|

시장보고서

상품코드

1852031

유럽의 심장 모니터링 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Europe Cardiac Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

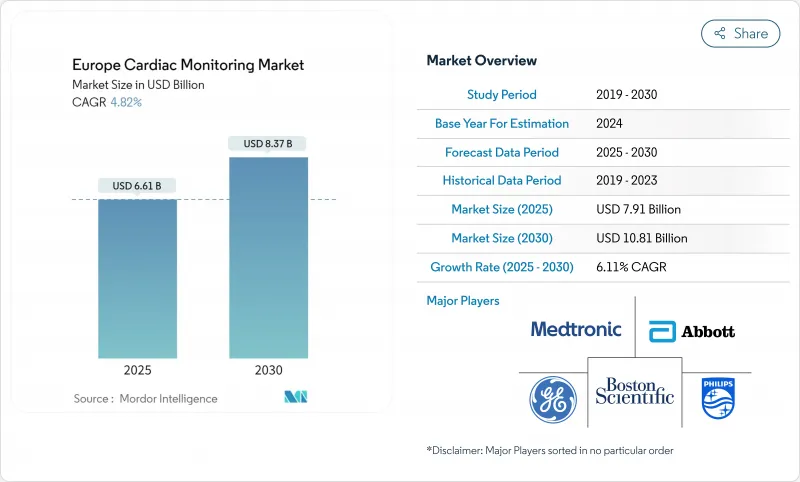

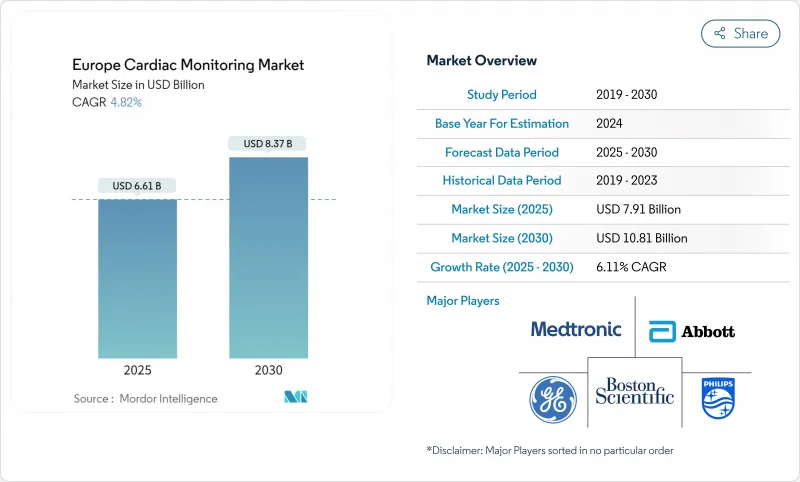

유럽의 심장 모니터링 시장은 2024년에 79억 1,000만 달러를 창출했고 CAGR 6.11%를 나타내, 2030년에는 108억 1,000만 달러에 이를 것으로 예측되고 있습니다.

이 오른쪽 어깨 상승의 성장을 지지하고 있는 것은 인구 동태의 고령화, 심혈관 질환 유병률의 상승, 조기 발견과 재택 관리에 보답하는 진료 보수 개혁입니다. 인공지능 알고리즘이 오보를 줄이고 외래 데이터가 임상적으로 실용적이 됨에 따라 병원 내 진단에서 지속적인 원격 모니터링으로의 이동이 가속화되고 있습니다. 규제 당국의 지원(특히 독일과 프랑스의 새로운 DRG 코드)은 의료 제공업체의 도입 위험을 더욱 감소시키고 병원의 용량 제약이 가상 병동 모델을 뒷받침하고 있습니다. 경쟁의 심각성은 여전히 완만하며 기존의 임베디드 장비 제조업체는 클라우드에서 리듬 데이터를 분석하는 소프트웨어 우선 기업과 경쟁하고 있습니다. 지속적인 장벽으로는 EU-MDR 컴플라이언스 비용과 GDPR(EU 개인정보보호규정) 의무 등을 들 수 있지만, 원격 심부전 연구에서 원격 모니터링은 재입원을 크게 줄이고 장기적인 수요를 유지하는 것으로 확인되었습니다.

유럽의 심장 모니터링 시장 동향과 인사이트

노화하는 유럽 인구에서 심혈관 질환의 유병률 상승

현재 고령자 코호트가 청소년을 능가하고 있으며 심혈관 질환으로 인한 연간 사망자 수는 이미 390만 명에 달할 전망입니다. 심방세동, 심부전, 복잡한 부정맥의 이환율 증가로 인해 혼잡한 병원 밖에서 작동하는 확장 가능한 진단이 요구되고 있습니다. 의료 시스템의 플래너는 에피소드적인 개입보다는 오히려 만성적인 케어 플랫폼에 자본을 돌리고 심장 모니터링이 중요한 인프라로 정착하고 있습니다. 독일, 프랑스, 이탈리아는 가장 이환율이 가파르며 이식 가능한 루프 레코더와 긴 수명 원격 측정 패치에 적합합니다. 지속적인 리듬 감시는 유럽 보건 연합의 목표에 부합하는 2차 예방 프로그램도 지원합니다.

EU의 의료 시스템 전반에서 외래 및 원격 심장 모니터링으로 이동

국가의 의료 서비스는 병상 부족과 간호 업무 부담을 줄이기 위해 가상 병동과 재택 ECG 패치에 눈을 돌리고 있습니다. 영국의 초기 데이터는 퇴원 전환 시 환자에게 AI 분석된 웨어러블 모니터를 장착하면 병원 재입원률이 감소하는 것으로 나타났습니다. 이탈리아와 스웨덴의 유사한 조종사는 클라우드 대시보드를 전자 의료 기록에 직접 통합하여 임상가가 병리 악화 전에 치료를 조정할 수 있도록 합니다. 이러한 분산화는 보다 집에 가까이 있는 케어를 추진하고, 이동에 의한 이산화탄소 배출량을 삭감하고, 환자의 만족도를 향상시키는 EU의 광범위한 정책과 동기화하고 있습니다.

엄격한 EU-MDR 규정 준수 비용

5,000유로에서 50만 유로의 인증료가 종합적인 임상 서류와 시판 후 감시를 요구하기 때문에 소규모 이노베이터는 포트폴리오를 축소하거나 대규모 기존 기업에 의한 인수를 모색하기 어렵습니다. 이 규정은 환자의 안전성을 강화하는 것이지만, AI 소프트웨어 업데이트를 지연시키고 신형 센서 시장 출시까지 시간을 늘릴 수 있습니다.

부문 분석

ECG 디바이스 시장 규모는 2024년에 42.23%의 매출을 차지하며, 최전선 진단으로서의 모달리티의 지위를 뒷받침했습니다. 실시간 데이터 전송과 자동 방어에 의해 지원되는 모바일 원격 측정은 즉시 개입 경보에 대한 임상의 수요를 반영하며 CAGR 6.98%를 나타낼 전망입니다. 이식형 루프 레코더는 현재 최대 6년의 배터리 수명을 제공하여 뇌졸중 임상 검사에 매력적인 제품이 되고 있습니다. 홀터 모니터는 24시간에서 48시간의 검사용으로 특히 신속한 대응이 중요한 1차 케어 현장에서 틈새를 유지하고 있습니다. 스마트 웨어러블은 소비자의 라이프 스타일 추적과 임상 등급의 정확성을 다루고 위험을 인식하는 젊은 사용자의 참여를 확대합니다. 이러한 기기에 내장된 AI는 기존의 스냅샷에서는 놓쳐져 있던 미묘한 심방세동 에피소드를 연속적인 스트림에서 찾아내 모니터링을 반응적인 것에서 예측적인 것으로 변화시킵니다. 듀얼 챔버 리드리스 페이스메이커의 규제 승인은 장비 선택을 더욱 넓히고 교차 판매 기회를 촉진합니다. 텔레메트리가 성장함에 따라 조달 예산은 하드웨어 단위보다 클라우드 대시보드 및 구독 분석에 돌입할 수 있습니다.

이 가속화를 통해 유럽의 심장 모니터링 시장에서 공급업체는 센서와 장기적인 소프트웨어 라이선스를 번들로 제공합니다. Patch-as-a-Service 계약은 대규모 선행 구매를 위한 자금이 부족한 병원 그룹에 호소하는 반면 제조업체는 지속적인 수익 가시성을 제공합니다. 경쟁사와의 차별화는 노이즈 감소 알고리즘, 환자 친화적인 접착제, 전자 의료 기록과의 상호 운용성에 달려 있습니다. 학술센터가 재입원률 감소를 입증하는 결과 데이터를 발표함에 따라 지불자의 신뢰는 상환 경로를 강화합니다. 이러한 원동력이 결합되어 모바일 텔레메트리는 주요 성장 엔진으로서의 역할을 확실히 하고, 이 분야는 10년 후까지 기존의 홀터 검사 대수를 추월할 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 유럽의 고령화 사회에 있어서 심혈관 질환의 유병률 상승

- EU의 의료 시스템 전체에서 외래 및 원격 심장 모니터링으로 이동

- 웨어러블 ECG 디바이스의 기술적 진보

- DRG와 국가 탈리프 일정에 근거한 유리한 상환 갱신

- 홀터 데이터에 있어서 AI 주도의 예측 분석 통합

- 중동 유럽에서 원격 심장 병학 허브의 출현

- 시장 성장 억제요인

- 엄격한 EU-MDR 대응 비용

- GDPR(EU 개인정보보호규정)의 데이터 프라이버시에 대한 우려가 원격 모니터링의 보급을 제한

- 주변 지역에서 훈련을 받은 전기 생리학자의 부족

- 장기 이식형 레코더의 배터리와 데이터 스토리지의 한계

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 바이어의 힘

- 공급자 파워

- 대체품의 위협

- 신규 참가업체의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 심전도 장치

- 홀터 모니터

- 이벤트 레코더

- 이동형 심장 원격 측정 장치

- 이식형 루프 레코더

- 스마트 웨어러블 모니터

- 최종 사용자별

- 병원

- 심장센터 및 클리닉

- 홈케어

- 외과 외래 센터

- 기타

- 국가별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Medtronic plc

- GE HealthCare Technologies Inc.

- Koninklijke Philips NV

- Abbott Laboratories

- Boston Scientific Corporation

- Biotronik SE & Co. KG

- Nihon Kohden Corporation

- Hillrom(Baxter)

- iRhythm Technologies Inc.

- AliveCor Inc.

- Schiller AG

- Mindray Medical International Ltd.

- Spacelabs Healthcare(OSI Systems)

- Bittium Corporation

- Withings SA

- Cardiologs Technologies SAS

- LivaNova PLC

- MicroPort Scientific

- Lepu Medical Technology

제7장 시장 기회와 향후 전망

KTH 25.11.18The Europe cardiac monitoring market generated USD 7.91 billion in 2024 and is forecast to expand at a 6.11% CAGR to reach USD 10.81 billion by 2030.

Underpinning this steady climb are demographic aging, rising cardiovascular disease prevalence, and reimbursement reforms that reward early detection and home-based management. The shift from episodic, in-hospital diagnostics to continuous remote monitoring is accelerating as artificial-intelligence algorithms reduce false alarms, making ambulatory data clinically actionable. Regulatory support-most notably new DRG codes in Germany and France-further de-risks provider adoption, while hospital capacity constraints encourage virtual-ward models. Competitive intensity remains moderate; established implantable-device manufacturers now vie with software-first firms that analyze rhythm data in the cloud. Persistent barriers include EU-MDR compliance costs and GDPR obligations, yet evidence from multicountry tele-heart-failure studies confirms that remote monitoring materially cuts readmissions, sustaining long-term demand.

Europe Cardiac Monitoring Market Trends and Insights

Rising Prevalence of Cardiovascular Diseases Among Europe's Ageing Population

An older cohort now outnumbers youth, and cardiovascular disease already contributes 3.9 million annual deaths, or 45% of all fatalities in the region who.int. Higher rates of atrial fibrillation, heart failure, and complex arrhythmias demand scalable diagnostics that operate outside crowded hospitals. Health-system planners are channeling capital toward chronic-care platforms rather than episodic interventions, cementing cardiac monitoring as critical infrastructure. Germany, France, and Italy face the steepest incidence curves, creating fertile ground for implantable loop recorders and long-life telemetry patches. Continual rhythm surveillance also supports secondary prevention programs that align with European Health Union objectives.

Shift Toward Ambulatory & Remote Cardiac Monitoring Across EU Health Systems

National health services are turning to virtual wards and home-based ECG patches to relieve bed shortages and nursing workloads. Early data from the United Kingdom shows hospital readmission rates falling when patients are fitted with AI-analyzed wearable monitors during discharge transitions nice.org.uk. Similar pilots in Italy and Sweden integrate cloud dashboards directly into electronic patient records, enabling clinicians to adjust therapy before decompensation events. This decentralization synchronizes with broader EU policy that pushes care closer to home, reduces carbon footprints from travel, and elevates patient satisfaction scores.

Stringent EU-MDR Compliance Costs

Certification fees ranging from EUR 5,000 to EUR 500,000 require comprehensive clinical dossiers and post-market surveillance, forcing smaller innovators either to curtail portfolios or seek acquisition by larger incumbents ema.europa.eu. Although the regulation fortifies patient safety, it may delay AI-software updates and prolong time-to-market for novel sensors.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Wearable ECG Devices

- Favourable Reimbursement Updates Under DRG & National Tariff Schedules

- Data-Privacy Concerns Under GDPR Limiting Remote-Monitoring Uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Europe cardiac monitoring market size for ECG devices accounted for 42.23% revenue in 2024, underscoring the modality's status as frontline diagnostics. Mobile telemetry, aided by real-time data transmission and automated triage, is on track for a 6.98% CAGR, reflecting clinician demand for immediate intervention alerts. Implantable loop recorders now offer up to six years of battery life, making them attractive for cryptogenic stroke workups. Holter monitors keep a niche for 24- to 48-hour studies, especially in primary-care settings where quick turnaround matters. Smart wearables bridge consumer lifestyle tracking and clinical-grade accuracy, expanding engagement among younger risk-aware users. AI embedded within these devices mines continuous streams for subtle atrial-fibrillation episodes that traditional snapshots miss, transforming monitoring from reactive to predictive. Regulatory approvals for dual-chamber leadless pacemakers further broaden device options and spur cross-selling opportunities. Taken together, telemetry's growth reorients procurement budgets toward cloud dashboards and subscription analytics rather than standalone hardware.

Following this acceleration, the Europe cardiac monitoring market is witnessing suppliers bundle sensors with longitudinal software licenses. Patch-as-a-service contracts appeal to hospital groups that lack capital for large upfront purchases, while giving manufacturers recurring revenue visibility. Competitive differentiation now hinges on noise-reduction algorithms, patient-friendly adhesives, and interoperability with electronic health records. As academic centers publish outcome data validating lower rehospitalization rates, payer confidence strengthens reimbursement pathways. These combined dynamics cement mobile telemetry's role as the principal growth engine and position the segment to overtake legacy Holter volume by the decade's end.

The Europe Cardiac Monitoring Market Report Segments the Industry Into Device Type (ECG Monitor, Event Recorder and More), B Technology (Conventional (Wired), Wireless & Wearable and More) End-Users (Hospitals & Clinics, Ambulatory Surgical Centers and More), and Country (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Medtronic

- GE HealthCare Technologies Inc.

- Koninklijke Philips

- Abbott Laboratories

- Boston Scientific

- BIOTRONIK

- Nihon Kohden

- Hillrom (Baxter)

- iRhythm Technologies

- AliveCor

- Schiller

- Mindray

- Spacelabs Healthcare (OSI Systems)

- Bittium Corporation

- Withings SA

- Cardiologs Technologies SAS

- LivaNova

- MicroPort

- Lepu Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of cardiovascular diseases among Europe's ageing population

- 4.2.2 Shift toward ambulatory & remote cardiac monitoring across EU health systems

- 4.2.3 Technological advancements in wearable ECG devices

- 4.2.4 Favourable reimbursement updates under DRG & national tariff schedules

- 4.2.5 Integration of AI-driven predictive analytics in Holter data

- 4.2.6 Emergence of tele-cardiology hubs in Central & Eastern Europe

- 4.3 Market Restraints

- 4.3.1 Stringent EU-MDR compliance costs

- 4.3.2 Data-privacy concerns under GDPR limiting remote-monitoring uptake

- 4.3.3 Shortage of trained electrophysiologists in peripheral regions

- 4.3.4 Battery & data-storage limits in long-term implantable recorders

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Buyer Power

- 4.7.2 Supplier Power

- 4.7.3 Threat of Substitutes

- 4.7.4 Threat of New Entrants

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type (Value)

- 5.1.1 ECG Devices

- 5.1.2 Holter Monitors

- 5.1.3 Event Recorders

- 5.1.4 Mobile Cardiac Telemetry

- 5.1.5 Implantable Loop Recorders

- 5.1.6 Smart Wearable Monitors

- 5.2 By End User (Value)

- 5.2.1 Hospitals

- 5.2.2 Cardiac Centres & Clinics

- 5.2.3 Home-Care Settings

- 5.2.4 Ambulatory Surgical Centres

- 5.2.5 Others

- 5.3 By Country (Value)

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Medtronic plc

- 6.3.2 GE HealthCare Technologies Inc.

- 6.3.3 Koninklijke Philips N.V.

- 6.3.4 Abbott Laboratories

- 6.3.5 Boston Scientific Corporation

- 6.3.6 Biotronik SE & Co. KG

- 6.3.7 Nihon Kohden Corporation

- 6.3.8 Hillrom (Baxter)

- 6.3.9 iRhythm Technologies Inc.

- 6.3.10 AliveCor Inc.

- 6.3.11 Schiller AG

- 6.3.12 Mindray Medical International Ltd.

- 6.3.13 Spacelabs Healthcare (OSI Systems)

- 6.3.14 Bittium Corporation

- 6.3.15 Withings SA

- 6.3.16 Cardiologs Technologies SAS

- 6.3.17 LivaNova PLC

- 6.3.18 MicroPort Scientific

- 6.3.19 Lepu Medical Technology

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment