|

시장보고서

상품코드

1851899

플렉소 인쇄기 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Flexographic Printing Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

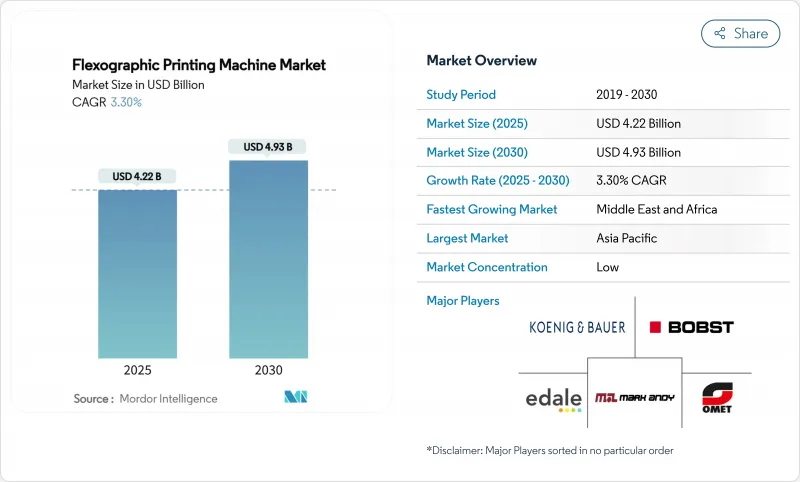

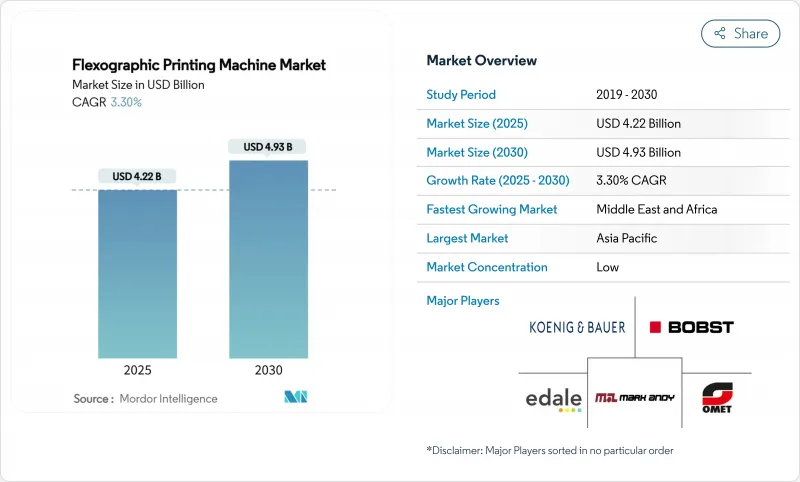

플렉소 인쇄기 시장 규모는 2025년에 42억 2,000만 달러로 추정되고, 2030년에는 49억 3,000만 달러에 이를 전망이며, CAGR 3.3%로 안정될 것으로 예측됩니다.

현재 투자 우선순위는 단순한 생산능력 확대보다는 자동화, 하이브리드 인쇄 기능, 엄격한 지속가능성 규칙에 대한 대응에 집중하고 있습니다. 전자상거래 관련 소량 인쇄, 수성 잉크 의무화, 디지털 트윈 유지보수 플랫폼은 컨버터 전체의 조달 기준을 재구성하고 있습니다. 고속 전환과 낮은 VOC 성능을 양립시키는 공급업체가 점유율을 확대하는 한편, 중국의 2026년 '그린 프레스' 정책으로 대표되는 지역의 보조금 제도가 경쟁 지도를 바꾸고 있습니다. 동시에 XSYS-MacDermid와 INX-C&A와 같은 합병은 제판과 잉크 전문가가 리드 타임을 단축하고 PFAS 규정을 극복하기 위해 어떻게 통합하는지를 보여줍니다.

세계의 플렉소 인쇄기 시장 동향 및 인사이트

비용 효율적인 소형 로트 패키징 능력

플렉소 인쇄기 제조업체는 설치 시간을 단축하고 수익성이 낮은 최소 로트를 5,000m에서 500m 가까이 단축했습니다. 사이클이 단축됨에 따라 계절 및 지역 한정 SKU가 있는 브랜드는 엄청난 비용 없이 맞춤형 그래픽을 전개할 수 있습니다. MacDermid사의 LUX ITP 플레이트는 기존의 2일에서 8시간에 플레이트룸을 나오게 되어 다음날의 아트 체인지를 목표로 하는 컨버터에 있어서 중요한 병목이 해소되었습니다. 보다 빠른 플레이트와 빠른 단계 교체로 플렉소 인쇄는 한 번 디지털 인쇄로 이동한 작업을 되찾을 수 있습니다. 따라서 컨버터는 속도와 유연성의 균형을 맞춘 미드레인지의 모듈형 라인에 투자하고 있으며, 플렉소 인쇄기 시장 전체의 설비 수요를 뒷받침하고 있습니다.

식품 등급의 지속 가능한 연포장 급증

유럽과 북미의 규제는 PFAS를 배제하는 한편, 완전한 재활용성을 요구하고 있습니다. 사이카플렉스는 2030년까지 100% 재활용 가능한 포트폴리오를 계획하고 있으며 5% PCR 함량으로 컨버터가 순환성을 입증해야 한다는 압력을 보여줍니다. INX사의 GelFlex EB 잉크는 라미네이션층을 제거하고 팩 총중량을 삭감하면서도 배리어성을 유지하고 있습니다(inxinternational.com). 컨버터가 EU의 2026년 8월 PFAS 캡까지 새로운 화학물질을 인증하려고 경쟁하는 가운데 수성 잉크와 EB 경화 잉크를 경쟁력 있는 속도로 가동할 수 있는 인쇄기에 대한 수요가 급증하고 플렉소 인쇄기 시장에 이익을 가져오고 있습니다.

설비 투자 집중형 다색 CI 인쇄기

풀 옵션 1,300mm CI 라인은 모듈형 대체 기계를 훨씬 초과하는 400만 달러로 거래됩니다. 그 결과 세계 기업조차도 2024년 주문을 연기했으며 Bobst의 CI 예약은 24% 감소했습니다. 중견 시장의 컨버터는 평균 가동량이 감소할 때 프리미엄 인쇄기에 자금을 제공하는 것을 주저하고 플렉소 인쇄기 시장의 갱신 주기를 늦추고 있습니다.

부문 분석

종이 및 판지는 2024년에 45.56%의 점유율로 플렉소 인쇄기 시장을 선도했으며, 소매 및 전자상거래용 카톤이나 재생 크래프트 라이너가 견인했습니다. 컨버터는 브랜드 규제를 충족시키기 위해 종이의 용이한 재활용성을 의지하고 있으며, 한편으로는 코팅의 개량에 의해 상온 식품의 보존 기간이 연장되고 있습니다. 그러나 플라스틱 필름은 단일 소재의 라미네이트와 PCR 블렌드가 순환성과 배리어의 요구를 해결하고 있기 때문에 CAGR 가장 빠른 6.57%로 성장을 지속하고, 있습니다.

INX의 EB 잉크에 의해 필름 구조로부터 라미네이트층을 제거하는 것이 가능하게 되어, 배리어성을 손상시키지 않고 게이지를 삭감할 수 있게 되었기 때문에 대체품의 쟁탈전이 격화하고 있습니다. UFlex 이집트의 새로운 PET 수지 생산 능력은 공급망 단축을 위한 세계적인 수지 자급의 움직임을 반영합니다. 전반적으로, 제지 컨버터는 콜게이터의 함대를 확대하고, 필름 제조업체는 하이 배리어 파우치를 추구하고, 기재별 인쇄기의 플렉소 인쇄기 시장 규모 전체에서 설비 수요를 지지하고 있습니다.

인라인 및 모듈 시스템은 2024년에 39.34%의 판매 점유율을 차지했으며, 프라이빗 브랜드 식품과 인디 화장품에 선호되는 적당한 취득 비용과 경쾌한 잡 체인지의 특징입니다. 중앙 압통 인쇄기는 자본 부담이 큰 것, CAGR 5.45%에서 가장 급속하게 성장하고 있으며, 수축 슬리브와 와이드 웹 스낵에서의 색과 색의 맞추기를 엄밀히 실시하는 브랜드의 요구에 추진되고 있습니다.

하이브리드 디자인은 이전 테두리를 모호하게 만듭니다. : Uteco의 OnyxOMNIA는 8색 플렉소 데크에 잉크젯 헤드를 스티치하여 가변 데이터를 허용하면서 400m/분을 실현합니다. CI OEM이 자동판 몸통과 디지털 트윈 진단을 전개함에 따라 24/6 시프트 컨버터는 고급화되어 플렉소 인쇄기 시장을 더 높은 사양의 플랫폼으로 견인하고 있습니다.

플렉소 인쇄기 시장은 소재별(종이 및 판지, 플라스틱 필름, 골판지 등), 프레스 유형별(중앙 압통(CI), 스택, 인라인 및 모듈), 최종 사용자 산업별(식음료, 의약품 및 헬스케어 등), 자동화 레벨별(기존, 스마트 및 IoT 대응), 지역별로 분류되어 있습니다. 시장 규모 및 예측은 금액(달러)으로 제공됩니다.

지역 분석

아시아태평양은 2024년 세계 매출의 40.56%를 차지했으며, 중국의 생산 능력 확장과 보조금 주도의 설비 갱신에 의해 '그린, 인텔리전트' 기준을 충족하는 CI 프레스가 지지되고 있습니다. 일본은 인건비가 높기 때문에 로봇에 의한 자재 관리의 채용이 가속화되고, 한국과 ASEAN의 컨버터는 지역의 간식이나 퍼스널케어 브랜드에 대응하기 위해서 연포장 라인에 투자합니다.

중동 및 아프리카는 CAGR 6.14%에서 가장 빠르게 성장하는 지역입니다. 인구 증가, 콜드체인 개선, FMCG 보급률 상승 등 새로운 연포장 공장에 박차를 가해 현지 수지 공급을 지원하는 이집트 UFlex의 PET 칩 시설과 같은 투자를 끌어들이고 있습니다. 걸프 국가들은 또한 순환 경제 목표를 달성하기 위해 수성 잉크를 개조하기 위해 시험적으로 실시했습니다.

북미와 유럽은 성숙하고 있는 반면, PFAS와 VOC 규제가 강화되는 가운데, 기술적인 페이스메이커로 계속하고 있습니다. EU는 2026년 8월에 25ppb의 PFAS 규제를 시행했으며, 컨버터는 배리어 코팅의 오버홀을 강요하고 있습니다. 북미의 인쇄회사는 주 수준의 솔벤트 규제에 의한 유사한 압력에 직면하고 있으며, 밀폐형 닥터 블레이드 시스템과 히트셋 에어 매니지먼트로의 업그레이드를 촉구하고 있습니다. 그 결과, 이들 지역에서는 매크로의 수량 성장이 둔화되고 있음에도 불구하고, 교체 수요가 플렉소 인쇄기 시장의 활력을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 비용 효율적인 소형 로트 포장 능력

- 식품 등급의 지속 가능한 연포장의 급증

- 전자상거래 완충액에서 골판지 생산 능력의 급속한 확대

- 북미와 EU에서 수성 저 VOC 잉크의 의무화

- 컨버팅 라인의 디지털 트윈과 AI에 의한 예지 보전 채용

- 중국 2026년 CI플렉소 설비에 그린 프레스 보조금

- 시장 성장 억제요인

- 설비 투자 집중형 다색 CI 인쇄기

- 유럽과 일본에서 숙련 프레스 오퍼레이터 부족

- 초단기 생산에 있어서 제판 리드 타임의 병목

- 배리어 코팅 적합성에 관한 PFAS 규제 강화

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 소재별

- 종이 및 판지

- 플라스틱 필름

- 금속 필름 및 박

- 골판지

- 기타 소재(바이오플라스틱, 라미네이트)

- 프레스 유형별

- 중앙 노출수(CI)

- 스택

- 인라인 및 모듈러

- 최종 사용자 업계별

- 식품 및 음료

- 의약품 및 헬스케어

- 퍼스널케어 및 화장품

- 소비자용 전자기기

- 물류 및 전자상거래

- 기타 최종 사용자 산업

- 자동화 레벨별

- 기존

- 스마트 및 IoT 대응

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 이탈리아

- 영국

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 케냐

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Bobst Group SA

- Windmoller and Holscher KG

- Koenig and Bauer AG

- Mark Andy Inc.

- Uteco Group

- Heidelberger Druckmaschinen AG

- OMET Srl

- MPS Systems BV

- Nilpeter A/S

- Gallus Ferd. Ruesch AG

- Soma Engineering

- PCMC(Barry-Wehmiller)

- Star Flex International

- Orient Sogyo Co. Ltd.

- Taiyo Kikai Ltd.

- Comexi Group

- Rotatek SA

- Wolverine Flexographic LLC

- Zhejiang Weigang Machinery

- Edale Ltd.

제7장 시장 기회 및 향후 전망

AJY 25.11.19The flexographic printing machine market size stands at USD 4.22 billion in 2025 and is on track to reach USD 4.93 billion by 2030, reflecting a steady 3.3% CAGR.

Investment priorities now revolve around automation, hybrid press capabilities, and compliance with tightening sustainability rules rather than simple capacity expansion. E-commerce-related short runs, water-based ink mandates, and digital-twin maintenance platforms are reshaping procurement criteria across converters. Suppliers that marry fast changeovers with low-VOC performance are gaining share, while regional subsidy programs, most notably China's 2026 "Green Press" policy, are altering the competitive map. At the same time, mergers such as XSYS-MacDermid and INX-C&A illustrate how plate-making and ink specialists are consolidating to cut lead times and navigate PFAS restrictions.

Global Flexographic Printing Machine Market Trends and Insights

Cost-effective short-run packaging capability

Flexographic press builders have slashed setup times, taking profitable minimum runs from 5,000 m to close to 500 m. Shorter cycles mean brands with seasonal or regional SKUs can deploy custom graphics without prohibitive costs. MacDermid's LUX ITP plates now leave the plate room in eight hours, down from two days, which removes a key bottleneck for converters targeting next-day art changes. Together, faster plates and rapid changeovers allow flexography to reclaim work that once defaulted to digital presses. Converters are therefore investing in mid-range modular lines that balance speed with flexibility, underpinning equipment demand across the flexographic printing machine market.

Surge in food-grade sustainable flexible packaging

European and North American regulations are eliminating PFAS while demanding full recyclability. Saica Flex plans a 100% recyclable portfolio by 2030 with 5% PCR content, showcasing the pressure on converters to prove circularity. INX's GelFlex EB inks remove lamination layers, cutting total pack weight yet maintaining barrier integrity inxinternational.com. Inline barrier-coating partnerships, such as Solenis-Heidelberg, further reduce secondary processes. As converters race to certify new chemistries before the EU's August 2026 PFAS cap, demand crescendos for presses that can run water-based or EB curing inks at competitive speeds benefiting the flexographic printing machine market.

Cap-ex intensive multi-color CI presses

A fully optioned 1,300 mm CI line can command USD 4 million, well above modular alternatives. As a result, even global accounts deferred orders in 2024, cutting Bobst CI bookings by 24%. Mid-market converters hesitate to finance premium presses when average run lengths are shrinking, slowing replacement cycles in the flexographic printing machine market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid corrugated capacity additions in e-commerce fulfillment

- Mandates on water-based low-VOC inks

- Skilled press-operator shortage in Europe and Japan

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper and paperboard led the flexographic printing machine market with 45.56% share in 2024, buoyed by retail e-commerce cartons and recycled kraft liners. Converters rely on paper's easy recyclability to satisfy brand mandates, while improved coatings are extending shelf life for ambient foods. Plastic films, however, chart the fastest 6.57% CAGR as mono-material laminates and PCR blends solve circularity and barrier needs.

The substitution battle intensifies as INX's EB inks allow film structures to drop a lamination layer, cutting gauge without compromising barrier. UFlex's new PET resin capacity in Egypt reflects global resin self-sufficiency moves to shorten supply chains. Overall, paper converters expand corrugator fleets, whereas film suppliers chase high-barrier pouches together sustaining equipment demand across the flexographic printing machine market size for substrate-specific presses.

In-line/modular systems held 39.34% revenue share in 2024 thanks to affordable acquisition costs and nimble job changes traits favored by private-label food and indie cosmetics. Central-impression presses, though capital-heavy, are gaining fastest at 5.45% CAGR, propelled by brand demands for tight color-to-color register on shrink sleeves and wide web snacks.

Hybrid designs blur former lines: Uteco's OnyxOMNIA stitches inkjet heads onto an eight-color flexo deck, delivering 400 m/min while enabling variable data . As CI OEMs roll out automatic plate cylinders and digital-twin diagnostics, converters with 24/6 shifts migrate upscale, driving the flexographic printing machine market toward higher-spec platforms.

Flexographic Printing Machine Market is Segmented by Material (Paper and Paperboard, Plastic Films, Corrugated Board, and More), Press Type (Central-Impression (CI), Stack, and In-Line / Modular), End-User Industry (Food and Beverage, Pharmaceutical and Healthcare, and More), Automation Level (Conventional, and Smart / IoT-Enabled), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 40.56% of global revenues in 2024, aided by China's capacity expansions and subsidy-driven equipment renewals that favor CI presses meeting "green, intelligent" criteria. Japan's high labor costs accelerate adoption of robotic material handling, while South Korean and ASEAN converters invest in flexible packaging lines to serve regional snack and personal-care brands.

Middle East & Africa is the fastest-growing territory at 6.14% CAGR. Population growth, cold-chain improvements, and rising FMCG penetration spur new flexible packaging plants, drawing investments like UFlex's PET chip facility in Egypt which anchors local resin supply. Gulf States are also piloting water-based ink retrofits to meet circular-economy targets.

North America and Europe, though mature, remain technology pacesetters as PFAS and VOC regulations tighten. The EU's 25 ppb PFAS ceiling effective August 2026 forces converters to overhaul barrier coatings. North American printers face similar pressure from state-level solvent rules, driving upgrades to enclosed-chamber doctor-blade systems and heat-set air management. Consequently, replacement demand keeps the flexographic printing machine market dynamic despite slower macro-volume growth in these regions.

- Bobst Group SA

- Windmoller and Holscher KG

- Koenig and Bauer AG

- Mark Andy Inc.

- Uteco Group

- Heidelberger Druckmaschinen AG

- OMET Srl

- MPS Systems BV

- Nilpeter A/S

- Gallus Ferd. Ruesch AG

- Soma Engineering

- PCMC (Barry-Wehmiller)

- Star Flex International

- Orient Sogyo Co. Ltd.

- Taiyo Kikai Ltd.

- Comexi Group

- Rotatek SA

- Wolverine Flexographic LLC

- Zhejiang Weigang Machinery

- Edale Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-effective short-run packaging capability

- 4.2.2 Surge in food-grade sustainable flexible packaging

- 4.2.3 Rapid corrugated capacity additions in e-commerce fulfilment

- 4.2.4 Mandates on water-based low-VOC inks in North America and EU

- 4.2.5 Converting-line digital twin and AI predictive-maintenance adoption

- 4.2.6 China 2026 Green Press subsidy for CI-flexo equipment

- 4.3 Market Restraints

- 4.3.1 Cap-ex intensive multi-colour CI presses

- 4.3.2 Skilled press-operator shortage in Europe and Japan

- 4.3.3 Plate-making lead-time bottlenecks for ultra-short runs

- 4.3.4 Tightening PFAS restrictions on barrier coating compatibility

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Paper and Paperboard

- 5.1.2 Plastic Films

- 5.1.3 Metallic Films and Foils

- 5.1.4 Corrugated Board

- 5.1.5 Others Material (Bioplastics, Laminates)

- 5.2 By Press Type

- 5.2.1 Central-Impression (CI)

- 5.2.2 Stack

- 5.2.3 In-Line / Modular

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Pharmaceutical and Healthcare

- 5.3.3 Personal-Care and Cosmetics

- 5.3.4 Consumer Electronics

- 5.3.5 Logistics and E-commerce

- 5.3.6 Other End-user Industry

- 5.4 By Automation Level

- 5.4.1 Conventional

- 5.4.2 Smart / IoT-Enabled

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 Italy

- 5.5.2.4 United Kingdom

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Kenya

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bobst Group SA

- 6.4.2 Windmoller and Holscher KG

- 6.4.3 Koenig and Bauer AG

- 6.4.4 Mark Andy Inc.

- 6.4.5 Uteco Group

- 6.4.6 Heidelberger Druckmaschinen AG

- 6.4.7 OMET Srl

- 6.4.8 MPS Systems BV

- 6.4.9 Nilpeter A/S

- 6.4.10 Gallus Ferd. Ruesch AG

- 6.4.11 Soma Engineering

- 6.4.12 PCMC (Barry-Wehmiller)

- 6.4.13 Star Flex International

- 6.4.14 Orient Sogyo Co. Ltd.

- 6.4.15 Taiyo Kikai Ltd.

- 6.4.16 Comexi Group

- 6.4.17 Rotatek SA

- 6.4.18 Wolverine Flexographic LLC

- 6.4.19 Zhejiang Weigang Machinery

- 6.4.20 Edale Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment