|

시장보고서

상품코드

1851919

벽지 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Wallpaper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

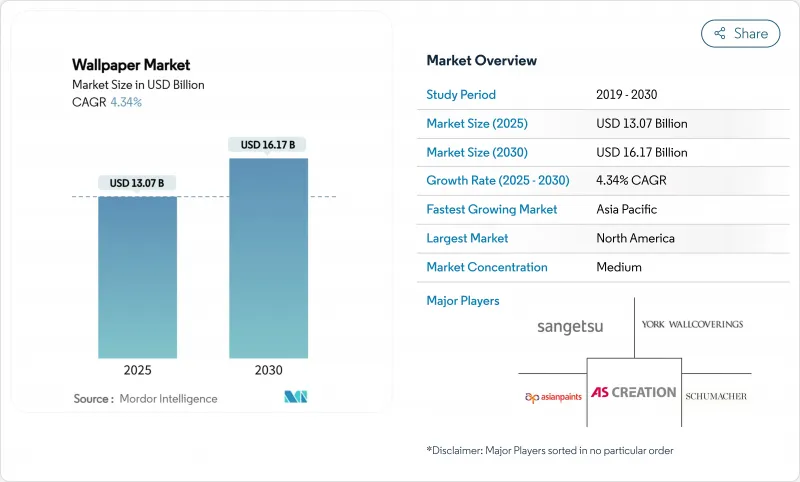

세계의 벽지 시장 규모는 2025년에 130억 7,000만 달러로 추정되고, 2030년에는 161억 7,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 4.34%로 성장할 전망입니다.

디지털 인쇄, 항균 코팅, 필 앤 스틱 기재가 주택 리폼의 급증, 접객의 리프레시 사이클 격화, 중소득 가구의 인테리어 미관에 대한 기대 증가와 함께 수렴하여 수요가 확대됩니다. GCC와 ASEAN의 호텔 건설 파이프라인은 엄격한 유지보수 일정을 견딜 수 있는 고급스럽고 내구성이 뛰어난 벽지를 지정하기 때문에 상업 시설 설치가 현재 주도되고 있습니다. 주택 채용은 동남아 정부가 저렴한 주택 프로그램에 보조금을 내고 북미 주택 소유자가 일상적인 재도장보다 개성적인 장식을 선택함에 따라 가속화되고 있습니다. 공급망은 염화 비닐의 가격 변동과 관세 인상에 직면하고 있지만, 제조업체는 수직 통합, 수지 장기 계약, 비 비닐 기재의 기술 혁신을 통해 금리를 확보하고 있습니다. 경쟁사와의 차별화는 옴니채널 유통, 지속가능성 증명, 온디맨드 인쇄에 의한 디자인 컨셉에서 완성 롤로의 변환 속도에 달려 있습니다.

세계의 벽지 시장 동향 및 인사이트

북미와 유럽에서 디지털 인쇄에 의한 개인 장식품 수요 급증

Roland DG와 Panasonic Housing Solutions(이하, 파나소닉)는 온디맨드 디지털 인쇄에 의해 디자이너가 제판이나 최소 로트의 제약으로부터 해방되어, 시리얼화된 패턴, 2mm까지의 촉감이 좋은 3D 텍스처, 디자인으로부터 시공까지의 사이클을 단축하는 고속 프로토타이핑이 가능하게 됩니다. Roland DG와 Panasonic Housing Solutions는 여분의 엠보스 패스를 필요로 하지 않고 조각 같은 표면을 생성하는 DIMENSE 기술을 발표했습니다. 럭셔리 페인트 제조업체 벤자민 무어는 알파 워크숍과 협업하여 1야드 125달러의 벽지를 핸드 페인트했습니다. 샌더슨 디자인 그룹(Sanderson Design Group)과 같은 유럽의 대기업은 1롤 1만 3,900엔에서 3만 5,100엔으로 판매하는 헤리티지와 디지털을 융합시킨 상품으로 이 부문을 쫓아 샌더슨의 독특한 스토리에 돈을 지불하는 부유층의 의욕을 실증하고 있습니다. 전자상거래는 보급을 가속화합니다. : 그레이엄 앤 브라운의 B2B 포털은 불과 12주만에 고객의 도입률이 90%에 달하여 주문 마찰과 재고 위험을 줄였습니다. 이로 인해 제조업체의 이익률이 향상되고 디지털 워크 플로우가 맞춤형 주택 및 부티크 상업 프로젝트의 기본 모드가 되었습니다.

동남아시아의 급속한 중소득자를 위한 도시형 주택 붐

인도네시아에서는 2024년 1분기에 GDP의 10.23%를 차지하는 건설이 이루어졌고, 베트남에서는 2025년 상반기에 60만 호를 넘는 사회주택이 건설되었습니다. 인도네시아의 One Million House 계획과 카타르가 지원하는 대출 채널 등 정부 프로그램은 첫 구매자의 구매력을 높여 브랜드 지향이면서 비용 효율적인 장식품 선택을 향하게 합니다. 아시아 개발은행은 2025년 역내 GDP 성장률을 4.5%로 예측하고 있으며, 이는 리폼에 대한 지출을 뒷받침하고 있습니다. 국제적인 생산자는 관세를 피하고 리드 타임을 단축하는 지역 공장에서 대응하고, 현지 브랜드는 수입 대체 인센티브를 이용합니다. 밀레니얼 세대의 온라인 구매 습관은 디지털 커스터마이징 플랫폼으로의 트래픽을 촉진하고 디지털 인쇄된 상품에 대한 인수를 더욱 강화합니다.

시장에서 대체품의 용이한 가용성

페인트, 장식 패널 및 디지털 디스플레이는 항상 가치 제안을 업그레이드하고 있으며 유지 보수의 간편성과 대화형 컨텐츠가 우세한 벽지 점유율을 침식합니다. 샤윈 윌리엄스의 페인트 쉴드는 페인트에 직접 살균 기능을 도입하여 2시간 만에 99.9%의 박테리아를 사멸시키고, 한때는 특수 벽지에만 사용된 예산을 획득했습니다. 텍스처 페인트, 벽 스티커, 거실 플랜트 벽은 생물 친화적인 디자인 서류를 실현하고 모듈 식 패널 시스템은 사무실이 밤새 공간을 재구성할 수 있게 합니다. 대용품의 폭이 넓어진 것으로, 벽지의 생산자는 촉감의 깊이, 소재의 원형성, 시공 효율을 강조하지 않을 수 없게 되었습니다.

부문 분석

부직포 제품은 2025년의 CAGR 전망을 6.06%로 추정하고, 벽지 시장 전체의 성장을 웃돌았습니다. 통기성이 있고 치수가 안정된 기재는 설치나 철거 작업을 간소화하기 위해서입니다. 비닐은 병원 사양의 내구성과 시장 경쟁력에 의해 2024년에는 32.43%의 점유율을 유지했지만, 환경에 대한 배려로부터 바이오 PVC, 재생 PET, 무용제 잉크에 대한 요구가 강해지고 있습니다. 종이 기반 라인은 축소되어 유지 보수의 용이성보다 진짜 지향의 전통적인 주택에서 살아남습니다. 패브릭의 표면 커버는 촉감의 따뜻함과 내장된 방음 기능을 제공하여 틈새 고급 공간에 도움이 됩니다. 보라 스타 피터의 Viared 시설은 기술적 다양성을 보여 주며 각 소재의 인쇄 적합성에 따라 표면 인쇄, 그라비아 인쇄, 스크린 인쇄 및 디지털 인쇄기를 하나의 지붕 아래에서 작동합니다.

부직포의 기세는 지속가능성 규제와 교차하여 FSC 인증 섬유 및 수성 접착제로 마케팅의 방향 전환을 촉진합니다. 이 부문의 민첩성은 항균 화학물질과 박리 및 스틱 접착제의 신속한 채택을 가능하게 하고, 임대 아파트에서 소아과 클리닉에 이르기까지 최종 사용 범위를 확장합니다. 비닐의 이노베이터는 프탈산에스테르 프리의 처방이나 에너지 절약의 엠보스 경화제로 대응해, 점유율을 지키고 있습니다. 금속 호일과 유리 섬유 강화 시트와 같은 새로운 복합재료는 난연성과 전자파 차폐가 필요한 기능적 틈새를 목표로 합니다.

디지털 기술은 2024년에 생산량의 58.42%를 차지했고, 매년 7.32%씩 증가해, 벽지 시장을 수주 생산의 패러다임으로 바꾸고 있습니다. 잉크젯 헤드와 UV 경화형 화학의 조합은 다양한 기판에 즉각적인 경화 및 생생한 채도를 제공하며, 라텍스 시스템은 낮은 VOC 코드를 준수합니다. 캐논 지침에 따르면 디지털은 버전을 필요로 하지 않으며, 설치 패널티 없이 맞춤형 롤에서 중간 규모의 호스피탈리티 주문까지 배치 크기를 가능하게 합니다. 스크린 인쇄는 특히 전통적인 다마스크에서는 풍부한 잉크 레이다운과 특수 효과가 여전히 다른 추종을 허용하지 않습니다. Flexo 인쇄는 고정밀 재현성이 실린더 투자를 정당화하는 장기적인 상업용 통로에서 지보를 굳히고 있습니다. 하이브리드 라인이 등장하고 기존의 스테이션 앞에 싱글 패스 디지털 유닛을 통합함으로써 대량 인쇄된 베이스에 맞춤형 모티프를 거듭할 수 있습니다.

고속 프루핑 루프와 AI 컬러 매칭 소프트웨어는 컨셉부터 시장 출시까지의 타임라인을 수개월에서 며칠로 단축시켜 디자이너가 유행 동향에 대응할 수 있게 합니다. 비용 이점은 재고에 그치지 않습니다. 디지털 소량 생산 기능은 운전 자본을 줄이고 진부한 재고의 감가상각을 줄입니다. 한편, UV-LED 램프의 효율은 에너지 비용을 줄이고 인쇄 회사가 탄소 중립 목표를 달성하는 데 도움이 됩니다. 옥틴크의 50년에 걸친 궤적은 레거시 숍이 인쇄 기술의 전통을 포기하지 않고 디지털로 개조가 가능하다는 것을 보여줍니다.

지역 분석

북미는 확립된 리노베이션 문화 및 디지털 인쇄 워크플로우의 조기 도입을 배경으로 2024년 출하를 이끌었습니다. 미국에서는 유연한 소매 컨셉에 추진된 필 앤 스틱의 유행이 원재료 비용의 변동에도 불구하고 예측 수요를 끌어올리고 있습니다. 캐나다 건설자재 시장은 2026년까지 4.5-5.5%의 성장이 예상되며 대응 가능한 기반에 시설 프로젝트가 더해집니다. 멕시코는 니어 쇼어링의 허브로 부상하고 아시아의 운임 변동을 완화하고자 하는 미국의 프리미엄 브랜드에 비용 효율적인 생산을 제공합니다. 요크월커버링스는 독립계 표면 인쇄 사업을 인수하여 지역 리더십을 강화하고 지역 공급망을 강화합니다.

유럽은 디자인의 전통과 엄격한 환경 규제로 강력한 가격 프리미엄을 유지했습니다. 독일과 이탈리아는 무용제 인쇄를 의무화하여 수성 잉크의 채용을 가속합니다. 영국의 인테리어는 샌더슨의 울에 영감을 받은 'Orwell Weaves' 및 'Country Woodland'의 발표에서 볼 수 있듯이 장인 기술에 의한 부활을 축하합니다. 스페인과 같은 남부 시장에서는 호스피탈리티가 있는 테라스를 돋보이게 하기 위해 자외선에 강한 야외용 벽재가 주목받고 있습니다. 동유럽 수요는 환율 변동에 좌우되지만, 폴란드와 체코에서는 리폼 보조금이 수량 감소를 완화하고 있습니다. 서큘러 이코노미(순환형 경제) 지령에 의해 생산자는 요람부터 요람까지 사용할 수 있는 기재를 인증해, 인수 제도를 시험적으로 도입하고 있습니다.

아시아태평양은 가장 급격한 수량 증가를 기록했습니다. 인도네시아는 연간 300만 호의 주택 공급을 계획하고 베트남의 사회 주택 건설 목표는 수십만 호를 추가하는 것입니다. 중국의 국내 생산 의욕은 수출 생산과 함께 높아지고 있으며, 범위의 경제로부터 혜택을 받는 메가 스케일 라인이 유지되고 있습니다. 인도 장식용 페인트의 선두 주자인 Asian Paints는 옴니 채널을 활용하여 이 회사의 서비스 부서에서 벽지 번들 상품을 교차 판매합니다. 성숙 시장의 일본과 한국은 고기능 제품을 선호합니다. : Sanghetts의 재생 PET 유리 필름은 저탄소 건축 기준을 충족하는 동시에 UV 방열 기능을 갖추고 있습니다. 호주는 산 화재의 영향을 받기 쉬운 지역을 위한 난연성 벽 패브릭에 축발을 놓고 기능적인 틈새를 충실히 하고 있습니다. 이 지역의 2025년 1분기까지의 호스피탈리티 파이프라인은 2,074건에 걸쳐 지속적인 계약량을 보장하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 북미와 유럽에서 디지털 인쇄 명함 장식품 수요 급증

- 동남아시아의 급속한 중소득자용 도시형 주택 붐

- 호스피탈리티의 리프레시 사이클이 GCC와 ASEAN의 프리미엄 상업 제품 견인

- 미국에서 소매업의 비주얼 머천다이징은 붙여 벗길 수 있는 비닐에 시프트

- 의료 개수에서 항균 코트 벽지의 채용

- 시장 성장 억제요인

- 시장에서 대체품의 용이한 이용 가능성

- PVC 가격의 난고하가 마진 압박

- 열과 습기에 노출되면 수명 단축

- 공급망 분석

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 유형별

- 비닐

- 부직포

- 종이 베이스

- 원단(실크, 린넨 등)

- 기타 벽지 유형

- 인쇄 기술별

- 디지털(잉크젯/EP)

- 스크린

- 플렉소 인쇄

- 기타 인쇄 기술

- 최종 사용자별

- 주택용

- 상업용

- -호스피탈리티

- - 기업 사무실

- - 살롱 및 스파

- - 병원

- - 기타 최종 사용자

- 유통 채널별

- 직접 판매

- 간접 판매

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주, 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Sangetsu Corporation

- York Wall Coverings Inc.

- AS Creation Tapeten AG

- Brewster Home Fashion LLC

- Grandeco Wallfashion Group

- Erismann & Cie. GmbH

- Sanderson Design Group PLC

- Tapetenfabrik Gebr. Rasch GmbH & Co. KG

- Marshalls Wallcoverings

- Asian Paints Ltd(Nilaya)

- Eximus Wallpaper

- Gratex Industries Ltd

- Graham & Brown Ltd

- Wallquest Inc.

- Adornis Wallpapers

- Arte International

- 4walls

- Omexco NV

- Life n Colors Private Limited

- Komar Products GmbH

- Houfling GmbH(Hohenberger)

제7장 시장 기회 및 향후 전망

AJY 25.11.19The global wallpaper market size reached USD 13.07 billion in 2025 and is forecast to touch USD 16.17 billion by 2030, advancing at a 4.34% CAGR during the period.

Demand expands as digital printing, antimicrobial coatings, and peel-and-stick substrates converge with surging residential renovation activity, intensified hospitality refresh cycles, and rising interior-aesthetic expectations among mid-income households. Commercial installations currently lead because hotel construction pipelines in the GCC and ASEAN continue to specify premium, durable wallcoverings that withstand rigorous maintenance schedules. Residential adoption accelerates as Southeast Asian governments subsidize affordable housing programs and North American homeowners opt for personalized decor over routine repainting. Supply chains face vinyl-chloride price swings and tariff hikes, yet manufacturers defend margins through vertical integration, long-term resin contracts, and innovation in non-vinyl substrates. Competitive differentiation now hinges on omnichannel distribution, sustainability credentials, and the speed with which on-demand printing can translate design concepts into finished rolls.

Global Wallpaper Market Trends and Insights

Surge in Demand for Digitally-Printed Personalised Decor in North America and Europe

On-demand digital printing liberates designers from plate-making and minimum-run constraints, enabling serialized patterns, tactile 3D textures up to 2 mm, and fast prototyping that shortens design-to-installation cycles. Roland DG and Panasonic Housing Solutions unveiled DIMENSE technology that produces sculpted surfaces without extra embossing passes, widening creative scope and cost efficiency. Luxury paint maker Benjamin Moore collaborated with The Alpha Workshops to hand-paint wallpapers retailing at USD 125 per yard, proof that customization supports 40-60% price premiums. European stalwarts such as Sanderson Design Group chase this segment with heritage-meets-digital launches that sell for ¥13,900-¥35,100 per roll, validating affluent willingness to pay for unique stories Sanderson. Ecommerce accelerates uptake: Graham & Brown's B2B portal reached 90% client adoption in just 12 weeks, cutting order friction and inventory risk. These gains lift manufacturer margins and position digital workflows as the default mode for bespoke residential and boutique commercial projects.

Rapid Mid-Income Urban Housing Boom in Southeast Asia

Indonesia reported construction representing 10.23% of GDP in Q1 2024 while Vietnam initiated over 600,000 social housing units during H1 2025, setting a long-tail demand curve for mid-priced wallcoverings that balance aesthetics with affordability. Government programs such as Indonesia's One Million House plan and Qatar-backed financing channels lift first-time buyers' purchasing power, steering them toward branded yet cost-effective decor choices. Asian Development Bank forecasts 4.5% regional GDP growth for 2025, underpinning discretionary renovation spending. International producers answer with regional plants that dodge tariffs and shorten lead times, while local brands exploit import substitution incentives. Millennials' online buying habits drive traffic to digital customization platforms, further intensifying the pull on digitally printed offerings.

Easy Availability of Substitutes in the Market

Paints, decorative panels, and digital displays constantly upgrade value propositions, eroding wallpaper's share where maintenance simplicity or interactive content holds sway. Sherwin-Williams Paint Shield introduces microbicidal functions directly into paint, killing 99.9% of bacteria in 2 hours and capturing budgets once reserved for specialty wallcoverings. Textured paints, wall decals, and living-plant walls fulfil biophilic design briefs, while modular panel systems allow offices to reconfigure spaces overnight. The broadening substitute set compels wallpaper producers to stress tactile depth, material circularity, and installation efficiency.

Other drivers and restraints analyzed in the detailed report include:

- Hospitality Refresh Cycles Driving Premium Commercial Wallpaper in GCC and ASEAN

- Retail Visual-Merchandising Shift to Peel-and-Stick Vinyl in the U.S.

- Vinyl-Chloride Price Volatility Compressing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-woven products opened 2025 with a 6.06% CAGR outlook, eclipsing overall wallpaper market growth as breathable, dimensionally stable substrates simplify installation and removal tasks. Premium installers champion the category because dry-strippable properties cut labour by up to 30%. Vinyl retained 32.43% wallpaper market share in 2024 thanks to hospital-grade durability and cost competitiveness, yet environmental scrutiny intensifies calls for bio-PVC, recycled PET, and solvent-free inks. Paper-based lines contract, surviving mostly in heritage residences where authenticity tops maintenance ease. Fabric surface coverings serve niche luxury spaces, offering tactile warmth and built-in acoustic dampening. Borastapeter's Viared facility illustrates technical diversity, running surface, gravure, screen, and digital presses under one roof to match each material's printability.

Non-woven momentum intersects sustainability regulation, prompting marketing pivots toward FSC-certified fibres and water-based adhesives. The segment's agility allows quick adoption of antimicrobial chemistries or peel-and-stick adhesives, widening end-use scope from rental apartments to pediatric clinics. Vinyl innovators respond with phthalate-free formulations and energy-saving emboss cures to defend share. Emerging composites such as metallic foils or glass fibre reinforced sheets target functional niches demanding fire retardancy or electromagnetic shielding.

Digital technologies captured 58.42% of production in 2024 and are adding 7.32% annually, transforming the wallpaper market into a make-to-order paradigm. Inkjet heads paired with UV-curable chemistries deliver immediate curing and vibrant colour saturation on diverse substrates, while latex systems comply with low-VOC codes. Canon's guidance confirms that digital eliminates plates, enabling batch sizes from a single customised roll to mid-volume hospitality orders without setup penalties. Screen printing retains pockets where rich ink laydown and special effects are still unrivalled, particularly for heritage damasks. Flexography holds ground in long-run commercial corridors where precision repeatability justifies cylinder investments. Hybrid lines emerge, integrating single-pass digital units ahead of conventional stations so bespoke motifs overlay mass-printed bases.

Rapid proofing loops and AI colour-matching software compress concept-to-market timelines from months to days, letting designers react to viral trends. Cost advantages extend beyond inventory: digital short-run capabilities reduce working capital and shrink obsolete stock write-offs. Meanwhile, UV-LED lamp efficiencies drop energy bills, helping printers meet carbon-neutral targets. Octink's 50-year trajectory shows legacy shops can retrofit for digital without surrendering printcraft heritage.

The Wallpaper Market Report is Segmented by Wallpaper Type (Vinyl, Non-Woven, Paper-Based, Fabric, Other), Printing Technology (Digital, Screen, Flexographic, Other), End User (Residential, Commercial), Distribution Channel (Direct Sales, Indirect Sales), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led 2024 shipments on the back of established renovation culture and early adoption of digital-print workflows. The U.S. peel-and-stick craze, fuelled by flexible retail concepts, bolsters forecast demand despite raw-material cost swings. Canada's construction-materials market expects 4.5-5.5% growth through 2026, adding institutional projects to the addressable base. Mexico emerges as a near-shoring hub, providing cost-efficient production for premium U.S. brands looking to mitigate Asian freight volatility. York Wallcoverings consolidates regional leadership after acquiring independent surface-print operations, strengthening local supply chains.

Europe preserves a strong pricing premium through design heritage and stringent eco-regulation. Germany and Italy push solvent-free print mandates, prompting accelerated adoption of water-based inks. United Kingdom interiors celebrate artisanal revival, evident in Sanderson's wool-inspired Orwell Weaves and Country Woodland launches. Southern markets such as Spain emphasise UV-stable outdoor wall applications to complement hospitality terraces. Eastern Europe's demand fluctuates with currency swings, though renovation subsidies in Poland and Czechia cushion volume declines. Circular-economy directives drive producers to certify cradle-to-cradle substrates and pilot take-back schemes.

Asia-Pacific records the steepest volume climb; Indonesia plans to deliver three million homes yearly while Vietnam's social housing targets add hundreds of thousands of units. China's domestic appetite strengthens alongside export output, sustaining mega-scale lines that benefit from economies of scope. India's decorative coatings leader Asian Paints leverages omnichannel reach to cross-sell wallpaper bundles under its services arm. Mature markets Japan and South Korea favour high-function products: Sangetsu's recycled-PET glass films meet low-carbon building codes while offering UV heat-shielding. Australia pivots to fire-retardant wall fabrics for bushfire-vulnerable regions, enriching the functional niche. Collectively, the region's 2,074-project hospitality pipeline through Q1 2025 guarantees sustained contract volumes.

- Sangetsu Corporation

- York Wall Coverings Inc.

- A.S. Creation Tapeten AG

- Brewster Home Fashion LLC

- Grandeco Wallfashion Group

- Erismann & Cie. GmbH

- Sanderson Design Group PLC

- Tapetenfabrik Gebr. Rasch GmbH & Co. KG

- Marshalls Wallcoverings

- Asian Paints Ltd (Nilaya)

- Eximus Wallpaper

- Gratex Industries Ltd

- Graham & Brown Ltd

- Wallquest Inc.

- Adornis Wallpapers

- Arte International

- 4walls

- Omexco NV

- Life n Colors Private Limited

- Komar Products GmbH

- Houfling GmbH (Hohenberger)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Demand for Digitally-Printed Personalised Decor in North America and Europe

- 4.2.2 Rapid Mid-Income Urban Housing Boom in Southeast Asia

- 4.2.3 Hospitality Refresh Cycles Driving Premium Commercial products in GCC and ASEAN

- 4.2.4 Retail Visual-Merchandising Shift to Peel-and-Stick Vinyl in the U.S.

- 4.2.5 Adoption of Antimicrobial Coated Wallcoverings in Healthcare Renovations

- 4.3 Market Restraints

- 4.3.1 Easy Availability of Substitues in the Market

- 4.3.2 Vinyl-Chloride Price Volatility Compressing Margins

- 4.3.3 Shorter Life-span on Exposure to Heat and Moisture

- 4.4 Supply-Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Vinyl

- 5.1.2 Non-woven

- 5.1.3 Paper-based

- 5.1.4 Fabric (Silk, Linen, etc.)

- 5.1.5 Other wallapaper Type

- 5.2 By Printing Technology

- 5.2.1 Digital (Inkjet/EP)

- 5.2.2 Screen

- 5.2.3 Flexographic

- 5.2.4 Other Printing Technology

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 -Hospitality

- 5.3.4 - Corporate Office Space

- 5.3.5 -Salons and Spas

- 5.3.6 - Hospitals

- 5.3.7 -Other End User

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales

- 5.4.2 Indirect Sales

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Sangetsu Corporation

- 6.4.2 York Wall Coverings Inc.

- 6.4.3 A.S. Creation Tapeten AG

- 6.4.4 Brewster Home Fashion LLC

- 6.4.5 Grandeco Wallfashion Group

- 6.4.6 Erismann & Cie. GmbH

- 6.4.7 Sanderson Design Group PLC

- 6.4.8 Tapetenfabrik Gebr. Rasch GmbH & Co. KG

- 6.4.9 Marshalls Wallcoverings

- 6.4.10 Asian Paints Ltd (Nilaya)

- 6.4.11 Eximus Wallpaper

- 6.4.12 Gratex Industries Ltd

- 6.4.13 Graham & Brown Ltd

- 6.4.14 Wallquest Inc.

- 6.4.15 Adornis Wallpapers

- 6.4.16 Arte International

- 6.4.17 4walls

- 6.4.18 Omexco NV

- 6.4.19 Life n Colors Private Limited

- 6.4.20 Komar Products GmbH

- 6.4.21 Houfling GmbH (Hohenberger)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment