|

시장보고서

상품코드

1852148

포름산 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Formic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

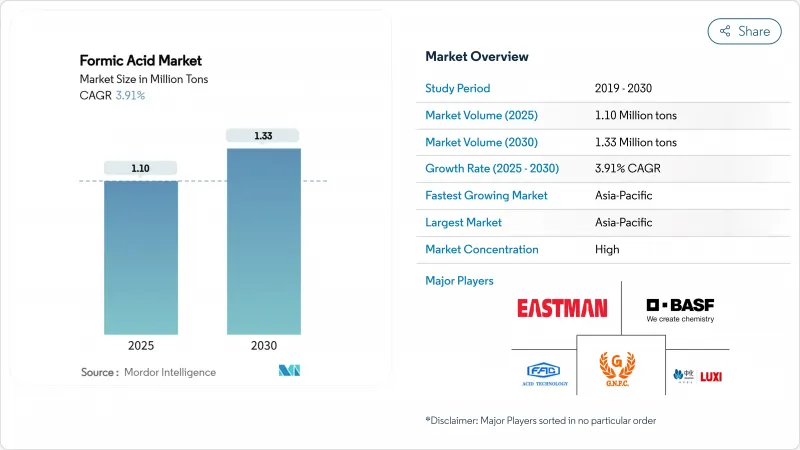

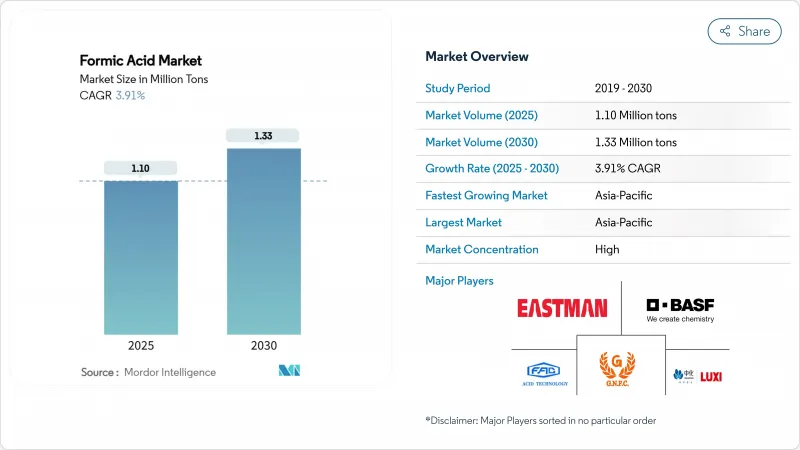

포름산 시장 규모는 2025년에 110만 톤, 예측기간(2025-2030년) CAGR은 3.91%를 나타내고, 2030년에는 133만 톤에 달할 것으로 예측됩니다.

항생제가없는 동물사료에 대한 수요 증가, 바이오 생산 투자 가속화, 가죽, 고무 및 의약품 응용 분야에서 꾸준한 흡수가이 성장 궤도를 지원합니다. 가축 사료의 보존은 이미 세계 소비의 37.04%를 차지하고 있으며 생산자가 저탄소 실적를 요구하고 있기 때문에 바이오의 루트는 CAGR 4.72%로 확대되고 있습니다. 지역적 기세는 아시아태평양이 견인하고 있으며, 풍부한 제조능력과 지원적인 정책에 따라 2030년까지 지역 CAGR은 4.61%가 될 것으로 예측됩니다. 공정 혁신, 특히 전기화학적 CO2-포름산 전환은 파일럿 프로젝트가 상업적 규모로 전환됨에 따라 공급 경제성을 더욱 재구성할 수 있습니다.

세계 포름산 시장 동향과 통찰

가축 사료 및 사일리지 첨가물에 대한 수요 증가

항생제를 사용하지 않는 가축 생산에 대한 수요로 인해 포름산은 방부제 및 항균제로 선호됩니다. 닭의 사료에 4 kg/톤 배합하는 것으로, 살모넬라균의 수를 검출할 수 없는 레벨까지 감소시킬 수 있어 식품의 안전성을 지키고, 규제 준수를 강화할 수 있습니다. 유럽식품안전기관은 돼지에는 12,000mg/kg까지, 닭에는 10,000mg/kg까지의 함유율을 인정하고 있으며, 법적인 확실성을 제공함으로써 채택을 가속시키고 있습니다. 이러한 요인이 상반되어 사료부문의 소비가 시장 전체의 성장률을 상회합니다.

가죽 및 태닝 산업의 큰 수요

고급 가죽 생산에서는 포름산을 사용하여 욕조의 pH를 3.8-4.2로 조정하여 크롬 고정을 촉진하고 미네랄산에 비해 염분 부하를 저감하고 있습니다. 세계의 가죽의 대부분을 공급하는 중국이나 인도의 탄너에서는 순도 85% 이상을 지정하는 곳이 증가하고 있어 일관성을 보증할 수 있는 공급자에게는 가격 프리미엄의 기회가 퍼지고 있습니다.

메탄올 원료 가격 변동

메탄올은 포름산 메틸 가수분해에 있어서 생산 비용의 60-70%를 차지하기 때문에 천연 가스에 연동하는 가격 변동은 이폭을 압박하고 장기 공급 계약을 복잡하게 하고 있습니다. 생산자는 신재생에너지 가격이 계속 줄어들면 원료 의존을 해소할 수 있는 CO2 전해 환원 경로를 시험적으로 도입함으로써 헤지하고 있습니다.

부문 분석

사료·사일리지 첨가물은 2024년 세계 판매량의 37.04%를 차지했고, 이 부문이 포름산 시장 규모의 최대 부분을 차지합니다. 항생제 성장 촉진제의 규제 억제에 힘입어 이 점유율은 CAGR 4.21%로 확대될 것으로 예측됩니다. 닭고기 사료는 4kg/t의 배합률로 살모넬라균이 검출되지 않게 되어, 농가의 신뢰와 소매점의 수용을 높이고 있습니다. 가죽 태닝은 산의 pH 조절과 크롬 침투의 이점을 살린 2위의 용도를 유지하고 있으며, 섬유공장은 염료욕의 완충능력을 평가했습니다. 고순도가 요구되는 의약품이나 특수 화학제품의 용도도 대두해 왔으며, 프리미엄 가격이 붙어 있습니다.

성장의 전망은 천연 고무 가공에도 더 빠른 응고 속도론과 더 높은 응집 인장 강도를 위해 포름산이 채택되고 있습니다. 세정과 스케일 제거는 무기산보다 환경 부하가 낮고 산의 미네랄 스케일의 용해력을 활용하여 안정된 틈새를 차지하지만 규모는 작습니다. SoftAcid와 같은 안전 설계된 제형은 소규모 사업자의 접근을 확대하고 예측 기간 동안 수요 증가를 시사합니다.

포름산 세계 시장은 용도(사료 및 사일리지 첨가물, 피혁 태닝, 기타), 생산 방법(포름산메틸 가수분해, 카르보닐화 기술, 기타 생산 방법), 최종 이용 산업(농업, 피혁 및 신발 등), 지역(아시아태평양, 북미 등)으로 구분됩니다. 시장 예측은 수량(톤)으로 제공됩니다.

지역별 분석

아시아태평양은 2024년 세계 소비량의 53.21%를 차지하고 포름산 시장 점유율의 최대 부분을 차지합니다. 중국은 이 지역공급을 지배하고 있으며, 메탄올과 강하의 화학 조합을 통합하여 비용 경쟁력을 확보하고 있습니다. 인도의 생산자는 수출 장려책과 국내 피혁 생산량 증가에 힘입어 지역의 자급률을 높이는 신공장을 건설하고 있습니다. 일본과 한국은 일렉트로닉스와 의약품 합성을 위해 고순도 원료를 조달하고 인도네시아는 고무 섹터의 흡수에 의해 더욱 성장을 추진하고 있습니다.

북미는 광대한 동물성 단백질 부문과 CO2 이용의 연구개발에 대한 정부 자금에 힘입어 2위의 지역입니다. 미국은 전기화학 생산장치의 시험적 전개를 선도하고 있으며, 10년 후까지는 상업 규모에 이를 것을 목표로 하고 있습니다. 캐나다 수요는 주로 곡물과 가축의 생산과 관련이 있지만 멕시코에서는 가죽과 섬유의 사용이 증가하고 있습니다.

유럽은 엄격한 사료·화학물질 규제와 적극적인 탈탄소화 목표를 겸비하여 바이오프로세스에 대한 투자에 박차를 가하고 있습니다. EU 수입 화학물질에 대한 안티덤핑 조치는 경쟁을 격화시키고 현지에서 생산 능력 확대를 촉진합니다. 남미는 브라질의 확대하는 축산 부문을 중심으로 성장하고 중동은 특수화학제품에 대한 투자를 촉구하는 다각화 정책의 혜택을 받습니다. 아시아가 수출을 늘리고 서쪽 지역이 저탄소 공급망으로 축발을 옮기면서 지역을 넘어선 무역 흐름은 유동적이 될 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 가축 사료와 사일리지 첨가물 수요 증가

- 가죽 및 태닝 산업의 상당한 수요

- 고무 제품 수요 증가

- 항균 특성에 대한 제약 산업의 채택 증가

- 바이오 베이스 생산 기술의 진전

- 시장 성장 억제요인

- 메탄올 원료 가격의 변동

- 부식과 취급에 관한 위험

- 바이오 프로피온산 대체 사용 증가

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 가격 분석

제5장 시장 규모와 성장 예측

- 용도별

- 사료 및 사일리지 첨가물

- 가죽 태닝

- 섬유 염색 및 마무리

- 의약·화학제품 중간체

- 기타 용도(고무·라텍스 응고제, 세정·탈스케일제 등)

- 생산방법별

- 포름산메틸 가수분해

- 카르보닐화 기술

- 기타 제조 방법(옥살산 루트, 발효·바이오 루트)

- 최종 이용 산업별

- 농업

- 가죽 및 신발

- 섬유

- 화학물질 및 용매

- 의약품

- 고무

- 기타 최종 사용자 산업(석유 및 가스, 식품 및 음료 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- BASF

- Eastman Chemical Company

- Gujarat Narmada Valley Fertilizers and Chemicals Ltd

- Luxi Chemical Group Co.,Ltd.

- Perstorp

- POLIOLI SpA

- Sintas Kurama Perdana

- Rashtriya Chemicals and Fertilizers Ltd

- Shandong Acid Technology Co., Ltd.

- Shandong Rongyue Chemical Co. Ltd

- Wuhan Ruisunny Chemical Co. Ltd

제7장 시장 기회와 장래의 전망

SHW 25.11.19The Formic Acid Market size is estimated at 1.10 Million tons in 2025, and is expected to reach 1.33 Million tons by 2030, at a CAGR of 3.91% during the forecast period (2025-2030).

Rising demand for antibiotic-free animal feed, accelerating investment in bio-based production, and steady uptake across leather, rubber, and pharmaceutical applications underpin this growth path. Animal feed preservation already captures 37.04% of global consumption, and bio-based routes are expanding at 4.72% CAGR as producers seek lower-carbon footprints. Regional momentum is led by Asia-Pacific, where abundant manufacturing capacity and supportive policies are expected to secure a 4.61% regional CAGR through 2030. Process innovation-most notably electrochemical CO2-to-formic acid conversion-could further reshape supply economics as pilot projects move toward commercial scale

Global Formic Acid Market Trends and Insights

Growing Demand for Animal Feed and Silage Additives

Demand for antibiotic-free livestock production has positioned formic acid as a preferred preservative and antimicrobial. At 4 kg/ton in poultry diets, the acid can drive Salmonella counts to undetectable levels, safeguarding food safety and reinforcing regulatory compliance. The European Food Safety Authority allows inclusion rates up to 12,000 mg/kg for pigs and 10,000 mg/kg for poultry, providing legal certainty that accelerates adoption. These factors collectively lift feed-segment consumption above overall formic acid market growth.

Substantial Demand from Leather and Tanning Industry

Premium leather production relies on formic acid to adjust bath pH to 3.8-4.2, accelerating chrome fixation while lowering salt loads compared with mineral acids. Chinese and Indian tanneries, which supply a sizable portion of global hides, increasingly specify >= 85% purity, opening price-premium opportunities for suppliers able to guarantee consistency.

Methanol Feedstock Price Volatility

Because methanol represents 60-70% of production costs in methyl formate hydrolysis, natural-gas-linked price swings compress margins and complicate long-term supply contracts. Producers are hedging by piloting CO2 electro-reduction routes that could break feedstock dependence if renewable power prices keep falling.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Rubber Products

- Growing Adoption in Pharmaceutical Industry for Antibacterial Properties

- Risks Related to Corrosion and Handling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Animal feed & silage additives controlled 37.04% of global volume in 2024, giving the segment the largest slice of formic acid market size. Supported by regulatory curbs on antibiotic growth promoters, this share is projected to widen at a 4.21% CAGR. In poultry rations, inclusion rates of 4 kg/ton eliminate detectable Salmonella, boosting farmer confidence and retailer acceptance. Leather tanning remains the second-largest application, capitalizing on the acid's pH control and chrome-penetration benefits, while textile mills value its dye-bath buffering capability. Pharmaceutical and specialty chemical uses are emerging, where high-purity requirements yield premium prices.

Growth prospects extend to natural rubber processing, which adopts formic acid for faster coagulation kinetics and higher aggregate tensile strength. Cleaning and descaling occupy a steady but smaller niche, leveraging the acid's mineral-scale dissolving power at lower environmental impact than stronger inorganic acids. Safety-engineered formulations such as SoftAcid broaden access among smaller operations, suggesting incremental demand upside over the forecast period.

The Global Formic Acid Market is Segmented by Application (Animal Feed and Silage Additives, Leather Tanning, and More), Production Method (Methyl Formate Hydrolysis, Carbonylation Technology, and Other Production Methods), End-Use Industry (Agriculture, Leather and Footwear, and More) and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific held 53.21% of global consumption in 2024, giving the region the largest slice of formic acid market share. China dominates regional supply, leveraging integrated methanol and downstream chemical complexes to ensure cost competitiveness. India's producers, supported by export incentives and growing domestic leather output, are building new plants that lift regional self-sufficiency. Japan and South Korea source high-purity material for electronics and pharmaceutical synthesis, while Indonesia drives incremental growth through rubber-sector uptake.

North America is the second-largest region, propelled by a vast animal-protein sector and government funding for CO2-utilization R&D. The United States leads pilot deployment of electrochemical production units, eyeing commercial scale by decade-end. Canada's demand is tied mainly to grain and livestock production, whereas Mexico sees rising leather and textile usage.

Europe combines strict feed and chemical regulations with aggressive decarbonization targets, spurring investment in bio-based processes. EU anti-dumping measures on imported chemicals intensify competition and encourage local capacity expansion. South America's growth centers on Brazil's expanding livestock sector, while the Middle East benefits from diversification agendas that encourage specialty-chemical investments. Cross-regional trade flows will likely stay fluid as Asia grows exports and western regions pivot to low-carbon supply chains.

- BASF

- Eastman Chemical Company

- Gujarat Narmada Valley Fertilizers and Chemicals Ltd

- Luxi Chemical Group Co.,Ltd.

- Perstorp

- POLIOLI SpA

- Sintas Kurama Perdana

- Rashtriya Chemicals and Fertilizers Ltd

- Shandong Acid Technology Co., Ltd.

- Shandong Rongyue Chemical Co. Ltd

- Wuhan Ruisunny Chemical Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Animal Feed and Silage Additives

- 4.2.2 Substantial Demand from Leather and Tanning Industry

- 4.2.3 Increasing Demand for Rubber Products

- 4.2.4 Growing Adoption in Pharmaceutical Industry for Antibacterial Properties

- 4.2.5 Growing Advancements in its Bio-based Production Technologies

- 4.3 Market Restraints

- 4.3.1 Methanol feedstock price volatility

- 4.3.2 Risks Related to Corrosion and Handling

- 4.3.3 Rising Usage of bio-propionic acid as alternative

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Price Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Application

- 5.1.1 Animal Feed and Silage Additives

- 5.1.2 Leather Tanning

- 5.1.3 Textile Dyeing and Finishing

- 5.1.4 Intermediary in Pharmaceuticals and Chemicals

- 5.1.5 Other Applications (Rubber and Latex Coagulation, Cleaning and Descaling Agents, etc.)

- 5.2 By Production Method

- 5.2.1 Methyl Formate Hydrolysis

- 5.2.2 Carbonylation Technology

- 5.2.3 Other Production Methods (Oxalic-acid Route, Fermentation/Bio-based Route)

- 5.3 By End-use Industry

- 5.3.1 Agriculture

- 5.3.2 Leather and Footwear

- 5.3.3 Textile

- 5.3.4 Chemicals and Solvents

- 5.3.5 Pharmaceuticals

- 5.3.6 Rubber

- 5.3.7 Others End User Industries (Oil and Gas, Food and Beverage, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Eastman Chemical Company

- 6.4.3 Gujarat Narmada Valley Fertilizers and Chemicals Ltd

- 6.4.4 Luxi Chemical Group Co.,Ltd.

- 6.4.5 Perstorp

- 6.4.6 POLIOLI SpA

- 6.4.7 Sintas Kurama Perdana

- 6.4.8 Rashtriya Chemicals and Fertilizers Ltd

- 6.4.9 Shandong Acid Technology Co., Ltd.

- 6.4.10 Shandong Rongyue Chemical Co. Ltd

- 6.4.11 Wuhan Ruisunny Chemical Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Sustainable Use of Formic Acid in Fuel Cell