|

시장보고서

상품코드

1852032

이탈리아의 내시경 검사 기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Italy Endoscopy Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

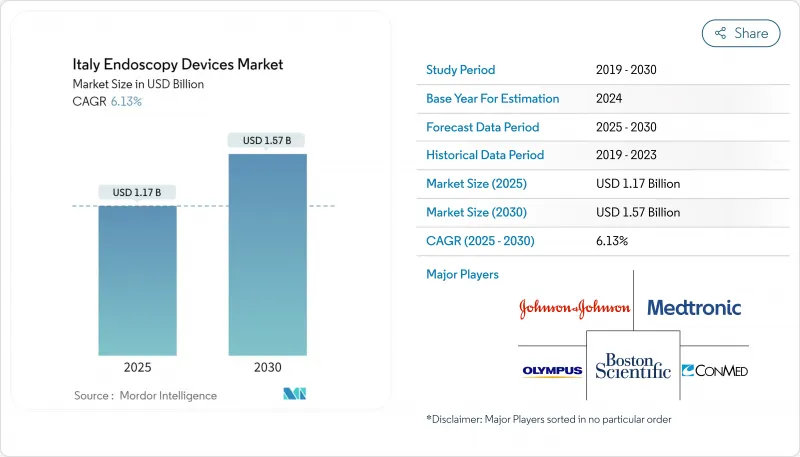

이탈리아의 내시경 검사 기기 시장은 2025년에 11억 7,000만 달러로 평가되며, 2030년에는 15억 8,000만 달러에 이를 것으로 예측됩니다.

이 기세는 소화기 질환의 이환율 상승, 인공지능을 활용한 영상진단의 임상적 수용 확대, 저침습 접근에 보답하는 정책적 지원 등이 겹친 것에 기인하고 있습니다. 당일치기 수술센터가 증가함에 따라 수요가 더욱 가속화되고 공급자는 일상 진단 및 치료 내시경 검사에 비용 효율적인 환경을 제공할 수 있습니다. 한편, 유럽 의료기기 규제(MDR)에 근거한 엄격한 재처리 규칙과 환자의 안전성에 대한 기대가 높아짐에 따라 일회용 액세서리의 인기가 높아지고 있습니다. 경제적 압력과 소규모 또는 남부 병원에서 불균일한 인력 배치의 상황은 성장을 억제하고 있지만, 보다 넓은 의미에서 상승 궤도에 미치는 것은 없습니다.

이탈리아 내시경 검사 기기 시장 동향과 인사이트

고령화의 진행에 따른 소화기 질환의 발생률 상승

이탈리아의 염증성 장 질환의 유병률은 2025년 인구 10만명당 218.3례에 달하고, 치료용 내시경 수요를 높이고 있습니다. IBD 환자의 입원률은 16.5%로, 6년간의 누적 수술 위험은 크론병에서 36%, 궤양성 대장염에서 20%로 여전히 높습니다. 그러므로 더 많은 전문센터가 있는 북부 지역에서는 조기 발견을 개선하고 수술로의 전환을 줄이기 위해 고급 영상 진단 장비와 고화질 유연한 범위를 구입합니다. 고령자층은 대장암 검진, 상부 소화관 출혈 관리, 만성 췌장염 평가 등의 수술 건수를 증가시켜, 복수년에 걸친 기기 갱신 예산을 지지하고 있습니다.

내시경 기술의 진보

클라우드 기반의 인공지능이 루틴의 대장 내시경 검사, 바렛 식도 모니터링, 궤양성 대장염의 스코어링을 확장. 올림푸스는 2024년 CADDIE, CADU, SMARTIBD의 CE 승인을 받았으며 2025년 상업 전개에 앞서 이탈리아에서 시험 도입을 시작했습니다. AI 엔진은 선종의 감지율을 높이고 전문의의 밀도가 고르지 않은 병원간에 품질을 표준화합니다. 통합된 클라우드 분석은 워크플로우 문서화를 간소화하고 MDR 컴플라이언스를 완화하고 차세대 비디오 프로세서 구매 결정을 가속화합니다.

고급 내시경 장비의 높은 비용

AI 지원 4K 타워 가격 태그는 종종 20만 유로(22만 6,597달러)를 초과합니다. 소규모 클리닉에서는 업그레이드가 지연되고 제조업체의 권장 사항을 넘어 감가상각 주기가 늘어나고 있습니다. MDR 규정 준수는 최종 사용자 정가에 영향을 주는 인증 비용을 추가합니다. 공급업체는 비용에 제약이 있는 구매자 간에 새로 고침 결정을 가속화하기 위해 임대 및 페이퍼 프로시저 플랜을 판매하는 경우가 늘고 있습니다.

부문 분석

액세서리 & 소모품 카테고리는 2030년까지 연평균 복합 성장률(CAGR) 13.8%를 나타내 감염 관리의 의무화에 의해 일회용 생검 집게, 스네어, 밸브의 채용에 박차가 걸리기 때문에 자본 설비를 상회합니다. 단일 사용 주입기 및 회수 그물은 교차 오염의 위험을 줄이고 세척 소독기의 능력이 제한된 시설에서 턴어라운드를 가속화합니다. 내시경은 올림푸스와 후지 필름의 고화질 연성 대장 내시경과 위 카메라에 지지되어 2024년 이탈리아의 내시경 검사 기기 시장 점유율 38%를 유지했습니다. 비디오 시스템에는 병변에 실시간으로 플래그를 지정하는 AI가 탑재되어 있어, 패스트 패스 진단의 정밀도가 높아지고 있습니다.

수술 장비도 혁신적이며, 특히 바이폴라 에너지 플랫폼과 제어식 CO2 배기구 펌프는 고급 절제를 용이하게 합니다. 액세서리 붐은 초기 자본 지출을 억제합니다. 공급업체는 대형 구매를 피하면서 각 기술에 대한 수익을 높이는 높은 처리량 소모품을 선호합니다. 단일 사용 범위의 바이오플라스틱 기반 핸들은 공급업체가 감염 대책과 지속가능성에 대한 고려 사항을 양립하는 방법을 보여줍니다.

2024년 이탈리아의 내시경 검사 기기 시장 규모는 대장암 검진과 궤양성 대장염의 모니터링에 힘입어 소화기내과가 56%의 점유율을 차지해 계속 기간 시장이 되었습니다. AI에 의한 폴립 검출은 선종 인식을 향상시키고 치료 액세서리와 호환되는 대형 채널 대장 내시경 수요를 강화합니다. 비만과 대사 수술은 ESG가 지불자의 지지와 환자의 수용을 얻으면서 CAGR 12.3%로 이 분야를 선도하고 있습니다. 이탈리아의 내시경 검사 기기 시장은 체중 관리를 목적으로 한 특수 봉합 장비와 위내 풍선 시스템에서 이익을 얻고 있습니다.

호흡기 내과는 관절 외장과 전자기 내비게이션에 의해 폐 말초 병변을 채취하는 유연한 경기관지침 생검이 대두하고 있습니다. 비뇨기과 및 부인과 분야에서는 병리학적 검출을 강화하는 협대역 영상 방광경과 자궁경이 채용되고 있습니다. 정형외과와 이비인후과에서는 외래환자의 관절경검사나 후두경검사용으로 초소형 내시경을 시용하여 이탈리아 내시경 검사 기기 시장의 유저층을 넓히고 있습니다. 신경학은 아직 개발 도상이지만, 낮은 침습 척추 수술을 위한 3D 시각화 플랫폼에 대한 투자를 모으고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화의 진전에 수반하는 소화기 질환 증가

- 내시경 기술의 진보

- 당일치기 수술센터의 확대가 플렉서블 내시경 보급을 가속

- 낮은 침습 수술에 대한 인식과 환자의 기호 향상

- 고급 치료 내시경에 대한 SSN 상환 개선

- 시장 성장 억제요인

- 고도 내시경 기기의 고비용

- 병원에서 훈련된 내시경 검사 서포트 스탭의 부족

- 경제적 제약과 예산의 한계

- 규제 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 내시경

- 유연 내시경

- 경성 내시경

- 캡슐 내시경

- 로봇 보조 내시경

- 일회용 내시경

- 영상 시스템

- 카메라 헤드

- 광원

- 영상 처리기

- 모니터 및 디스플레이

- 데이터 기록기 및 저장 장치

- 내시경 수술 기기

- 에너지 시스템

- 주입기 및 흡입 펌프

- 내시경 스테이플러 및 봉합 장치

- 회수 장치

- 유체 관리 시스템

- 액세서리 및 소모품

- 내시경

- 용도별

- 위장관학

- 호흡기학

- 비뇨기학

- 부인과

- 정형외과(관절경)

- 심장학

- 이비인후과 수술

- 신경학

- 비만 및 대사 수술

- 기타 용도

- 최종 사용자별

- 공립병원

- 사립병원 및 전문클리닉

- 외래 수술 센터(ASC)

- 사무실 기반 의사 진료 환경

- 위생별

- 재사용 내시경

- 일회용 내시경

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Olympus Corporation

- Karl Storz SE & Co. KG

- Fujifilm Holdings Corporation

- Boston Scientific Corporation

- Medtronic plc

- Pentax Medical(HOYA Corporation)

- CONMED Corporation

- Stryker Corporation

- Smith & Nephew plc

- Richard Wolf GmbH

- Cook Medical Inc.

- Steris plc

- Cantel Medical(Cantel Medical Italy)

- Ambu A/S

- Intuitive Surgical Inc.

- EFER Endoscopy

- SonoScape Medical Corp.

- Aohua Endoscopy

- Endotics

- ERBE Elektromedizin GmbH

- Inventis srl

제7장 시장 기회와 향후 전망

KTH 25.11.18The Italy endoscopy devices market was valued at USD 1.17 billion in 2025 and is forecast to reach USD 1.58 billion by 2030, translating into a 6.13% CAGR through the period.

Momentum stems from a confluence of rising gastrointestinal disease incidence, wider clinical acceptance of artificial-intelligence-enabled imaging, and policy support that rewards minimally invasive approaches. Demand accelerates further as day-surgery centers multiply, giving providers cost-effective settings for routine diagnostic and therapeutic endoscopy. Meanwhile, single-use accessories gain traction in response to stringent reprocessing rules under the European Medical Device Regulation (MDR) and heightened patient safety expectations. Economic pressures and uneven staffing conditions in smaller or southern hospitals temper growth but have not derailed the broader upward trajectory.

Italy Endoscopy Devices Market Trends and Insights

Rising Incidence of Gastrointestinal Diseases Coupled with Growing Aging Population

Italy's inflammatory bowel disease prevalence reached 218.3 cases per 100,000 residents in 2025, raising therapeutic endoscopy demand. Hospitalization persists at 16.5% for IBD patients, and cumulative six-year surgery risk remains high at 36% for Crohn's disease and 20% for ulcerative colitis. Northern regions, with more specialty centers, therefore buy advanced imaging towers and high-definition flexible scopes to improve early detection and reduce surgical conversions. An older demographic intensifies procedure volumes for colorectal cancer screening, upper GI bleeding management, and chronic pancreatitis assessment, supporting multi-year equipment replacement budgets.

Advancements in Endoscopic Technologies

Cloud-based artificial intelligence now augments routine colonoscopy, Barrett's Esophagus surveillance, and ulcerative colitis scoring. Olympus secured CE approval for CADDIE, CADU, and SMARTIBD in 2024, with Italian pilot deployments preceding the 2025 commercial rollout. AI engines raise adenoma detection rates and standardize quality across hospitals with uneven specialist density. Integrated cloud analytics also streamline workflow documentation, easing MDR compliance and accelerating purchasing decisions for next-generation video processors.

High Cost of Advanced Endoscopy Equipment

Price tags for AI-ready 4K towers often exceed EUR 200,000 (USD 226,597). Smaller clinics defer upgrades, extending depreciation cycles past manufacturer recommendations. MDR compliance adds certification expenses that funnel into end-user list prices. Vendors increasingly pitch leasing or pay-per-procedure plans to accelerate refresh decisions among cost-constrained buyers.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Day-Surgery Centers Accelerates Flexible Endoscope Adoption

- Growing Awareness and Patient Preference for Minimally Invasive Procedures

- Shortage of Trained Endoscopy Support Staff in Hospitals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Accessories & Consumables category will climb at a 13.8% CAGR through 2030, outstripping capital equipment as infection-control mandates spur adoption of disposable biopsy forceps, snares, and valves. Single-use injectors and retrieval nets lower cross-contamination risk and expedite turnaround in facilities with limited washer-disinfector capacity. Endoscopes maintained 38% Italy Endoscopy Devices market share during 2024, anchored by high-definition flexible colonoscopes and gastroscopes from Olympus and Fujifilm. Video systems increasingly embed AI to flag lesions in real time, enhancing first-pass diagnostic accuracy.

Operative devices also witness innovations, notably bipolar energy platforms and controlled CO2 insufflation pumps that facilitate advanced resections. The accessories boom moderates initial capital outlays; providers prioritize high-throughput consumables that boost revenue per procedure while avoiding large-ticket purchases. Bioplastic-based handles in single-use scopes illustrate how vendors couple infection control with sustainability concerns.

Gastroenterology remained the backbone with 56% share of Italy Endoscopy Devices market size in 2024, underpinned by colorectal cancer screening and ulcerative colitis monitoring. AI-assisted polyp detection improves adenoma recognition, which in turn reinforces demand for large-channel colonoscopes compatible with therapeutic accessories. Bariatric & Metabolic Surgery is pacing the field at a 12.3% CAGR as ESG gains payer backing and patient acceptance. The Italy Endoscopy Devices market benefits from specialized suturing devices and intragastric balloon systems aimed at weight management.

Pulmonology gains ground thanks to flexible transbronchial needle biopsies that sample peripheral lung lesions, aided by articulating sheaths and electromagnetic navigation. Urology and gynecology segments adopt narrow-band imaging cystoscopes and hysteroscopes that enhance pathology detection. Orthopedic and ENT specialties experiment with micro-endoscopes for outpatient arthroscopy and laryngoscopy, broadening the Italy endoscopy devices market user base. Neurology remains nascent but attracts investments in 3D visualization platforms for minimally invasive spine procedures.

The Italy Endoscopy Devices Market Report is Segmented by Product Type (Endoscopes, Visualization Systems, Endoscopy Operative Devices, and Accessories & Consumables), Application (Gastroenterology, Pulmonology, Gynecology, Cardiology, and More), End User (Public Hospitals, and More), Hygiene (Reusable Endoscopes and Single-Use Endoscopes). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Olympus

- Karl Storz

- FUJIFILM

- Boston Scientific

- Medtronic

- Pentax Medical (HOYA Corporation)

- Conmed

- Stryker

- Smiths Group

- Richard Wolf

- Cook Group

- Steris plc

- Cantel Medical (Cantel Medical Italy)

- Ambu

- Intuitive Surgical

- EFER Endoscopy

- SonoScape Medical Corp.

- Aohua Endoscopy

- Endotics

- Erbe Elektromedizin

- Inventis srl

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Gastrointestinal Diseases Coupled with Growing Aging Population

- 4.2.2 Advancements in Endoscopic Technologies

- 4.2.3 Expansion of Day-Surgery Centers Accelerates Flexible Endoscope Adoption

- 4.2.4 Growing Awareness and Patient Preference for Minimally Invasive Procedures

- 4.2.5 Improved SSN Reimbursement for Advanced Therapeutic Endoscopy

- 4.3 Market Restraints

- 4.3.1 High Cost of Advanced Endoscopy Equipment

- 4.3.2 Shortage of Trained Endoscopy Support Staff in Hospitals

- 4.3.3 Economic Constraints and Budget Limitations

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Endoscopes

- 5.1.1.1 Flexible Endoscopes

- 5.1.1.2 Rigid Endoscopes

- 5.1.1.3 Capsule Endoscopes

- 5.1.1.4 Robot-Assisted Endoscopes

- 5.1.1.5 Disposable (Single-Use) Endoscopes

- 5.1.2 Visualization Systems

- 5.1.2.1 Camera Heads

- 5.1.2.2 Light Sources

- 5.1.2.3 Video Processors

- 5.1.2.4 Monitors & Displays

- 5.1.2.5 Data Recorders & Storage

- 5.1.3 Endoscopy Operative Devices

- 5.1.3.1 Energy Systems

- 5.1.3.2 Insufflators & Suction Pumps

- 5.1.3.3 Endoscopic Staplers & Suturing Devices

- 5.1.3.4 Retrieval Devices

- 5.1.3.5 Fluid Management Systems

- 5.1.4 Accessories & Consumables

- 5.1.1 Endoscopes

- 5.2 By Application

- 5.2.1 Gastroenterology

- 5.2.2 Pulmonology

- 5.2.3 Urology

- 5.2.4 Gynecology

- 5.2.5 Orthopedic Surgery (Arthroscopy)

- 5.2.6 Cardiology

- 5.2.7 ENT Surgery

- 5.2.8 Neurology

- 5.2.9 Bariatric & Metabolic Surgery

- 5.2.10 Other Applications

- 5.3 By End User

- 5.3.1 Public Hospitals

- 5.3.2 Private Hospitals & Specialty Clinics

- 5.3.3 Ambulatory Surgery Centers

- 5.3.4 Office-Based Physician Settings

- 5.4 By Hygiene

- 5.4.1 Reusable Endoscopes

- 5.4.2 Single-Use Endoscopes

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Olympus Corporation

- 6.3.2 Karl Storz SE & Co. KG

- 6.3.3 Fujifilm Holdings Corporation

- 6.3.4 Boston Scientific Corporation

- 6.3.5 Medtronic plc

- 6.3.6 Pentax Medical (HOYA Corporation)

- 6.3.7 CONMED Corporation

- 6.3.8 Stryker Corporation

- 6.3.9 Smith & Nephew plc

- 6.3.10 Richard Wolf GmbH

- 6.3.11 Cook Medical Inc.

- 6.3.12 Steris plc

- 6.3.13 Cantel Medical (Cantel Medical Italy)

- 6.3.14 Ambu A/S

- 6.3.15 Intuitive Surgical Inc.

- 6.3.16 EFER Endoscopy

- 6.3.17 SonoScape Medical Corp.

- 6.3.18 Aohua Endoscopy

- 6.3.19 Endotics

- 6.3.20 ERBE Elektromedizin GmbH

- 6.3.21 Inventis srl

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment