|

시장보고서

상품코드

1852098

갑상선 기능 검사 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Thyroid Function Test - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

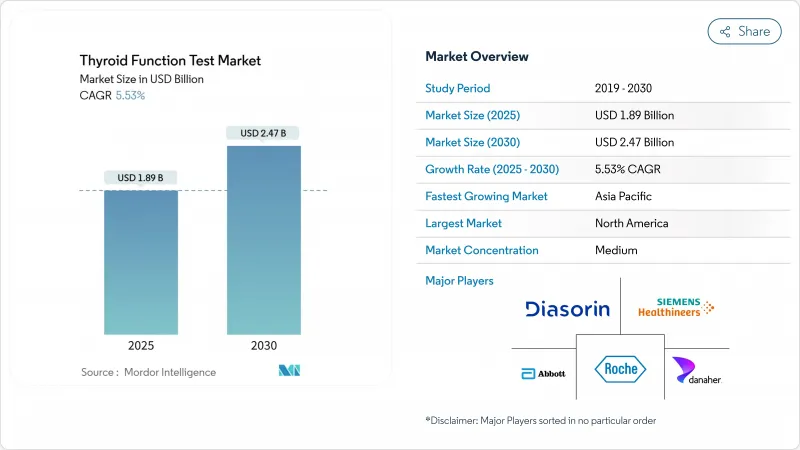

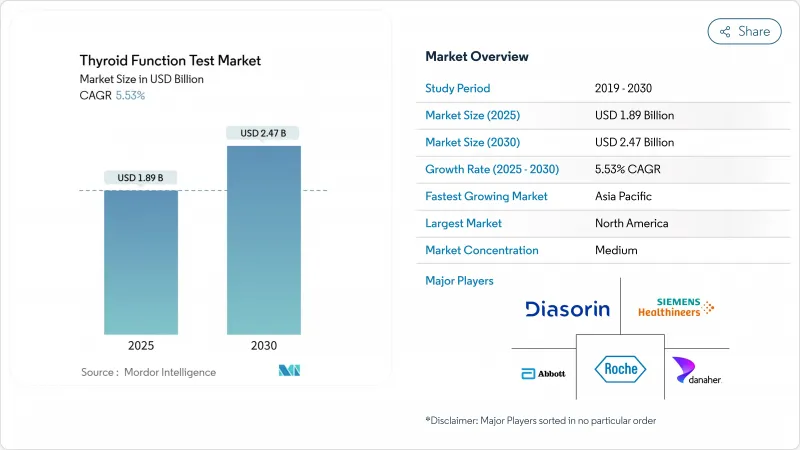

갑상선 기능 검사 시장 규모는 2025년에 18억 9,000만 달러, 예측 기간 동안 CAGR은 5.53%를 나타내고, 2030년에는 24억 7,000만 달러에 도달할 것으로 예측됩니다.

세계적인 갑상선 질환 유병률 증가, 노인 인구의 확대, 신생아 스크리닝 프로그램의 보급이 이러한 성장을 지원하고 있습니다. 기술 통합, 특히 고감도 3세대 면역 측정법, 새로운 질량 분석법, AI 유도 반사 검사 알고리즘은 진단 정확도를 높이는 동시에 미국의 70% 카운티에 영향을 미치는 내분비 전문의 부족으로 인한 작업 부담을 완화합니다. 미국 FDA의 2024년 임상 실험실 개발 검사 프레임워크와 같은 규제 변경은 더 높은 컴플라이언스 비용을 초래하지만 더 높은 표준화를 약속합니다. 가격 투명성에 관한 법률과 일괄 계약 협상은 보다 낮은 비용의 독립 검사 기관으로 검사량을 이동시키고 경쟁을 격화시키지만 환자 접근은 확대됩니다.

세계의 갑상선 기능 검사 시장 동향과 통찰

갑상선 질환 부담 증가

갑상선기능저하증의 유병률은 인도에서 11%에 달하는 반면, 구미 국가에서는 2-4.6%이며, 요오드충족율, 유전, 환경폭로의 지리적인 차이가 부각되고 있습니다. 잠재성 갑상선 기능 항진증은 미국 청소년의 4.4%를 앓고 있으며, 스크리닝 프로그램을 촉진하는 진단되지 않은 코호트를 돋보이게 합니다. 자가면역성 갑상선 질환에 대한 인식 증가는 기존의 호르몬 측정 외에도 항체 패널 수요를 확대하고 있습니다. 조기 발견은 하류 심혈관 질환과 인지 합병증을 줄이므로 지불자는 스크리닝 적용 범위를 넓히는 경제적 인센티브를 얻을 수 있습니다. 이러한 힘은 종합적으로 갑상선 기능 검사 시장의 꾸준한 확장을 지원합니다.

고령화로 정기검진량 증가

인구의 고령화, 특히 60세 이상의 여성의 노화는 갑상선기능저하증 및 갑상선기능항진증의 발생률 상승과 관련이 있습니다. 미국에서는 2036년까지 최대 8만 6,000명의 의사 부족이 예측되고 있으며, 내분비학은 가장 타격을 받는 전문 분야 중 하나이기 때문에 자동화 플랫폼과 1차 케어에 근거한 검사 경로의 채택이 가속화되고 있습니다. 보험사에 의한 예방검진의 환불에 의해 갑상선 패널이 정기검진에 통합되어, 검사 오더가 반응적인 것으로부터 적극적인 것에 변화하고 있습니다. 디지털화된 집단 건강 이니셔티브는 검사량을 더욱 확대하여 갑상선 기능 검사 시장의 장기 성장을 강화합니다.

복잡한 해석과 비오틴 간섭 문제

고용량의 비오틴 보충제는 검사 환자의 최대 10%에서 면역 측정 결과를 왜곡하고 검사 시설은 진단을 지연시키는 7일간의 검사 중지를 강요합니다. 간섭은 플랫폼에 따라 다르므로 병원 네트워크 간의 조화를 복잡하게 만듭니다. 게다가 임신 중이거나 심각한 질환에서 호르몬 결합 단백질의 이동은 미묘한 해석을 필요로 하기 때문에 1차 케어의 임상의 중에는 주문을 제한하는 사람도 있어 갑상선 기능 검사 시장의 눈앞의 이익을 억제하고 있습니다.

부문 분석

2024년 갑상선 기능 검사 시장에서 TSH 측정법은 42.86%의 슬라이스를 차지했고, 이는 민감한 고속선 스크리닝에 대한 가이드라인의 선호도를 반영하고 있습니다. 항-TPO 항체 측정법과 항-TG 항체 측정법은 절대량은 적지만, 자가면역성 갑상선염의 인지가 가속됨에 따라 CAGR 7.56%로 확대되고 있습니다. 터보 TSI 바이오 검정은 배달 시간을 며칠에서 몇 시간으로 단축하고 포인트 오브 케어 항체 키트는 10 분 이내에 실용적인 결과를 제공합니다. 새로운 질량 분석 패널은 복잡한 경우에 지지를 모으고, 높은 특이성과 낮은 간섭을 약속하며, 갑상선 기능 검사 시장을 확대합니다.

유리/총 T4 측정은 용량 점증과 감별 진단에 필수적인 것으로 변함이 없지만, 유리/총 T3 측정은 단발성 T3 중독증의 유병률이 낮기 때문에 틈새 역할을 담당하고 있습니다. 분화형 갑상선암의 후속을 위한 사이로글로불린과 수양암을 위한 칼시토닌이라는 특수한 마커는 증수를 가져오지만, 갑상선 기능 검사 시장 전체의 규모를 크게 변동시키는 것은 아닙니다. AI 기반 패턴 인식 도구는 현재 임상의가 여러 분석 프로파일을 해석하는 데 도움이 진단의 모호성을 줄이고 항체 패널의 보급을 촉구하고 있습니다.

Immuno Assay는 2024년 매출액의 60.23%를 차지했고, 시프트당 수천 검체를 처리하는 자동화학발광 및 ELISA 플랫폼을 활용하고 있습니다. 분산형 의료 모델에 의해 포인트 오브 케어 형식의 CAGR은 8.86%가 되어, 성장은 계속되지만 완만하게 됩니다. 금 나노 쉘을 사용한 래터럴 플로우 스트립은 TSH 검출 임계치를 0.16μIU/mL까지 낮추어 실험실 등급의 감도에 필적합니다. 디지털 면역 분석은 클라우드에 연결된 결과를 원격 모니터링에 제공하여 갑상선 기능 검사 시장을 확장합니다.

질량 분석기의 채택은 비교할 수 없는 특이성을 요구하는 레퍼런스 실험실에서 증가하고, 특히 단백질 결합이 면역 측정에 영향을 미치는 유리 호르몬의 측정에 적합합니다. 형광 편광법과 일렉트로케밀루미네센스는 여전히 조사에서 전문적인 도구입니다. COVID-19는 신속하고 최소한의 검사를 거치는 진단법에 대한 평가를 높이고 있으며, 이 행동 전환은 팬데믹 후 휴대용 기기의 보급을 지원하고 갑상선 기능 검사 업계 전체 투자의 우선순위를 재형성하고 있습니다.

지역 분석

북미는 2024년에 34.89%로 가장 규모가 큰 지역 점유율을 유지했으며, 광범위한 보험 적용, 높은 질병 인지도, 정교한 검사 인프라에 밀려났습니다. 그러나 미국에서는 70%의 카운티에 내분비 전문의가 부족해 AI 트리어지 툴이나 원격 내분비학 진찰의 보급을 촉진하고 있습니다. 가격 벤치마크 규제는 의료 시스템에 긴급성이 없는 패널을 독립 실험실로 돌려주도록 촉구하고 채널 믹스는 변화하지만 갑상선 기능 검사 시장 전체의 성장은 유지됩니다.

아시아태평양은 CAGR 6.89%에서 가장 빠르게 성장하는 지역입니다. 인도의 11% 갑상선 기능 저하증 유병률은 상당한 검진 기회를 시사합니다(ijmedicine.com). 중국의 갑상선암 이환율 상승과 대규모 인구 기반은 그 양에 박차를 가하는 한편, 일본의 급속한 고령화 사회는 일상적인 모니터링을 추진합니다. 태국 및 기타 국가의 정부 지원을 통한 신생아 스크리닝의 확대는 거의 보편적인 커버리지의 실현 가능성을 나타내고 예측 가능한 양을 끌어내고 지역의 갑상선 기능 검사 시장 규모를 증가시킵니다. 규제의 불균일성과 상환의 격차가 과제로 남아 있지만 디지털 의료에 대한 투자와 민간 실험실의 파트너십이 장벽을 상쇄합니다.

유럽은 국민 모두 보험제도와 엄격한 임상 가이드라인에 힘입어 꾸준하지만 완만한 확대를 보여주고 있습니다. 예산의 제약은 집중 조달과 일괄 계약을 촉진하고 비용 효율적인 공급업체를 선호합니다. 브렉시트 이후 규제 재조정은 복잡성을 증가시키고 있지만, 확립된 품질 기준이 임상의의 신뢰를 뒷받침합니다. 중동, 아프리카 및 남미는 건강 관리 인프라의 성숙과 함께 장기 성장 포켓으로 부상합니다. 이동식 검사 장비와 원격 의료 플랫폼은 지리적 장애를 극복하고 갑상선 기능 검사 시장의 미개척 지역으로의 확장을 뒷받침합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 갑상선 질환의 부담 증가

- 고령화에 의해 정기검진량이 증가

- 고감도 제3세대 면역 측정법이 임상적 유용성을 향상시킨다

- 정부 자금에 의한 신생아 스크리닝과 인구 스크리닝 프로그램

- 가정용 검사 키트와 원격 검사 서비스

- AI 기반 반사율 테스트 알고리즘으로 테스트 주문 증가

- 시장 성장 억제요인

- 복잡한 해석과 비오틴 간섭의 문제

- 내분비 전문의의 부족이 진단과 후속을 지연시킨다

- 번들 계약에 의한 실험실 검사 가격의 압축

- 과도한 선별 및 과잉 치료에 대한 가이드라인 반발

- 규제 상황

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력/소비자

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 시험별

- TSH 검사

- 유리 T4/총 T4 검사

- 유리 T3/총 T3 검사

- 항 TPO/항 TG 항체 검사

- 기타 시험

- 기술별

- 면역검정(CLIA, ELISA, RIA)

- 신속 포인트 오브 케어 검사

- 질량 분석

- 기타 기술

- 샘플 유형별

- 혈청/혈장

- 모세혈(관)혈액(지문 채혈)

- 건조 혈액 스폿

- 최종 사용자별

- 병원

- 진단 실험실

- 기타 최종 사용자

- 지리

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott

- Zhengzhou Autobio Co., Ltd.

- bioMrieux SA

- Danaher Corporation(Beckman Coulter)

- DiaSorin SpA

- F. Hoffmann-La Roche Ltd

- Qualigen, Inc.

- QuidelOrtho Corporation

- Siemens Healthineers

- Thermo Fisher Scientific Inc.

- Werfen

- Boditech Med Inc.

- Ortho Clinical Diagnostics

- Mindray Bio-Medical Electronics

- Randox Laboratories

- Tosoh Corporation

- Diazyme Laboratories

- Sysmex Corporation

- PerkinElmer Inc.

- IBL-America

- Sekisui Diagnostics

- Euroimmun AG

제7장 시장 기회와 장래의 전망

SHW 25.11.19The thyroid function testing market size is valued at USD 1.89 billion in 2025 and is projected to reach USD 2.47 billion by 2030, posting a CAGR of 5.53% during the forecast period.

Rising global thyroid disease prevalence, an expanding elderly population, and the spread of newborn screening programs anchor this growth. Technology integration-especially high-sensitivity third-generation immunoassays, emerging mass-spectrometry methods, and AI-guided reflex-testing algorithms-elevates diagnostic accuracy while easing the workload created by endocrinologist shortages that affect 70% of US counties. Regulatory changes such as the US FDA's 2024 framework for laboratory-developed tests introduce higher compliance costs yet promise greater standardization. Price transparency laws and bundled-contract negotiations are shifting volumes toward lower-cost independent laboratories, intensifying competition but expanding patient access.

Global Thyroid Function Test Market Trends and Insights

Rising Burden of Thyroid Disorders

Hypothyroidism prevalence reaches 11% in India versus 2-4.6% in Western nations, underscoring geographic differences in iodine sufficiency, genetics, and environmental exposures. Subclinical hyperthyroidism affects 4.4% of US adolescents, highlighting an undiagnosed cohort that fuels screening programs. Growing autoimmune thyroid disease awareness expands demand for antibody panels alongside traditional hormone measures. Earlier detection reduces downstream cardiovascular and cognitive complications, giving payers economic incentives to broaden screening coverage. Collectively these forces underpin steady expansion of the thyroid function testing market.

Aging Population Raises Routine Screening Volumes

Population aging, especially among women older than 60, correlates with higher hypo- and hyperthyroidism rates. A projected US physician shortfall of up to 86,000 by 2036, with endocrinology among the hardest-hit specialties, is accelerating adoption of automated platforms and primary-care-based testing pathways. Insurer reimbursement for preventive screening pushes thyroid panels into routine checkups, transforming test ordering from reactive to proactive. Digitally enabled population-health initiatives further scale testing volumes, reinforcing long-term growth in the thyroid function testing market.

Complex Interpretation & Biotin Interference Issues

High-dose biotin supplements distort immunoassay results in up to 10% of tested patients, forcing laboratories to impose 7-day cessation windows that delay diagnosis. Interference varies by platform, complicating harmonization across hospital networks. Additionally, hormone-binding protein shifts in pregnancy and critical illness demand nuanced interpretation, prompting some primary-care clinicians to limit ordering, which tempers near-term gains for the thyroid function testing market.

Other drivers and restraints analyzed in the detailed report include:

- High-Sensitivity 3rd-Gen Immunoassays Improve Clinical Utility

- Government-Funded Newborn & Population Screening Programs

- Shortage Of Endocrinologists Slows Diagnosis & Follow-Up

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The TSH assay held a 42.86% slice of the thyroid function testing market in 2024, reflecting guideline preference for a sensitive first-line screen. Anti-TPO and Anti-TG antibody assays, while smaller in absolute volume, are expanding at 7.56% CAGR as autoimmune thyroiditis recognition accelerates. Turbo TSI bioassays cut turnaround time from days to hours, and point-of-care antibody kits deliver actionable results inside 10 minutes. Emerging mass-spectrometry panels gain favor in complex cases, promising higher specificity and lower interference, thereby broadening the thyroid function testing market.

Free/total T4 assays remain indispensable for dose titration and differential diagnosis, whereas free/total T3 holds a niche role given low prevalence of isolated T3 toxicosis. Specialized markers-thyroglobulin for differentiated thyroid cancer follow-up and calcitonin for medullary carcinoma-provide incremental revenues but do not materially shift overall thyroid function testing market size. AI-based pattern-recognition tools now help clinicians interpret multi-analyte profiles, reducing diagnostic ambiguity and encouraging wider antibody-panel adoption.

Immunoassays controlled 60.23% of 2024 revenues, leveraging automated chemiluminescent and ELISA platforms that process thousands of samples per shift. Growth continues but moderates as decentralized care models fuel an 8.86% CAGR for point-of-care formats. Lateral-flow strips using gold nanoshells cut TSH detection thresholds to 0.16 µIU/mL, matching lab-grade sensitivity. Digital immunoassays provide cloud-connected results for remote monitoring, widening the thyroid function testing market.

Mass spectrometry adoption rises within reference labs seeking unparalleled specificity, especially for free hormones where protein binding skews immunoassays. Fluorescence polarization and electrochemiluminescence remain specialty tools in research. COVID-19 heightened appreciation for rapid, minimally attended diagnostics, a behavioral shift sustaining post-pandemic uptake of portable devices and reshaping investment priorities across the thyroid function testing industry.

The Thyroid Function Test Market Report is Segmented by Test (TSH Test, Free/Total T4 Test, Free/Total T3 Test, and More), Technique (Immunoassay, Rapid Point-Of-Care Tests, and More), Sample Type (Serum/Plasma, and More), End User (Hospital, Diagnostic Laboratory, Other End Users, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained the largest regional share at 34.89% in 2024, propelled by broad insurance coverage, high disease awareness, and sophisticated lab infrastructure. Endocrinologist shortages in 70% of US counties, however, risk pockets of under-service, prompting wider deployment of AI triage tools and tele-endocrinology consults. Price-benchmarking regulations spur health systems to reroute non-urgent panels to independent labs, altering channel mix but sustaining overall thyroid function testing market growth.

Asia-Pacific is the fastest-growing arena at 6.89% CAGR. India's 11% hypothyroidism prevalence signals a substantial screening opportunity [ijmedicine.com]. China's rising thyroid cancer incidence and large population base fuel volume, while Japan's rapidly aging society drives routine monitoring. Government-backed newborn screening expansions in Thailand and elsewhere demonstrate near-universal coverage feasibility, unlocking predictable volumes and elevating regional thyroid function testing market size. Regulatory heterogeneity and reimbursement gaps remain challenges, yet digital health investments and public-private lab partnerships offset barriers.

Europe shows steady but slower expansion, anchored by universal health systems and stringent clinical guidelines. Budget constraints encourage centralized procurement and bundled contracts, favoring cost-efficient suppliers. Regulatory realignment post-Brexit adds complexity, yet established quality standards sustain clinician confidence. Middle East & Africa and South America emerge as longer-term growth pockets as healthcare infrastructure matures. Mobile testing units and telehealth platforms help overcome geographic obstacles, extending reach of the thyroid function testing market into underserved locales.

- Abbott Laboratories

- Zhengzhou Autobio Co., Ltd.

- bioMerieux

- Danaher

- DiaSorin

- Roche

- Qualigen, Inc.

- QuidelOrtho

- Siemens Healthineers

- Thermo Fisher Scientific

- Werfen

- Boditech Med

- Ortho Clinical Diagnostics

- Mindray Bio-Medical Electronics

- Randox Laboratories

- Tosoh

- Diazyme Laboratories

- Sysmex

- PerkinElmer

- IBL-America

- Sekisui Diagnostics

- Euroimmun

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Thyroid Disorders

- 4.2.2 Aging Population Raises Routine Screening Volumes

- 4.2.3 High-Sensitivity 3rd-Gen Immunoassays Improve Clinical Utility

- 4.2.4 Government-Funded Newborn & Population Screening Programs

- 4.2.5 Direct-To-Consumer At-Home Test Kits & Tele-Lab Services

- 4.2.6 AI-Driven Reflex-Testing Algorithms Increase Test Orders

- 4.3 Market Restraints

- 4.3.1 Complex Interpretation & Biotin Interference Issues

- 4.3.2 Shortage Of Endocrinologists Slows Diagnosis & Follow-Up

- 4.3.3 Lab Test Price Compression from Bundled Contracts

- 4.3.4 Guideline Push-Back Against Over-Screening & Over-Treatment

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Test

- 5.1.1 TSH Test

- 5.1.2 Free/Total T4 Test

- 5.1.3 Free/Total T3 Test

- 5.1.4 Anti-TPO/Anti-TG Antibody Tests

- 5.1.5 Other Test

- 5.2 By Technique

- 5.2.1 Immunoassay (CLIA, ELISA, RIA)

- 5.2.2 Rapid Point-of-Care Tests

- 5.2.3 Mass Spectrometry

- 5.2.4 Other Techniques

- 5.3 By Sample Type

- 5.3.1 Serum/Plasma

- 5.3.2 Capillary Blood (Finger-prick)

- 5.3.3 Dried Blood Spot

- 5.4 By End User

- 5.4.1 Hospital

- 5.4.2 Diagnostic Laboratory

- 5.4.3 Other End Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Zhengzhou Autobio Co., Ltd.

- 6.3.3 bioMrieux SA

- 6.3.4 Danaher Corporation (Beckman Coulter)

- 6.3.5 DiaSorin SpA

- 6.3.6 F. Hoffmann-La Roche Ltd

- 6.3.7 Qualigen, Inc.

- 6.3.8 QuidelOrtho Corporation

- 6.3.9 Siemens Healthineers

- 6.3.10 Thermo Fisher Scientific Inc.

- 6.3.11 Werfen

- 6.3.12 Boditech Med Inc.

- 6.3.13 Ortho Clinical Diagnostics

- 6.3.14 Mindray Bio-Medical Electronics

- 6.3.15 Randox Laboratories

- 6.3.16 Tosoh Corporation

- 6.3.17 Diazyme Laboratories

- 6.3.18 Sysmex Corporation

- 6.3.19 PerkinElmer Inc.

- 6.3.20 IBL-America

- 6.3.21 Sekisui Diagnostics

- 6.3.22 Euroimmun AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment