|

시장보고서

상품코드

1851947

바이오 계면활성제 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Biosurfactants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

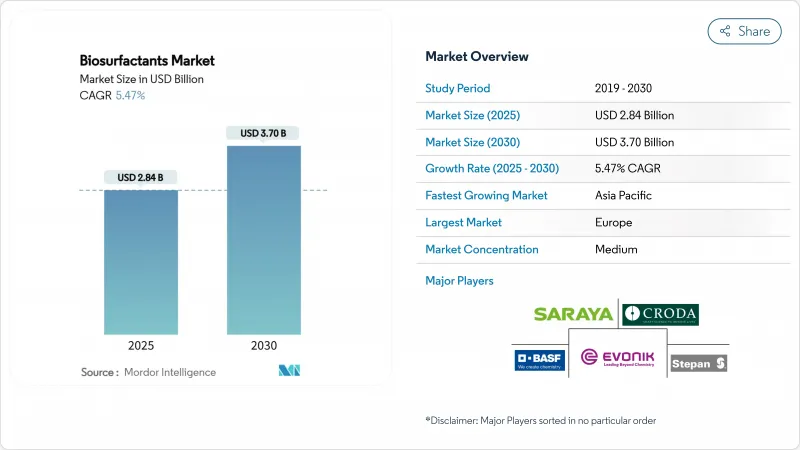

바이오 계면활성제 시장 규모는 2025년에 28억 4,000만 달러, 예측기간(2025-2030년)의 CAGR은 5.47%를 나타내고, 2030년에는 37억 달러에 달할 것으로 예측됩니다.

생분해성 성분에 대한 강력한 정책명령, 대규모 발효에 있어서의 꾸준한 돌파구, 퍼스널케어와 유전 화학 용도 수요 증가가 이 궤도를 총체적으로 지원하고 있습니다. 생산자는 저비용 폐기물 기질을 통합하고 급성장하는 아시아태평양 공급 기지가 세계 무역 흐름을 재구성함에 따라 생산 경제성은 미생물 합성에 기울기 시작했습니다. 경쟁 전략의 핵심은 업스트림 원료와 다운스트림 정제를 모두 제어하는 것입니다.

세계 바이오 계면활성제 시장 동향과 통찰

APAC의 개인 관리 및 화장품 수요 증가

이 지역의 소득 성장과 소비자의 "깨끗한 라벨" 성분에 대한 전환은 천연 유래의 온화한 계면 활성제에 대한 수요를 강화하고 있습니다. 당지질 분자는 탁월한 피부과학적 적합성을 통해 이러한 요구에 부응하며, 배합자에게 합성 에톡실레이트를 대체하는 명확한 옵션을 제공합니다. BASF는 레인포레스트 얼라이언스 인증의 야자유 계면활성제 Dehyton PK45GA/RA를 발표함으로써 이에 부응하여 피부 친화적인 스킨케어 제품을 타겟으로 했습니다. 현지 제조업체는 팜 핵과 코코넛 공급망에 가까운 것을 이용하여 비용을 더욱 압축하고 납품 사이클을 단축하고 있습니다. 소비자의 기대 증가와 구조적 공급 우위를 결합함으로써 바이오 계면활성제 시장은 퍼스널케어의 주류 채용을 향해 가속화되고 있습니다. 결국 이 변화는 아시아태평양의 유럽의 특수 계면활성제에 대한 수입 의존도를 낮추어 세계 무역 패턴의 균형을 되찾을 것으로 예측됩니다.

EU와 미국에서 생분해성 계면활성제의 규제 강화

유럽 연합(EU)의 세제 규제 갱신은 디지털 제품 여권, 엄격한 생분해성 지표, 인 함량 상한(phosphorus ceiling)을 도입하며 화석 유래 계면활성제의 재제조 비용이 높아지는 조치를 취했습니다. 이와 병행하여 미국 환경보호청은 유해물질 규제법(Toxic Substances Control Act)에 등록을 확대하여 로커스 인제엔츠의 Amphi 바이오 계면활성제 전제품을 대상으로 했습니다. 이러한 정책의 움직임은 바이오 계면활성제가 본질적인 우위를 지닌 대서양을 넘어 컴플라이언스 회랑을 형성하고 있습니다. 새로운 기준을 충족하는 기업은 보다 신속한 제품 인가를 확보하고 가격과 성능과 함께 지속가능성 점수를 중시하게 된 대형 소매업체의 선반 공간을 지킬 수 있습니다. 따라서 규제의 확실성은 바이오 계면활성제 시장 침투율 향상에 직결됩니다.

식품 및 의약품 등급 재료의 엄격한 순도 표준

식품 및 의약품의 최종 용도는 낮은 엔도톡신 수준과 배치 사이의 일관성이 요구되므로 하류에서 다단계 연마가 필요합니다. 각 공정에서 자본 지출과 수율 손실이 발생하여 상품 원가가 상승합니다. 규제기관은 새로운 바이오서팩트 부형제를 승인하기 전에 안전 서류와 알레르겐 연구를 요구하고 상업적 일정을 늦추고 있습니다. 소규모 기업에는 이러한 연구에 자금을 제공하는 자원이 없는 경우가 많으며, 자본력이 있는 기존 기업만이 이러한 프리미엄 부문을 추구할 수 있습니다. 그 결과, 시장은 이분화되고 벌크의 상품 수요는 꾸준히 성장하고 있지만, 초고순도 틈새는 진입 장벽에 의해 보호되고 있습니다.

부문 분석

당지질은 2024년 바이오 계면활성제 시장 점유율의 69.28%를 차지했으며, 수량 기준이든 수익 기반이든 구조적 우위성을 확인했습니다. 또한 2030년까지 연평균 복합 성장률(CAGR)은 가장 빠른 5.90%로 단일 분자 클래스를 중심으로 규모의 경제가 계속 구축되고 있음을 뒷받침하고 있습니다. 에보닉 슬로바키아 공장에서 상업화된 람노리피드는 최적화된 슈도모나스 발효를 통해 상품 생산량을 유지하고 전환 비용을 낮출 수 있음을 보여줍니다. 소홀로리피드는 최첨단 당지질이며, 2025년에 파일럿 라인을 가동시키는 호리펠름사와 같은 신규 참가 기업을 끌고 있습니다. 경쟁업체와의 차별화는 현재 균주 공학 및 통합 정제를 다루는 지적 재산의 폭넓은 곳으로 이동하고 있습니다.

서팩틴과 같은 리포펩티드는 항균 작용이 계면활성제와 활성 성분의 이중 효용을 초래하는 농업 바이오컨트롤로 점유율을 확대합니다. 인지질은 소규모이지만, 상처 치유 크림이나 점적 제제로 큰 이득을 가져, 그 인간 세포 적합성으로부터 프리미엄 가격이 설정되어 있습니다. 고분자의 바이오 계면활성제와 리케니신은 산업용 탈지와 고온유 추출이라는 기술적 틈새를 차지하고 있어 내열성이 요구됩니다. 바이오 계면활성제 시장 규모가 확대됨에 따라 제품의 다양성이 여러 가격 사다리를 지원하고 공급업체가 범용품과 특수품의 이익을 균형을 잡을 수 있도록 진화하는 포트폴리오가 제시합니다.

바이오 계면활성제 보고서는 제품 유형(당지질, 인지질, 계면활성제, 리케니신 등), 원료(식물성 기름, 산업 폐기 글리세롤, 농업 잔류물, 기타), 용도(세제·공업용 클리너, 화장품, 식품 가공, 유전 화학제품, 기타), 지역(아시아태평양, 동아프리카, 남아메리카, 남미)

지역 분석

정착한 생명공학 인프라와 식물성 기름래 투입물을 우대하는 엄격한 환경정책에 따라 유럽이 2024년 매출액의 52.15%를 차지했습니다. 세제 지침의 갱신은 더 높은 생분해성 임계값을 의무화하여 수요를 강화하여 유럽 생산자의 대응 가능한 양을 확대하고 있습니다. 에보닉의 산업용 람노 리피드 플랜트와 BASF의 RSPO 인증 계면활성제 라인 등의 시설은 자국의 리더십을 유지하기 위한 자본 헌신을 반영하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 6.14%로 성장하여 주요 수요의 중심지가 될 것으로 예측됩니다. 중국은 정밀 발효 및 산업용 바이오파크 인프라 정비에 많은 투자를 하고 바이오 계면활성제의 대량 생산을 위한 국내 생산 능력을 구축하고 있습니다. 인도에서는 확대하는 중산계급이 퍼스널케어 지출을 견인하는 한편, 식물성 기름 농장에 근접하고 있기 때문에 원료 로지스틱스가 효율적으로 유지됩니다. 일본의 제제 제조업체는 화장품용의 고순도 당지질을 요구하고 있어, 선진적인 규제 제도를 활용해 가격 프리미엄을 획득하고 있습니다.

북미는 EPA(환경보호국)의 승인과 연방 정부의 바이오 이코노미 보조금 등 유리한 정책 신호로부터 혜택을 받는 대규모 기반을 유지하고 있습니다. 이 지역에는 대규모 제조업과 에너지 부문이 있기 때문에 산업용 세정제와 유전용 화학약품이 여전히 가장 강력한 견인 요인이 되고 있습니다. 남미에는 풍부한 원료가 있어, 제조 비용은 경쟁력이 있지만, 발효 인프라가 한정되어 있기 때문에 생산량은 적습니다. 중동 및 아프리카는 틈새 비즈니스 기회를 개척하고 있습니다. 걸프 석유 회사는 유층 자극에 람노 리피드를 사용하는 파일럿 테스트를 실시하고, 아프리카 소비재 회사는 도시 시장을 위한 식물성 클리너를 테스트하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아태평양의 개인 관리 및 화장품 수요 증가

- EU와 미국에서의 생분해성 계면활성제의 규제 강화

- FMCG 메이저의 브랜드 레벨에서의 지속가능성에의 헌신

- 발효의 스케일업 비용 절감 곡선

- 바이오 계면활성제 기반 SKU에 대한 탄소 상쇄 크레딧

- 시장 성장 억제요인

- 석유계 계면활성제에 대한 높은 생산 비용

- 식품 및 제약 등급 재료에 대한 엄격한 순도 사양

- 생산주에 관한 특허의 복잡성

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 당지질

- 인지질

- 서팩틴

- 리케니신

- 고분자 바이오 계면활성제

- 기타 제품 유형

- 원료별

- 식물성 기름(콩, 팜, 유채)

- 산업폐기물 글리세롤

- 농업 잔류물(당밀, 유청)

- 기타(동물성 유지, 합성 당류)

- 용도별

- 세제 및 공업용 클리너

- 화장품(퍼스널케어)

- 식품가공

- 유전용 화학제품

- 농업 화학제품

- 섬유

- 기타 용도

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- AGAE Technologies, LLC

- AmphiStar Biosurfactants

- BASF

- Biotensidon GmbH

- Croda International Plc

- Dispersa Inc.

- Ecover

- Evonik Industries AG

- Givaudan

- GlycoSurf

- Jeneil Biotech

- Kaneka Corporation

- Saraya.Co.Ltd

- Stepan Company

- Syensqo

- TeeGene Biotech

- TensioGreen

- WHEATOLEO

제7장 시장 기회와 장래의 전망

SHW 25.11.25The Biosurfactants Market size is estimated at USD 2.84 billion in 2025, and is expected to reach USD 3.70 billion by 2030, at a CAGR of 5.47% during the forecast period (2025-2030).

Robust policy mandates for biodegradable ingredients, steady breakthroughs in large-scale fermentation, and rising demand from personal care and oilfield chemicals applications collectively anchor this trajectory. Production economics have begun tilting toward microbial synthesis as producers integrate low-cost waste substrates, while fast-growing Asia-Pacific supply hubs reshape global trade flows. Competitive strategies now revolve around controlling both upstream feedstock and downstream purification, a shift that favors companies with vertically integrated operations.

Global Biosurfactants Market Trends and Insights

Expansion of Personal-Care and Cosmetics Demand in APAC

Regional income growth and a consumer pivot toward "clean label" ingredients have intensified demand for mild surfactants that are naturally derived. Glycolipid molecules meet this need through excellent dermatological compatibility, giving formulators a clear alternative to synthetic ethoxylates. BASF responded by unveiling Dehyton PK45 GA/RA, a Rainforest Alliance-certified coconut-oil surfactant that targets gentle skin-care products. Local manufacturers leverage proximity to palm kernel and coconut supply chains to further compress costs and shorten delivery cycles. This combination of rising consumer expectations and structural supply advantages accelerates the biosurfactants market toward mainstream personal-care adoption. Over time the shift is expected to rebalance global trade patterns by lowering Asia-Pacific's import dependence on European specialty surfactants.

Regulatory Push for Biodegradable Surfactants in EU and US

The European Union's updated detergent regulation introduces digital product passports, stringent biodegradability metrics, and phosphorus ceilings, measures that make fossil-based surfactants costlier to reformulate. In parallel, the U.S. Environmental Protection Agency expanded Toxic Substances Control Act registration to cover Locus Ingredients' full Amphi biosurfactant line, sending a clear acceptance signal for microbial surfactants across industrial uses. These synchronized policy moves create a trans-Atlantic compliance corridor in which biosurfactants hold an intrinsic advantage. Companies meeting the new criteria secure faster product approvals, protecting shelf space at major retailers that now rank sustainability scores alongside price and performance. Regulatory certainty, therefore, translates directly into rising biosurfactants market penetration.

Tight Purity Specs for Food and Pharma-Grade Material

Food and pharmaceutical end uses require low endotoxin levels and batch-to-batch consistency, which demand multistep downstream polishing. Each step adds capital expense and yield losses, inflating cost of goods. Regulatory bodies insist on safety dossiers and allergen studies before approving new biosurfactant excipients, slowing commercial timelines. Small firms often lack resources to fund these studies, allowing only well-capitalized incumbents to pursue these premium segments. The result is a bifurcated market in which bulk commodity demand grows steadily but ultra-high-purity niches remain protected by entry barriers.

Other drivers and restraints analyzed in the detailed report include:

- Brand-Level Sustainability Commitments by FMCG Majors

- Fermentation Scale-Up Lowering Cost Curves

- Patent Thickets Around Production Strains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Glycolipids captured 69.28% of the biosurfactants market share in 2024, confirming their structural dominance in both volume and revenue terms. They also deliver the fastest 5.90% CAGR to 2030, underscoring how economies of scale continue to build around a single molecular class. Rhamnolipid commercialization at Evonik's Slovak plant shows that optimized Pseudomonas fermentation can sustain commodity output and drive down conversion costs. Sophorolipids represent the most advanced glycolipid variant and attract new entrants like Holiferm that commission pilot lines in 2025. Competitive differentiation now shifts toward intellectual-property breadth, covering strain engineering and integrated purification.

Lipopeptides such as surfactin gain share in agricultural biocontrol, where antimicrobial action offers dual utility as a surfactant and active ingredient. Phospholipids remain small but deliver outsized margins in wound-healing creams and intravenous formulations where their human-cell compatibility commands premium pricing. Polymeric biosurfactants and lichenysin occupy technical niches, industrial degreasing and high-temperature oil extraction, requiring thermal resilience. The evolving portfolio demonstrates that as the biosurfactants market size broadens, product diversity supports multiple price ladders, enabling suppliers to balance commodity volumes with specialty profits.

The Biosurfactants Report is Segmented by Product Type (Glycolipids, Phospholipids, Surfactin, Lichenysin, and More), Feedstock (Vegetable Oils, Industrial Waste Glycerol, Agricultural Residues, Others), Application (Detergents and Industrial Cleaners, Cosmetics, Food Processing, Oilfield Chemicals, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Europe anchored 52.15% of 2024 revenue through entrenched biotechnology infrastructure and stringent environmental policy that favors plant-based inputs. Updated detergent directives strengthen demand by mandating higher biodegradability thresholds, thereby expanding addressable volumes for European producers. Facilities such as Evonik's industrial rhamnolipid plant and BASF's RSPO-certified surfactant lines reflect capital commitment to maintaining home-region leadership.

Asia-Pacific is forecast to grow at 6.14% CAGR to 2030, turning into the primary demand center. China directs considerable state investment toward precision fermentation and industrial bio-park infrastructure, creating domestic capacity for large-volume biosurfactant output. India's expanding middle class drives personal-care spending, while proximity to vegetable-oil plantations keeps raw-material logistics efficient. Japanese formulators seek high-purity glycolipids for cosmeceuticals, leveraging the country's advanced regulatory system to command price premiums.

North America maintains a sizable base that benefits from favorable policy signals, including EPA approvals and federal bio-economy grants. Given the region's large manufacturing and energy sectors, industrial cleaning and oilfield chemicals remain the strongest pull factors. South America's feedstock abundance offers competitive manufacturing costs, but limited fermentation infrastructure keeps output small. Middle East and Africa develop niche opportunities; Gulf oil producers run pilot trials using rhamnolipids for reservoir stimulation, while African consumer goods companies test plant-based cleaners for urban markets.

- AGAE Technologies, LLC

- AmphiStar Biosurfactants

- BASF

- Biotensidon GmbH

- Croda International Plc

- Dispersa Inc.

- Ecover

- Evonik Industries AG

- Givaudan

- GlycoSurf

- Jeneil Biotech

- Kaneka Corporation

- Saraya.Co.Ltd

- Stepan Company

- Syensqo

- TeeGene Biotech

- TensioGreen

- WHEATOLEO

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Personal-Care and Cosmetics Demand In APAC

- 4.2.2 Regulatory Push for Biodegradable Surfactants in EU and US

- 4.2.3 Brand-Level Sustainability Commitments by FMCG Majors

- 4.2.4 Fermentation Scale-Up Lowering Cost Curves

- 4.2.5 Carbon-Offset Credits for Biosurfactant-Based SKUs

- 4.3 Market Restraints

- 4.3.1 High Production Cost Vs Petro-Surfactants

- 4.3.2 Tight Purity Specs for Food and Pharma-Grade Material

- 4.3.3 Patent Thickets around Production Strains

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Glycolipids

- 5.1.2 Phospholipids

- 5.1.3 Surfactin

- 5.1.4 Lichenysin

- 5.1.5 Polymeric Bio-surfactants

- 5.1.6 Other Product Types

- 5.2 By Feedstock

- 5.2.1 Vegetable Oils (soy, palm, rapeseed)

- 5.2.2 Industrial Waste Glycerol

- 5.2.3 Agricultural Residues (molasses, whey)

- 5.2.4 Others (Animal Fat, Synthesised Sugars)

- 5.3 By Application

- 5.3.1 Detergents and Industrial Cleaners

- 5.3.2 Cosmetics (Personal Care)

- 5.3.3 Food Processing

- 5.3.4 Oilfield Chemicals

- 5.3.5 Agricultural Chemicals

- 5.3.6 Textiles

- 5.3.7 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 AGAE Technologies, LLC

- 6.4.2 AmphiStar Biosurfactants

- 6.4.3 BASF

- 6.4.4 Biotensidon GmbH

- 6.4.5 Croda International Plc

- 6.4.6 Dispersa Inc.

- 6.4.7 Ecover

- 6.4.8 Evonik Industries AG

- 6.4.9 Givaudan

- 6.4.10 GlycoSurf

- 6.4.11 Jeneil Biotech

- 6.4.12 Kaneka Corporation

- 6.4.13 Saraya.Co.Ltd

- 6.4.14 Stepan Company

- 6.4.15 Syensqo

- 6.4.16 TeeGene Biotech

- 6.4.17 TensioGreen

- 6.4.18 WHEATOLEO

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment