|

시장보고서

상품코드

1851902

고해상도 용융 분석 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)High-Resolution Melting Analysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

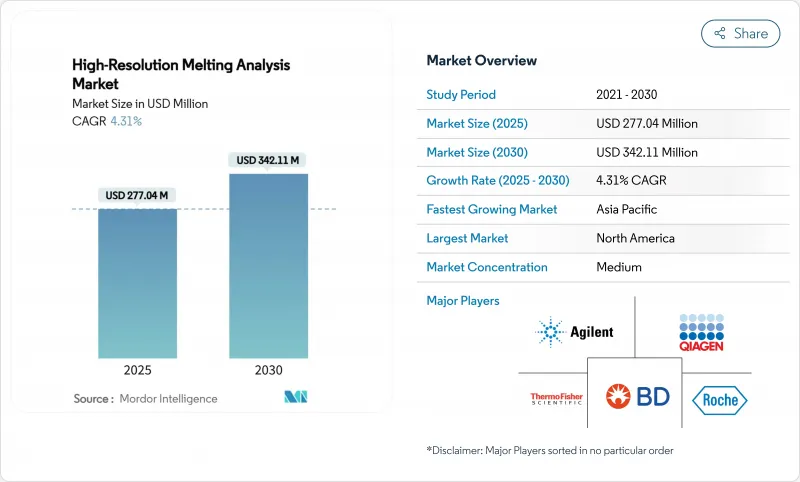

고해상도 용융 분석 시장 규모는 2025년에 2억 7,704만 달러, 2030년에는 3억 4,211만 달러로 성장하고, 2025-2030년의 CAGR은 4.31%를 나타낼 것으로 예측되고 있습니다.

정밀의료 프로그램의 강력한 섭취, 유전자 검사에 대한 폭넓은 상환, 차세대 시퀀싱에 대한 명확한 비용 우위성이 수요를 지원하고 있습니다. 확립된 분자진단 공급업체는 HRM, 디지털 PCR 및 클라우드 분석을 결합한 통합 플랫폼을 지속적으로 도입하고, 수작업 단계를 줄이고, 턴어라운드를 가속화하며, 검사당 비용을 낮추고 있습니다. 아시아태평양과 라틴아메리카에서는 감염증 감시 프로그램이 새로운 고처리량 이용 사례를 창출하고 있는 반면, 포인트 오브 케어의 이노베이터는 분자 검사 전문 지식이 없는 클리닉에 컴팩트한 기기를 보급하려고 하고 있습니다. 한편 임상실에서 노동력 부족은 자동화를 가속화하고 HRM은 이용하기 쉽고 비용 효율적인 유전자형 분석 작업자로서의 입지를 공고히 하고 있습니다.

세계 고해상도 용융 분석 시장 동향과 통찰

정밀의료 이니셔티브 채택 확대

Precision Medicin 프로그램은 현재 종양학에 그치지 않고 순환기학, 정신 의학, 만성 질환 관리에 이르기까지 신속한 유전자 약물 매칭 분석에 크게 의존하고 있습니다. 미국 Medicare & Medicaid 서비스 센터는 Pharma Cogenomics 검사의 보험 적용을 제안하여 HRM 플랫폼이 임상적으로 대처할 수 있는 변이체에 대한 상환을 보장할 수 있도록 했습니다. UnitedHealthcare와 같은 주요 지불 기관은 임상적 유용성이 입증되면 일관된 보험 적용을 인정하는 정책을 강화하기 시작했으며 HRM 시약 공급업체에게 안정적인 수입원이 되고 있습니다. 진단제 제조업체는 QIAGEN의 QIAstat-Dx를 동반진단제에 배포할 수 있는 바와 같이 1시간 이내에 제노타이핑 결과를 제공하는 카트리지 기반 워크플로우에 HRM 모듈을 통합하여 대응하고 있습니다. 검사 비용 절감, 신속한 납기 및 청구 명확화의 조합으로 병원 실험실은 일상적인 약물 반응 패널에서 상거래 시퀀싱을 대체하는 것을 추진하여 설치 기반을 확대하고 있습니다.

유전자 검사 상환 정책 확대

미국과 유럽의 지불자는 제한적이고 적응증에 특화된 규칙에서 분석 정확도와 임상적 유용성에 대한 보상 근거 기반 프레임워크로 전환하고 있습니다. American Journal of Managed Care 잡지가 110개의 의료보험제도를 추적 조사한 결과, 2023년부터 2025년에 걸쳐, 15개 이상의 작용가능한 약제와 유전자의 쌍을 커버하는 제도가 두배로 되는 것으로 나타났습니다. HRM 시스템은 시퀀싱의 몇 분의 한 가격으로 감도 임계값에 도달하기 때문에 대량 스크리닝에 적합합니다. 유럽 의료 기술 평가 네트워크(European Network for Health Technology Assessment) 하에서 EU 지급자의 협력은 국경을 넘는 상환 결정을 더욱 가속화하고 다국적 실험실에 통일된 전망을 부여하고 있습니다. 선도적인 플랫폼 공급업체는 HRM 시약에 보험자 대응 보고서를 자동으로 생성하는 클라우드 포털을 번들하여 소규모 지역 병원의 관리 오버헤드를 줄이고 이익을 얻고 있습니다.

HRM 장비에 필요한 고액 설비 투자

엔트리 레벨 HRM 플랫폼은 서비스 계약을 제외하고 60,000달러에서 120,000달러를 차지합니다. 2024년 한 조사에 따르면 미국 임상실의 29.1%가 기술자 확보가 어려울 것이라고 응답하고 있으며, 경영진은 장비 업그레이드를 늦추려고 합니다. 디지털 트윈 프로젝트는 가동률을 높이고 검사당 상각 비용을 낮추는 점에서 유망하지만, 워크플로 최적화 소프트웨어는 추가로 10-20만 달러가 추가되므로 총 투자액은 높아집니다. 임대 계약 등의 자금 조달 솔루션도 등장하고 있지만, 2024년 이후의 금리 인상에 의해 리스 비용이 상승하고, 이익률이 낮은 공립 병원에서의 도입은 제한되고 있습니다.

부문 분석

시약 및 소모품의 2024년 매출은 최대로 49.54%를 차지했습니다. 시약으로 인한 고해상도 용융 분석 시장 규모는 1억 3,740만 달러에 이르고, 이 범주는 분석 메뉴의 확대와 함께 한 자리 대 중반의 안정적인 성장을 유지할 것으로 예측됩니다. 검사기기의 매출은 CAGR 6.53%로 가속하고 있는데, 이는 다시설 전개하는 의료시스템이 검사기사의 시간을 단축하고 모든 시설에서 품질을 표준화하는 통합형 자동분석장치에 투자하고 있기 때문입니다. 제조업체는 현재 클라우드 라이선스와 검증된 분석을 장비에 번들로 제공하여 성과 기반 조달 모델을 따르는 종합적인 계약을 맺고 있습니다. 소프트웨어 및 서비스 매출은 여전히 전체의 10% 미만이지만, 성숙한 시장에서 가장 빠르게 증가하고 있으며, 거기에서 실험실은 24시간 365일 지원을 보장하는 벤더가 운영하는 플랫폼에 데이터 분석을 아웃소싱하고 있습니다.

지역 분석

북미는 2024년 세계 매출의 41.56%를 차지하며, 자금력 있는 레퍼런스 랩, 실용적인 유전자 약제 쌍을 커버하는 지불자 정책, 전국적인 서비스 계약을 제공하는 통합된 공급자 기반에 지지되고 있습니다. 이 지역 수요는 동반진단 시험의 활성화에도 뒷받침되고 있으며, 완전 자동화된 HRM 스위트를 갖춘 계약 연구 기관에 대량의 데이터가 흐르고 있습니다. 노동력 부족은 여전히 과제이며, 미국의 실험실 기술자의 결원률은 2024년에 46%를 넘어 네트워크는 사람의 개입을 최소화하는 워크 어웨이 워크플로우를 갖춘 장비의 채용을 촉구하고 있습니다.

아시아태평양은 가장 급성장하고 있는 지역으로, 2030년까지의 CAGR은 5.45%를 나타낼 전망이며, 국민 모두 보험 제도나, 호주의 5억 10만 달러의 Genomics Health Futures Mission과 같은 정부 출자의 유전체 이니셔티브에 추진되고 있습니다. 중국의 병원 조달 개혁은 비용 효율적인 국산 진단약을 우대하고 있으며 HRM 기기와 정부 승인 시약 메뉴를 번들한 현지 합작 사업을 뒷받침하고 있습니다. 인도와 필리핀은 배터리 팩에서 작동하는 카트리지 기반 HRM 검사를 모바일 POC 시험으로 도입하여 중앙 검사실이 없는 지역에서의 접근을 확대하고 있습니다.

유럽은 학술의료센터의 치밀한 네트워크와 약리유전체학를 지원하는 상환환경 덕분에 견고한 수요를 획득하고 있습니다. EU의 의료기기 규제는 시판 후 감시의 조화를 도모하고 있으며, 공급자가 범유럽적인 HRM 키트를 출시하는 데 도움이 됩니다. 독일과 프랑스 병원은 익명화된 용융 곡선 데이터를 국가의 바이오뱅크 리포지토리로 라우팅하는 클라우드 기반 분석을 통합하여 유전체의 발견과 치료 결과 간의 번역 연구를 가속화하고 있습니다.

중동, 아프리카와 남미는 총 매출액의 10% 미만이지만 감염 프로그램이 아웃브레이크 대응 지침으로 신속한 제노타이핑을 요구하고 있기 때문에 검사량은 두 자리 성장을 기록하고 있습니다. 2024년에 케냐에서 발생한 리프트 밸리 열에서는 HRM을 탑재한 이동 판매차가 도입되어 샘플 처리 시간이 5일에서 당일로 단축되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정밀 의학 이니셔티브의 채택 증가

- 유전자 검사 상환 정책의 확대

- 동반진단약 개발 파이프라인의 급증

- 유전체 감시 프로그램에 대한 정부 자금 증가

- 분산형 포인트 오브 케어 분자 검사의 보급

- 높은 처리량 워크플로우를 위한 클라우드 기반 애널리틱스 통합

- 시장 성장 억제요인

- HRM 기기에 필요한 고액 설비 투자

- 실험실 간의 분석 프로토콜의 표준화는 제한적

- 숙련된 분자 진단 인력 부족

- 신흥국의 규제 불확실성

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 및 서비스별

- 시약 및 소모품

- 인터칼레이트 염료

- 마스터 믹스

- DNA 스탠다드 & 컨트롤

- 기기

- 실시간 PCR 시스템

- 디지털 PCR 시스템(HRM 대응)

- 소형 POC 기기

- 소프트웨어 및 서비스

- 용융 곡선 분석 소프트웨어

- 클라우드 기반 애널리틱스 및 AI 서비스

- 밸리데이션 & 트레이닝 서비스

- 시약 및 소모품

- 용도별

- SNP 유전자형 분석

- 돌연변이 발견

- 병원체 특정

- 메틸화 분석

- 기타 용도

- 최종 사용자별

- 연구소·학술 기관

- 제약 및 바이오테크놀러지 기업

- 병원 및 진단센터

- 기타 최종 사용자

- 지리

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific Inc.

- Bio-Rad Laboratories Inc.

- Qiagen NV

- Agilent Technologies Inc.

- F. Hoffmann-La Roche AG

- Illumina Inc.

- Azura Genomics

- Canon Inc.

- bioMerieux SA

- Meridian Bioscience Inc.

- New England Biolabs

- Promega Corporation

- LGC Biosearch Technologies

- Takara Bio Inc.

- Cepheid(Danaher)

- Fluidigm Corporation

- Analytik Jena AG

- Pacific Biosciences of California Inc.

- Sysmex Corporation

제7장 시장 기회와 장래의 전망

SHW 25.11.25The high-resolution melting analysis market size stands at USD 277.04 million in 2025 and is forecast to grow to USD 342.11 million in 2030, advancing at a 4.31% CAGR over 2025-2030.

Strong uptake of precision-medicine programs, broader reimbursement for genetic tests, and a clear cost advantage over next-generation sequencing are sustaining demand. Established molecular-diagnostics suppliers keep introducing integrated platforms that combine HRM, digital PCR, and cloud analytics to cut manual steps, speed turnaround, and lower per-test cost. Infectious-disease surveillance programs in Asia-Pacific and Latin America are creating new, high-throughput use cases, while point-of-care innovators are pushing compact instruments into clinics that lack molecular-testing expertise. Meanwhile, labor shortages in clinical labs are accelerating automation, cementing HRM's position as an accessible, cost-effective genotyping workhorse.

Global High-Resolution Melting Analysis Market Trends and Insights

Growing Adoption of Precision Medicine Initiatives

Precision-medicine programs now stretch well beyond oncology into cardiology, psychiatry, and chronic-disease management, and they rely heavily on rapid gene-drug matching assays. The US Centers for Medicare & Medicaid Services proposed coverage for pharmacogenomic testing, enabling HRM platforms to secure reimbursement for clinically actionable variants. Leading payers such as UnitedHealthcare have started aligning policies that grant consistent coverage once clinical utility is proven, creating a stable revenue stream for HRM reagent vendors. Diagnostic manufacturers respond by embedding HRM modules into cartridge-based workflows that deliver genotyping results in under an hour, as illustrated by QIAGEN's QIAstat-Dx expansion into companion diagnostics. The combination of lower test cost, quicker turnaround, and billing clarity is driving hospital labs to replace Sanger sequencing in routine drug-response panels, thereby broadening the installed base.

Expansion of Genetic Testing Reimbursement Policies

Payers in the United States and Europe are shifting from restrictive, indication-specific rules toward evidence-based frameworks that reward analytical accuracy and clinical usefulness. An American Journal of Managed Care study tracking 110 health-plan policies showed that plans covering >=15 actionable drug-gene pairs doubled between 2023 and 2025. HRM systems gain because they reach sensitivity thresholds at a fraction of sequencing's price, which suits high-volume screening. EU payer cooperation under the European Network for Health Technology Assessment has further accelerated cross-border reimbursement decisions, giving multinational labs a uniform outlook. Large platform suppliers capitalize by bundling HRM reagents with cloud portals that auto-generate insurer-ready reports, reducing administrative overhead in small community hospitals.

High Capital Investment Required for HRM Instrumentation

Entry-level HRM platforms cost between USD 60,000 and USD 120,000, excluding service contracts, a hurdle for small labs whose reimbursement flows remain volatile. Staffing shortages compound the problem; one 2024 survey found 29.1% of US clinical labs reported difficulty retaining technologists, pushing management to delay equipment upgrades. Digital-twin projects show promise in boosting utilization and lowering amortized cost per test, yet such workflow-optimization software adds another USD 100,000-200,000, keeping total investment high. Financing solutions such as reagent-rental agreements are emerging, but interest-rate hikes since 2024 have raised leasing costs, limiting uptake in low-margin public hospitals.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Companion Diagnostics Development Pipelines

- Increasing Government Funding for Genomic Surveillance Programs

- Limited Standardization of Assay Protocols Across Laboratories

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and consumables generated the largest revenue in 2024, contributing 49.54% due to recurring refill demand that scales with installed instruments. The High-Resolution Melting Analysis market size attributable to reagents reached USD 137.4 million, and the category is forecast to maintain steady mid-single-digit growth as assay menus widen. Instrument revenue is accelerating at a 6.53% CAGR because multisite health systems invest in unified, automated analyzers that slash technician time and standardize quality across campuses. Manufacturers now bundle instruments with cloud licenses and validated assays, creating all-inclusive contracts that align with outcome-based procurement models. Software and service revenue, although still below 10% of overall value, is climbing fastest in mature markets where labs outsource data interpretation to vendor-operated platforms that guarantee 24/7 support.

The High-Resolution Melting Analysis Market Report is Segmented by Product & Service (Reagents & Consumables, Instruments, and Software & Services), Application (SNP Genotyping, and More), End-User (Research Laboratories & Academic Institutes, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America produced 41.56% of global revenue in 2024, underpinned by well-funded reference labs, payer policies that cover actionable gene-drug pairs, and a consolidated supplier base that offers nationwide service contracts. The region's demand is also buoyed by high companion-diagnostic trial activity, which funnels large volumes into contract research organizations equipped with fully automated HRM suites. Workforce shortages remain a challenge; US lab-technologist vacancy rates surpassed 46% in 2024, prompting networks to adopt instruments with walk-away workflows that minimize human intervention.

Asia-Pacific is the fastest-growing territory, projected at a 5.45% CAGR through 2030, propelled by universal-health-coverage programs and government-funded genomic initiatives such as Australia's USD 500.1 million Genomics Health Futures Mission. China's hospital-procurement reforms, which favor cost-effective domestic diagnostics, are encouraging local joint ventures that bundle HRM instruments with government-approved reagent menus. Mobile point-of-care pilots in India and the Philippines showcase cartridge-based HRM tests that run off battery packs, broadening access in regions lacking central labs.

Europe commands solid demand thanks to a dense network of academic medical centers and a supportive reimbursement climate for pharmacogenomics. The EU Medical Device Regulation harmonizes post-market surveillance, aiding suppliers in launching pan-European HRM kits. Hospitals in Germany and France are integrating cloud-based analytics that route anonymized melt-curve data into national bio-bank repositories, accelerating translational research links between genomic findings and therapy outcomes.

Middle East & Africa and South America collectively capture under 10% of revenue but record double-digit test-volume growth as infectious-disease programs seek rapid genotyping to guide outbreak response. Deployment of HRM-equipped mobile vans during the 2024 Rift Valley fever outbreak in Kenya cut sample processing times from five days to same day, reinforcing demand for ruggedized platforms in remote regions.

- Thermo Fisher Scientific

- Bio-Rad Laboratories

- QIAGEN

- Agilent Technologies

- Roche

- Illumina

- Azura Genomics

- Canon

- bioMerieux

- Meridian Bioscience

- New England Biolabs

- Promega

- LGC Biosearch Technologies

- Takara Bio

- Cepheid (Danaher)

- Fluidigm

- Analytik Jena

- Pacific Bioscience

- Sysmex

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Precision Medicine Initiatives

- 4.2.2 Expansion of Genetic Testing Reimbursement Policies

- 4.2.3 Surge in Companion Diagnostics Development Pipelines

- 4.2.4 Increasing Government Funding for Genomic Surveillance Programs

- 4.2.5 Proliferation of Decentralized Point-of-Care Molecular Testing

- 4.2.6 Integration of Cloud-Based Analytics for High-Throughput Workflows

- 4.3 Market Restraints

- 4.3.1 High Capital Investment Required for HRM Instrumentation

- 4.3.2 Limited Standardization of Assay Protocols Across Laboratories

- 4.3.3 Shortage of Skilled Molecular Diagnostics Personnel

- 4.3.4 Regulatory Uncertainty in Emerging Economies

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product & Service

- 5.1.1 Reagents & Consumables

- 5.1.1.1 Intercalating Dyes

- 5.1.1.2 Master Mixes

- 5.1.1.3 DNA Standards & Controls

- 5.1.2 Instruments

- 5.1.2.1 Real-time PCR Systems

- 5.1.2.2 Digital PCR Systems (HRM-enabled)

- 5.1.2.3 Compact POC Devices

- 5.1.3 Software & Services

- 5.1.3.1 Melt-curve Analysis Software

- 5.1.3.2 Cloud-based Analytics & AI Services

- 5.1.3.3 Validation & Training Services

- 5.1.1 Reagents & Consumables

- 5.2 By Application

- 5.2.1 SNP Genotyping

- 5.2.2 Mutation Discovery

- 5.2.3 Pathogen Identification

- 5.2.4 Methylation Analysis

- 5.2.5 Other Applications

- 5.3 By End-user

- 5.3.1 Research Laboratories & Academic Institutes

- 5.3.2 Pharmaceutical & Biotechnology Companies

- 5.3.3 Hospitals & Diagnostic Centers

- 5.3.4 Other End-users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Bio-Rad Laboratories Inc.

- 6.3.3 Qiagen N.V.

- 6.3.4 Agilent Technologies Inc.

- 6.3.5 F. Hoffmann-La Roche AG

- 6.3.6 Illumina Inc.

- 6.3.7 Azura Genomics

- 6.3.8 Canon Inc.

- 6.3.9 bioMerieux SA

- 6.3.10 Meridian Bioscience Inc.

- 6.3.11 New England Biolabs

- 6.3.12 Promega Corporation

- 6.3.13 LGC Biosearch Technologies

- 6.3.14 Takara Bio Inc.

- 6.3.15 Cepheid (Danaher)

- 6.3.16 Fluidigm Corporation

- 6.3.17 Analytik Jena AG

- 6.3.18 Pacific Biosciences of California Inc.

- 6.3.19 Sysmex Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment