|

시장보고서

상품코드

1851921

소자 시스템 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Degaussing Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

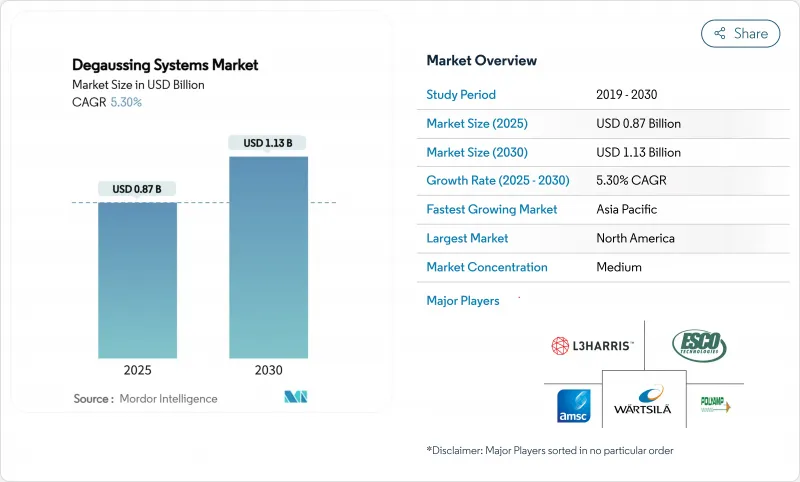

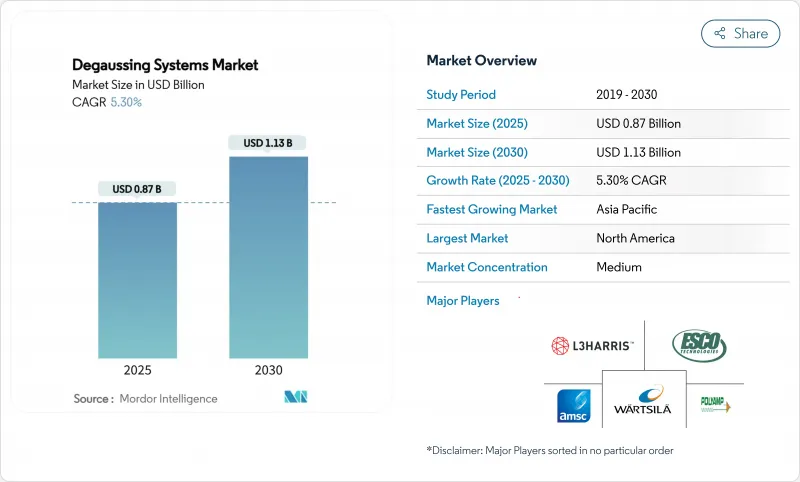

소자 시스템 시장 규모는 2025년 8억 7,000만 달러, 2030년에는 11억 3,000만 달러에 이르고, CAGR은 5.3%를 보일 것으로 예측됩니다.

해군 경비 증가, 자기 영향형 기뢰의 고도화, 함대 수명 연장 프로그램의 꾸준한 페이스가 이 확대를 지지하고 있습니다. 북미의 구축함과 순양함 업그레이드, 유럽의 기뢰 소해정 조달, 아시아태평양의 잠수함 플릿의 확대가 전자기 시그니처 제어의 광범위한 고객 기반을 확보하고 있습니다. 고온 초전도(HTS) 코일과 소프트웨어 정의 제어 장치가 기술 업데이트 사이클을 촉진하는 반면, 인공지능(AI) 알고리즘은 코일 전류를 실시간으로 조정하여 성능 임계값을 높입니다. 레트로핏 수요가 계약활동을 지배하고 있는 이유는 해군이 시그니처 매니지먼트를 신조선에 지출하지 않고 배의 수명을 연장하는 비용 효율적인 방법으로 간주하고 있기 때문입니다. HTS 테이프와 희토류 자기 센서를 둘러싼 공급망의 압력은 단기적인 성장을 억제하지만 수직 통합 구성 요소 라인을 가진 Tier One 벤더는 대부분의 혼란을 완화합니다.

세계 소자 시스템 시장 동향과 통찰

해군 근대화 예산 증가로 소자 시스템 투자 가속화

국방예산의 꾸준한 증가로 여러 해에 걸친 함선 업그레이드 파이프라인이 활발해지고 있습니다. 미국 해군의 구축함 수명 연장 패키지에서는 전자전 강화의 핵심으로서 시그니처 관리의 개수가 예정되어 있습니다. 이탈리아의 기뢰 소해정 프로그램에서는 저자기 음향 기술이 기본적인 장비로 포함되어 있습니다. 필리핀과 캐나다의 유사한 조달 청사진은 소자 시스템 시장의 장기적인 활주로를 확고하게 만듭니다.

자기 영향형 해저 지뢰의 배치 확대가 자기 신호 제어 수요를 촉진

최신 지뢰는 자기, 음향, 압력 센서를 결합하여 정밀한 자기장 억제 요건을 높이고 있습니다. 인도의 다중 독감 지뢰의 검증은 해군 플래너가 대항해야 하는 살상력 증가를 보여줍니다. 역사적인 손실 수치는 기뢰가 여전히 가장 비용 효율적인 대수상 무기임을 밝히고 있으며, 심해함 및 해안 함선 전체에서 견고한 디가싱 필요성을 뒷받침하고 있습니다.

급증하는 자본 투자와 장기적인 유지 보수 비용은 보다 광범위한 채택을 제한합니다.

첨단 소자 시스템과 관련된 상당한 선행 투자와 지속적인 운영 비용은 특히 예산이 제한된 소규모 해군 부대의 경우 채용 장벽이 될 것입니다. 종합적인 디가우스 설비는 선박의 총 건축비의 2-5%를 차지하고, HTS 기반 패키지는 구리 코일에 의한 대체품을 40-60% 웃도는 프리미엄이 요구됩니다. 극저온 냉각 플랜트, 헬륨 로지스틱스, 인증된 기술자 등 특수한 라이프사이클 지원은 중형 전투함의 10년간 유지보수에 200만-400만 달러를 추가합니다. 이러한 재정적인 현실에서 해군은 종종 우선 순위가 낮은 선체에 자기 발자국을 남기는 것을 받아들이면서 모든 지역의 서명 관리를 항공 모함, 잠수함 및 최전선 구축함으로 제한해야합니다. 그 결과 신흥 해양 국가로 시장 침투가 지연되고, 그 이유는 자본 비용이 다른 전투 시스템의 업그레이드를 압박하기 때문입니다.

부문 분석

부문 합계는 눈에 띄지 않는 플랫폼이 지출을 지원하는 방법을 돋보이게합니다. 잠수함 카테고리는 2024년 소자 시스템 시장 매출의 29.65%를 차지하지만, 수뢰 대책함은 CAGR 7.89%에서 가장 빠르게 확대됩니다. 이 성능 차이는 영향력 있는 기뢰로 인한 위협이 현저하다는 점과 빙점이나 해안에서의 은폐가 전략적으로 중요하다는 것을 반영합니다. 호주, 인도, 한국의 잠수함 계획에서는 설계 단계에서 풀할 코일 세트를 통합하고 있으며, 뒷부분이 일반적인 수상함과는 대조적입니다. 수뢰 소해정의 선체는 이미 저 페라이트 복합재로 만들어졌지만 잔류 자기를 부수기 위해 분산형 마이크로 루프를 추가하고 있습니다. 구축함과 플리게이트함은 레이더와 소나의 갱신 사이클과 시기를 동일하게 하여 중기의 업그레이드가 이루어지므로, 데가우스의 작업 범위에 시너지 효과가 생겨 큰 수요를 유지하고 있습니다.

해군은 예산을 배분할 때 함선 고유의 리스크 익스포저를 고려합니다. 잠수함은 지속적인 수동적 감지 위험에 직면하기 때문에 높은 사양의 독자적인 소재가 정당화됩니다. 반대로 코르벳은 지역의 자기 조건에 맞게 정격화된 표준화된 코일 모듈을 사용하여 비용을 분산하는 모듈 아키텍처를 채택하고 있습니다. 이러한 미묘한 조합으로 공급업체는 제어 코드를 다시 작성하지 않고 30m 무인선에서 100,000톤의 수송선까지 구성 가능한 시스템을 실전 투입해야 합니다.

2024년 매출의 60.90%를 차지한 것은 연속적인 소자 시스템이며, 이것이 기준선으로 적합하다는 것을 강조하고 있습니다. 탈자력은 여전히 핵심이지만, 최신의 강재는 극지 통과를 반복해도 높은 잔류 자력을 유지하기 때문에 탈자력이 재부상하고 있습니다. 2030년까지의 CAGR이 6.12%인 것은 해군이 지뢰가 있는 초크 포인트에 배치하기 전에 정기적인 소자를 중요한 보험으로 간주하고 있음을 뒷받침하고 있습니다. 현재의 부두측의 소자 케이지는 종래의 절반의 처리 시간으로 95.5%의 자속 밀도 저감이 가능한 펄스 직류 기술을 채택하고 있습니다. 게다가, 운반가능한 치료 매트는 프리깃함이 홈 도크로 돌아가지 않고 순찰 중에 서명을 재설정할 수 있게 합니다.

더 작은 틈새이지만 거리 측정 시설은 경험적 자기장 데이터를 제공하여 피드백 루프를 닫습니다. 소프트웨어 분석은 이러한 측정치를 코일 전류 설정값으로 외삽하여 낮은 수익 부문조차도 보다 수익성이 높은 디지털 서비스로 풀스루를 생성한다는 것을 입증합니다.

지역 분석

북미는 2024년 매출의 34.17%를 차지했습니다. 미국 해군의 구축함과 순양함의 수명 연장 계약만으로 국산 코일, 자력계, 제어 유닛을 선호하는 수십억 달러의 파이프라인이 유지되고 있습니다. 캐나다의 킹스톤급 데가우스 리노베이션과 동맹국의 대외군사판매(FMS) 사례는 이 지역의 지위를 더욱 강화하고 있습니다. 3개의 HTS 테스트 베드가 인증되었으며 북미 야드는 세계에서 가장 첨단 초전도 배포 프로그램을 호스팅합니다.

아시아태평양은 2030년까지 최고 CAGR 8.80%로 성장할 전망입니다. 방어 예산 증가와 바다의 쟁탈은 수요를 촉진합니다. 일본은 모가미급 프리게이트함의 HTS 시험을 확대하고 호주 AUKUS 잠수함의 시도는 기존 기준을 능가하는 자기 시그니처 관리 기준을 통합합니다. 인도의 수뢰 계획은 동남아시아의 해안 함대의 확대와 함께 무인 플랫폼용 마이크로 데가우스 솔루션의 채택을 가속화하고 있습니다. 중국의 조선소는 신조의 054B형에 AI 구동의 필드 튜닝 소프트웨어를 짜넣어, 이 지역의 기술 페이스를 설정해, 동업 타사에 따라잡도록 촉구하고 있습니다.

유럽은 NATO의 발트해와 북극권의 태세에 따라 활기차며 여전히 매우 중요합니다. 이탈리아의 기뢰소해 구상이나 프랑스의 FDI 프리게이트함 시리즈에는 시스템 오브 시스템즈의 조달을 추진하는 구축과 측거의 조합이 짜넣어지고 있습니다. 영국의 31형 계획에서는 디지털 트윈으로 검증된 코일 레이아웃이 표준 사양이 되어, 자기 위생에 대한 지역의 헌신이 강조되고 있습니다. 극지조사 쇄빙선에 대한 병행투자는 전투기 이외의 수익원을 다양화하고, 소자 벤더에 민간 해양 틈새 시장을 도입하여 전투원을 넘어 수익원을 다각화합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 해군 근대화 예산 증가에 의해 소자 시스템에 대한 투자가 가속

- 자기 시그니처 제어 수요를 유발하는 자기 영향 해상 광산의 배치 증가

- 구식의 수상 함정을 대상으로 한 레트로핏 이니셔티브의 확대.

- 컴팩트하고 효율적인 시스템을 가능하게 하는 고온 초전도(HTS) 코일 기술 출현

- 실시간 시그니처 관리를 위한 AI를 활용한 적응 알고리즘의 통합

- 스텔스성이 높은 무인 지상·수중 차량의 시스템에 대한 요구 증가

- 시장 성장 억제요인

- 급증하는 자본 지출과 장기적인 유지 보수 비용은 보다 광범위한 채택을 제한

- 복잡한 방위 조달 수속에 의한 취득 스케줄의 연장

- 신흥 레일건 및 지향성 에너지 무기 시스템에의 자원 재분배에 의해 자금 조달의 가능성이 저하

- HTS 테이프와 희토류 기반의 자기 센서공급 체인 취약성이 생산의 확장성을 방해한다

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 선박 유형별

- 항공모함

- 구축함

- 호위함

- 초계함

- 잠수함

- 대기뢰전함정

- 기타 선박 유형

- 솔루션별

- 디가우징

- 디퍼밍

- 레인징

- 구성요소별

- 컨트롤 유닛(DCU)

- 파워 앰프

- 코일과 케이블

- 자력계와 센서

- 소프트웨어 및 분석

- 설치 유형별

- 신설

- 레트로 핏

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 기타 남미

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- L3Harris Technologies Inc.

- Wartsila Corporation

- Polyamp AB

- Larsen & Toubro Limited

- Exail SAS

- IFEN SpA

- American Superconductor Corporation(AMSC)

- Dayatech Merin Sdn Bhd

- DA Group

- Ultra Electronics Holdings Ltd.

- Babcock International Group

- Thales Group

- ESCO Technologies inc.

제7장 시장 기회와 장래의 전망

SHW 25.11.25The degaussing systems market size is estimated at USD 0.87 billion in 2025 and is forecasted to reach USD 1.13 billion by 2030, advancing at a 5.3% CAGR.

Rising naval expenditure, the growing sophistication of magnetic-influence sea mines, and the steady pace of fleet-life-extension programs underpin this expansion. North American destroyer and cruiser upgrades, European mine-hunter procurement, and expanding Asia-Pacific submarine fleets ensure a broad customer base for electromagnetic signature control. High-temperature superconducting (HTS) coils and software-defined control units foster technology refresh cycles, while artificial-intelligence (AI) algorithms push performance thresholds by moderating coil currents in real time. Retrofit demand governs contract activity because navies view signature management as a cost-effective path to stretching ship life without new-build outlays. Supply-chain pressure around HTS tape and rare-earth magnetic sensors tempers short-term growth, yet tier-one vendors with vertically integrated component lines mitigate most disruption.

Global Degaussing Systems Market Trends and Insights

Rising Naval Modernization Budgets Accelerating Investment in Degaussing Systems

Steady growth in defense allocations keeps multi-year ship-upgrade pipelines active. The US Navy's destroyer life-extension package earmarks signature-management retrofits as core electronic-warfare enhancements. Italy's mine-hunter program embeds low-magneto-acoustic technologies as a baseline fit. Similar procurement blueprints in the Philippines and Canada cement a long runway for the degaussing systems market.

Increased Deployment of Magnetic-Influence Sea Mines Driving Demand for Magnetic Signature Control

Modern mines combine magnetic, acoustic, and pressure sensors, elevating precise field suppression requirements. The validation of India's multi-influence ground mine exemplifies the rising lethality that naval planners must counter. Historical loss figures reveal that mines remain the most cost-effective anti-surface weapon, anchoring the need for robust degaussing across blue-water and littoral vessels.

Elevated Capital Expenditure and Long-Term Maintenance Costs Limit Broader Adoption

The substantial upfront investment and ongoing operational expenses associated with advanced degaussing systems create adoption barriers, particularly for smaller naval forces with constrained budgets. Comprehensive degaussing installations can represent 2-5% of total vessel construction costs, and HTS-based packages command premiums that exceed copper-coil alternatives by 40-60%. Specialized lifecycle support-including cryogenic cooling plants, helium logistics, and certified technicians-adds USD 2-4 million over a 10-year maintenance horizon for a mid-sized combatant. These financial realities often force navies to confine full-spectrum signature management to aircraft carriers, submarines, and frontline destroyers while accepting residual magnetic footprints on lower-priority hulls. Consequently, market penetration among emerging maritime nations lags because capital charges crowd out other combat-system upgrades.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Retrofit Initiatives Targeting Older Surface Vessels for Degaussing Upgrades

- Emergence of High-Temperature Superconducting Coil Technology Enabling Compact and Efficient Systems

- Supply-Chain Vulnerabilities for HTS Tape and Rare-Earth-Based Magnetic Sensors Hinder Production Scalability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The segment totals underline how covert platforms anchor spending. The submarines category accounted for 29.65% of degaussing systems market revenue in 2024, while mine counter-measure ships will expand fastest at 7.89% CAGR. This performance differential mirrors the pronounced threat from influence mines and the strategic premium on under-ice and littoral concealment. Submarine programmes in Australia, India, and South Korea integrate full-hull coil sets at the design stage, contrasting with surface ships where retrofitting is the norm. Mine-hunter hulls already built with low-ferrite composites still add distributed micro-loops to crush residual magnetism. Destroyers and frigates maintain sizeable demand because mid-life upgrades coincide with radar and sonar refresh cycles, creating a multiplier effect for degaussing work scopes.

Navies weigh vessel-specific risk exposure when allocating budgets. Submarines face continuous passive detection risk and thus justify high-spec proprietary materials. Conversely, corvettes adopt modular architectures that spread costs using standardized coil modules rated for regional magnetic conditions. The nuanced mix obliges suppliers to field configurable systems ranging from 30-meter unmanned craft to 100,000-ton carriers without rewriting control code.

Continuous degaussing systems cornered 60.90% of 2024 revenue, highlighting their status as a baseline fit. Though degaussing remains core, deperming has re-emerged because modern steels retain higher remanence after repeated polar transits. A 6.12% CAGR through 2030 underscores how navies view periodic demagnetization as vital insurance before deployment into mined chokepoints. Contemporary pierside deperming cages employ pulsed direct current techniques capable of 95.5% flux-density reduction in half the legacy processing time. Additionally, portable deperming mats allow frigates to reset signatures during patrols without returning to home dock, raising operational readiness and underpinning a positive outlook for the deperming slice of the degaussing systems market.

Although a smaller niche, ranging facilities close the feedback loop by providing empirical magnetic-field data. Software analytics extrapolate these readings into coil-current setpoints, demonstrating that even lower-revenue segments create pull-through for higher-margin digital services.

The Degaussing Systems Market Report is Segmented by Vessel Type (Aircraft Carriers, Destroyers, Frigates, Corvettes, Submarines, and More), Solution (Degaussing, Deperming, and Ranging), Component (Control Units, Power Amplifiers, Coils and Cabling, and More), Installation Type (New-Build Installation and Retrofit), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 34.17% of 2024 revenue. The US Navy's destroyer and cruiser service-life-extension contracts alone sustain a multi-billion-dollar pipeline that favors domestically produced coils, magnetometers, and control units. Canada's Kingston-class degaussing refits and allied Foreign Military Sales (FMS) cases further reinforce the region's standing. With three qualified HTS testbeds, North American yards host the most advanced superconducting deployment programmes worldwide.

Asia-Pacific will post the highest 8.80% CAGR through 2030. Rising defense budgets and contested sea lanes propel demand. Japan extends HTS trials to its Mogami-class frigates, while Australia's AUKUS submarine endeavour integrates magnetic-signature management standards that exceed legacy benchmarks. India's mine programme, coupled with Southeast Asian littoral fleet expansion, accelerates the adoption of micro-degaussing solutions for unmanned platforms. Chinese shipyards embed AI-driven field-tuning software across new Type 054B builds, setting regional technology pace and prompting peers to keep up.

Europe remains pivotal, galvanized by NATO's Baltic and High North posture. Italy's mine-hunter initiative and France's FDI frigate series incorporate deperming and ranging combinations that drive systems-of-systems procurement. The United Kingdom's Type 31 programme specifies digital-twin-validated coil layouts as standard, underscoring regional commitment to magnetic hygiene. Parallel investments in polar research icebreakers introduce civil maritime niches for degaussing vendors, diversifying revenue streams beyond combatants.

- L3Harris Technologies Inc.

- Wartsila Corporation

- Polyamp AB

- Larsen & Toubro Limited

- Exail SAS

- IFEN S.p.A.

- American Superconductor Corporation (AMSC)

- Dayatech Merin Sdn Bhd

- DA Group

- Ultra Electronics Holdings Ltd.

- Babcock International Group

- Thales Group

- ESCO Technologies inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising naval modernization budgets accelerating investment in degaussing systems

- 4.2.2 Increased deployment of magnetic-influence sea mines driving demand for magnetic signature control

- 4.2.3 Expansion of retrofit initiatives targeting older surface vessels for degaussing upgrades

- 4.2.4 Emergence of high-temperature superconducting (HTS) coil technology enabling compact and efficient systems

- 4.2.5 Integration of AI-powered adaptive algorithms for real-time signature management

- 4.2.6 Growing requirement for systems in stealthy unmanned surface and underwater vehicles

- 4.3 Market Restraints

- 4.3.1 Elevated capital expenditure and long-term maintenance costs limit broader adoption

- 4.3.2 Extended acquisition timelines due to complex defense procurement procedures

- 4.3.3 Resource reallocation toward emerging railgun and directed-energy weapon systems reduces funding availability

- 4.3.4 Supply-chain vulnerabilities for HTS tape and rare-earth-based magnetic sensors hinder production scalability

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Vessel Type

- 5.1.1 Aircraft Carriers

- 5.1.2 Destroyers

- 5.1.3 Frigates

- 5.1.4 Corvettes

- 5.1.5 Submarines

- 5.1.6 Mine Countermeasure Vessels

- 5.1.7 Other Vessel Types

- 5.2 By Solution

- 5.2.1 Degaussing

- 5.2.2 Deperming

- 5.2.3 Ranging

- 5.3 By Component

- 5.3.1 Control Units (DCU)

- 5.3.2 Power Amplifiers

- 5.3.3 Coils and Cabling

- 5.3.4 Magnetometers and Sensors

- 5.3.5 Software and Analytics

- 5.4 By Installation Type

- 5.4.1 New-Build Installation

- 5.4.2 Retrofit

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 L3Harris Technologies Inc.

- 6.4.2 Wartsila Corporation

- 6.4.3 Polyamp AB

- 6.4.4 Larsen & Toubro Limited

- 6.4.5 Exail SAS

- 6.4.6 IFEN S.p.A.

- 6.4.7 American Superconductor Corporation (AMSC)

- 6.4.8 Dayatech Merin Sdn Bhd

- 6.4.9 DA Group

- 6.4.10 Ultra Electronics Holdings Ltd.

- 6.4.11 Babcock International Group

- 6.4.12 Thales Group

- 6.4.13 ESCO Technologies inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment