|

시장보고서

상품코드

1851991

전자처방전 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)E-prescribing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

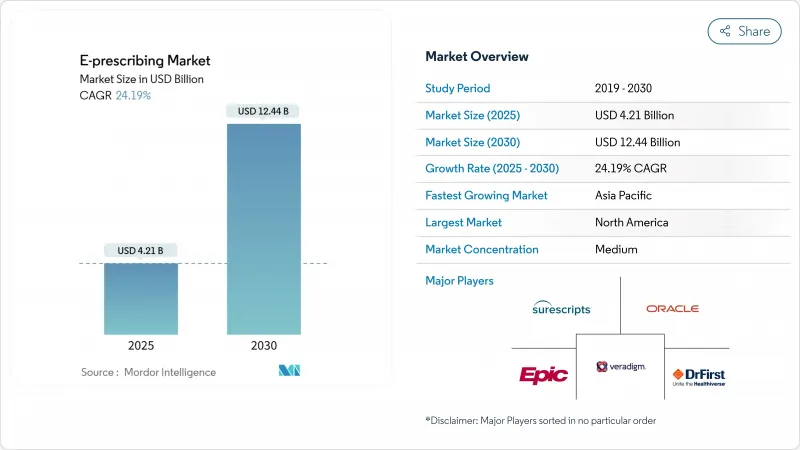

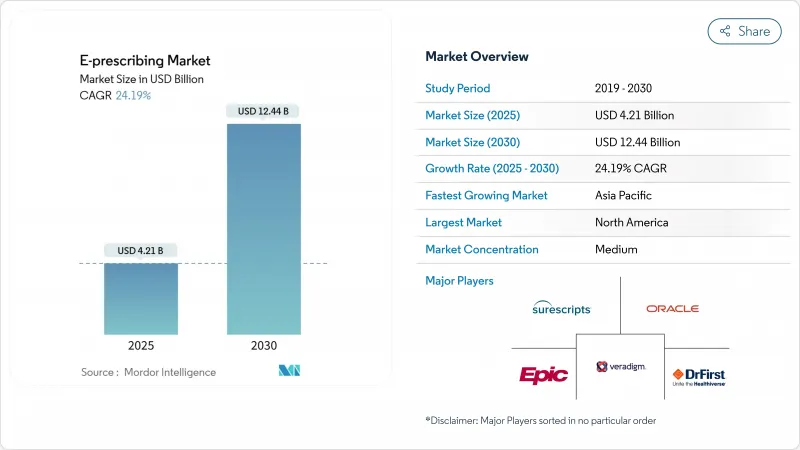

전자처방전 시장 규모는 2025년에 42억 1,000만 달러에 이르고, 2030년에는 124억 4,000만 달러에 달하며, CAGR 24.19%를 나타낼 것으로 예측됩니다.

규제의 의무화, 헬스케어의 디지털화, 미국에서 매년 약 2,500억 달러의 비용이 들고 있는 처방전 부정을 억제할 필요성 등이 계속해서 수요를 가속화하고 있습니다. 의약품 단체국이 2025년 12월까지 스케줄 II-V의 약제의 원격 처방의 유연성을 확대하기로 결정한 것도 그 기세를 뒷받침하고 있습니다. 병원, 클리닉, 약국, 성장하는 원격 의료 네트워크에 급속한 도입으로 전자처방전 시장은 강력한 성장 궤도를 유지하고 있습니다.

북미는 2024년에 전자처방전 시장의 38.54%를 차지하고, 메디케어·메디케이드 서비스 센터(CMS)가 2023년에 시행한, 규제 약물 처방의 적어도 70%를 전자적으로 쓰는 것을 의료 제공업체에게 의무화하는 규칙이 돌풍이 되었습니다. 아시아태평양은 마이 넘버 카드를 전자처방전에 연결시키는 일본의 의료 DX 프로그램과 간병, 보험, 의약품 공급망을 연결하는 중국의 3 의료 제휴 개혁에 의해 2030년까지 연평균 복합 성장률(CAGR) 25.45%를 나타낼 전망입니다. 2024년 점유율은 소프트웨어가 65.45%로 우위를 유지했지만, 서비스가 CAGR 26.45%로 가장 급성장하고 있습니다. 통합 EHR 또는 병원 정보 시스템의 이용률은 72.34%이지만, 모바일 퍼스트 앱이 CAGR 26.56%로 상승하고 있습니다. 클라우드 딜리버리는 54.34%로 톱, 규제 약물(EPCS)은 38.54%로 최대의 처방 클래스를 형성하고 있지만, 특수 의약품은 CAGR 25.67%로 급성장하고 있습니다.

세계의 전자처방전 시장 동향과 인사이트

처방전자화의 정부에 의한 의무화

전자처방전의 의무화로 세계 처방전 워크플로우가 재조합되고 있습니다. DEA(마약 단속국)가 가까이 발표하는 특별 등록 프레임워크는 원격 의료 허가에 3개의 계층을 도입하고, 임상의에게 주별 원격 의료 자격을 보유하고, 일정 II-V 약물의 전자처방전을 사용하도록 의무화하고 있습니다. 캘리포니아 주에서는 2022년 1월 이후 규제의 유무에 관계없이 모든 처방전을 전자화하는 규칙이 제정되어 현재 35개 주가 EPCS법을 시행하는 등 의무화가 급속히 확대되고 있음을 나타냅니다. CMS는 이미 2028년 1월에 NCPDP SCRIPT 표준 버전 2023011로의 마이그레이션을 확인했으며, 시스템은 실시간 혜택 도구 및 강화된 처방 데이터를 지원하도록 요청하고 있습니다. 주 처방약 모니터링 프로그램을 점검하는 연방 정부의 요건은 3년 이내에 실시될 예정이며, 전자처방전이 규제 약물의 유일한 안전한 경로임을 더욱 확실히 하고 있습니다. 이러한 연쇄 규칙은 전자처방전 시장을 유기 성장을 훨씬 넘어 견인하는 대체 사이클을 생성합니다.

투약의 안전성과 케어의 질에 대한 주목의 향상

미국에서는 연간 12만 5,000명의 사망으로 이어지는 실수를 줄이기 위해 환자 안전 관점에서 건강 관리 시스템에 고급 처방 도구의 도입이 요구되고 있습니다. Surescripts의 Sig IQ는 2024년에 41억 명의 환자의 지시를 번역하고 자유 텍스트를 구조화된 지시로 변환하여 부작용으로 인한 긴급 외래 진찰을 줄였습니다. Epic Systems는 100개 이상의 AI 기반 처방 관리 기능을 통합하여 상호작용을 스크리닝하여 최적의 투여를 제안합니다. DEA는 또한 EPCS에 0.001 미만의 오조합률을 가진 생체인증을 요구하고 있으며, 프리미엄 플랫폼이 선호되는 보안 요구가 높아지고 있습니다. 약물 치료 관리 시스템은 현재 처방 내역과 실시간 복약 보험 모니터링을 결합하여 연간 2,500억 달러의 복약 보험 위반 비용을 처리합니다. 실시간 혜택 도구는 화면 비용과 수식 피드백을 통해 처방전 당 37달러를 절약하고 안전성을 더욱 높입니다.

데이터 프라이버시 및 사이버 보안에 대한 우려

건강 관리는 여전히 ransomware의 모습의 표적입니다. Change Healthcare의 공격으로 미국 환자의 1/3 이상의 처방전 워크플로가 중단되어 긴급한 종이 기반 프로세스를 강요했습니다. DEA는 또한 범죄자가 대량의 부정한 처방전을 만들 수 있도록 하는 EHR 자격증 도용에 대해 경고합니다. 의료 사이버 보안 개선법과 같은 입법안은 메디케어의 지불을 보안의 준비에 연결하는 것으로, 소규모 진료소에 있어서는 비용 부담이 늘어나게 됩니다. 이중 인증, 디지털 서명, 심층 감사 추적의 의무화는 운영의 복잡성을 더욱 향상시킵니다. 지방 및 소규모 의료 제공업체는 엄격한 요구 사항을 충족하기 위한 자금과 전문 지식이 부족한 경우가 많으며, 도입이 지연되고 충분한 서비스를 받지 못한 지역의 전자처방전 시장을 좁히고 있습니다.

부문 분석

2024년 매출의 65.45%는 소프트웨어로, 이는 병원 및 클리닉의 핵심 라이선스 수요를 반영했습니다. 한편, CAGR 26.45%를 나타낼 것으로 예측되는 서비스는 도입 지원, 규제 지침, 지속적인 최적화를 중시하는 조직의 동향을 반영하고 있습니다. Surescripts의 2024년에 41억 Sig IQ 지침은 기본 데이터 전송에서 부가가치 투약 관리로의 전환을 보여주었습니다.

서비스 붐은 기술만으로는 처방의 과제를 해결할 수 없습니다고 보강하고 있습니다. 현재는 좌학 연수, 변경 관리 워크숍, 헬프 데스크의 아웃소싱이 일상적으로 실시되고 있습니다. 이러한 서비스의 상승은 벤더에게 구독과 같은 끈질긴 수입을 가져오고 성숙한 지역에서도 전자처방전 시장을 유지합니다. DEA 바이오메트릭과 향후 SCRIPT 표준을 수용하기 위한 업그레이드는 이 부문의 장기 성장 궤도를 보장합니다.

통합 EHR 또는 HIS 솔루션은 2024년 전자처방전 시장의 72.34%를 차지하며, 케어 워크플로에 통합된 역할을 활용했습니다. 모바일 퍼스트 앱은 회진이나 왕진시에 즉시 주문 엔트리를 가능하게 하는 안전한 태블릿이나 스마트폰 덕분에 CAGR26.56%로 추격하고 있습니다. 독립형 시스템은 EHR의 전반적인 도입이 현실적이지 않은 틈새 환경에서 그 중요성을 유지합니다.

Epic의 AI 대응 처방 툴의 파도는 EHR 대기업이 점유율을 지키는 한편, 중소의 모바일 참가 기업이 사용 용이성과 초기 비용이 낮게 경쟁하고 있음을 나타냅니다. 모바일 솔루션은 아웃리치 프로그램, 팝업 클리닉 및 재해 지역을 지원합니다. 그러나 통합 제품군은 복잡한 다기능 관리에 필수적인 검사 값, 문제 목록 및 의사 결정 지원 기능에 대한 더 깊은 액세스를 제공합니다.

지역 분석

북미가 2024년에 38.54%의 점유율을 차지하고 전자처방전 시장을 독점했습니다. 이것은 성숙한 네트워크 인프라와 강력한 연방 정부의 의무에 의해 지원됩니다. Surescripts사는 같은 해 미국 플랫폼에서 25억 건의 처방전을 라우팅하여 보급의 정착상을 부각시켰습니다. 변경 건강 관리의 침해와 같은 사이버 보안의 지속적인 사건과 데이터 공유의 지속적인 과제는 이 지역의 미래 투자 요구를 강조하지만, 메디케어와 민간 보험에 통합된 인센티브가 성장세를 유지하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 25.45%로 가장 빠른 궤도를 기록했습니다. 일본은 전국민의 마이 넘버 ID와 처방 이력을 링크시킨 전국 규모의 데이터베이스를 전개하고, 중국은 3의료 제휴 정책 아래 치료-보험-약국의 통합 네트워크를 구축하고 있습니다. 인도, 한국 및 호주 정부는 마찬가지로 전국 의약품 모니터링 시스템을 선호하고 있으며, 공급업체가 레거시 제약 없이 클라우드 및 모바일 솔루션을 도입할 수 있는 비약적인 기회를 창출하고 있습니다. 중국에서는 2027년까지 1,380억 달러의 헬스케어 지출이 예측되고 있으며, 전자처방전 시장 확대의 여지가 큽니다.

유럽에서는 독일의 e-Rezept 프로그램과 NHS의 모바일 앱에 의한 처방 서비스가 꾸준한 진전을 보이며 현재는 매월 310만건의 재진료 의뢰에 대응하고 있습니다. EU27개국에 걸쳐 다양한 규제 환경이 하모나이제이션을 늦추고 있지만, 엄격한 데이터 보호의 틀은 소비자의 신뢰를 높이고 있습니다. 브라질, 사우디아라비아, 아랍에미리트(UAE)에서는 공공 부문의 디지털화가 초기 프로젝트를 이끌고 있습니다. 따라서 세계적인 전망은 북미와 유럽에서 성숙한 사용과 아시아태평양에서 급속한 스케일 업, 신흥 지역에서 선택적 시험적 도입이 결합되어 전자처방전 시장의 장기적인 성장을 유지합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전자처방전 도입에 대한 정부의 의무

- 의약품의 안전성과 의료의 질에 대한 주목 고조

- 의료비 절감과 업무 효율화의 필요성

- 클라우드 기반 의료 IT 인프라의 보급 확대

- 텔레헬스와 디지털 약국의 생태계 확대

- 새로운 가치 기반 의료와 약가의 투명성

- 시장 성장 억제요인

- 데이터 프라이버시와 사이버 보안에 대한 우려

- 상호 운용성과 데이터 표준화의 부족

- 의료 제공업체의 워크플로우 붕괴와 사용성 장벽

- 소규모 및 농촌에 있어서 한정된 기술적 전문성

- 규제 상황

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 구성 요소별

- 하드웨어

- 소프트웨어

- 서비스

- 시스템 유형별

- 독립형 시스템

- 통합 EHR/HIS 시스템

- 모바일 우선 앱

- 배포 모드별

- 클라우드 기반

- 웹 기반

- On-Premise

- API Platform-as-a-Service

- 처방 유형별

- 신규 처방

- 재처방/갱신

- 규제 약물(EPCS)

- 특수 의약품

- 최종 사용자별

- 병원

- 클리닉

- 약국 및 우편 주문

- 원격의료 공급자

- 지리

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Veradigm LLC

- Surescripts

- Epic Systems Corporation

- Oracle(Cerner)

- DrFirst

- eClinicalWorks

- NextGen Healthcare

- MEDITECH

- Greenway Health

- Practice Fusion

- McKesson(CoverMyMeds)

- Omnicell

- RelayHealth(Change Healthcare)

- RxNT

- DoseSpot

- CompuGroup Medical(eMDs)

- WellSky

- Altera Digital Health

제7장 시장 기회와 향후 전망

KTH 25.11.18The electronic prescribing market size reached USD 4.21 billion in 2025 and is forecast to climb to USD 12.44 billion by 2030, advancing at a 24.19% CAGR.

Regulatory mandates, healthcare digitization, and the need to curb prescription fraud that costs the United States about USD 250 billion every year continue to accelerate demand. Momentum is further supported by the Drug Enforcement Administration's decision to extend telemedicine prescribing flexibilities for Schedule II-V medications through December 2025. Rapid adoption across hospitals, clinics, pharmacies, and growing telehealth networks keeps the electronic prescribing market on a robust growth path.

North America held 38.54% of the electronic prescribing market in 2024, lifted by the Centers for Medicare & Medicaid Services (CMS) rule obligating providers to write at least 70% of controlled substance prescriptions electronically, with enforcement that began in 2023. Asia-Pacific is expanding at a 25.45% CAGR through 2030 due to Japan's medical DX program that links My Number cards to electronic prescriptions and China's three-medical linkage reforms that connect care, insurance, and pharmaceutical supply chains. Software remained dominant with 65.45% share in 2024, yet services are the fastest-growing component at 26.45% CAGR. Integrated EHR or hospital information systems account for 72.34% of usage, but mobile-first apps are rising at 26.56% CAGR. Cloud delivery leads with 54.34%, and controlled substances (EPCS) form the largest prescription class at 38.54%, while specialty drugs grow fastest at 25.67% CAGR.

Global E-prescribing Market Trends and Insights

Government Mandates for Electronic Prescription Adoption

Mandatory e-prescribing laws are realigning prescription workflows worldwide. The DEA's forthcoming special registration framework introduces three tiers of telemedicine authorization, obliging clinicians to hold state-specific telemedicine credentials and use electronic prescriptions for Schedule II-V drugs. California's rule that all prescriptions-controlled or not-be electronic since January 2022 shows how quickly mandates expand, with 35 states now enforcing EPCS legislation. CMS has already confirmed the transition to NCPDP SCRIPT Standard version 2023011 in January 2028, compelling systems to support real-time benefit tools and enhanced formulary data. A federal requirement to check state Prescription Drug Monitoring Programs is set for implementation within three years, further cementing e-prescribing as the only secure route for controlled substances. These cascading rules create a replacement cycle that drives the electronic prescribing market far beyond organic growth.

Rising Focus On Medication Safety And Quality Of Care

Patient-safety imperatives push healthcare systems to adopt advanced prescribing tools that reduce errors linked to 125,000 deaths a year in the United States. Surescripts' Sig IQ translated 4.1 billion patient directions in 2024, converting free text to structured instructions that cut emergency department visits for adverse events. Epic Systems embedded more than 100 AI-based prescription management features that screen interactions and suggest optimal dosing. The DEA also requires biometric authentication with a false match rate below 0.001 for EPCS, escalating security needs that favor premium platforms. Medication therapy management systems now combine prescription histories with real-time adherence monitoring, addressing USD 250 billion in annual non-adherence costs. Real-time benefit tools further enhance safety by saving patients USD 37 per prescription through on-screen cost and formulary feedback.

Data Privacy And Cybersecurity Concerns

Healthcare remains a prime ransomware target. The Change Healthcare attack interrupted prescription workflows for more than one-third of U.S. patients, forcing emergency paper-based processes. The DEA has also warned about EHR credential theft that allows criminals to generate massive volumes of fraudulent scripts. Legislative proposals like the Health Care Cybersecurity Improvement Act would tie Medicare payments to security readiness, adding cost burdens for small practices. Mandatory two-factor authentication, digital signatures, and detailed audit trails further raise operating complexity. Rural or small providers often lack funds and expertise to meet stringent requirements, slowing adoption and narrowing the electronic prescribing market in underserved regions.

Other drivers and restraints analyzed in the detailed report include:

- Need For Healthcare Cost Reduction And Operational Efficiency

- Growing Penetration Of Cloud-Based Healthcare IT Infrastructure

- Lack Of Interoperability And Data Standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024 software accounted for 65.45% of revenue, reflecting core licensing demand across hospitals and clinics. Services, however, projected at a 26.45% CAGR, underline how organizations now value onboarding support, regulatory guidance, and continuous optimization. Surescripts' 4.1 billion Sig IQ instructions in 2024 illustrate a shift from basic data transport to value-added medication management.

The services boom reinforces that technology alone does not solve prescribing challenges. Implementation now routinely covers classroom training, change-management workshops, and help-desk outsourcing. This service overlay creates sticky, subscription-like income for vendors and sustains the electronic prescribing market even in mature geographies. Recurrent upgrades to meet DEA biometrics or upcoming SCRIPT standards secure the segment's long-term growth trajectory.

Integrated EHR or HIS solutions held 72.34% of the electronic prescribing market in 2024, capitalizing on their embedded role in point-of-care workflow. Mobile-first apps are catching up with a 26.56% CAGR thanks to secure tablets and smartphones that enable immediate order entry during rounds or home visits. Stand-alone systems stay relevant in niche environments where full EHR rollouts remain impractical.

Epic's wave of AI-enabled prescribing tools demonstrates how EHR giants defend share, while smaller mobile entrants compete on usability and low upfront cost. Mobile solutions also serve outreach programs, pop-up clinics, and disaster zones. Yet integrated suites still provide deeper access to lab values, problem lists, and decision support-capabilities crucial for complex polypharmacy management.

The E-Prescribing Market Report is Segmented by Component (Hardware, and More), Type of System (Stand-Alone Systems, and More), Delivery Mode (Cloud-Based, Web-Based, and More), Prescription Type (NewRx. And More), End User (Hospitals, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America dominated the electronic prescribing market with 38.54% share in 2024, sustained by mature network infrastructure and strong federal mandates. Surescripts routed 2.5 billion prescriptions on its U.S. platform that year, highlighting entrenched adoption. Persistent cybersecurity events such as the Change Healthcare breach and ongoing data-sharing challenges underscore the region's future investment needs, yet incentives embedded in Medicare and commercial insurance maintain growth momentum.

Asia-Pacific posted the fastest trajectory at 25.45% CAGR through 2030. Japan is rolling out a nationwide database that links every citizen's My Number ID to prescription histories, while China builds integrated treatment-insurance-pharmacy networks under its three-medical linkage policy. Governments in India, South Korea, and Australia are equally prioritizing national drug monitoring systems, creating leapfrog opportunities that let providers deploy cloud and mobile solutions without legacy constraints. A projected USD 138 billion healthcare outlay in China by 2027 offers substantial room for electronic prescribing market expansion.

Europe exhibits steady progress driven by Germany's e-Rezept program and the NHS mobile-app prescription service that now handles 3.1 million repeat requests monthly. Diverse regulatory environments across 27 EU states slow harmonization, but strict data-protection frameworks bolster consumer trust. South America along with the Middle East & Africa remain nascent but attractive; public-sector digitization drives early projects in Brazil, Saudi Arabia, and the United Arab Emirates. The global outlook therefore pairs mature usage in North America and Europe with rapid scale-up in Asia-Pacific and selective pilot adoption across emerging regions, sustaining long-term growth for the electronic prescribing market.

- Veradigm

- Surescripts

- Epic Systems

- Oracle

- DrFirst

- eClinicalWorks

- NextGen Healthcare

- Meditech

- Greenway Health

- Practice Fusion

- McKesson (CoverMyMeds)

- Omnicell

- RelayHealth (Change Healthcare)

- RxNT

- DoseSpot

- CompuGroup Medical (eMDs)

- WellSky

- Altera Digital Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Mandates for Electronic Prescription Adoption

- 4.2.2 Rising Focus on Medication Safety And Quality of Care

- 4.2.3 Need For Healthcare Cost Reduction and Operational Efficiency

- 4.2.4 Growing Penetration of Cloud-Based Healthcare IT Infrastructure

- 4.2.5 Expansion of Telehealth and Digital Pharmacy Ecosystems

- 4.2.6 Emerging Value-Based Care and Medication Price Transparency

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cybersecurity Concerns

- 4.3.2 Lack of Interoperability and Data Standardization

- 4.3.3 Provider Workflow Disruption and Usability Barriers

- 4.3.4 Limited Technical Expertise in Small and Rural Practices

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Type of System

- 5.2.1 Stand-alone Systems

- 5.2.2 Integrated EHR/HIS Systems

- 5.2.3 Mobile-first Apps

- 5.3 By Delivery Mode

- 5.3.1 Cloud-based

- 5.3.2 Web-based

- 5.3.3 On-premise

- 5.3.4 API Platform-as-a-Service

- 5.4 By Prescription Type

- 5.4.1 NewRx

- 5.4.2 Refill / Renewal

- 5.4.3 Controlled Substances (EPCS)

- 5.4.4 Specialty Drugs

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Clinics

- 5.5.3 Pharmacies & Mail-order

- 5.5.4 Telehealth Providers

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Veradigm LLC

- 6.3.2 Surescripts

- 6.3.3 Epic Systems Corporation

- 6.3.4 Oracle (Cerner)

- 6.3.5 DrFirst

- 6.3.6 eClinicalWorks

- 6.3.7 NextGen Healthcare

- 6.3.8 MEDITECH

- 6.3.9 Greenway Health

- 6.3.10 Practice Fusion

- 6.3.11 McKesson (CoverMyMeds)

- 6.3.12 Omnicell

- 6.3.13 RelayHealth (Change Healthcare)

- 6.3.14 RxNT

- 6.3.15 DoseSpot

- 6.3.16 CompuGroup Medical (eMDs)

- 6.3.17 WellSky

- 6.3.18 Altera Digital Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment