|

시장보고서

상품코드

1852135

증후군 멀티플렉스 진단 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Syndromic Multiplex Diagnostic - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

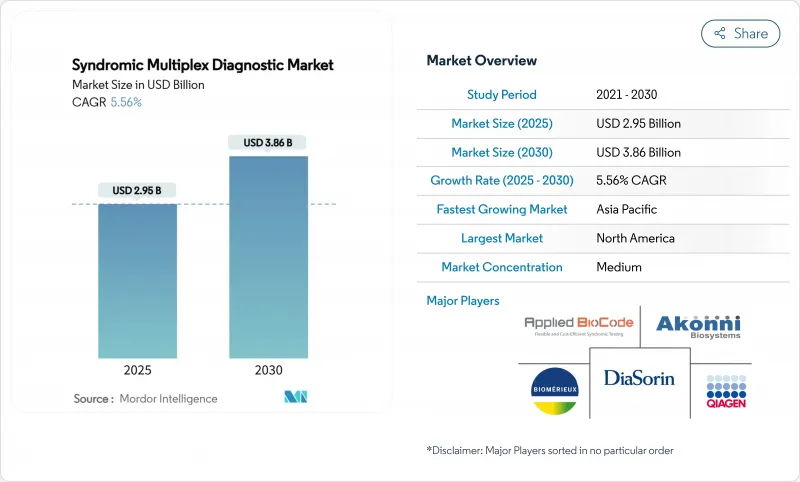

증후군 멀티플렉스 진단 시장 규모는 2025년에 29억 5,000만 달러에 이르고, 2030년에는 38억 6,000만 달러에 달할 것으로 예상되며, 이 기간의 CAGR은 5.56%를 나타낼 전망입니다.

이 확장은 하나의 검체에서 여러 병원체를 확인하고 검체 채취에서 표적 치료까지의 기간을 단축하는 정밀 검사로의 세계적인 변화에 직접 기인합니다. 호흡기 검사 패널은 유행 후 병원에 대한 투자와 의사가 멀티플렉스 호흡기 워크플로우에 익숙해지고 있다는 점을 뒷받침하며 여전히 주요 수익원이 되고 있습니다. 동시에 신경학에 특화된 패널은 다른 모든 임상 카테고리를 능가합니다. 이는 임상의가 수막염과 뇌염의 경우에 더 빠른 답변을 요구하기 때문이며, 이러한 경우는 지연이 사망률의 상승으로 이어집니다. 기술의 채택은 이러한 임상 우선 순위를 반영합니다. 멀티플렉스 PCR은 여전히 주류이지만 차세대 시퀀서(NGS) 플랫폼은 실험실이 보다 광범위한 유전체 프로파일링을 시도하기 때문에 가장 빠른 단위 성장을 기록하고 있습니다. 과거에는 몇 시간 안에 결과를 내고 있던 POC(Point-of-Care) 시스템이 현재는 약 15분 만에 실용적인 응답을 돌려주게 되어, 지불자는 조기 개입에 의한 의료비 절약을 인식하고 있습니다.

세계의 증후군 멀티플렉스 진단 시장 동향과 인사이트

감염증 이환율 상승

바이러스와 박테리아의 위협이 재연되고 있어 한 번의 검사로 중복 감염을 구별할 수 있는 폭넓은 호흡기, 소화기, 열성 질환 패널에 대한 수요가 높아지고 있습니다. WHO의 2024년 세계보건지출조사에서는 유행기간의 예산이 예방에서 급성기 의료로 향하고 멀티플렉스 어세이가 현재 채우는 진단 갭을 남기고 있는 것을 확인했습니다. 항균제 내성은 경험적 치료가 치료 실패의 위험을 수반하기 때문에 정확한 식별 필요성을 더욱 높여줍니다. 미국 FDA가 2024년에 원두와 같은 신흥 약물의 긴급 사용을 허가한 것은 검사실이 신속하게 재구성할 수 있는 전개 가능한 패널을 요구하는 규제 당국의 요구를 명확히 했습니다. 이러한 유연성은 종종 참조 실험실이 발생 지역에서 멀리 떨어진 곳에 있는 아프리카와 동남아시아 공중 보건 바이어를 끌어들입니다. 한편, 서유럽 병원에서는 내성 마커 검출을 일상적인 패혈증 검사에 통합하여 광역 항생제에 대한 노출을 줄이고 있습니다.

증가하는 분자진단 기술의 채택

헬스케어 관리자는 검사당 가격보다 총 비용 절감에 중점을 두고 있습니다. Multiplex PCR은 급성 호흡기 사례의 평균 재원 일수를 하루 단축하고 시약 비용 상승을 상쇄합니다. QIAGEN은 2024년에 QIAstat-Dx 호흡기 패널과 중추신경계 패널에 대해 여러 FDA 허가를 받았으며, 규제 당국이 증후군 신청 경로를 합리화하는 방법을 보여주었습니다. 디지털 PCR과 등온법은 성숙했고, 일부 플랫폼은 0.01% 대립유전자 빈도로 변이체를 검출하게 되었고, 종양학 및 이식 모니터링이 새로운 수익원으로 가능해졌습니다. CLIA의 면제로 미국 외래 진료소에서의 접근이 확대되고 증후군 멀티플렉스 진단 시장의 3차 센터 이외의 침투가 강화되었습니다.

증후군 검사 패널의 고비용

보편적인 확산을 막는 가장 큰 장애물은 여전히 가격입니다. 인도의 호흡기 패널은 입원 환자용 항생제의 전체 과정과 비슷한 비용이 들 수 있으며, 지방 병원은 검사를 배정해야 합니다. 미국에서는 MolDX 프로그램에 의해 알고리즘에 의한 감도의 주장 이상의 적용을 정당화하기 위해 제조업체에 임상적 유용성에 관한 서류를 제출하도록 요구하고 있습니다. 패널 크기의 인플레이션은 예산을 더욱 압박합니다. 30 표적 분석은 임상적으로 관련성이 있는 표적의 서브세트만이라도 상환액의 상한을 초과할 수 있습니다. 따라서 이해관계자는 입원 및 항생제 사용 감소와 지불을 연관시키는 위험 공유 모델을 모색하고 있지만, 이러한 합의에는 현재 수집하는 공급업체가 거의 없는 종단적인 결과 데이터가 필요합니다.

부문 분석

증후군 멀티플렉스 진단 시장의 2024년 매출액의 42.45%는 호흡기계 분석이었으며, 상환과 임상의에 대한 주지가 정착하고 있는 것으로 밝혀졌습니다. 한편, 중추신경계 패널은 조기 항바이러스 요법이나 항균 요법의 지침이 되는 신속 검사가 신경과 의사에게 받아들여지고 있기 때문에 2030년까지의 CAGR은 7.65%를 나타낼 전망입니다. 이러한 수요가 증가함에 따라 중추신경계 분야 시장 점유율은 현재 10%대 중반부터 10년 후까지 4분의 1에 이를 수 있습니다. 임상의는 배양을 우선하는 전략에서는 수막염 증례의 최대 50%로 병원체가 간과되기 때문에 소아나 이식 환자 집단에서는 멀티플렉스 분자 검사 결과가 필수적이라고 지적하고 있습니다. 패널의 상용화 압력은 호흡기 검사에서 더 두드러지며 공급업체는 순수한 분석 정확도보다는 빠른 런타임과 연결 기능으로 차별화를 도모합니다. Karius는 메타유전체 분석과 숙주 반응 마커를 결합한 폐 감염 분석에서 Breakhrough Device의 승인을 받았으며 호흡기 관리의 새로운 프론티어를 보여줍니다.

한편, 소화기계와 비뇨생식기계의 패널은 호흡기계와 중추신경계 검사에 뒤처져 있는 것, 매출 전체에 대한 기여는 꾸준히 상승을 계속하고 있습니다. 장관병원균에서 항생제 내성의 상승과 스튜어드십 프로그램의 필요성이 남아시아와 동남아시아의 3차 의료기관에서 소화기계 패널의 수주를 자극하고 있습니다. 요로 감염과 성 감염 패널은 CLIA 면제의 매장 승인을 통해 지역 클리닉을 수량 증가의 원동력으로 자리 매김하고 있습니다. FDA가 급성 열성 질환 패널에 별도의 장비 클래스를 설치하면 호흡기 감염과 전신성 감염에 걸친 멀티 신드롬 카트리지에 문이 열리고 현재 부문 구분이 모호해질 수 있습니다.

Multiplex PCR은 여전히 2024년 매출의 58.45%를 차지하며 증후군 멀티플렉스 진단 시장 점유율의 최대 슬라이스를 확보했습니다. 샘플 당 비용과 턴키 워크 플로우로 병원 실험실에 계속 통합되어 있습니다. 그러나 NGS의 CAGR은 8.12%이며, 시퀀싱 비용이 저하되면 지출 증가의 일부를 흡수할 수 있을 가능성이 있습니다. 실험실은 박테리아, 곰팡이, 바이러스, 기생충을 편차 없이 검출할 수 있는 NGS를 높이 평가했습니다. NGS 용도과 관련된 증후군 멀티플렉스 진단 시장 규모는 상환 경로가 임상 요구와 일치하면 2030년까지 10억 달러에 접근할 수 있습니다.

마이크로어레이는 제한된 동적 범위와 복잡한 워크플로우가 새로운 도입을 방해합니다. 디지털 PCR은 낮은 빈도의 내성 돌연변이와 종양에서 미세 잔류 병변을 모니터링하는 틈새 역할을 담당하지만 자본 강도가 보급을 제한하고 있습니다. DiaSorin사의 Liaison Plex는 PCR과 비드 기반 면역검출을 혼합한 모듈형 시스템으로 2024년 FDA 인증을 받아 하이브리드 미래 아키텍처를 제안했습니다.

지역 분석

북미는 확립된 상환, 전자 의료 기록 통합, 성숙한 외래 POC 네트워크를 통해 2024년 매출의 41.43%를 차지했습니다. 이 지역의 증후군 멀티플렉스 진단 시장 규모는 현재의 정책 기세 하에 2030년까지 16억 달러에 달할 가능성이 있습니다. CMS의 상환이 호흡기 패널과 패혈증 패널의 채용을 뒷받침하는 한편, 벤처 자금이 시판의 분자 검사를 대상으로 하는 신흥 기업을 지원합니다. 병원 그룹은 패널 결과를 항균제 관리 대시보드와 연결하기 위한 집중 데이터 분석을 점점 더 도입하고 채택을 강화하고 있습니다.

유럽에서는 IVDR의 준수에 따라 지속적인 시판 후 조사 데이터가 요구되기 때문에 꾸준하지만 완만한 확대가 계속되고 있습니다. 공중보건기구는 이민과 관련된 아웃브레이크를 신속하게 감지하기 위해 국경국에 멀티플렉스를 설치하는 데 도움을 줍니다. 이 지역의 성장은 POC 장비보다 미드스루풋 검사 시스템에 기울어져 있지만, 현재 논의되고 있는 CLIA와 동등한 면제 컨셉이 실시되면, 독일과 프랑스에서는 약국에서의 도입에 박차가 걸릴 가능성이 있습니다.

아시아태평양은 CAGR 6.43%와 가장 강력한 궤도를 그렸습니다. 중국은 2022년에 8조 5,000억 위안(GDP의 7.05%)의 의료비를 투입해 인도는 2024-2028년도 사이에 10-12%의 진단약 성장을 예측하고 있으며, 뎅기열, 진달래병, 다제 내성 결핵에 종사하는 증후군 플랫폼에 자금을 투자했습니다. 민간 파트너십은 클라우드 연결에 지원되는 카트리지식 PCR 장비를 지구 병원에 공급합니다. 일본과 한국은 정밀의료를 지원하기 위해 NGS를 도입한 병원 실험실의 업그레이드를 계속하고 간접적으로 미생물 시퀀싱 능력을 확대하고 있습니다.

남미와 중동 및 아프리카는 수익에서 후진을 숭배하고 있지만 의미있는 성장 포켓을 보여줍니다. 브라질은 지역 인플루엔자 감시를 위해 호흡기 멀티플렉스 검사에 투자하고 사우디아라비아는 이식 건수가 많은 3차 센터에서 CNS 패널을 시험적으로 도입하고 있습니다. 사하라 이남의 아프리카에서는 AFENET의 CoLTeP 이니셔티브가 검사 시설의 인증 확보를 지원하고 HIV에 인접한 기회감염을 다루는 멀티플렉스 설치를 위한 기증자 자금을 인출합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 감염증 증가

- 분자진단 기술의 채용 확대

- 확대하는 POC(Point-of-Care) 검사 인프라

- 증후군 패널에 대한 유리한 상환 정책

- 신흥국에서의 의료비 증가

- 멀티플렉스 PCR과 NGS 플랫폼의 기술적 진보

- 시장 성장 억제요인

- 증후군 검사 패널의 고비용

- 분자진단에 있어서 제한된 숙련 노동력

- 엄격한 규제 당국의 승인 프로세스

- 불충분한 임상 검사 정보 시스템의 통합

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 증후군 유형별

- 호흡기

- 위장관

- 중추신경계

- 요로감염 및 성병

- 기술 플랫폼별

- 다중 PCR

- 마이크로어레이 기반

- 등온 증폭

- NGS 기반

- 패널 규모별

- 10개 이하 표적

- 11-20개 표적

- 20개 이상 표적

- 최종 사용자별

- 병원

- 진단 실험실

- POC(Point-of-Care)/소매 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- bioMerieux

- Danaher(Cepheid)

- F. Hoffmann-La Roche(GenMark)

- Abbott

- Qiagen

- DiaSorin SpA(Luminex)

- Thermo Fisher Scientific

- Seegene Inc.

- Becton, Dickinson and Company

- Hologic Inc.(Mobidiag)

- Randox Laboratories

- Genetic Signatures

- Meridian Bioscience

- Bosch Healthcare Solutions

- Biocartis

- AusDiagnostics

- Accelerate Diagnostics

- OpGen(Curetis)

- Akonni Biosystems, Inc.

- QuantuMDx

- Applied BioCode

제7장 시장 기회와 향후 전망

KTH 25.11.25The syndromic multiplex diagnostic market size reached USD 2.95 billion in 2025 and is forecast to climb to USD 3.86 billion by 2030, reflecting a 5.56% CAGR over the period.

This expansion traces directly to a global shift toward precision testing that identifies multiple pathogens from a single specimen, shortening the path between specimen collection and targeted therapy. Respiratory test panels remain the primary revenue generator, fueled by post-pandemic hospital investments and physician familiarity with multiplex respiratory workflows. At the same time, neurology-focused panels outpace every other clinical category as clinicians seek faster answers for meningitis and encephalitis cases where delays translate into higher mortality. Technology adoption mirrors these clinical priorities: multiplex PCR continues to dominate, yet next-generation sequencing (NGS) platforms are posting the fastest unit growth as laboratories experiment with broader genomic profiling. Another catalyst is surging demand for near-patient testing; point-of-care systems that once delivered results in hours now return actionable answers in roughly 15 minutes, prompting payers to recognize the cost-of-care savings that flow from earlier intervention.

Global Syndromic Multiplex Diagnostic Market Trends and Insights

Rising Prevalence of Infectious Diseases

Resurgent viral and bacterial threats elevate demand for broad respiratory, gastrointestinal, and febrile-illness panels that can distinguish co-infections in a single run. WHO's 2024 global health spending study confirmed pandemic-era budget reallocations away from prevention and toward acute care, leaving diagnostic gaps that multiplex assays now fill. Anti-microbial resistance compounds the need for precise identification because empiric therapy risks treatment failure. The United States FDA's emergency-use authorizations for emerging agents such as monkeypox in 2024 underscored regulators' desire for deployable panels that laboratories can reconfigure quickly. This flexibility attracts public-health buyers in Africa and Southeast Asia, where reference labs often sit far from outbreak zones. Hospitals in Western Europe, meanwhile, are integrating resistance-marker detection into routine sepsis work-ups to reduce broad-spectrum antibiotic exposure.

Growing Adoption of Molecular Diagnostic Technologies

Healthcare administrators increasingly weigh total-cost-of-care savings rather than per-test price. Multiplex PCR cuts average hospital stays by one day in acute respiratory cases, offsetting higher reagent costs. QIAGEN received multiple FDA clearances for its QIAstat-Dx respiratory and CNS panels during 2024, illustrating how regulators are streamlining pathways for syndromic submissions. Digital PCR and isothermal methods have matured; some platforms now detect variants at 0.01% allele frequency, enabling oncology and transplant monitoring as additional revenue streams. CLIA waiver status has widened access in U.S. outpatient clinics, strengthening the syndromic multiplex diagnostic market's penetration outside tertiary centers.

High Cost of Syndromic Test Panels

Pricing remains the chief obstacle to universal adoption. A respiratory panel in India can cost as much as an entire course of inpatient antibiotics, forcing provincial hospitals to ration testing. Payers in the United States ask manufacturers to submit clinical-utility dossiers under the MolDX program to justify coverage beyond algorithmic sensitivity claims. Panel size inflation further strains budgets; a 30-target assay may exceed reimbursement caps even when only a subset of targets is clinically relevant. Stakeholders therefore explore risk-sharing models that link payment to reduced hospitalization or antibiotic use, though such agreements require longitudinal outcomes data that few suppliers collect today.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Point-of-Care Testing Infrastructure

- Technological Advancements in Multiplex PCR and NGS Platforms

- Limited Skilled Workforce in Molecular Diagnostics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Respiratory assays generated 42.45% of 2024 revenue for the syndromic multiplex diagnostic market, highlighting entrenched reimbursement and clinician familiarity. Conversely, central nervous system panels are forecast to post a 7.65% CAGR through 2030 as neurologists embrace rapid testing that guides early antiviral or antibacterial therapy. This rising demand could lift the CNS segment's share of the syndromic multiplex diagnostic market size from the current mid-teens toward one-quarter by decade's end. Clinicians note that culture-first strategies miss pathogens in up to 50% of meningitis cases, making multiplex molecular results indispensable for pediatric and transplant populations. Panel commoditization pressures are more pronounced in respiratory testing, prompting vendors to differentiate via faster run times and connectivity features rather than pure analytic accuracy. Karius earned a Breakthrough Device nod for a lung-infection assay that combines metagenomic sequencing with host-response markers, signaling a new frontier in respiratory care.

Meanwhile, gastrointestinal and urogenital panels continue their steady climb, although their contribution to overall revenue trails respiratory and CNS testing. Rising antibiotic resistance in enteric pathogens and the need for stewardship programs stimulate orders for GI panels among tertiary centers in South and Southeast Asia. Urinary-tract and sexually-transmitted-infection panels benefit from CLIA-waived over-the-counter approvals, positioning community clinics as an incremental volume engine. FDA's creation of a separate device class for acute febrile illness panels opens doors for multi-syndrome cartridges that span respiratory and systemic infections, potentially blurring current segmentation demarcations.

Multiplex PCR still delivered 58.45% of 2024 revenue, securing the largest slice of the syndromic multiplex diagnostic market share. Its cost-per-sample and turnkey workflows keep it embedded in hospital labs. Yet NGS is tracking an 8.12% CAGR and could absorb a meaningful fraction of incremental spend as sequencing costs drop. Laboratories value NGS for unbiased detection across bacteria, fungi, viruses, and parasites-especially in chronic or immunocompromised cohorts where odd pathogens thrive. The syndromic multiplex diagnostic market size attached to NGS applications could approach USD 1 billion by 2030 if reimbursement pathways align with clinical need.

Microarrays are gradually ceding ground; their limited dynamic range and cumbersome workflows deter new installations. Digital PCR holds a niche in monitoring low-frequency resistance mutations and minimal residual disease in oncology, but its capital intensity limits penetration. Suppliers increasingly bundle multiple chemistries into a single chassis; DiaSorin's Liaison Plex mixes PCR and bead-based immunodetection in a modular system cleared by FDA in 2024, hinting at hybrid future architectures.

The Syndromic Multiplex Diagnostic Market Report is Segmented by Type of Syndrome (Respiratory, Gastrointestinal, Central Nervous System, and CUTI & STDs), Technology Platform (Multiplex PCR, and More), Panel Size (<=10 Targets, and More), End-User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 41.43% of 2024 revenue owing to established reimbursement, electronic medical-record integration, and a mature outpatient POC network. The syndromic multiplex diagnostic market size for the region could reach USD 1.6 billion by 2030 under current policy momentum. CMS reimbursement boosts adoption of respiratory and sepsis panels, while venture funding supports start-ups targeting over-the-counter molecular tests. Hospital groups increasingly deploy centralized-data analytics to correlate panel results with antimicrobial stewardship dashboards, reinforcing adoption.

Europe follows with steady but slower expansion as IVDR compliance demands continuous post-market surveillance data. Public health agencies subsidize multiplex installations in border countries to detect migrant-related outbreaks rapidly. Regional growth leans on mid-throughput laboratory systems rather than POC devices, yet CLIA-equivalent waiver concepts under discussion could spur pharmacy adoption in Germany and France once implemented.

Asia-Pacific posts the strongest trajectory at a 6.43% CAGR. China's 8.5 trillion-yuan health outlay in 2022 (7.05% of GDP) and India's projected 10-12% diagnostics growth between FY 2024 and FY 2028 are funneling capital toward syndromic platforms that tackle dengue, scrub typhus, and multi-drug-resistant tuberculosis. Public-private partnerships supply district hospitals with cartridge-based PCR units backed by cloud connectivity. Japan and South Korea continue upgrading hospital labs with NGS to support precision medicine, indirectly broadening microbial sequencing capacity.

South America and the Middle East & Africa trail in revenue but demonstrate meaningful growth pockets. Brazil invests in respiratory multiplex testing for regional influenza surveillance, while Saudi Arabia pilots CNS panels in tertiary centers managing high transplant volumes. In Sub-Saharan Africa, AFENET's CoLTeP initiative helps laboratories secure accreditation, unlocking donor funds for multiplex installations that handle HIV-adjacent opportunistic infections.

- bioMerieux

- Danaher (Cepheid)

- F. Hoffmann-La Roche (GenMark)

- Abbott Laboratories

- QIAGEN

- DiaSorin S.p.A (Luminex)

- Thermo Fisher Scientific

- Seegene

- Beckton Dickinson

- Hologic Inc. (Mobidiag)

- Randox Laboratories

- Genetic Signatures

- Meridian Bioscience

- Bosch Healthcare Solutions

- Biocartis

- AusDiagnostics

- Accelerate Diagnostics

- OpGen (Curetis)

- Akonni Biosystems, Inc.

- QuantuMDx

- Applied BioCode

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Infectious Diseases

- 4.2.2 Growing Adoption of Molecular Diagnostic Technologies

- 4.2.3 Expanding Point-of-Care Testing Infrastructure

- 4.2.4 Favorable Reimbursement Policies for Syndromic Panels

- 4.2.5 Increasing Healthcare Expenditure in Emerging Economies

- 4.2.6 Technological Advancements in Multiplex PCR and NGS Platforms

- 4.3 Market Restraints

- 4.3.1 High Cost Of Syndromic Test Panels

- 4.3.2 Limited Skilled Workforce in Molecular Diagnostics

- 4.3.3 Stringent Regulatory Approval Processes

- 4.3.4 Inadequate Laboratory Information System Integration

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type of Syndrome

- 5.1.1 Respiratory

- 5.1.2 Gastrointestinal

- 5.1.3 Central Nervous System

- 5.1.4 cUTI & STDs

- 5.2 By Technology Platform

- 5.2.1 Multiplex PCR

- 5.2.2 Microarray-Based

- 5.2.3 Isothermal Amplification

- 5.2.4 NGS-Based

- 5.3 By Panel Size

- 5.3.1 <=10 Targets

- 5.3.2 11-20 Targets

- 5.3.3 >20 Targets

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Laboratories

- 5.4.3 Point-Of-Care / Retail Clinics

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 bioMerieux

- 6.3.2 Danaher (Cepheid)

- 6.3.3 F. Hoffmann-La Roche (GenMark)

- 6.3.4 Abbott

- 6.3.5 Qiagen

- 6.3.6 DiaSorin S.p.A (Luminex)

- 6.3.7 Thermo Fisher Scientific

- 6.3.8 Seegene Inc.

- 6.3.9 Becton, Dickinson and Company

- 6.3.10 Hologic Inc. (Mobidiag)

- 6.3.11 Randox Laboratories

- 6.3.12 Genetic Signatures

- 6.3.13 Meridian Bioscience

- 6.3.14 Bosch Healthcare Solutions

- 6.3.15 Biocartis

- 6.3.16 AusDiagnostics

- 6.3.17 Accelerate Diagnostics

- 6.3.18 OpGen (Curetis)

- 6.3.19 Akonni Biosystems, Inc.

- 6.3.20 QuantuMDx

- 6.3.21 Applied BioCode

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment