|

시장보고서

상품코드

1852152

메타물질 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Metamaterials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

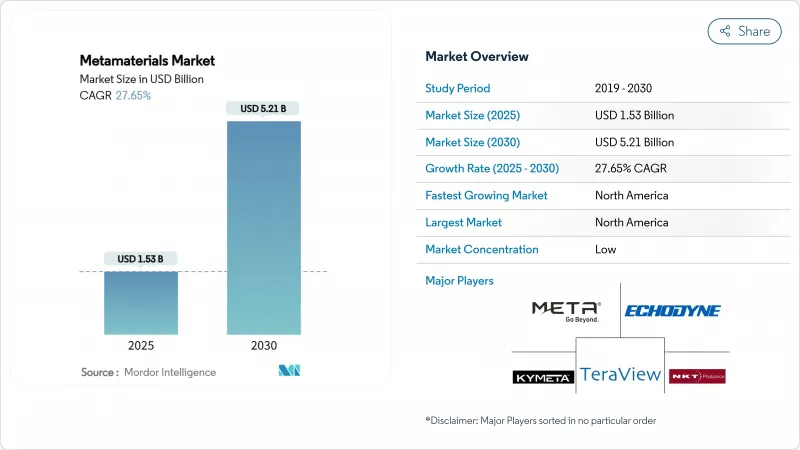

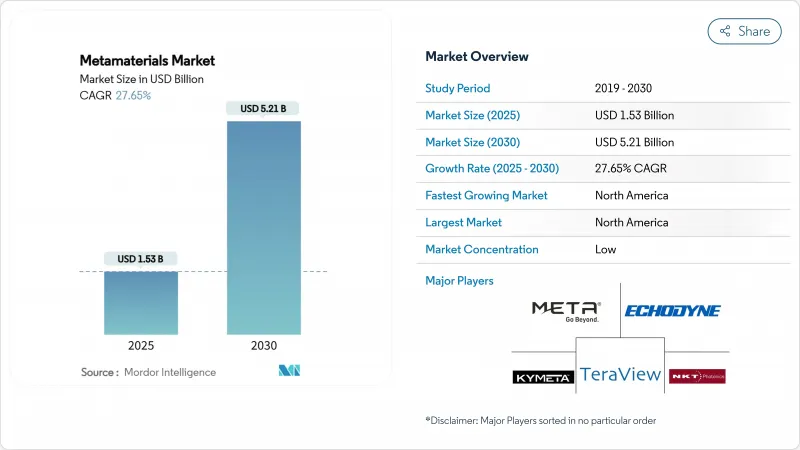

메타물질 시장 규모는 2025년에 15억 3,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 27.65%로, 2030년에는 52억 1,000만 달러에 달할 것으로 예상됩니다.

북미는 지역별로 35.88%의 점유율을 차지하고 있으며, 2030년까지 연평균 복합 성장률(CAGR)은 28.92%로 가장 빠르게 성장하고 있습니다. 수요의 핵심은 5G/6G 배포, 방어 스텔스 요구 사항, 에너지 효율적인 장치입니다. 전자기 메타물질은 안테나와 주파수 선택성 표면에서의 다용도 역할로 수익의 44.19%를 차지합니다. 안테나 및 레이더 시스템은 이미 지출의 62.94%를 차지하고 있으며 항공우주 및 방어 바이어는 최종 사용자 수요의 54.19%를 차지하고 있습니다. 틈새 전문가가 독자적인 디자인을 상용화하기 때문에 경쟁 분야는 단편적입니다. 높은 제조 비용과 제한된 표준화가 널리 보급되는 것을 방해하고 있지만, 적층 조형과 나노 패브리케이션의 급속한 진보가 이러한 제약을 좁히고 있습니다.

세계의 메타물질 시장 동향과 인사이트

5G 및 6G 네트워크 계획 확대 차세대 커넥티비티를 실현하는 메타물질

메타물질 기반 안테나는 몇 기가비트의 처리량을 유지하면서 빔 제어 하드웨어를 초박층으로 압축하여 mm파 전송을 재정의합니다. 60GHz에서 입증된 디지털 코딩된 메타서피스는 여러 개의 동시 빔을 생성하고 도시 지역에서 신호 차단을 완화하며 6G의 신뢰성을 지원하는 능력을 갖추고 있습니다. 2D 메타서피스는 지상파 이외의 5G/6G 커버리지의 링크 버짓을 향출시킵니다. 상업 벤더는 실험실 프로토타입의 범위를 넘어 재구성 가능한 지능형 표면을 통합한 하이브리드 위성 단말로 모바일 플랫폼의 중단 없는 연결성을 확보하고 있습니다. 얇은 하드웨어와 소프트웨어 정의 제어의 이러한 조합은 통신 사업자가 세계의 고대역 네트워크를 고밀도화함에 따라 메타물질 시장을 지속적인 통신 지출에 위치시킵니다.

나노기술과 재료 과학의 발전 : 원자 규모의 정밀 공학

연방정부 프로그램은 2025년 22억 달러를 국가 나노기술 구상 하에 요구하고 있으며 누적 지출은 450억 달러를 넘어 원자 규모 제조를 위한 공유 인프라를 제공합니다. 레이어 바이 레이어의 적층 조형법은 현재, 표면 전체에 걸쳐 연속적으로 변화하는 경사 지수 프로파일을 구축하고, 엔지니어에게 위상, 진폭, 편광을 국소적으로 조정하는 툴 박스를 부여하고 있습니다. 이러한 정확도는 메타 재료를 구조 건강 모니터, 생물 의학 임플란트 및 자동차 레이더 하우징에 삽입하는 것을 가속화합니다. 3D 프린팅된 인터로킹 블록을 사용하여 주파수 선택성 업소버를 생성하는 초기 생산 테스트에서는 공구 단계를 줄이면서 99.5%의 흡수율을 달성했습니다. 이러한 돌파구는 진입 장벽을 낮추고, 중기적으로는 주류 디바이스 제조업체들에게 대량 생산을 가능하게 합니다.

메타물질 : 시장 침투를 막는 지식 격차의 인식 부족

복잡한 파동 물리학의 개념은 전용 연구 개발 예산이없는 분야의 의사 결정자를 망설이게합니다. 미국 국립과학재단은 이 격차를 실제 훈련으로 채우기 위해 선진 제조업 노동력 프로그램에 3억 8,667만 달러를 기록했습니다. 안테나의 소형화와 노이즈 감쇠의 장점을 시각화하는 실증 프로젝트는 채용을 확대하고 있지만, 라틴아메리카와 동남아시아의 일부 중소기업은 여전히 학습 곡선이 어려운 것에 직면하고 있습니다.

부문 분석

전자유도형은 2024년 매출액의 44.19%를 차지했으며, CAGR 29.27%를 나타낼 것으로 예측되어 메타물질 시장의 핵심 역할을 강화하고 있습니다. 주파수 선택 패널, 위상 배열 안테나, 네거티브 지수 렌즈로의 통합으로 통신 및 방어 분야에서 수요가 확대되고 있습니다. 금액 기준으로 이 집단은 메타물질 시장 규모의 7억 2,259만 달러를 차지하고, 2030년에는 30억 달러를 넘는 기세입니다. 생물화학적 감도를 높인 그래핀 공진기에 의한 테라헤르츠 검출의 상승은 미래의 기회를 증가시킵니다.

음향, 쌍곡선 및 음수 지수와 같은 새로운 틈새는 기능적인 팔레트를 확장합니다. 음향 구조는 EU가 자금을 제공하는 METAVISION 시험에 의해 산업 플랜트의 기계 진동을 감쇠시킵니다. 쌍곡면 슬래브는 초해상 이미징을 위한 하위 회절 광자를 채널링하여 의료 진단의 자산이 됩니다. 여러 클래스를 융합시킨 하이브리드 스택은 소리, 열, 빛의 멀티모달 제어를 하나의 라미네이트로 가능하게 합니다. 따라서 연구에 대한 관심이 다양화를 가속시키는 한편, 전자파의 우위성을 스케일로 강화하고 있습니다.

지역 분석

북미는 35.88%의 점유율을 차지하고, CAGR은 28.92%로 가장 높습니다. 선진제조업과 노동력 프로그램을 위한 연방정부 투자는 3억 8,667만 달러로 견고한 혁신 생태계를 강화하고 있습니다. 항공우주, 방위, 전기통신의 프라임이 집중됨으로써 초기 단계 수요가 보장되고 현지 공급업체가 대량생산 방식을 개량할 수 있게 됩니다.

아시아태평양은 산업화와 전자공학 능력이 대규모 공적 자금으로 수렴하고 있습니다. 중국의 전략적 기술 계획은 자원을 6G 및 위성 네트워크로 향하게 하고, 기지국 및 휴대 단말 안테나용 메타서피스의 현지 채용을 가속화하고 있습니다. 인도 전자제품 생산액은 생산연계인센티브(PLI) 제도 하에서 2020-21 회계연도 55조 4천억 루피(760억 달러)에서 2023-2024 회계연도 95조 2천억 루피(1,150억 달러)로 증가하며 반도체 등급 메타물질 부품에 대한 비옥한 토대를 마련했습니다. 일본과 한국은 자율주행차와 스마트 공장용 고주파 레이더 흡수체를 정제하고 있습니다.

영국의 혁신 전략과 독일 인더스트리 4.0 로드맵 아래, 첨단 재료를 대상으로 한 관민 프로그램 덕분에 유럽은 큰 점유율을 차지하고 있습니다. 낮은 자기장 MRI와 산업 소음 감소의 현장 시험은 활발한 공동 연구 네트워크를 증명합니다. 정책 프레임 워크는 개방형 테스트 베드와 표준화를 중시하고 메타물질 시장을 국경을 넘은 확장 성으로 이끌고 있습니다.

남미와 중동, 아프리카는 메타물질로 강화된 전기통신 백본을 활용해 레거시 인프라를 뛰어넘는 새로운 프론티어입니다. 원격 센서 노드에 전력을 공급하는 에너지 수확 메타서피스는 지역의 비전화 우선순위에 부합하며, 비용 장벽이 완화되면 미개척의 가능성을 나타냅니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 5G와 6G 네트워크 계획 확대

- 나노기술과 재료과학의 진보

- 양자 컴퓨팅과 포토닉스의 진전

- 항공우주 및 방위산업에서의 수요 증가

- 에너지 효율과 지속가능성의 중시의 고조

- 시장 성장 억제요인

- 메타물질의 장점 인식 부족

- 메타물질의 합성 비용

- 재료의 내구성과 표준화의 우려

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 특허 분석

제5장 시장 규모와 성장 예측

- 유형별

- 전자

- 테라헤르츠

- 광자

- 가변형

- 주파수 선택 표면(FSS)

- 기타 유형(음향, 음지수 및 쌍곡선, 비선형 및 키랄)

- 용도별

- 안테나 및 레이더

- 센서

- 은폐 장치

- 슈퍼 렌즈

- 빛과 소리 필터링

- 기타 용도(태양광, 흡수체 등)

- 최종 사용자 업계별

- 항공우주 및 방위

- 통신

- 일렉트로닉스

- 헬스케어

- 기타 최종 사용자 업계(자동차 및 운송, 에너지 및 전력 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Acoustic Metamaterials Group Limited(AMG)

- Echodyne Corp.

- Evolv Technologies, Inc.

- Fractal Antenna Systems, Inc

- JEM Engineering

- Kymeta Corporation

- Meta Materials Inc.

- Metalenz, Inc.

- Metamagnetics

- Multiwave Technologies

- Nanohmics Inc.

- Nanoscribe GmbH and Co. KG

- NanoSonic, Inc.

- NKT Photonics A/S

- Pivotal Commware

- Teraview Limited

제7장 시장 기회와 향후 전망

KTH 25.11.25The Metamaterials Market size is estimated at USD 1.53 billion in 2025, and is expected to reach USD 5.21 billion by 2030, at a CAGR of 27.65% during the forecast period (2025-2030).

North America holds the leading 35.88% regional slice and is also the fastest-growing territory, propelled by a 28.92% CAGR through 2030. Demand pivots on 5G/6G roll-outs, defense stealth requirements, and energy-efficient devices. Electromagnetic metamaterials account for 44.19% of revenue thanks to their versatile role in antennas and frequency-selective surfaces. Antenna and radar systems already command 62.94% of spending, and aerospace and defense buyers contribute 54.19% of end-user demand. The competitive field remains fragmented as niche specialists commercialize proprietary designs. High fabrication costs and limited standardization still curb wider uptake, but rapid advances in additive manufacturing and nanofabrication are narrowing these constraints.

Global Metamaterials Market Trends and Insights

Expansion of 5G and 6G Network Plan: Metamaterials Enabling Next-Generation Connectivity

Metamaterial-based antennas are redefining millimeter-wave transmission by compressing beam-steering hardware into ultra-thin layers while sustaining multi-gigabit throughput. A digitally coded metasurface demonstrated at 60 GHz produced multiple simultaneous beams, a capability that mitigates urban signal blockage and underpins 6G reliability. Satellite links profit as well; 2D metasurfaces boost link budgets for non-terrestrial 5G/6G coverage. Commercial vendors have moved beyond lab prototypes, with hybrid satellite terminals integrating reconfigurable intelligent surfaces to secure uninterrupted connectivity for mobile platforms. This marriage of low-profile hardware and software-defined control positions the metamaterials market for sustained telecom spending as carriers densify high-band networks worldwide.

Advancements in Nanotechnology and Material Science: Precision Engineering at Atomic Scale

Federal programs request USD 2.2 billion for 2025 under the National Nanotechnology Initiative, lifting cumulative outlays above USD 45 billion and furnishing shared infrastructure for atomic-scale fabrication . Layer-by-layer additive methods now build graded index profiles that vary continuously across a surface, giving engineers a toolbox for tailoring phase, amplitude, and polarization locally. Such precision accelerates the insertion of metamaterials into structural health monitors, biomedical implants, and automotive radar housings. Early production trials using 3D-printed interlocking blocks to create frequency-selective absorbers reached 99.5% absorptivity while reducing tooling steps. These breakthroughs lower entry barriers and make volume output feasible for mainstream device makers over the medium term.

Lack of Awareness of Benefits of Metamaterials: Knowledge Gap Limiting Market Penetration

Complex wave-physics concepts deter decision-makers in sectors without dedicated R&D budgets. The U.S. National Science Foundation earmarked USD 386.67 million for advanced manufacturing workforce programs to bridge this gap with hands-on training . Demonstration projects that visualize gains in antenna miniaturization or noise attenuation are widening adoption, yet smaller firms in Latin America and parts of Southeast Asia still face steep learning curves.

Other drivers and restraints analyzed in the detailed report include:

- Growing Advancements in Quantum Computing and Photonics: Convergence Creating New Possibilities

- Increasing Demand from the Aerospace and Defense Industry: Strategic Applications Driving Adoption

- Cost of Synthesization of Metamaterials: Economic Barriers to Commercialization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electromagnetic variants accounted for 44.19% of 2024 revenue and are forecast to expand at 29.27% CAGR, reinforcing their role as the cornerstone of the metamaterials market. Their integration into frequency-selective panels, phased-array antennas, and negative-index lenses drives pervasive demand across telecom and defense. In value terms, this cohort represented USD 722.59 million of the metamaterials market size and is on track to cross USD 3.0 billion by 2030. The rise of terahertz detection, powered by graphene resonators with heightened biochemical sensitivity, amplifies future opportunities.

Emerging niches such as acoustic, hyperbolic, and negative-index formats broaden the functional palette. Acoustic structures dampen machinery vibration in industrial plants, supported by EU-funded METAVISION trials. Hyperbolic slabs channel sub-diffraction photons for super-resolution imaging, an asset in medical diagnostics. Hybrid stacks that fuse multiple classes unlock multi-modal control over sound, heat, and light within a single laminate. Research interest therefore accelerates diversification while reinforcing electromagnetic dominance at scale.

The Metamaterials Market Report Segments the Industry by Type (Electromagnetic, Terahertz, Tunable, Photonic, and More), Application (Antenna and Radar, Sensors, Cloaking Devices, Superlens, and More), End-User Industry (Healthcare, Telecommunication, and More), and Geography (Asia-Pacific, North America, Europe, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America translated a 35.88% stake and the highest regional CAGR of 28.92%. Federal investments of USD 386.67 million for advanced manufacturing and workforce programs reinforce a robust innovation ecosystem. Concentrated aerospace, defense, and telecom primes guarantee early-stage demand, enabling local suppliers to refine mass-production methods.

Asia-Pacific follows as industrialization and electronics capacity converge with sizable public funding. China's strategic technology plans channel resources into 6G and satellite networks, accelerating local adoption of metasurfaces for base-station and handset antennas. India's electronics output grew from INR 5.54 lakh crore (USD 76 billion) in FY 2020-21 to INR 9.52 lakh crore (USD 115 billion) in FY 2023-24 under the PLI scheme, providing fertile ground for semiconductor-grade metamaterial components. Japan and South Korea refine high-frequency radar absorbers for autonomous vehicles and smart factories.

Europe commands a sizeable share thanks to public-private programs targeting advanced materials under the UK Innovation Strategy and Germany's Industry 4.0 roadmap. Field trials in low-field MRI and industrial noise abatement testify to a thriving collaboration network. Policy frameworks emphasize open test beds and standardization, steering the metamaterials market toward cross-border scalability.

South America and the Middle East & Africa represent emerging frontiers, leveraging metamaterial-enhanced telecom backbones to leapfrog legacy infrastructure. Energy-harvesting metasurfaces that power remote sensor nodes align with regional off-grid electrification priorities, signaling untapped potential once cost barriers abate.

- Acoustic Metamaterials Group Limited (AMG)

- Echodyne Corp.

- Evolv Technologies, Inc.

- Fractal Antenna Systems, Inc

- JEM Engineering

- Kymeta Corporation

- Meta Materials Inc.

- Metalenz, Inc.

- Metamagnetics

- Multiwave Technologies

- Nanohmics Inc.

- Nanoscribe GmbH and Co. KG

- NanoSonic, Inc.

- NKT Photonics A/S

- Pivotal Commware

- Teraview Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of 5G and 6G Network Plan

- 4.2.2 Advancements in Nanotechnology and Material Science

- 4.2.3 Growing Advancements in Quantum Computing and Photonics

- 4.2.4 Increasing Demand from the Aerospace and Defense Industry

- 4.2.5 Growing Emphasis on Energy Efficiency and Sustainability

- 4.3 Market Restraints

- 4.3.1 Lack of Awareness of Benefits of Metamaterials

- 4.3.2 Cost of Synthesization of Metamaterials

- 4.3.3 Concerns of Material Durability and Standardization

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Patent Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Electromagnetic

- 5.1.2 Terahertz

- 5.1.3 Photonic

- 5.1.4 Tunable

- 5.1.5 Frequency Selective Surface (FSS)

- 5.1.6 Other Types(Acoustic, Negative-Index and Hyperbolic, Non-linear and Chiral)

- 5.2 By Application

- 5.2.1 Antenna and Radar

- 5.2.2 Sensors

- 5.2.3 Cloaking Devices

- 5.2.4 Superlens

- 5.2.5 Light and Sound Filtering

- 5.2.6 Other Applications (Solar, Absorbers, etc.)

- 5.3 By End-user Industry

- 5.3.1 Aerospace and Defense

- 5.3.2 Telecommunications

- 5.3.3 Electronics

- 5.3.4 Healthcare

- 5.3.5 Other End user Industries (Automotive and Transportation, Energy and Power, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Acoustic Metamaterials Group Limited (AMG)

- 6.4.2 Echodyne Corp.

- 6.4.3 Evolv Technologies, Inc.

- 6.4.4 Fractal Antenna Systems, Inc

- 6.4.5 JEM Engineering

- 6.4.6 Kymeta Corporation

- 6.4.7 Meta Materials Inc.

- 6.4.8 Metalenz, Inc.

- 6.4.9 Metamagnetics

- 6.4.10 Multiwave Technologies

- 6.4.11 Nanohmics Inc.

- 6.4.12 Nanoscribe GmbH and Co. KG

- 6.4.13 NanoSonic, Inc.

- 6.4.14 NKT Photonics A/S

- 6.4.15 Pivotal Commware

- 6.4.16 Teraview Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Use of Metamaterials in Solar Systems

- 7.3 Metamaterial-based Radars for Drones