|

시장보고서

상품코드

1852044

행동 재활 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Behavioral Rehabilitation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

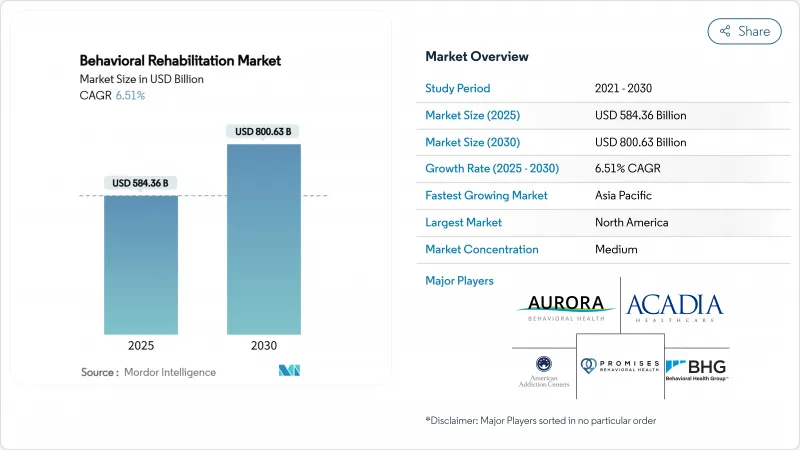

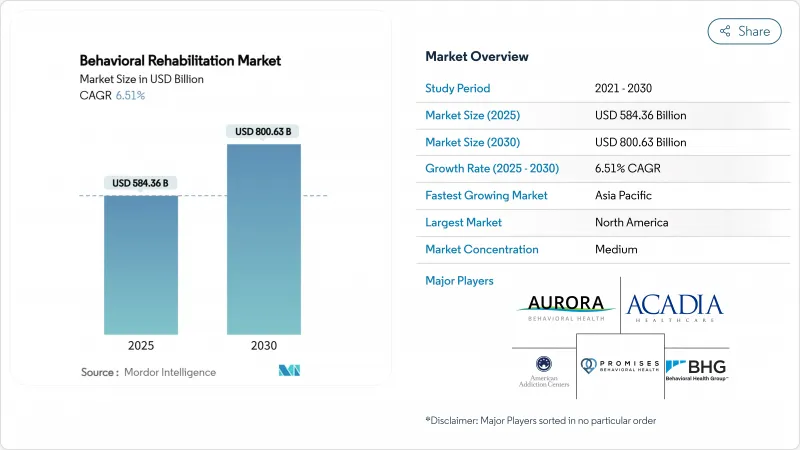

행동 재활 시장 규모는 2025년 5,843억 달러로 추정되고, 2030년에는 CAGR 6.51%로 성장할 전망이며, 8,006억 3,000만 달러로 확대될 것으로 예측됩니다.

견고한 수요는 정신 건강의 보급률 상승, 텔레헬스의 신속한 보급, 행동요법 및 의료 급여의 평등을 의무화하는 정책의 움직임으로 인해 발생합니다. 불안 장애는 진단과 치료를 요구하는 행동 증가를 반영하며, 2024년에는 31%로 최대의 행동 재활 시장 점유율을 유지했습니다. 외래 프로그램은 비용과 스티그마를 줄이는 지역 기반 모델로 37%의 매출을 차지했습니다. 가상 및 원격 재활의 틈새는 메디케어의 영구적인 유연성으로 원격 액세스가 가능해 CAGR 12.4%로 확대될 전망입니다. 북미는 42%의 매출을 이끌고 있지만, 아시아태평양은 공중 보건 캠페인과 가처분 소득 증가를 배경으로 CAGR 7%로 가장 빠른 성장을 기록했습니다.

세계의 행동 재활 시장 동향 및 인사이트

세계의 정신 건강 질환 부담 증가로 수요 가속화

정신질환의 세계적인 증가로 기존의 치료 능력이 향상되고 있습니다. 미국에서는 인구의 3분의 1이 정신건강 전문가 부족 지역에 살고 있으며, 서비스 필요성 및 가용성 사이에 격차가 있음을 보여줍니다. 약물 과다 복용으로 인한 사망자는 2021년에 10만 7,000명을 넘었으며, 치료되지 않은 행동 장애는 생산성 손실과 의료비로 연간 2,800억 달러의 손실을 미국 경제에 주고 있습니다. 이 수치는 모든 치료법에서 용량 확장의 필요성을 강조합니다.

커버리지 패리티를 향한 정부의 정책 전환

Mental Health Parity and Addiction Equity Act에 따른 최종 규칙은 2025년 1월 1일에 시행되며, 의료보험제도가 의료급여보다 엄격한 제한을 행동 의료에 적용하는 것이 금지됩니다. 의료보험은 네트워크의 타당성 및 이용 관리를 분석해야 합니다. CMS의 2025년 진료 보상 명세서에서는 FDA가 승인한 디지털 치료제 및 안전 계획 서비스를 위한 새로운 코드도 추가되어 의료 제공업체를 위한 새로운 상환의 길이 열립니다.

서비스 이용을 제한하는 근본적인 편견 및 문화적 장벽

2024년 기준에서 미국의 10대 청소년의 58.5%만이 충분한 감정 및 사회적 지원을 얻고 있다고 응답하고 있으며, 약물 남용 장애를 안고 있는 히스패닉계 미국인의 91%는 필요한 치료를 받지 못했습니다. 문화적 규범, 언어 격차, 공식적인 제도에 대한 불신감이 비록 서비스가 있어도 그 이용을 방해하고 있습니다. 이 홈을 채우기 위해서는 지역 사회에 뿌리를 둔 아웃리치, 이중 언어의 인재육성, 문화적으로 적절한 피어 서포트 모델이 필수적입니다.

부문 분석

불안장애는 2024년 시장 규모에 31.12% 기여했으며, 주요 부문으로서의 지위를 굳혔습니다. 진단률 증가와 보험 적용 범위 확대는 조기 개입을 촉진하고 AI 기반 모니터링 툴은 어드히어런스를 45% 향상시켰습니다. 모바일 앱을 통해 인지 행동 컨텐츠를 제공하는 디지털 치료제는 치료사가 주도하는 프로토콜을 강화하고 클리닉의 벽을 넘어 도달 범위를 확대합니다. 예를 들어, 몰입형 VR 노출 요법은 부적응 공포 반응을 재조정하고 치료 기간을 단축하는 데 도움이 됩니다.

약물 남용 장애는 2025-2030년 연평균 복합 성장률(CAGR) 7.81%로 성장할 것으로 예측됩니다. 정책 우선순위는 현재 진행 중인 오피오이드 위기를 반영하며, 2025년에는 주 오피오이드 대응 프로그램에 16억 달러가 기록됩니다. 약물 보조 요법의 확대와 988 위기 관리 전화에 대한 자금 제공은 조기 발견 및 도입을 지원합니다. 매니지드 케어의 보급은 지속적인 단약에 보답하는 가치 기반 계약으로 의료 제공업체를 유도하고 데이터 주도의 결과 추적 및 사회적 지원 서비스의 도입을 시설에 촉구하고 있습니다.

2024년 외래 환자 서비스 시장 점유율은 37.12%였습니다(행동 재활). CMS는 2025년 이후 외래 행동 의료에 새로운 시설 전문 제공업체 유형을 지정하여 인가를 받은 카운슬러나 결혼 및 가족 치료사에 의한 직접 청구가 가능하게 됩니다. 이러한 변화는 클리닉의 재정적 지속가능성을 강화하고 충분한 서비스를 받지 못한 지역으로의 지리적 확산을 가속화합니다.

입원 센터는 주로 급성 위기 및 이중 진단의 복잡성을 관리하고 여전히 수익의 상당한 비율을 모으고 있습니다. 업데이트된 SAMHSA 위기 관리 지침은 988 콜센터, 이동 위기 관리 팀, 안정화 단위로 구성된 협력 시스템을 강조합니다. 주택 프로그램은 청소년의 결과와 비용 효과에 대한 감시의 눈이 엄격해지고 있으며, 사업자는 증거 기반 프로토콜을 표준화하고 일상적인 성능 대시 보드를 발표하도록 요구되고 있습니다.

지역 분석

2024년 행동 재활 시장 점유율은 종합적인 보험 적용과 성숙한 의료 제공업체 네트워크를 배경으로 북미가 42.15%로 선두를 차지했습니다. 패리티 규제의 이행과 2025년 988 크라이시스 라인에 대한 6억 200만 달러의 연방 정부의 자금 지원으로 서비스 액세스가 강화됩니다. 프라이빗 주식 펀드가 여러 주에 걸쳐 플랫폼을 인수하고, 전자 의료 기록을 표준화하며, 결과 보고서를 강화하기 위해 통합이 활발해지고 있습니다. 그러나 임상 직원의 노동 조합화가 진행되고 임금 비용이 상승하며 운영자는 원격 모니터링을 통한 효율화를 목표로 합니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 2025-2030년 CAGR 7.01%로 성장할 전망입니다. 일본, 중국, 인도에서는 정부의 캠페인에 의해 정신건강 상담이 비종교화되어 국민보험 제도에 보험 적용이 통합되고 있습니다. 학사 수준의 카운슬러를 인증하는 태스크 시프팅 프로그램은 빠르게 능력을 확장하고 있습니다. 이 지역의 의료 기술 부문은 임상 의사 부족을 극복하고 농촌 지역에 행동 재활 서비스를 확대하기 위해 언어에 얽매이지 않는 채팅봇에 투자하고 있습니다.

유럽은 국민 모두 보험제도와 견고한 사회보호 메커니즘에 힘입어 2024년 27%의 매출을 유지했습니다. 영국과 독일 등의 국가에서는 디지털 세라퓰틱스 포뮬러가 도입되어 의사가 법정 자금으로 상환되는 앱 기반의 인지 행동 프로그램을 처방할 수 있게 되었습니다. 그러나 노동력의 인구동태는 퇴직이 다가오고 있음을 시사합니다. 현재 EU의 일부 국가는 정신과 의사의 자격을 갖춘 이민자에게 신속한 면허 취득의 길을 제공합니다.

중동 및 아프리카는 기초가 작은 반면, 정부가 국가 비전 계획에 정신 건강 목표를 통합하고 있기 때문에 일관된 성장을 경험하고 있습니다. 특히 걸프 협력 회의 회원국에서는 원격 의료 플랫폼이 임상의의 부족과 문화적 편견을 피하고 있습니다. 국제 NGO는 현지 부처와 제휴하여 지역에 뿌리를 둔 재활센터를 건설하고 동료 지원 근로자를 양성하고 있으며 증거 기반 개입에 대한 맹아적인 수요에 박차를 가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계 정신건강 질병 부담의 증대가 재활 서비스 수요 가속

- 행동적 케어의 보험 적용 평준화를 향한 정부의 정책 전환

- 텔레헬스 및 디지털 플랫폼의 급속한 보급이 액세스 확대

- 프라이빗 주식 및 전략적 투자를 통한 생산 능력 강화 및 표준화

- 1차 케어 경로에 대한 행동 의료의 통합이 도입 증가 초래

- 워크포스 이노베이션(피어 서포트, AI 트리어지)에 의한 서비스 효율화

- 시장 성장 억제요인

- 서비스 이용을 제한하는 뿌리 깊은 스티그마 및 문화적 장벽

- 면허가 있는 행동요법 전문가 부족이 확장성 제한

- 세분화된 진료 보상 모델이 의료 제공업체의 재무에 불확실성 초래

- 데이터 프라이버시 및 국경을 넘은 규제가 원격 재활의 확대 지연

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 행동 장애 유형별

- 불안 장애

- 기분 장애

- 물질 남용 장애

- 퍼스널리티 장애

- 주의 결함 장애

- 자폐증 스펙트럼

- 의료 환경별

- 외래 환자 프로그램

- 입원 프로그램

- 레지덴셜 프로그램

- 치료 방법별

- 상담

- 의약품

- 지원 서비스

- 기타 치료법

- 배송 방법별

- 대면식 시설 베이스

- 가상 및 원격 재활

- 하이브리드

- 연령층별

- 어린이 및 청소년(17세 이하)

- 성인(18-64세)

- 고령자(65세 이상)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Acadia Healthcare Co. Inc.

- Universal Health Services Inc.

- Magellan Health Inc.

- Springstone Inc.

- American Addiction Centers Holdings Inc.

- Aurora Behavioral Health System

- Behavioral Health Group LLC

- Haven Behavioral Healthcare Inc.

- Promises Behavioral Health

- Niznik Behavioral Health

- Teladoc Health Inc.

- Lyra Health Inc.

- Ginger

- Brightline Inc.

- Talkspace Inc.

- MindPath Health

- Cigna Behavioral Health

제7장 시장 기회 및 향후 전망

AJY 25.11.26The behavioral rehabilitation market size is valued at USD 584.3 billion in 2025 and is forecast to advance to USD 800.63 billion by 2030 at a CAGR of 6.51%.

Solid demand stems from rising mental-health prevalence, swift telehealth uptake, and policy moves that mandate parity between behavioral and medical benefits. Anxiety disorders retain the largest behavioral rehabilitation market share at 31% in 2024, reflecting heightened diagnosis and treatment-seeking behavior. Outpatient programs command 37% revenue owing to community-based models that trim costs and stigma. The virtual/tele-rehabilitation niche is expanding at 12.4% CAGR as permanent Medicare flexibilities open remote access. North America leads with 42% revenue, while Asia-Pacific posts the fastest 7% CAGR on the back of public-health campaigns and growing disposable incomes.

Global Behavioral Rehabilitation Market Trends and Insights

Escalating Global Mental-Health Disease Burden Accelerating Demand

The worldwide rise in mental-health disorders is stretching existing treatment capacity. One-third of the U.S. population lives in designated Mental Health Professional Shortage Areas, demonstrating the gap between service need and availability. Drug-overdose deaths exceeded 107,000 in 2021, and untreated behavioral conditions cost the U.S. economy USD 280 billion annually in lost productivity and medical expenses. These figures underscore the imperative for capacity expansion across all treatment modalities.

Government Policy Shifts Toward Coverage Parity

Final rules under the Mental Health Parity and Addiction Equity Act take effect on January 1, 2025, prohibiting health plans from applying stricter limits to behavioral health than to medical benefits. Plans must analyze network adequacy and utilization management, which is expected to widen coverage for millions of Americans. CMS's 2025 physician fee schedule also adds new codes for FDA-cleared digital therapeutics and safety-planning services, unlocking fresh reimbursement pathways for providers.

Persistent Stigma & Cultural Barriers Limiting Service Uptake

Only 58.5% of U.S. teenagers reported adequate emotional and social support in 2024, and 91% of Hispanic Americans with substance-use disorders did not receive needed treatment. Cultural norms, language gaps, and mistrust of formal systems hamper engagement even when services exist. Community-based outreach, bilingual workforce development, and culturally relevant peer-support models are essential to close this divide.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Telehealth & Digital Platforms

- Integration of Behavioral Health into Primary-Care Pathways

- Shortage of Licensed Behavioral-Health Professionals Restricting Scalability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Anxiety disorders contributed 31.12% to the behavioral rehabilitation market size in 2024, cementing their status as the dominant segment. Rising diagnosis rates and broader insurance coverage promote early intervention, while AI-based monitoring tools have lifted adherence by 45%. Digital therapeutics that deliver cognitive-behavioral content via mobile apps reinforce therapist-led protocols and extend reach beyond clinic walls. Immersive VR exposure therapy, for instance, helps recalibrate maladaptive fear responses and shortens course duration.

Substance-abuse disorders are projected to log a 7.81% CAGR between 2025 and 2030. Policy priority reflects the ongoing opioid crisis, with USD 1.6 billion earmarked for the State Opioid Response program in 2025. Medication-assisted treatment expansion and 988 crisis-line funding support earlier identification and referral. Managed-care penetration is steering providers toward value-based contracts that reward sustained abstinence, nudging facilities to adopt data-driven outcome tracking and wraparound social-support services.

Outpatient services accounted for 37.12% behavioral rehabilitation market share in 2024 as payers favor lower-intensity, community-anchored care. CMS has designated new facility-specialty provider types for outpatient behavioral health beginning 2025, enabling direct billing by licensed counselors and marriage-and-family therapists. These shifts bolster financial sustainability for clinics and accelerate geographic spread into underserved zones.

Inpatient centers still attract significant percentage of revenue, primarily managing acute crises and dual-diagnosis complexity. Updated SAMHSA crisis-care guidelines stress a coordinated system comprising 988 call centers, mobile crisis teams, and stabilization units. Residential programs face heightened scrutiny over youth outcomes and cost-effectiveness, prompting operators to standardize evidence-based protocols and publish routine performance dashboards.

The Behavioral Rehabilitation Market Report is Segmented by Type of Behavioral Disorder (Anxiety Disorder, and More), Healthcare Setting (Outpatient Programs, and More), Treatment Method (Counselling, and More), by Age Group (Adults, and More), Delivery Mode (In-Person Facility-Based, and More), Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America topped the behavioral rehabilitation market with a 42.15% share in 2024 on the strength of comprehensive insurance coverage and mature provider networks. Implementation of parity regulations and USD 602 million federal funding for the 988 crisis-line in 2025 reinforce service access. Consolidation is brisk as private equity funds buy multi-state platforms, standardize electronic medical records, and elevate outcome reporting. Rising unionization among clinical staff, however, is lifting wage costs and nudging operators toward tele-supervision efficiencies.

Asia-Pacific is the fastest-growing region, registering a 7.01% CAGR between 2025 and 2030. Government campaigns in Japan, China, and India are destigmatizing mental-health consultations and embedding coverage into national insurance schemes. Task-shifting programs that certify bachelor-level counselors are rapidly scaling capacity. The region's med-tech sector is investing in language-agnostic chatbots to surmount clinician shortages and extend behavioral rehab services into rural districts.

Europe maintained 27% revenue in 2024, supported by universal health coverage and robust social-protection mechanisms. Countries such as the United Kingdom and Germany have introduced digital-therapeutics formularies that allow physicians to prescribe app-based cognitive behavioral programs reimbursed under statutory funds. Workforce demographics, however, signal impending retirements; several EU nations now offer expedited licensure pathways for migrants with psychiatric credentials.

The Middle East & Africa, while smaller in base, is experiencing consistent growth as governments integrate mental-health targets into national vision plans. Telehealth platforms circumvent clinician scarcity and cultural stigma, particularly in Gulf Cooperation Council member states. International NGOs are partnering with local ministries to build community-based rehab centers and train peer support workers, fueling nascent demand for evidence-based interventions.

- Acadia Healthcare Co. Inc.

- Universal Health Services

- Magellan Health

- Springstone

- American Addiction Centers Holdings Inc.

- Aurora Behavioral Health System

- Behavioral Health Group LLC

- Haven Behavioral Healthcare

- Promises Behavioral Health

- Niznik Behavioral Health

- Teladoc Health

- Lyra Health

- Ginger

- Brightline Inc.

- Talkspace Inc.

- MindPath Health

- Cigna Behavioral Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Mental-Health Disease Burden Accelerating Demand for Rehabilitation Services

- 4.2.2 Government Policy Shifts Toward Coverage Parity for Behavioral Care

- 4.2.3 Rapid Adoption of Telehealth & Digital Platforms Expanding Access

- 4.2.4 Private-Equity & Strategic Investment Boosting Capacity & Standardization

- 4.2.5 Integration of Behavioral Health into Primary-Care Pathways Increasing Referrals

- 4.2.6 Workforce Innovation (Peer Support, AI Triage) Enhancing Service Efficiency

- 4.3 Market Restraints

- 4.3.1 Persistent Stigma & Cultural Barriers Limiting Service Uptake

- 4.3.2 Shortage of Licensed Behavioral-Health Professionals Restricting Scalability

- 4.3.3 Fragmented Reimbursement Models Creating Provider Financial Uncertainty

- 4.3.4 Data-Privacy & Cross-Border Regulation Slowing Tele-rehab Expansion

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type of Behavioral Disorder

- 5.1.1 Anxiety Disorder

- 5.1.2 Mood Disorder

- 5.1.3 Substance Abuse Disorder

- 5.1.4 Personality Disorder

- 5.1.5 Attention Deficit Disorder

- 5.1.6 Autism Spectrum Disorder

- 5.2 By Healthcare Setting

- 5.2.1 Outpatient Programs

- 5.2.2 Inpatient Programs

- 5.2.3 Residential Programs

- 5.3 By Treatment Method

- 5.3.1 Counselling

- 5.3.2 Medication

- 5.3.3 Support Services

- 5.3.4 Other Treatment Methods

- 5.4 By Delivery Mode

- 5.4.1 In-Person Facility-based

- 5.4.2 Virtual / Tele-rehabilitation

- 5.4.3 Hybrid

- 5.5 By Age Group

- 5.5.1 Children & Adolescents (<=17 yrs)

- 5.5.2 Adults (18-64 yrs)

- 5.5.3 Geriatric (>=65 yrs)

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Acadia Healthcare Co. Inc.

- 6.3.2 Universal Health Services Inc.

- 6.3.3 Magellan Health Inc.

- 6.3.4 Springstone Inc.

- 6.3.5 American Addiction Centers Holdings Inc.

- 6.3.6 Aurora Behavioral Health System

- 6.3.7 Behavioral Health Group LLC

- 6.3.8 Haven Behavioral Healthcare Inc.

- 6.3.9 Promises Behavioral Health

- 6.3.10 Niznik Behavioral Health

- 6.3.11 Teladoc Health Inc.

- 6.3.12 Lyra Health Inc.

- 6.3.13 Ginger

- 6.3.14 Brightline Inc.

- 6.3.15 Talkspace Inc.

- 6.3.16 MindPath Health

- 6.3.17 Cigna Behavioral Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment