|

시장보고서

상품코드

1852138

원편광 이색성 분광계 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Circular Dichroism Spectrometers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

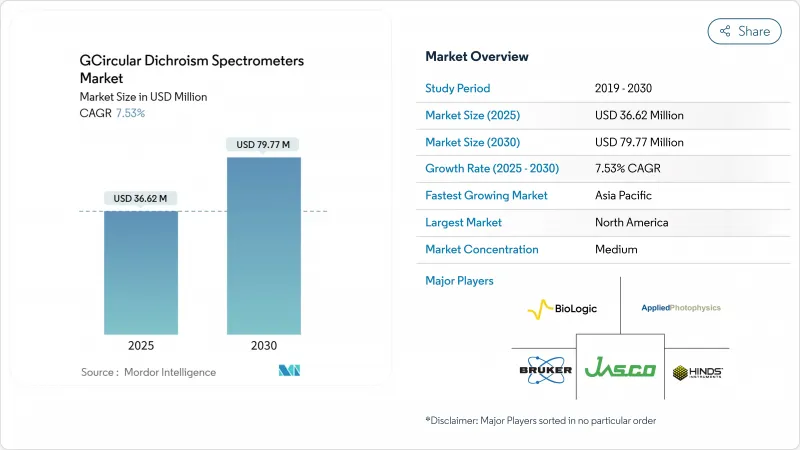

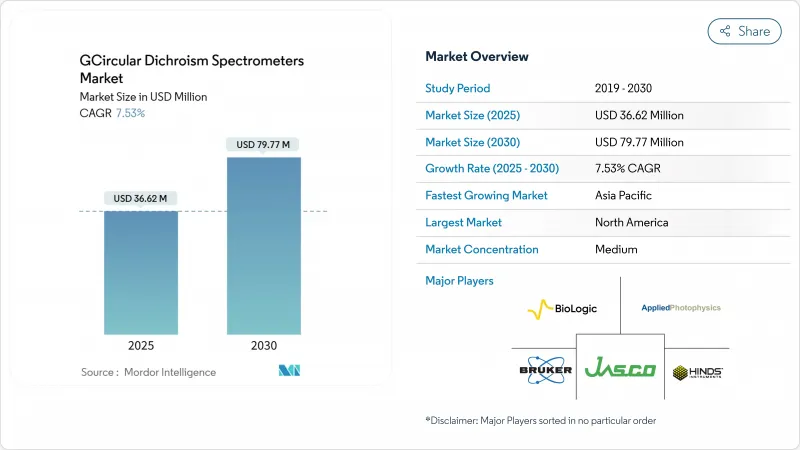

원편광 이색성 분광계 시장 규모는 2025년에 3,662만 달러, 2030년에는 7,977만 달러로 확대될 것으로 예측되고, CAGR은 7.53%를 나타낼 전망입니다.

실제로 이 분야의 기세는 바이오의약품 제조의 스케일 업, 바이오시밀러 파이프라인 증가, 고차 단백질 구조 검증에 대한 FDA-EMA의 기대 강화에 지지되고 있습니다. 또한 NIH와 NSF의 자금 지원을 통해 학문적 핵심 시설이 윤택한 자본을 유지하는 것도 수요를 지원합니다. 공급측의 진보, 특히 벤치탑의 자동화와 양자 캐스케이드 레이저 진동 CD는 샘플당 비용을 낮추고 사용의 용이성을 넓혀줍니다. 한편 중견의약품개발업무수탁기관(CRO)은 멀티유저 시스템을 구매하고 자본 지출을 피포스 서비스 수입으로 전환하는 경우가 늘어나고 있어 원편광 이색성 분광계 시장에 새로운 볼륨을 투입하고 있습니다. 공정 분석 기술을 중심으로 한 기술의 수렴은 지속적인 생물학적 제제 생산 라인에 직접 장비를 통합하여 일상적인 연구 예산 변동으로부터 공급업체를 추가로 격리합니다.

세계의 원편광 이색성 분광계 시장 동향과 인사이트

세계 바이오의약품 제조 확대

연속생산으로 이행하는 생물제제공장에서는 CD프로브를 프로세스라인에 직접 통합하여 실시간으로 접는 검증을 실시하여 보다 높은 처리량 사양을 추진하고 플로어 스탠드형 시스템을 지지하고 있습니다. 브루커의 2024년 매출이 33억 7,000만 달러로 급증한 것은 이러한 설비 투자 프로젝트와 관련된 장비의 보급을 뒷받침하고 있습니다. 벤더는 현재 자동 큐벳 체인저와 GMP 지원 소프트웨어를 번들로 운영자의 개입 시간을 단축하고 21 CFR Part 11의 기대에 부합하도록 하고 있습니다. 배치 출시량이 많으면 연금 수입을 확정하는 다년 서비스 계약도 촉진됩니다. 이러한 요인들이 결합되어 원편광 이색성 분광계 시장에는 견고한 컴플라이언스 플로어가 형성되어 있습니다.

생명과학기기에서 연구개발비 증가

NIH의 2025년 요구량 501억 달러는 보조금을 통한 실험실 업그레이드를 지속적으로 유지하고 NSF의 4,000만 달러의 단백질 설계 이니셔티브는 고급 구조 검증 키트 수요를 지원합니다. 학술 컨소시엄은 구매력을 강화하고 다양한 단백질 라이브러리에 해당하는 AI 구동 스펙트럼 디콘볼루션을 갖춘 벤치탑 장치를 선택합니다. 조달 사이클은 멀티 검출기 패키지를 지정하는 경우가 많아 턴키 시스템을 출하할 수 있는 제조업체가 보상되게 되어 있습니다. 이러한 자금력으로 장비의 갱신 간격이 안정되어 원편광 이색성 분광계 시장을 뒷받침하고 있습니다.

CD 시스템의 높은 자본 비용과 운영 비용

프리미엄 시스템은 GMP 소프트웨어 및 서비스 계약을 추가하면 25만 달러를 초과할 수 있으며 처음 구매하는 사람의 자본 예산을 압박합니다. 공급 체인 관세는 미국의 광학 부품 서브어셈블리 수입업체의 육상 비용에 10-15%를 올릴 위험이 있습니다. 운영비에는 액체 질소 물류, 램프 교체, 특수 교정기 등이 포함되어 총 소유 비용이 상승합니다. 공용시설 모델은 그 부담의 일부를 경감하지만, 예약의 병목이 발생해, 일각을 다투는 실험을 저해합니다. 이러한 요인은 가격에 민감한 지역에서 원편광 이색성 분광계 시장의 고성장에 대한 낙관적인 관점을 약화시키고 있습니다.

부문 분석

2024년 원편광 이색성 분광계 시장 규모에서는 벤치탑형이 45.34%의 압도적 점유율을 차지하며, 아카데믹 실험실과 중견 바이오 기업의 일상적인 단백질 폴드 스크리닝의 요구에 부응했습니다. 실험실은 컴팩트한 실적, 신속 스캔 모드, 옵션인 자동 플레이트 리더를 선택합니다. 플로어 스탠딩형은 절대적인 출하 대수가 적지만, 24시간 365일의 신뢰성과 높은 S/N비가 요구되는 연속 생산 라인이기 때문에 가장 빠른 대수 성장을 기록하고 있습니다. 국립 광원에 설치된 특수 SRCD 빔라인은 장파장이 필요한 틈새 막 단백질 프로젝트에 해당합니다. 하버드 메디컬 스쿨에 설치된 듀얼 J-1500은 벤치탑이 고처리량 안정성 연구의 중심이 되는 것을 보여줍니다. 예측에서 벤치탑은 계속해서 교체 주기를 지배하는 반면, 플로어 스탠드 플랫폼은 그린 필드 플랜트를 획득하고 원평광 이색성 분산계 시장에서 균형 잡힌 수익 믹스를 유지합니다.

이와 병행하여 제품 업그레이드는 카테고리 간의 경계를 모호하게 만듭니다. 벤더는 한때 대형 시스템 전용이었던 로봇 오토샘플러를 벤치 탑에 개조하여 소규모 실험실이 96웰 플레이트를 밤새 처리할 수 있도록 했습니다. 반대로 플로어 스탠드 모델에는 모듈형 광학계가 내장되어 있어 사용자가 공장을 향하지 않고 UV, 가시 및 중적외선 헤드를 교체할 수 있습니다. 이러한 기능의 동등성으로 인해 과거 가격 차이를 줄이면서 처리량과 견고성에 대한 차별화된 가치 제안을 지원합니다. 궁극적으로 진화하는 실험실 워크플로우는 두 제품 클래스의 확장을 보장하고 원평광 이색성 분산계 시장 전반에 걸쳐 광범위한 기회 기반을 강화합니다.

전자 CD는 2024년에도 원편광 이색성 분광계 시장 점유율의 55.32%를 차지했습니다. 그 이유는 원자외선 영역에서 단백질 과학자가 특이한 알파 헬릭스와 베타 시트의 지문을 얻을 수 있기 때문입니다. 이 조사방법은 성숙한 검증 가이드를 통해 규제 당국에 쉽게 제출할 수 있으며 배치 릴리스 분석의 기본값입니다. 싱크로트론 방사광 CD는 빔라인에 대한 액세스에 한정되는 것이며, 국립시설이 공업적인 대기시간을 개방해, 종래의 광학계에서는 도달 불가능한 170nm까지의 파장을 제공하기 때문에 CAGR이 가장 급속하게 성장하고 있습니다. 진동 CD는 키랄 저분자 QA/QC에 진입하고 있지만, 현재 사용자는 양자 캐스케이드 레이저 광원에 돈을 지불할 준비가 되어 있는 제약회사의 입체화학 그룹입니다. JASCO의 중적외 양자 캐스케이드 벤치 시스템은 획득 시간을 몇 시간에서 몇 분으로 단축함으로써 VCD가 틈새에서 일상적인 워크플로로 마이그레이션할 수 있음을 보여줍니다.

이 기술들 사이의 상호 수분은 증가하고 있습니다. 소프트웨어 패키지는 전자 및 진동 영역에 걸친 스펙트럼의 오버레이를 가능하게 하고 있으며, 단백질의 백본과 측쇄의 키랄성을 한눈에 볼 수 있게 되었습니다. 휴대용 SRCD 애드온도 평가 중이지만 빔타임을 사용할 수 있는지 여부가 중요한 요소입니다. SRCD와 VCD는 프리미엄 마진을 제공하며 원편광 이색성 분광계 시장 전반에 걸쳐 단계적인 가격 체계를 유지하고 있습니다.

지역 분석

북미는 2024년에 원편광 이색성 분광계 시장 점유율의 38.54%를 유지해, 성숙한 생물 제제 파이프라인, FDA의 엄격한 분석에 대한 기대, 자금력이 있는 학술 에코시스템에 지지되었습니다. NIH의 2025년 예산은 501억 달러로 공유 시설에서 일관된 장비 업데이트율을 보장합니다. 중요한 광학 부품 어셈블리에 10-15%의 관세가 걸릴 수 있으며 단기적으로 가격이 상승할 수 있지만 보증 할인과 임대 모델이 타격을 완화합니다. 캐나다에서는 백신제조의 증강이 진행되고 있으며, 특히 GMP제조 플로어용으로 설계된 바닥재형 CD라인의 지역 조달이 활발해지고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 8.53%로 가장 급성장하고 있는 지역으로, 중국의 현대적인 생물 제제 클러스터, 인도의 적극적인 바이오시밀러 목표, 일본의 재생 의료 품질 툴에 대한 투자가 뒷받침하고 있습니다. 중국 CD 벤더는 비용 최적화 벤치에 주력하고 있지만 세계 기업은 FDA 지원 검증 패키지가 필요한 다국적 합작투자에서 대용량 주문을 받고 있습니다. 인도의 국영 바이오 파크는 설비 대출을 일괄하여 실시하여 신흥 기업 수요를 끌어내고 있습니다. 이 지역적 기세는 중고 수입 장비에 대한 종속성을 줄여 원평광 이색성 분산계 시장 전체에서 프리미엄 부문의 침투를 가속화합니다.

유럽은 균형이 잡히지 만 성장은 둔화되고 있으며 대규모 제약 회사 개보수와 Horizon Europe의 연구 모집 전후에 안정적입니다. 독일과 스위스는 멤브레인 단백질 의약품에 대한 고정밀 CD에 대한 투자를 계속하고 있지만, 영국의 브레그짓 후 세관 이동으로 장비 배달의 계획 기간을 연장해야합니다. 동유럽의 CRO는 가격 경쟁력있는 서비스 허브로 부상하고 서양 스폰서를 유치하기 위해 중견 CD 유닛을 구입합니다. 라틴아메리카와 중동에서는 소규모이지만 현저한 성과가 나타나고, 현지 백신 구상이 파일럿 랩의 건설에 박차를 가하고 있습니다. 그러나 스펙트로스카피의 인재는 제한적이며 자금조달주기의 변동도 산발적이기 때문에 이 지역의 단기적인 상승 여지는 제한적입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계 바이오 의약품 제조 확대

- 생명과학 기기에 있어서 연구 개발비 증가

- 원이색성 하드웨어의 기술 혁신

- 신약 개발에 있어서 단백질 구조 분석 수요 증가

- 구조 생물학 연구에 대한 학술 자금 증가

- 공정 분석 기술을 위한 통합 분광학 플랫폼의 출현

- 시장 성장 억제요인

- CD 시스템의 높은 자본 비용과 운영 비용

- 훈련된 분광학 전문가의 제한된 가용성

- 고해상도 대체법에의 기호의 고조

- 새로운 CD기술에 대한 규제상의 밸리데이션의 과제

- 규제 상황(FDA, EMA, ICH Q5E, USP <781>)

- 기술 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 탁상형 원편광 이색성 분광계

- 플로어 스탠딩 원편광 이색성 분산계

- SRCD 빔라인 장치

- CD 마이크로 분산계

- 기술별

- 전자 CD(ECD)

- 진동 CD(VCD)

- 싱크로트론 방사선 CD(SRCD)

- 용도별

- 단백질 2차 구조 결정

- 백신학 및 항원 구조 연구

- 바이오시밀러 및 생물학적 제제 동등성 평가

- 품질 관리/배치 출시 시험

- 신약 개발 스크리닝 및 히트 검증

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 계약 연구/제조 기관(CROs/CMOs)

- 학술 및 정부 연구 기관

- 병원 및 진단 실험실

- 지리

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- JASCO

- Bruker

- Applied Photophysics

- Bio-Logic Science Instruments

- Hinds Instruments

- Thermo Fisher Scientific

- Agilent Technologies

- Shimadzu

- CRAIC Technologies

- Aviv Biomedical

- ISS Inc.

- Ocean Insight

- Quantum Design International

- HORIBA Scientific

- SpectroPolaritek

제7장 시장 기회와 향후 전망

KTH 25.11.25The circular dichroism spectrometers market size sits at USD 36.62 million in 2025 and is forecast to expand to USD 79.77 million by 2030, reflecting a steady 7.53% CAGR.

In practice, the sector's momentum is anchored in biopharmaceutical manufacturing scale-up, rising biosimilar pipelines, and tighter FDA-EMA expectations for higher-order protein structure validation. Demand is additionally supported by NIH and NSF funding streams that keep academic core facilities well capitalized. Supply-side advances-most notably benchtop automation and quantum-cascade-laser vibrational CD-lower per-sample costs and broaden usability. Meanwhile, mid-sized contract research organizations (CROs) increasingly purchase multi-user systems and convert capital outlays into fee-for-service revenues, injecting new volume into the Circular Dichroism Spectrometers market. Technology convergence around process analytical technology further insulates vendors from routine research budget swings, embedding instruments directly into continuous biologics production lines.

Global Circular Dichroism Spectrometers Market Trends and Insights

Expansion of Global Biopharmaceutical Manufacturing

Biologic plants shifting toward continuous production embed CD probes directly into process lines for real-time folding validation, driving higher-throughput specifications and favoring floor-standing systems. Bruker's 2024 revenue spike of USD 3.37 billion underscores the instrumentation pull-through tied to these capital projects. Vendors now bundle automated cuvette changers and GMP-ready software, shortening operator intervention time and aligning with 21 CFR Part 11 expectations. Larger batch-release volumes encourage multi-year service contracts that lock in annuity revenue. Together, these factors add a sturdy compliance floor beneath the Circular Dichroism Spectrometers market.

Rising R&D Expenditure in Life Sciences Instrumentation

NIH's FY 2025 request of USD 50.1 billion keeps grant-backed lab upgrades on pace, while the NSF's USD 40 million protein-design initiative anchors demand for advanced structure-validation kits. Academic consortia consolidate purchasing power, opting for benchtop instruments equipped with AI-driven spectral deconvolution that handles diverse protein libraries. Procurement cycles increasingly specify multi-detector packages, rewarding manufacturers able to ship turn-key systems. These funding dynamics promote steady instrument refresh intervals, buttressing the Circular Dichroism Spectrometers market.

High Capital and Operational Costs of CD Systems

Premium systems can exceed USD 250,000 once GMP software and service agreements are added, straining capital budgets for first-time buyers. Supply-chain tariffs risk adding 10-15% to landed costs for U.S. importers of optics sub-assemblies. Operational expenses include liquid-nitrogen logistics, lamp replacements, and specialized calibrants, lifting total cost of ownership. Shared-facility models relieve part of that burden but produce reservation bottlenecks that deter time-sensitive experiments. These factors collectively temper high-growth optimism for the Circular Dichroism Spectrometers market in price-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Technological Innovations in Circular Dichroism Hardware

- Growing Demand for Protein Structure Analysis in Drug Discovery

- Limited Availability of Trained Spectroscopy Professionals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Benchtop units delivered a commanding 45.34% share of Circular Dichroism Spectrometers market size in 2024 by meeting everyday protein-fold screening needs of academic labs and mid-tier biotechs. Laboratories choose them for compact footprints, rapid scan modes, and optional automated plate readers. Floor-standing models, although fewer in absolute shipments, record the fastest unit growth because continuous-manufacturing lines require 24/7 reliability and higher s/n ratios. Specialty SRCD beamline configurations, housed at national light-sources, serve niche membrane-protein projects where extended wavelengths matter. The Harvard Medical School installation of dual J-1500s illustrates how benchtops remain central to high-throughput stability studies. Over the forecast, benchtops will continue to dominate replacement cycles, while floor-standing platforms capture green-field plants, keeping a balanced revenue mix inside the Circular Dichroism Spectrometers market.

In parallel, product upgrades blur lines between categories. Vendors now retrofit benchtops with robotic autosamplers once exclusive to large systems, letting smaller labs process 96-well plates overnight. Conversely, floor-standing models incorporate modular optics so users swap in UV, visible, or mid-IR heads without factory service visits. This feature parity compresses the historical price spread yet supports differentiated value propositions around throughput and robustness. Ultimately, evolving lab workflows ensure both product classes expand, reinforcing the broad opportunity base across the Circular Dichroism Spectrometers market.

Electronic CD still held 55.32% of Circular Dichroism Spectrometers market share in 2024 because its far-UV range delivers the alpha-helix and beta-sheet fingerprints prized by protein scientists. The method's mature validation guides ease regulatory submissions, making it the default for batch-release assays. Synchrotron Radiation CD, while confined to beamline access, posts the briskest CAGR as national facilities open industrial queue time and deliver wavelengths down to 170 nm unattainable on conventional optics. Vibrational CD elbows into chiral-small-molecule QA/QC, though current users remain pharma stereochemistry groups ready to pay for quantum-cascade-laser sources. JASCO's mid-IR quantum-cascade bench system demonstrates that VCD can migrate from niche to daily workflow by shortening acquisition times from hours to minutes.

Cross-pollination among these technologies is growing. Software packages increasingly allow spectral overlay across electronic and vibrational regimes, providing a single-view protein backbone plus side-chain chirality. Portable SRCD add-ons are under evaluation, but beamtime availability stays the gating factor. Over the outlook, Electronic CD will remain the workhorse while SRCD and VCD supply premium margins, preserving a tiered pricing architecture across the Circular Dichroism Spectrometers market.

The Circular Dichroism Spectrometers Market Report is Segmented by Product Type (Benchtop CD Spectrometers, and More), Technology (Electronic CD (ECD), and More), Application (Protein Secondary-Structure Determination, and More), End User (Pharmaceutical & Biotechnology Companies, and More), Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 38.54% of Circular Dichroism Spectrometers market share in 2024, buoyed by mature biologics pipelines, FDA's rigorous analytical expectations, and a well-funded academic ecosystem. The NIH's 2025 appropriation of USD 50.1 billion guarantees consistent instrument refresh rates at shared facilities. A possible 10-15% tariff on critical optics assemblies could lift short-term prices, but warranty discounts and lease models cushion the blow. Canada's vaccine-manufacturing build-out amplifies regional procurement, particularly for floor-standing CD lines designed for GMP production floors.

Asia-Pacific is the fastest-expanding arena at an 8.53% CAGR through 2030, propelled by China's modern biologic clusters, India's aggressive biosimilar targets, and Japan's investment in regenerative medicine quality tools. Chinese CD vendors focus on cost-optimized benches, but global players win large-capacity orders at multinational joint-ventures needing FDA-ready validation packages. India's state-sponsored biotech parks bundle equipment financing, unlocking demand among start-ups. This regional momentum reduces historical dependency on imported second-hand gear and accelerates premium segment penetration across the Circular Dichroism Spectrometers market.

Europe exhibits balanced but slower growth, stabilizing around large pharma refurbishments and Horizon Europe research calls. Germany and Switzerland continue to invest in high-precision CD for membrane-protein drug work, while the UK's post-Brexit customs shifts require longer planning windows for instrument delivery. Eastern European CROs emerge as price-competitive service hubs, purchasing mid-tier CD units to attract western sponsors. Smaller but notable gains surface in Latin America and the Middle East, where local vaccine initiatives spur pilot lab construction. However, limited spectroscopy talent and sporadic funding cycle volatility temper near-term upside in those regions.

- Jasco

- Bruker

- Applied Photophysics

- Bio-Logic Science Instruments

- Hinds Instruments

- Thermo Fisher Scientific

- Agilent Technologies

- Shimadzu

- CRAIC Technologies

- Aviv Biomedical

- ISS

- Ocean Insight

- Quantum Design International

- HORIBA Scientific

- SpectroPolaritek

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope Of The Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Global Biopharmaceutical Manufacturing

- 4.2.2 Rising R&D Expenditure in Life Sciences Instrumentation

- 4.2.3 Technological Innovations in Circular Dichroism Hardware

- 4.2.4 Growing Demand for Protein Structure Analysis in Drug Discovery

- 4.2.5 Increasing Academic Funding for Structural Biology Research

- 4.2.6 Emergence of Integrated Spectroscopy Platforms For Process Analytical Technology

- 4.3 Market Restraints

- 4.3.1 High Capital and Operational Costs of CD Systems

- 4.3.2 Limited Availability of Trained Spectroscopy Professionals

- 4.3.3 Growing Preference for High-Resolution Alternative Methods

- 4.3.4 Regulatory Validation Challenges for New CD Technologies

- 4.4 Regulatory Landscape (FDA, EMA, ICH Q5E, USP <781>)

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat Of New Entrants

- 4.6.2 Bargaining Power Of Buyers

- 4.6.3 Bargaining Power Of Suppliers

- 4.6.4 Threat Of Substitutes

- 4.6.5 Intensity Of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Benchtop CD Spectrometers

- 5.1.2 Floor-Standing CD Spectrometers

- 5.1.3 SRCD Beamline Instruments

- 5.1.4 CD Microspectrometers

- 5.2 By Technology

- 5.2.1 Electronic CD (ECD)

- 5.2.2 Vibrational CD (VCD)

- 5.2.3 Synchrotron Radiation CD (SRCD)

- 5.3 By Application

- 5.3.1 Protein Secondary-Structure Determination

- 5.3.2 Vaccinology & Antigen Conformation Studies

- 5.3.3 Biosimilar & Biologic Comparability Assessments

- 5.3.4 Quality Control / Batch Release Testing

- 5.3.5 Drug Discovery Screening & Hit Validation

- 5.4 By End-User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Contract Research / Manufacturing Organizations (CROs/CMOs)

- 5.4.3 Academic & Government Research Institutes

- 5.4.4 Hospital & Diagnostic Laboratories

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 JASCO

- 6.3.2 Bruker

- 6.3.3 Applied Photophysics

- 6.3.4 Bio-Logic Science Instruments

- 6.3.5 Hinds Instruments

- 6.3.6 Thermo Fisher Scientific

- 6.3.7 Agilent Technologies

- 6.3.8 Shimadzu

- 6.3.9 CRAIC Technologies

- 6.3.10 Aviv Biomedical

- 6.3.11 ISS Inc.

- 6.3.12 Ocean Insight

- 6.3.13 Quantum Design International

- 6.3.14 HORIBA Scientific

- 6.3.15 SpectroPolaritek

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment