|

시장보고서

상품코드

1852051

신경 내시경 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Neuroendoscopy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

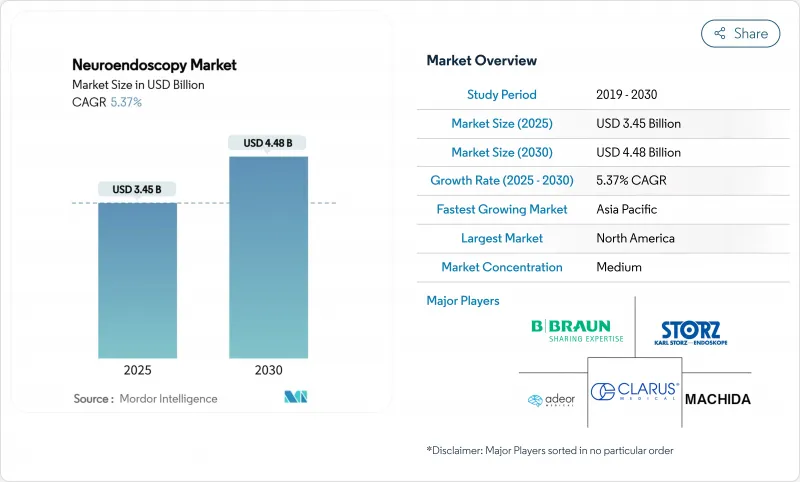

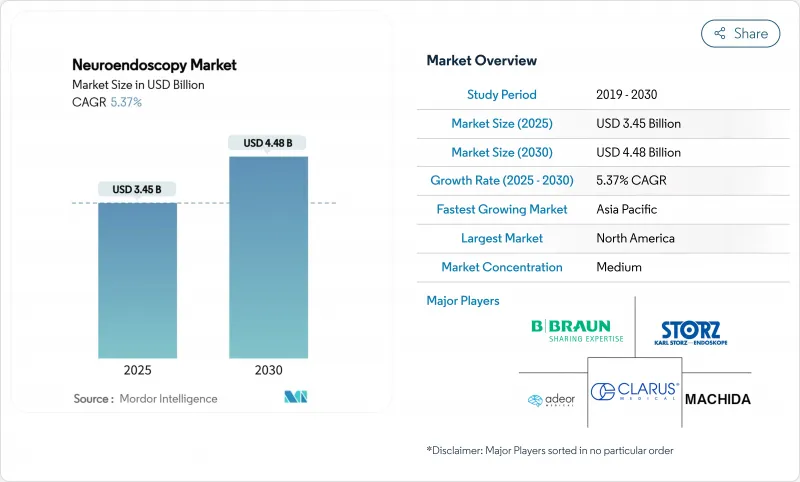

신경 내시경 시장 규모는 2025년에 34억 5,000만 달러로 추정되고, 2030년에는 44억 8,000만 달러에 이를 전망이며, CAGR 5.37%로 성장할 것으로 예측됩니다.

이 확장은 신경 기능을 유지하면서 회복을 단축하는 저침습 수술에 대한 선호도 증가를 반영합니다. 이 기세는 고화질 광학계, 네비게이션 소프트웨어, 로봇 공학, 인공지능을 구사한 화상 해석의 상호 비옥화에 의해 지원되고 있으며, 이들에 의해 내시경 뇌외과 수술의 용도 범위가 넓어져, 수술의 정밀도가 향상하고 있습니다. 일회용 기구는 아직 소수파이지만, 감염 제어의 우선순위가 높아짐에 따라 점유율을 획득하고 있으며, 내비게이션 일체형 타워의 설치 베이스가 확대됨에 따라 임상 도입에 대한 장벽이 낮아지고 있습니다. 대기업 다국적 기업이 세계 판매망과 연구개발 규모를 활용하는 한편, 일회용 기기나 소아 전용 플랫폼에서는 전문적인 진출 기업이 약진하고 있습니다. 병원이 설비 투자 자금을 비축하는 데 어려움을 겪고 있거나 학습 곡선이 어려워 외과 의사의 도입이 늦어지는 것(특히 Tier 1 센터 이외) 등의 역풍이 계속되고 있습니다.

세계의 신경 내시경 시장 동향 및 인사이트

세계적인 뇌종양 및 두개저종양 증가에 따른 저침습 신경 내시경 수요 증가

신경계 질환의 세계적인 유병률은 38억 명에 달하며 중추신경계 종양의 이환율은 증가하고 있습니다. 다형 교모세포종의 관리는 여전히 어렵고, 외과의사는 최대한의 안전한 절제를 달성하면서 피질 파괴를 줄이는 접근법의 채택에 박차를 가하고 있습니다. 2024년에 발표된 임상연구에 따르면 신경내시경에 의한 절제는 기존의 마이크로서저리보다 개두면적이 최대 70% 작고, 절제율도 동등하게 높으며, 합병증의 발생률도 낮다고 합니다. 이러한 결과는 사례 수가 증가함에 따라 저침습 기술로의 전환을 강화합니다.

광학, 시각화, 내비게이션의 기술적 진보가 임상 성과 향상

신경 내시경과 결합한 실시간 3D 재구성은 수두증에 대한 션트 설치의 정확성을 향상시켰고, 최근의 다시설 임상시험에서는 위치불량 합병증을 감소시켰습니다. 전용 로봇 암은 좁은 복도에서도 기구를 안정시키고 서브밀리메트릭의 진동 여과를 제공함으로써 이전에는 접근할 수 없었던 병변에도 도달할 수 있게 되었습니다. 이러한 진보는 외과 의사의 신뢰성을 높이고 조기 도입 시설에서 수술 시간을 단축하고 있습니다.

고급 시스템의 높은 자본 비용 및 유지 보수 비용이 보급 저해

뉴로네비게이션 대응 타워, 고해상도 카메라, 고강성 스코프의 조달은 저소득자 층에서는 진료과의 연간 설비 예산을 넘는 경우가 많습니다. 지속적인 교정 및 서비스 계약은 또한 재정을 압박하고 뇌신경 수술의 요구가 급증하는 고소득층 및 중소득층 시설 간의 격차를 넓혀가고 있습니다.

부문 분석

경성 스코프는 2024년 매출의 68%를 차지했으며, 뇌실내 및 두개저 통로에 적합한 선명한 광학 시스템을 제공하는 시스템의 신경 내시경 시장 점유율의 이점을 지원합니다. 플렉서블 스코프는 2025-2030년 연평균 복합 성장률(CAGR) 8.3%로 가속화될 전망입니다. 제조업체 각사는 선단부의 직경을 4mm 이하로 축소해, 재사용 가능한 카메라에 필적하는 해상도를 가지는 칩 온 더 칩 카메라를 탑재하고 있습니다. 증강현실 오버레이는 현재 외과 의사의 디스플레이에 해부학 랜드마크를 직접 투영하고 있으며, 이 기능은 다기관 공동 시험에서 평가 중입니다.

고분자 광학계 및 재활용 가능한 패키징의 진보는 병원의 지속가능성 위원회가 지적한 환경문제를 완화하기 위한 것입니다. 초기 라이프사이클 평가는 신재생 에너지의 투입이 전체 제조 소비량의 60%를 초과하면 선택된 단일 사용 모델의 탄소 중립 제조를 달성할 수 있음을 시사합니다. 프리미엄 재사용 키트와 턴키 일회용 세트의 가격 차이가 줄어들면서 병원은 범위 손상과 오염 제거 지연으로 인한 다운타임을 고려한 가치 분석을 검토하고 있습니다.

재사용 가능한 유닛은 수백 번의 처치로 상각되기 때문에 2024년 신경 내시경 시장 규모의 67%를 차지했습니다. 그러나, 오염제거 프로토콜은 다단계 워크플로우를 필요로 하기 때문에 인건비와 화학약품 비용이 상승하여 시설이 컴플라이언스 위반에 노출됩니다. NICE는 높은 처리량의 재처리 인프라가 존재하는 경우, 단일 사용 범위는 비용 효율성이 떨어질 수 있다고 경고하지만, 재처리 실패가 소송의 화종이 될 수 있음을 인정합니다.

이동식 라이트 케이블, 긁힘이 적은 사파이어 창, 강화된 각도 조절 메커니즘 등 산업 디자인의 변화로 인해 재사용 가능한 범위의 수명이 2,000 사이클 이상으로 연장되고 비용 곡선이 유지에 유리하게 구부러집니다. 단일 사용 채널에 대한 생분해성 폴리머에 대한 병행 연구는 임상적, 경제적, 환경적 지표를 동시에 충족시킬 수 있는 최종 수렴을 시사합니다.

지역 분석

북미는 2024년 매출에서 38%를 차지했으며, 첨단 병원 네트워크, 신속한 FDA 인증 패스웨이, 높은 신경외과 훈련 밀도에 의해 지원되고 있습니다. AI를 활용한 플래닝 플랫폼은 네비게이션 시스템과의 통합이 진행되고 있어 절제 마진을 샤프하게 해, 퍼스트 패스의 성공률을 높이고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 9.1%로 가장 급성장하고 있는 지역입니다. 일본에서는 고령화가 진행되고, 국민 모두 보험 제도가 도입되고 있기 때문에 기기의 갱신 사이클이 견조합니다. 중국에서는 Scivita Medical Technology와 같은 국내 제조업체가 외국계 기존 제조업체에 도전하고 있으며 공급업체 믹스의 변화를 보여줍니다. 인도에서는 관민 병원이 확대되어 내시경실에 대한 액세스가 확산되고 있습니다.

유럽은 각국의 의료제도가 저침습 전략을 장려하고 재원일수를 단축하고 있기 때문에 중요한 점유율을 유지하고 있습니다. 중동 및 아프리카에서는 걸프 협력 회의와 남아프리카의 3차 의료 센터에 대한 투자가 목표입니다. 라틴아메리카에서는 브라질과 아르헨티나가 학술적 파트너십과 자선 아웃리치에 뒷받침된 채용을 선도하고 있습니다. 뇌신경 외과 아웃리치 재단은 저자원 환경 전반에 걸쳐 수행된 1,985건의 수술을 통해 확장 가능한 효과를 입증합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 뇌종양 및 두개저 종양의 세계 부담 증가에 의한 신경 내시경 저침습 수술 수요 증가

- 광학, 시각화, 내비게이션의 기술적 진보에 의한 임상 결과 향상

- 신흥 경제국에서의 의료 인프라 및 뇌신경외과 수술 능력 확대

- 신경 내시경 기기의 보급을 지지하는 유리한 규제 및 상환 정책

- 고령화 사회 신경 질환에 대한 감수성 시술 건수의 자극

- 시장 성장 억제요인

- 첨단 신경 내시경 시스템의 높은 자본 비용 및 유지 보수 비용이 자원에 제약이 있는 환경에서의 보급 제한

- 가파른 학습 곡선 및 한정된 외과의 훈련이 수술 도입률에 영향

- 의료기기의 재처리, 무균성, 관련 소송에 대한 우려

- 혁신 및 특허의 상황

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 경성 신경 내시경

- 비디오 스코프

- 파이버 스코프

- 연성 신경 내시경

- 경성 신경 내시경

- 사용성별

- 재사용 가능한 신경 내시경

- 일회용 및 단일 사용 신경 내시경

- 용도별(수술 유형)

- 경비신경 내시경

- 뇌실내 신경 내시경

- 경두개 신경 내시경

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 전문 클리닉

- 연구 및 학술기관

- 환자 속성별

- 성인

- 소아

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Adeor Medical AG

- B. Braun Melsungen AG

- KARL STORZ SE & Co. KG

- Medtronic plc

- Olympus Corporation

- Stryker Corporation

- FUJIFILM Holdings Corporation

- Carl Zeiss Meditec AG

- Pentax Medical(HOYA Corp.)

- Ackermann Instrumente GmbH

- Clarus Medical

- Machida Endoscope Co. Ltd

- Schindler Endoskopie Technologie GmbH

- Tonglu Wanhe Medical Instrument Co. Ltd

- Visionsense Corporation

- Locamed Ltd

- Richard Wolf GmbH

- XION Medical GmbH

- Rudolf Medical GmbH

제7장 시장 기회 및 향후 전망

AJY 25.11.26The neuroendoscopy market size stands at USD 3.45 billion in 2025 and is forecast to reach USD 4.48 billion by 2030, advancing at a 5.37% CAGR.

This expansion reflects rising preference for minimally invasive procedures that shorten recovery while preserving neurological function. Momentum is sustained by cross-fertilization between high-definition optics, navigation software, robotics and artificial-intelligence-driven image analysis, which together broaden the applications of endoscopic neurosurgery and elevate procedural accuracy. Disposable instruments-though still a minority-are capturing share as infection-control priorities intensify, and the growing installed base of navigation-integrated towers lowers barriers to clinical adoption. Competitive dynamics remain moderately concentrated: large multinationals leverage global distribution and R&D scale, yet specialized entrants are making headway in single-use devices and pediatric-specific platforms. Headwinds persist where hospitals struggle to fund capital equipment and where the steep learning curve slows surgeon uptake, especially outside tier-one centers.

Global Neuroendoscopy Market Trends and Insights

Rising Global Burden of Brain & Skull-Base Tumors Increasing Demand for Minimally Invasive Neuroendoscopy

The global prevalence of nervous-system disorders affects 3.8 billion people, and central-nervous-system tumors impose growing morbidity. Glioblastoma multiforme remains difficult to manage, spurring surgeons to adopt approaches that reduce cortical disruption while achieving maximal safe resection. Clinical studies published in 2024 show neuroendoscopic resections require craniotomy areas up to 70% smaller than conventional microsurgery, with comparably high extirpation rates and lower complication incidence. These outcomes reinforce the shift toward minimally invasive techniques as caseloads climb.

Technological Advancements in Optics, Visualization, and Navigation Enhancing Clinical Outcomes

Real-time 3D reconstruction paired with neuroendoscopy has improved shunt placement accuracy for hydrocephalus, cutting malposition complications in recent multicenter trials. Purpose-built robotic arms stabilize instrumentation in narrow corridors and provide sub-millimetric tremor filtration, extending reach to previously inaccessible lesions. Together, these advances lift surgeon confidence and are shortening operating times in early adopter sites.

High Capital & Maintenance Costs of Advanced Systems Restricting Uptake

Procurement of neuronavigation-ready towers, high-resolution cameras and rigid scopes often exceeds a department's annual equipment budget in low-income settings. Ongoing calibration and service contracts further strain finances, widening the gap between high-income and middle-income facilities where neurosurgical needs are surging.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Healthcare Infrastructure and Neurosurgery Capacity in Emerging Economies

- Favorable Regulatory and Reimbursement Policies Supporting Adoption of Neuroendoscopic Devices

- Steep Learning Curve and Limited Surgeon Training Affecting Adoption Rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rigid scopes captured 68% of 2024 revenue, underpinning the neuroendoscopy market share advantage of systems offering crystal-clear optics suited to intraventricular and skull-base corridors. Flexible scopes are accelerating at an 8.3% CAGR from 2025 to 2030. Manufacturers are shrinking distal tip diameters below 4 mm and integrating chip-on-the-tip cameras that rival reusable counterparts in resolution. Augmented-reality overlays now project anatomic landmarks directly onto surgeon displays, a capability under evaluation in multicenter trials.

Advances in polymer optics and recyclable packaging aim to mitigate environmental concerns cited by hospital sustainability boards. Early lifecycle assessments suggest carbon-neutral production of selected single-use models is achievable if renewable-energy inputs exceed 60% of total manufacturing consumption. As pricing narrows between premium reusable kits and turnkey disposable sets, hospitals are recalibrating value analyses that consider downtime due to scope damage or decontamination backlog.

Reusable units comprise 67% of the 2024 neuroendoscopy market size thanks to amortization over hundreds of procedures. Decontamination protocols, however, require multistep workflows that raise labor and chemical costs while exposing facilities to compliance lapses. NICE has cautioned that single-use scopes can be cost-ineffective when high-throughput reprocessing infrastructure exists, yet it also acknowledges reprocessing failures as a litigatory flashpoint.

Industrial design changes-detachable light cables, scratch-resistant sapphire windows and reinforced angulation mechanisms-are extending reusable scope lifespans beyond 2,000 cycles, bending cost curves in favor of retention. Parallel work on biodegradable polymers for single-use channels signals an eventual convergence where clinical, economic and environmental metrics can be met simultaneously.

The Neuroendoscopy Market Report is Segmented by Product Type (Rigid Neuroendoscopes and Flexible Neuroendoscopes), Usability (Reusable Neuroendoscopes and Single-Use Neuroendoscopes), Application (Transnasal Neuroendoscopy, and More), End User (Hospitals, and More), Patient Demographics (Adult and Pediatric) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 38% revenue in 2024, supported by advanced hospital networks, rapid FDA clearance pathways and high neurosurgical training density. AI-augmented planning platforms are increasingly integrated with navigation systems, sharpening resection margins and bolstering first-pass success rates.

Asia-Pacific is the fastest-growing region at 9.1% CAGR to 2030. Japan's aging population, coupled with universal coverage, drives robust equipment refresh cycles. China's domestic producers, such as Scivita Medical Technology, are challenging foreign incumbents, signaling a shift in vendor mix. India's public-private hospital expansion is widening access to endoscopic suites, while training exchanges with global centers raise procedural competency levels.

Europe maintains meaningful share as national health systems encourage minimally invasive strategies to trim lengths of stay. The Middle East and Africa are witnessing targeted investments in tertiary centers within the Gulf Cooperation Council and South Africa. In Latin America, Brazil and Argentina lead adoption, underpinned by academic partnerships and charitable outreach; the Neurosurgery Outreach Foundation has demonstrated scalable impact through 1,985 surgeries conducted across low-resource settings.

- Adeor Medical

- B. Braun

- Karl Storz

- Medtronic

- Olympus

- Stryker

- FUJIFILM

- Carl Zeiss

- Pentax Medical (HOYA Corp.)

- Ackermann Instrumente

- Clarus Medical

- Machida Endoscope

- Schindler Endoskopie Technologie

- Tonglu Wanhe Medical Instrument

- Visionsense

- Locamed

- Richard Wolf

- XION Medical GmbH

- Rudolf Medical GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Burden of Brain & Skull-Base Tumors Increasing Demand for Minimally Invasive Neuroendoscopy

- 4.2.2 Technological Advancements in Optics, Visualization, and Navigation Enhancing Clinical Outcomes

- 4.2.3 Expanding Healthcare Infrastructure and Neurosurgery Capacity in Emerging Economies

- 4.2.4 Favorable Regulatory and Reimbursement Policies Supporting Adoption of Neuroendoscopic Devices

- 4.2.5 Aging Population Susceptibility to Neurological Disorders Stimulating Procedure Volumes

- 4.3 Market Restraints

- 4.3.1 High Capital & Maintenance Costs of Advanced Neuroendoscopic Systems Restricting Uptake in Resource-Constrained Settings

- 4.3.2 Steep Learning Curve and Limited Surgeon Training Affecting Procedure Adoption Rates

- 4.3.3 Concerns Over Device Reprocessing, Sterility, and Associated Litigation

- 4.4 Innovation & Patent Landscape

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Rigid Neuroendoscopes

- 5.1.1.1 Videoscopes

- 5.1.1.2 Fiberscopes

- 5.1.2 Flexible Neuroendoscopes

- 5.1.1 Rigid Neuroendoscopes

- 5.2 By Usability

- 5.2.1 Reusable Neuroendoscopes

- 5.2.2 Disposable / Single-Use Neuroendoscopes

- 5.3 By Application (Surgery Type)

- 5.3.1 Transnasal Neuroendoscopy

- 5.3.2 Intraventricular Neuroendoscopy

- 5.3.3 Transcranial Neuroendoscopy

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Specialty Clinics

- 5.4.4 Research & Academic Institutes

- 5.5 By Patient Demographics

- 5.5.1 Adult

- 5.5.2 Pediatric

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Adeor Medical AG

- 6.3.2 B. Braun Melsungen AG

- 6.3.3 KARL STORZ SE & Co. KG

- 6.3.4 Medtronic plc

- 6.3.5 Olympus Corporation

- 6.3.6 Stryker Corporation

- 6.3.7 FUJIFILM Holdings Corporation

- 6.3.8 Carl Zeiss Meditec AG

- 6.3.9 Pentax Medical (HOYA Corp.)

- 6.3.10 Ackermann Instrumente GmbH

- 6.3.11 Clarus Medical

- 6.3.12 Machida Endoscope Co. Ltd

- 6.3.13 Schindler Endoskopie Technologie GmbH

- 6.3.14 Tonglu Wanhe Medical Instrument Co. Ltd

- 6.3.15 Visionsense Corporation

- 6.3.16 Locamed Ltd

- 6.3.17 Richard Wolf GmbH

- 6.3.18 XION Medical GmbH

- 6.3.19 Rudolf Medical GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment