|

시장보고서

상품코드

1910447

접이식 상자 포장 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Folding Carton Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

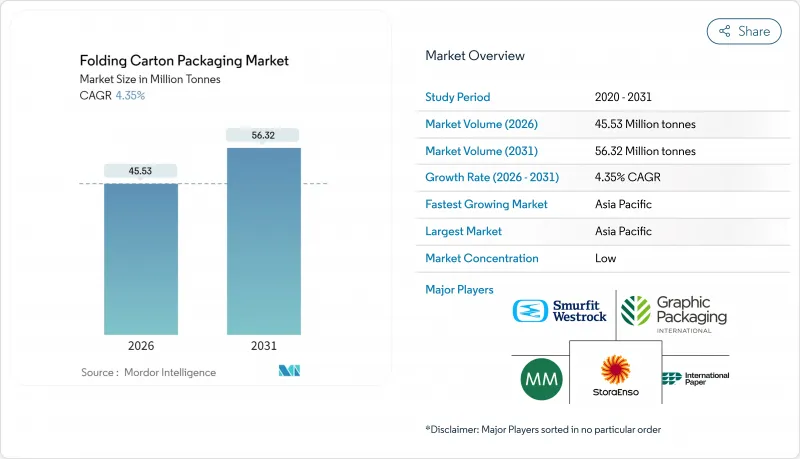

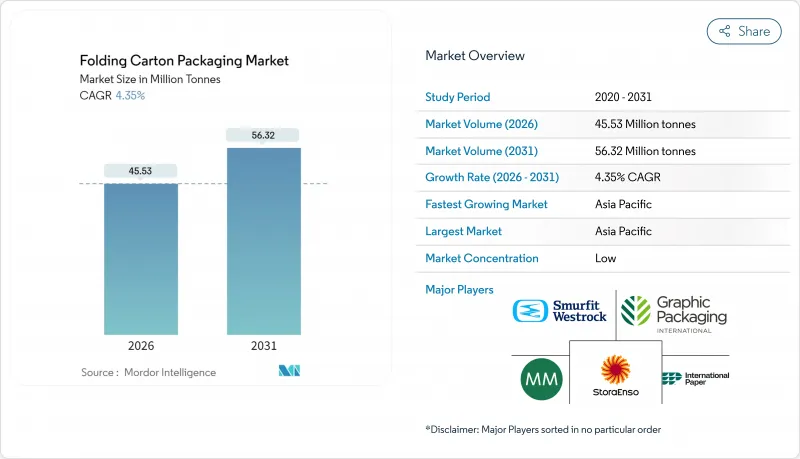

접이식 상자 포장 시장은 2025년 4,363만 톤으로 평가되었고, 2026년에는 4,553만 톤, 2031년까지 5,632만 톤에 이르고, 2026년부터 2031년에 걸쳐 CAGR 4.35%로 성장할 것으로 예측되고 있습니다.

지속적인 수요는 브랜드를 섬유계 대체품으로 이끄는 엄격한 법규제와 재활용의무도 충족시키는 보호포장 형태를 촉진하는 전자상거래의 확대로 인해 발생하고 있습니다. 특히 화장품과 영양보조식품에 있어서의 소비재의 고급화 가속은 접이식 상자 포장 시장에 있어서의 고그래픽·부가가치 디자인의 중요성을 한층 더 높이고 있습니다. 유럽연합(EU)과 중국의 재생소재 함유 규제는 저품질 생산자들에게 진입장벽을 높이고 있으며, 통합제지공장이 추적 가능성가 있는 판지급으로 점유율을 획득할 수 있게 하고 있습니다. 원재료 가격의 변동은 비통합 컨버터의 이익률을 압박하는 한편, 보다 예측 가능한 비용 구조를 제공하는 재생 섬유 스트림의 도입을 가속화하고 있습니다.

세계 접이식 상자 포장 시장 동향과 인사이트

지속가능성 주도에 의한 재생가능 포장으로의 전환

브랜드 소유자는 투자자의 요청과 소매점의 회수 규칙을 충족하기 위해 플라스틱에서 재생 가능한 판지로 전환하고 있습니다. 스토라엔소사가 2030년까지 100% 재생 가능한 라인을 실현한다고 표명한 것으로, 접이식 상자 포장 시장의 여러 해에 걸친 수요 전망이 확고한 것이 되었습니다. EU의 확대 생산자 책임 제도(EPR) 비용은 복합 소재 패키지의 폐기 비용을 밀어 올리고 비용 편익의 균형을 카톤에 유리하게 기울이고 있습니다. 접객 산업 및 산업 분야에서도 플라스틱 인서트를 성형 섬유 칸막이판으로 대체하여 유사한 전환이 진행되고 있습니다. 주요 소매업체는 패키지에 재활용 함량을 표시하는 섬유 기반 형식을 선호함으로써 이러한 목표를 충족합니다. 이러한 움직임이 결합되어 순환성은 마케팅 옵션이 아니라 조달의 전제조건으로 정착되고 있습니다.

전자상거래 포장 수요 급증

멀티 채널 선도는 파손률과 운송 비용 절감을 위해 소포 워크플로우를 재설계하고 있으며, 접이식 카톤은 용적 효율이 뛰어나 전면 그래픽 인쇄에도 대응합니다. 아마존의 2024년 10-K 보고서는 포장 최적화가 완성의 핵심 기둥으로 자리매김하고 있으며, 설계 개선이 네트워크 전체의 비용 절감으로 이어지는 실태를 반영합니다. 아시아태평양에서는 온라인 식품 및 화장품 부문의 급성장에 따라 장거리 수송을 견디는 변조 방지 기능이 있는 경질 포장에 대한 수요가 높아지고 있습니다. 역 물류에서도 카톤은 무결성을 유지하여 반품률을 줄이기 때문에 유리합니다. 도시 지역에서 마이크로 완성 거점이 증가함에 따라 온 디맨드 피킹 사이클에 해당하는 소형 접이식 판지가 가정 용품 분야에서 점유율을 확대하고 있습니다.

버진 펄프 가격 및 공급 변동성

펄프의 스팟 가격은 2024년 5월 생산자 물가 지수 219.835를 기록하여 단기 계약에 의존하는 가공업자에게 타격을 주었습니다. 유지 보수 사이클 동안 공장 정지는 공급을 더욱 박탈시키고, 가공업자는 가격 급등을 흡수하거나 비용을 다운스트림으로 전가할지 여부를 선택해야 합니다. 통합형 대기업은 골판지 원지와 판지기계간에 섬유를 나눔으로써 변동을 상쇄합니다만, 스팟 임베디드을 실시하는 독립계 기업은 운전자금의 고갈에 직면합니다. 그 결과 발생한 비용 구조의 격차가 M&A를 가속시켜 소규모 사업자는 밸런스 시트의 개선을 도모합니다. 위험 회피 수단의 채택은 증가하지만 소매업의 재고 감소와 관련된 수요의 불확실성으로 인해 그 효과가 감소합니다.

부문 분석

의료 및 의약품 분야는 2025년에 접이식 상자 포장 시장의 17.34%를 차지했고, 고령화와 생물학적 제제의 발매를 배경으로, 2031년까지 연평균 복합 성장률(CAGR)6.71%로 확대가 전망됩니다. 21 CFR Part 211을 준수하기 위해서는 변조 방지 스트라이프 라인과 직렬화 윈도우가 필수적이지만, 이러한 기능은 다층 구조의 복잡성을 추가하지 않고 접이식 판지에 쉽게 통합 할 수 있습니다. 식품 및 음료 카테고리는 접이식 상자 포장 시장의 33.18%를 차지하고, 냉장 대응 코팅 판지의 장점을 살린 레디밀 채택이나 음료 멀티팩에 의해 수요를 유지하고 있습니다. 한편, 퍼스널케어 분야에서는 고급 광택니스를 활용해, 경쟁이 심한 전문점에서의 선반상에서의 차별화를 도모하고 있습니다.

임상시험 활동이 증가함에 따라 처방전 변경시 진부화를 억제하는 디지털 인쇄에 적합한 소량 포장이 수요를 유발하고 있습니다. 클래스 A 클린 룸 시설을 가지는 카톤 가공업자는 오염 관리와 감사 대응 능력에 있어서 범용품 제조업체를 능가해, 원재료비 상승시에도 가격 프리미엄의 유지를 가능하게 하고 있습니다. 대중용 식품 분야에서는 경량 칩 보드를 이용한 분량 관리형 시리얼 스낵 트레이가 기반 수요를 지지해 경기 순환에 기인하는 수요 변동을 완화하고 있습니다.

접이식 상자 포장 시장 보고서는 최종 사용자 산업(식품 및 음료, 가정용품, 퍼스널케어 및 화장품, 의료 및 의약품, 담배, 전기 및 하드웨어), 소재 유형(무표백 판지 등), 인쇄 기술(오프셋 인쇄, 디지털 인쇄 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년에 접이식 상자 포장 시장 점유율의 38.42%를 차지했고, 명확한 주도적 지위를 유지하고 있습니다. 중국, 인도, 인도네시아에서 옴니채널 소매가 심화됨에 따라 6.82%의 연평균 복합 성장률(CAGR)로 계속 성장하고 있습니다. 중국의 가공업자는 국내 전자기기 수출업체가 요구하는 엄격한 파열강도 목표를 충족시키기 위해 기계설비의 고도화를 진행하고 있습니다. 또한 정부의 생분해성 규제가 PFAS 프리 코팅의 채택을 가속화하고 있습니다. 일본에서는 편의점의 밀 키트 보급에 따라 냉동고 대응 보드 수요가 증가하고, 고급 골판지 수요가 높아지고 있습니다. 한편 한국에서는 재활용성 등급제도에 따라 섬유포장자재의 표준화가 진행되어 고수율 탈묵라인의 도입이 촉진되고 있습니다.

북미에서는 생생한 그래픽을 갖춘 작은 로트 카톤이 필요한 D2C 구독 브랜드가 성장을 지원합니다. 인터내셔널 페이퍼에 의한 DS 스미스사 99억 달러 인수는 동서에 퍼지는 가공 거점을 확립해, 수송 거리를 단축하는 것과 동시에, 지역별 CPG 수요 급증에의 대응력을 강화합니다. 캐나다에서 재활용하기 어려운 플라스틱의 금지로 인해 냉동 식품과 유제품이 다시 카톤 보드 슬리브로 돌아갑니다. 멕시코의 전자 장비 조립의 니어 쇼어링은 ESD 대책 판지 인서트 수요를 급증시키고 미국 제지 공장에서 버진 크래프트 라이너의 수입을 견인하고 있습니다.

유럽은 혁신 중심의 자세를 유지하고, 포장 및 포장 폐기물 규제에 의해 2028년까지 완전 리사이클화를 의무화하고, 2026년 8월까지 불소계 배리어재를 배제합니다. 독일, 프랑스, 영국에서는 금속 효과와 수성 잉크를 융합시킨 디지털 장식 라인이 선구적으로 도입되어 고급스러운 시각적 목표와 환경 규제가 양립되고 있습니다. 동유럽의 가공업자는 골판지 제조기의 갱신을 위한 EU 자금을 확보하고 있습니다만, 과자류의 수출에는 여전히 카톤보드가 선택되고 있습니다. 그 이유는 높은 매장 임팩트에 있습니다. 새로운 규제의 확실성으로 차세대 코팅 설비에 대한 설비 투자가 활발해지고, 유연한 필름 사용자도 장기 보존 SKU를 위한 섬유 대체재를 재검토하는 움직임이 나오고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 지속가능성을 중시한 재활용 가능 포장으로의 전환

- 전자상거래 포장 수요의 급증

- 프리미엄화와 추세 및 진열 효과를 고려한 고급 인쇄 수요 증가

- 세계의 플라스틱 삭감 규제

- 디지털 인쇄 기술에 의해 소량 생산 및 마이크로 타겟팅 가능

- 밀키트 및 레디밀 정기 구독 서비스 확산

- 시장 성장 억제요인

- 버진 펄프의 가격과 공급 변동성

- 연성 파우치로의 대체 현상

- 배리어 카톤의 제한적인 재활용성

- PFAS 프리 코팅의 컴플라이언스 비용

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 지정학적 영향 분석

제5장 시장 규모와 성장 예측

- 최종 사용자 업계별

- 식음료

- 가정용

- 퍼스널케어 및 화장품

- 의료 및 의약품

- 담배

- 전기 및 하드웨어

- 소재 유형별

- 고형 표백 판지(SBB)

- 코트 무표백 크래프트 보드(CUK)

- 화이트 라인 칩 보드

- 접이식 상자 판지

- 인쇄 기술별

- 오프셋 인쇄

- 디지털(잉크젯/일렉트로 포토그래피)

- 플렉소 인쇄

- 그라비아 인쇄

- 기타 인쇄 기술

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Smurfit Westrock plc

- Graphic Packaging International LLC

- Mayr-Melnhof Karton AG

- DS Smith plc

- International Paper Company

- Stora Enso Oyj

- Georgia-Pacific LLC

- Mondi plc

- Huhtamaki Oyj

- Seaboard Folding Box Co. Inc.(Vidya Brands)

- American Carton Company

- All Packaging Company

- Edelmann GmbH

- CCL Healthcare(CCL Industries Inc.)

- Rengo Co., Ltd.

- Sonoco Products Company

- Autajon Group

- Southern Champion Tray

제7장 시장 기회와 장래의 전망

SHW 26.01.26The folding carton packaging market is expected to grow from 43.63 million tonnes in 2025 to 45.53 million tonnes in 2026 and is forecast to reach 56.32 million tonnes by 2031 at 4.35% CAGR over 2026-2031.

Sustained demand emerges from stricter legislation that steers brands toward fiber-based substitutes and from e-commerce expansion, which rewards protective formats that also meet recycling mandates. Accelerating premiumization in consumer goods, especially cosmetics and nutraceuticals, magnifies the folding carton packaging market's focus on high-graphic, value-added designs. Recycled-content regulations in the European Union and China raise barriers for low-quality producers, enabling integrated mills to capture share with traceable paperboard grades. Raw-material price volatility narrows margins for non-integrated converters, yet it simultaneously accelerates adoption of recycled fiber streams that deliver more predictable cost structures.

Global Folding Carton Packaging Market Trends and Insights

Sustainability-led Shift to Recyclable Packaging

Brand owners are migrating from plastic toward recyclable board to satisfy investor directives and retail take-back rules. Stora Enso's pledge for 100% recyclable lines by 2030 anchors multi-year volume visibility for the folding carton packaging market. Extended Producer Responsibility fees in the EU raise disposal costs on mixed-material packs, tilting the cost-benefit equation in favor of cartons. The hospitality and industrial sectors echo the shift by swapping plastic inserts for molded fiber partitions. Large retailers align with these targets by preferring fiber-based formats that declare recycled-content percentages on-pack. Together, the moves embed circularity as a procurement prerequisite rather than a marketing option.

E-commerce Packaging Demand Boom

Multichannel giants are redesigning parcel workflows to cut damage rates and freight costs, and folding cartons excel at cube efficiency while supporting full-surface graphics. Amazon's 2024 10-K cites packaging optimization as a core fulfillment pillar, reflecting how design tweaks cascade into network savings. Asia Pacific's surging online grocery and beauty segments amplify demand for tamper-evident, rigid solutions that survive long "first-mile-to-last-mile" journeys. Reverse logistics also favors cartons because integrity retention lowers the percentage of unsaleable returns. As micro-fulfillment hubs proliferate in urban centers, small-format folding cartons that accommodate on-demand picking cycles gain share across household staples.

Virgin Pulp Price and Supply Volatility

Pulp spot prices touched a Producer Price Index level of 219.835 in May 2024, exposing converters that rely on short-term contracts. Mill shutdowns during maintenance cycles tighten supply further, forcing converters to either absorb spikes or pass costs downstream. Integrated majors offset swings by diverting fiber between containerboard and cartonboard machines, yet spot-buying independents face working-capital drains. The resulting spread in cost structures accelerates M&A as sub-scale players seek balance-sheet relief. Hedge-instrument adoption rises, but the effectiveness is diluted by demand unpredictability linked to retail destocking.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization and Shelf-Impact Printing Needs

- Global Plastic-Reduction Regulations

- Substitution by Flexible Pouches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Healthcare and Pharmaceuticals claimed 17.34% of the folding carton packaging market in 2025 and are poised to climb at a 6.71% CAGR to 2031 on the back of aging demographics and biologic drug launches. Compliance with 21 CFR Part 211 demands tamper-evidence striplines and serialization windows, features readily integrated into folding cartons without adding multilayer complexity. The Food and Beverages category, holding 33.18% of the folding carton packaging market share, sustains volumes through ready-meal adoption and beverage multipacks that benefit from refrigerator-grade coated boards. Meanwhile, Personal Care leans on premium gloss varnishes to anchor shelf differentiation in crowded specialty stores.

Growing clinical trial activity triggers short-run packs that suit digital printing, cutting obsolescence when formulations shift. Carton converters with Class A cleanroom sites out-compete commodity players on contamination control and audit readiness, enabling price premiums even as input costs rise. For mass-market foods, portion-controlled cereal and snack trays rely on lightweight chipboard, underpinning baseline volume and cushioning overall demand swings driven by economic cycles.

The Folding Carton Packaging Market Report is Segmented by End-User Industry (Food and Beverages, Household, Personal Care and Cosmetics, Healthcare and Pharmaceuticals, Tobacco, and Electrical and Hardware), Material Type (Solid Bleached Board, and More), Printing Technology (Offset Lithography, Digital, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tonnes).

Geography Analysis

Asia Pacific maintains clear leadership with 38.42% of the folding carton packaging market share in 2025 and is advancing at a 6.82% CAGR as omni-channel retail deepens in China, India, and Indonesia. Chinese converters upscale machinery to meet domestic electronics exporters' stringent burst-strength targets, and government mandates on biodegradability accelerate the adoption of PFAS-free coatings. Japanese premium carton demand rises as convenience-store meal kits proliferate and require freezer-grade board. Meanwhile, South Korea's recyclability grading scheme further standardizes fiber packaging inputs and incentivizes high-yield deinking lines.

North America sustains growth through direct-to-consumer subscription brands that need small-batch cartons with vibrant graphics. International Paper's USD 9.9 billion DS Smith acquisition provides coast-to-coast converting nodes, trimming freight miles, and enhancing responsiveness to regional CPG demand surges. Canadian bans on difficult-to-recycle plastics redirect frozen entrees and dairy products back into cartonboard sleeves. Mexico's near-shoring of electronics assembly escalates demand for ESD-safe carton inserts, pulling imports of virgin Kraft liner from United States mills.

Europe remains innovation-centric, with the Packaging and Packaging Waste Regulation forcing full recyclability by 2028 and eliminating fluorinated barriers by August 2026. Germany, France, and the United Kingdom pioneer digital embellishment lines that marry metallic effects with water-based inks, aligning luxury visual targets with environmental mandates. Eastern European converters secure EU funding to update corrugators, yet cartonboard remains the format of choice for confectionery exports due to its higher shelf impact. The new regulatory certainty galvanizes CapEx in next-generation coating kitchens, nudging flexible-film users to reconsider fiber alternatives for long-shelf-life SKUs.

- Smurfit Westrock plc

- Graphic Packaging International LLC

- Mayr-Melnhof Karton AG

- DS Smith plc

- International Paper Company

- Stora Enso Oyj

- Georgia-Pacific LLC

- Mondi plc

- Huhtamaki Oyj

- Seaboard Folding Box Co. Inc. (Vidya Brands)

- American Carton Company

- All Packaging Company

- Edelmann GmbH

- CCL Healthcare (CCL Industries Inc.)

- Rengo Co., Ltd.

- Sonoco Products Company

- Autajon Group

- Southern Champion Tray

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainability-led shift to recyclable packaging

- 4.2.2 E-commerce packaging demand boom

- 4.2.3 Premiumization and shelf-impact printing needs

- 4.2.4 Global plastic-reduction regulations

- 4.2.5 Digital printing enables short-run micro-targeting

- 4.2.6 Meal-kit and ready-meal subscriptions surge

- 4.3 Market Restraints

- 4.3.1 Virgin pulp price and supply volatility

- 4.3.2 Substitution by flexible pouches

- 4.3.3 Limited recycling for barrier cartons

- 4.3.4 PFAS-free coating compliance costs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Geopolitical Impact Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By End-user Industry

- 5.1.1 Food and Beverages

- 5.1.2 Household

- 5.1.3 Personal Care and Cosmetics

- 5.1.4 Healthcare and Pharmaceuticals

- 5.1.5 Tobacco

- 5.1.6 Electrical and Hardware

- 5.2 By Material Type

- 5.2.1 Solid Bleached Board (SBB)

- 5.2.2 Coated Unbleached Kraftboard (CUK)

- 5.2.3 White-lined Chipboard

- 5.2.4 Folding Boxboard

- 5.3 By Printing Technology

- 5.3.1 Offset Lithography

- 5.3.2 Digital (Inkjet / Electrophotography)

- 5.3.3 Flexography

- 5.3.4 Gravure

- 5.3.5 Other Printing Technology

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Graphic Packaging International LLC

- 6.4.3 Mayr-Melnhof Karton AG

- 6.4.4 DS Smith plc

- 6.4.5 International Paper Company

- 6.4.6 Stora Enso Oyj

- 6.4.7 Georgia-Pacific LLC

- 6.4.8 Mondi plc

- 6.4.9 Huhtamaki Oyj

- 6.4.10 Seaboard Folding Box Co. Inc. (Vidya Brands)

- 6.4.11 American Carton Company

- 6.4.12 All Packaging Company

- 6.4.13 Edelmann GmbH

- 6.4.14 CCL Healthcare (CCL Industries Inc.)

- 6.4.15 Rengo Co., Ltd.

- 6.4.16 Sonoco Products Company

- 6.4.17 Autajon Group

- 6.4.18 Southern Champion Tray

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment