expected only after large-scale outcome studies demonstrate cost savings.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of elastography for NASH-related fibrosis staging

- AI-enabled point-of-care ultrasound elastography

- High capital cost of MRI-based systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ultrasound elastography captured 62.75% revenue in 2024, reflecting superior workflow integration and lower cost relative to MR platforms. That share equates to USD 2.83 billion of the elastography imaging market size in 2024. MR elastography advances at a 7.35% CAGR, underpinned by gold-standard accuracy for fibrosis staging, but uptake is limited to tertiary centers due to high acquisition costs. Continuous R&D delivers conformable ultrasound electronics for non-planar monitoring, while AI automation enhances repeatability across operator skill levels.

MR elastography's precision sustains demand in complex hepatology practices, yet capital barriers spur hybrid purchasing strategies where ultrasound handles routine follow-up and MR is reserved for equivocal cases. Equipment vendors integrate AI reconstruction to shorten MR scan times and reduce per-exam cost. The balancing act between clinical gold-standard status and economic realities shapes long-term modality mix.

Shear-wave techniques represented 45.71% of 2024 sales, underlining their quantitative advantage and lower operator bias. Strain elastography's 7.81% CAGR owes to software upgrades that convert existing scanners at minimal cost-a value proposition compelling in community hospitals. The elastography imaging market share leadership of shear-wave is reinforced by guideline endorsements for liver fibrosis and thyroid nodule assessment.

Transient elastography holds a niche in NASH monitoring, whereas ARFI benefits interventional radiology by providing real-time stiffness cues during needle placement. Hybrid solutions that fuse shear-wave with ARFI emerge to satisfy oncology procedural guidance. Diagnostic performance gains from machine-learning-based stiffness estimation continue to blur boundaries among technology types.

The Elastography Imaging Market Report is Segmented by Modality (Ultrasound Elastography, and More), Technology Type (Strain Elastography, and More), Imaging Technique (2-D Imaging, 3-D/4-D Imaging), Portability (Trolley-Based Systems, Portable Systems), Application (Radiology, and More), End-User (Hospitals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America dominated revenue with a 41.25% share in 2024. Favorable reimbursement for liver elastography and rapid AI software clearance create a receptive regulatory environment. The United States initiated multi-center trials measuring elastography endpoints in NASH drug development, anchoring demand among hepatologists.

Europe maintains stable adoption as national health systems emphasize cost-effectiveness; portable devices offer lower total cost of ownership for district hospitals. The region's imaging societies publish harmonized protocols, improving cross-country comparability and vendor neutrality.

Asia-Pacific delivers an 8.52% CAGR, fueled by expanding healthcare spending, large diabetic populations, and domestic manufacturing of affordable ultrasound chips. China's NMPA issued updated Class III imaging guidelines in 2024, expediting domestic product registrations and spurring local competition. India's point-of-care programs incorporate handheld elastography to screen fatty-liver disease in primary care.

The Middle East and Africa witness incremental adoption through private hospital groups investing in premium diagnostic services. South America shows steady growth as public health campaigns emphasize non-invasive cirrhosis detection, particularly in Brazil and Argentina.

- Canon

- Esaote

- FUJIFILM

- GE Healthcare

- Supersonic Imagine

- Hologic

- Koninklijke Philips

- Mindray

- Resoundant Inc.

- Samsung Medison Co. Ltd.

- Siemens Healthineers

- Hitachi

- Butterfly Network Inc.

- Clarius Mobile Health Corp.

- Echosens SA

- BK Medical ApS

- Terason Corporation

- Verasonics Inc.

- Shenzhen Wisonic Medical Tech.

- Alpinion Medical Systems

- Ultrasonix Medical Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence Of Chronic Diseases & Breast Cancer

- 4.2.2 Shift Toward Minimally-Invasive Surgeries

- 4.2.3 Adoption Of Elastography For Nash-Related Liver Fibrosis Staging

- 4.2.4 Ai-Enabled Point-Of-Care Ultrasound Elastography

- 4.2.5 Robotic-Assisted Elastography-Guided Biopsy Platforms

- 4.2.6 Commercial Rollout Of Handheld Shear-Wave Probes

- 4.3 Market Restraints

- 4.3.1 Unfavorable Reimbursement Frameworks

- 4.3.2 High Capital Cost Of MRI-Based Systems

- 4.3.3 Operator-Dependence Limiting Reproducibility

- 4.3.4 Supply-Chain Shortage Of High-Frequency Piezo Crystals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Modality

- 5.1.1 Ultrasound Elastography

- 5.1.2 Magnetic Resonance Elastography

- 5.2 By Technology Type

- 5.2.1 Strain Elastography

- 5.2.2 Shear-Wave Elastography

- 5.2.3 Transient Elastography

- 5.2.4 Acoustic Radiation Force Impulse (ARFI)

- 5.3 By Imaging Technique

- 5.3.1 2-D Imaging

- 5.3.2 3-D / 4-D Imaging

- 5.4 By Portability

- 5.4.1 Cart / Trolley-based Systems

- 5.4.2 Portable / Handheld Systems

- 5.5 By Application

- 5.5.1 Radiology

- 5.5.2 Cardiology

- 5.5.3 Urology

- 5.5.4 Vascular

- 5.5.5 Obstetrics & Gynecology

- 5.5.6 Orthopedic & Musculoskeletal

- 5.5.7 Rheumatology

- 5.5.8 Physical Medicine & Rehabilitation

- 5.6 By End-User

- 5.6.1 Hospitals

- 5.6.2 Ambulatory Surgical Centers

- 5.6.3 Diagnostic Imaging Centers

- 5.6.4 Specialty Clinics

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East & Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Canon Medical Systems Corporation

- 6.3.2 Esaote SpA

- 6.3.3 Fujifilm Holdings Corporation

- 6.3.4 GE HealthCare

- 6.3.5 Supersonic Imagine

- 6.3.6 Hologic Inc.

- 6.3.7 Koninklijke Philips N.V.

- 6.3.8 Mindray Medical International Ltd.

- 6.3.9 Resoundant Inc.

- 6.3.10 Samsung Medison Co. Ltd.

- 6.3.11 Siemens Healthineers AG

- 6.3.12 Hitachi Ltd.

- 6.3.13 Butterfly Network Inc.

- 6.3.14 Clarius Mobile Health Corp.

- 6.3.15 Echosens SA

- 6.3.16 BK Medical ApS

- 6.3.17 Terason Corporation

- 6.3.18 Verasonics Inc.

- 6.3.19 Shenzhen Wisonic Medical Tech.

- 6.3.20 Alpinion Medical Systems

- 6.3.21 Ultrasonix Medical Corp.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment