|

시장보고서

상품코드

1852158

나노섬유 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Nanofiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

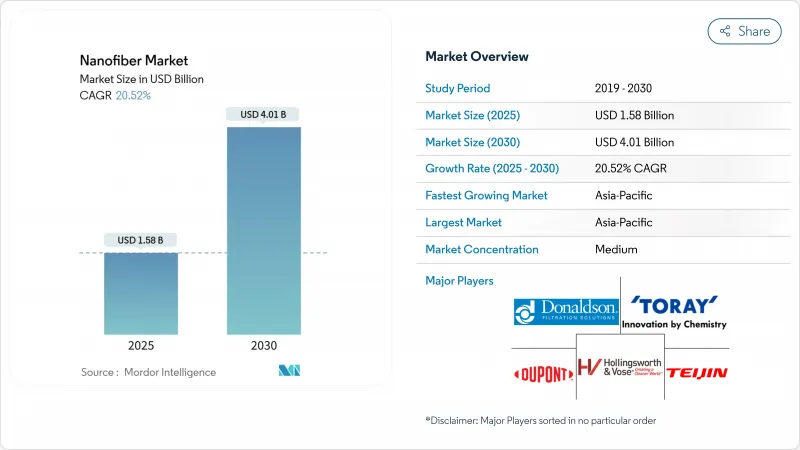

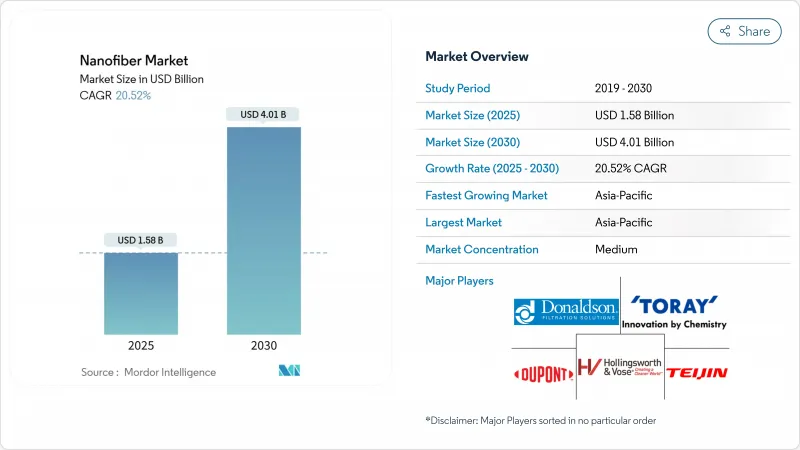

나노섬유 시장 규모는 2025년에 15억 8,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 20.52%로, 2030년에는 40억 1,000만 달러에 이를 것으로 예상됩니다.

의료, 여과, 에너지 저장, 첨단 섬유 응용 분야에서 높은 표면적 재료에 대한 수요 증가가 이러한 전망을 지원합니다. 아시아태평양은 38%의 매출로 선도하고 있으며, 강력한 제조 에코시스템으로부터 혜택을 받아 2030년까지 연평균 복합 성장률(CAGR) 22%를 나타낼 것으로 예상되며, 최대 및 급성장 지역 기반으로서의 이중 역할을 강화하고 있습니다. 폴리머 제품 카테고리는 2024년 매출의 42%를 차지하는 성숙한 전기 스피닝 생산 능력에 의해 지원되지만, 탄수화물 기반 등급은 보다 광범위한 지속가능성 변화를 반영하여 CAGR 27%의 성장 템포를 설정합니다. 도레이와 듀폰 등 세계적인 기존 기업들이 판매량에 있어서 리더십을 유지하는 한편, 나노 레이어 등의 혁신 기업은 독자적인 제조 기술을 도입하여 이익률이 높은 의료나 에너지의 틈새를 획득하고 있습니다. 폴리아크릴로니트릴(PAN) 원료의 가격 변동과 더불어, 탄소 나노섬유의 스케일 업 장애물은 여전히 높고, 당분간 공급 전망을 약화시키고 있습니다.

세계의 나노섬유 시장 동향과 인사이트

의료 및 제약 업계 수요 증가

나노섬유 기반 약물전달 플랫폼은 현재 85% 이상의 약물 충전과 96시간까지의 서방을 실현하여 치료 밀착성을 비약적으로 높여 전신 독성을 저하시키고 있습니다. 세포 외 매트릭스와 같은 구조는 우수한 세포 접착을 지원하고 치유 시간을 단축하고 흉터를 최소화하는 차세대 조직 비계를 가능하게합니다. 선진적인 상처 피복재를 채용하고 있는 병원에서는 환자 회전율의 향상이 의료비의 삭감으로 이어져 조달 의욕이 높아지고 있습니다. 정형외과 영역에서 나노섬유 스캐폴드에 대한 규제 경로가 밝혀지고 있으며, 개발자 시장 출시까지의 시간적 위험이 감소하고 있습니다. 이러한 의료적 돌파구를 종합하면 상환의 전망이 높아져 가치가 있는 헬스케어 채널에 대한 지속적인 수요가 강화됩니다.

EV 기가팩토리의 고 표면적 배터리 분리기 수요

일렉트로스팬 나노섬유 분리기는 치수를 손출시키지 않고 150℃의 온도 상승에 견딜 수 있어 EV의 중요한 안전 기준을 충족할 수 있게 되었습니다. 이온 전도성 향상으로 사이클 수명을 유지하면서 급속 충전 능력을 최대 40% 향출시켜 아시아와 미국의 기가팩토리에서 조달을 끌고 있습니다. 자동 롤 투 롤 라인의 생산량은 연간 300만㎡를 넘어 기존의 폴리올레핀 필름과의 비용 격차가 축소되고 있습니다. 선도적인 셀 제조업체에 의한 설비 도입은 다년간공급 계약을 고정화해 나노섬유 벤더에게 예측 가능한 수량의 가시성을 가져오고 있습니다. 중국과 미국의 국가적 깨끗한 이동성 혜택은 새로운 셀 케미스트리에서 분리기의 채택을 더욱 촉진하고 있습니다.

불안정한 PAN 원료 가격

PAN은 탄소나노파이버 전구체의 약 90%를 차지하며, 그 스팟 가격은 매년 최대 20% 변동하고, 다운스트림 공급자의 마진 안정성을 손출시키고 있습니다. 아크릴로 니트릴 사료 부족과 관련된 공급 중단은 재고 위험을 증가시키고 생산자는 지속가능성 신용을 높이면서 원료 비용을 kg 당 9 달러 이하로 줄일 수있는 석유 아스팔텐 또는 리그닌 대체품을 추구하도록 촉구합니다. 불순물 관리 및 기계적 성능 변동으로 인해 전환 기간이 장기화되고 PAN 변동성에 대한 노출이 장기화되고 있습니다. 구매자는 지수와 연계된 계약을 통해 헤지하고 있지만 장기적인 가격 전망이 여전히 제한되어 있기 때문에 적극적인 생산 능력 확대가 억제되고 있습니다.

부문 분석

폴리머 시스템은 확립된 일렉트로스피닝 라인과 포장, 여과, 바이오메디컬 기기 등 폭넓은 화학적 범용성으로 인해 2024년 매출의 42%를 차지했습니다. 탄수화물 기반 등급은 최종 사용자가 세계적인 순환형 경제(서큘러 이코노미) 지령에 따른 생분해성으로 생물 유래의 대체품을 추구하고 있기 때문에 수량은 적은 것, CAGR 27%로 가속하고 있습니다. 셀룰로오스 나노섬유는 아라미드에 필적하는 인장 강도를 가지면서 주위 조건 하에서 생분해되기 때문에 포장 공급업체는 단일 사용 용도로 채용되어야 합니다. 키틴 나노 화이버는 고유 항균 특성으로 상처 케어 제조업체를 매료시키고 조개 폐기물의 유가화 투자에 박차를 가하고 있습니다. 탄소나노파이버는 특수에너지와 일렉트로닉스용도에서 중요한 용도를 찾아내지만, 생산규모와 비용의 과제가 당면의 성장을 억제하고 있습니다.

탄수화물을 기반으로 한 제품의 기세는 화석 플라스틱의 사용을 줄이는 브랜드 소유자의 약속에 의해 증폭됩니다. EU의 일부 주에서는 일회용 합성 섬유를 금지하는 법이 제정되어 있으며, 이러한 움직임은 더욱 강해지고 있습니다. 고분자상과 세라믹상을 혼합한 복합 나노섬유는 고온 여과 틈새에서 중요한 역할을 합니다. 금속 및 금속 산화물 등급은 높은 전도성 및 광촉매 활성이 중요한 촉매 용도 및 감지 용도에 유용합니다. 세라믹 나노섬유는 항공우주 및 퍼니스 인테리어의 단열재로서 수요를 유지하고 있습니다. 원재료의 연구개발이 임업과 농업 폐기물의 흐름으로 이동함에 따라 비용 곡선은 수렴하고 보다 광범위한 나노섬유 시장을 강화할 것으로 예측됩니다.

지역 분석

아시아태평양은 2024년 매출의 38%를 차지하며 중국, 일본, 한국은 깊은 전자 공급망과 정부 지원 나노테크 이니셔티브의 혜택을 받았습니다. 중국에서는 EV의 생산 거점이 호조로 나노섬유 세퍼레이터 수요가 높아지고 있습니다. 지속가능한 소재를 대상으로 한 지역 활성화 펀드는 리그닌 유래 나노섬유 플랜트에 대한 투자 위험을 더욱 완화시킵니다. 이러한 에코시스템은 아시아태평양의 CAGR을 22%로 끌어올려 아시아태평양이 계속해서 세계의 수량 성장을 지지하고 있습니다.

북미는 의료, 방위, 에너지 분야에 보조금을 배분하는 2025년도 국가 나노기술 구상 예산 22억 달러를 가진 미국이 견인해 세계적인 수익 창출에 있어 중요한 역할을 하고 있습니다. 나노섬유 기반 재생 임플란트의 임출시험은 FDA의 고속 트랙 상태를 확보하고 상업화를 가속화하고 있습니다. 국방기관은 여과장치와 보호복의 연구개발을 후원하여 국내 공급망을 강화하고 있습니다. 캐나다의 클린 기술 우대 조치와 자동차 거점에의 근접성이 배터리 재료에 있어서 국경을 넘은 협력에 불을 붙인다.

독일과 프랑스의 엄격한 지속가능성 프레임워크가 견인하는 유럽은 생분해성 나노섬유 포장과 HVAC 솔루션으로 시장을 선도하고 있습니다. 호라이즌 유럽의 보조금은 스케일업과 표준화를 신속하게 진행하는 산학 클러스터를 육성하고 REACH 준수 가이드라인은 규제 확실성을 제공합니다. 성장률은 아시아태평양보다 뒤떨어지는 것, EU가 일부 일회용 플라스틱을 금지하는 지령을 내놓은 것으로, 외식 산업이나 퍼스널케어 제품에 대체의 기회가 태어나고 있습니다. 남미, 중동 및 아프리카에서는 식수 부족에 대한 대응과 농업 효율의 향상 프로그램이 견인역이 되고 있어, 해수 담수화와 방출 제어형 비료에의 나노섬유막의 조기 채용이 수익의 원동력이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 의료 및 제약 업계에서의 수요 증가

- EV 기가팩토리에서의 고표면적 배터리 세퍼레이터 수요

- 고효율 여과재 수요

- 자동차 산업의 성장

- 섬유 산업에서의 확대

- 시장 성장 억제요인

- 불안정한 PAN 원료 가격

- 카본 나노 화이버로의 이행의 어려움

- 건강과 안전에 대한 우려

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 기술 스냅샷

- 특허 분석

제5장 시장 규모와 성장 예측

- 제품 유형별

- 고분자 나노섬유

- 탄소 나노섬유

- 복합 나노섬유

- 금속 및 금속 산화물 나노섬유

- 세라믹 나노섬유

- 탄수화물 기반 나노섬유

- 용도별

- 물 및 공기 여과

- 의료

- 에너지 저장

- 자동차 및 운송

- 일렉트로닉스

- 섬유

- 기타 용도

- 제조 기술별

- 전기방사(니들 방식)

- 니들리스 전기방사

- 용액 블로우 방사

- 포스 스피닝/로터리 제트 방사

- 멜트 블로잉

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Applied Sciences Inc.

- Argonide Corporation

- Asahi Kasei Corporation

- Chuetsu Pulp & Paper Co. Ltd.

- Donaldson Company Inc.

- DuPont

- Esfil Tehno AS

- eSpin Technologies Inc.

- FibeRio Technology Corp.

- Hollingsworth & Vose

- IREMA-Filter GmbH

- Japan Vilene Company Ltd.

- NanoLayr Ltd

- Nanoval GmbH & Co. KG

- NIPPON PAPER INDUSTRIES CO., LTD.

- Pardam SRO

- Rengo Co., Ltd.

- Sappi Ltd.

- SNC Fiber

- Spur AS

- Teijin Limited

- Toray Industries Inc.

- US Global Nanospace Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.25The Nanofiber Market size is estimated at USD 1.58 billion in 2025, and is expected to reach USD 4.01 billion by 2030, at a CAGR of 20.52% during the forecast period (2025-2030).

Heightened demand for high-surface-area materials in medical, filtration, energy storage, and advanced textile applications anchors this outlook. Asia-Pacific, with an existing 38% revenue lead, benefits from strong manufacturing ecosystems and is expected to expand at 22% CAGR through 2030, reinforcing its dual role as both the largest and fastest-growing regional base. The polymeric product category holds 42% of 2024 revenue, supported by mature electrospinning capacity, while carbohydrate-based grades set the growth tempo at 27% CAGR, reflecting a wider sustainability shift. Global incumbents such as Toray Industries and DuPont maintain volume leadership while innovators like NanoLayr deploy proprietary manufacturing to capture high-margin medical and energy niches. Persistent scale-up hurdles for carbon nanofibers, coupled with price volatility in polyacrylonitrile (PAN) feedstock, temper the near-term supply outlook.

Global Nanofiber Market Trends and Insights

Increasing Demand from Medical and Pharmaceutical Industries

Nanofiber-based drug delivery platforms now achieve 85%-plus drug loading and sustained release for up to 96 hours, sharply improving therapeutic adherence and lowering systemic toxicity. Their extracellular-matrix-like architecture supports superior cell attachment, enabling next-generation tissue scaffolds that cut healing time and minimize scarring. Hospitals adopting advanced wound dressings cite patient-turnover gains that translate to reduced care costs, strengthening procurement appetite. Regulatory pathways for nanofiber scaffolds in orthopedics continue to clarify, lowering time-to-market risk for developers. Collectively, these medical breakthroughs elevate reimbursement prospects and reinforce recurring demand across high-value healthcare channels.

Demand for High-Surface-Area Battery Separators in EV Gigafactories

Electrospun nanofiber separators now withstand 150 °C thermal excursions without dimensional loss, addressing critical EV safety standards. Enhancements in ion conductivity are extending fast-charge capability by up to 40% while preserving cycle life, a gain attracting procurement from Asian and US gigafactories. Automated roll-to-roll lines scale output beyond 3 million m2 annually, narrowing cost gaps with conventional polyolefin films. Capital deployment by major cell producers is locking in multiyear supply contracts, providing predictable volume visibility for nanofiber vendors. National clean-mobility incentives in China and the United States further amplify separator adoption in new cell chemistries.

Volatile PAN Feedstock Prices

PAN constitutes about 90% of carbon nanofiber precursors, and its spot price fluctuates by up to 20% annually, eroding margin stability for downstream suppliers. Supply disruptions linked to acrylonitrile feed shortages intensify inventory risk, prompting producers to pursue petroleum-asphaltene or lignin alternatives that can cut raw-material cost below USD 9 per kg while raising sustainability credentials. Transition timeframes remain lengthy due to impurity management and variable mechanical performance, prolonging exposure to PAN volatility. Buyers hedge through index-linked contracts, but long-term pricing visibility is still limited, dampening aggressive capacity expansion.

Other drivers and restraints analyzed in the detailed report include:

- Demand for High-Efficiency Filtration Materials

- Growth in the Automotive Industry

- Difficulty in Shifting Carbon Nanofibers from Lab to Plant Scale

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The polymeric category anchors 42% of 2024 revenue, driven by well-established electrospinning lines and broad chemical versatility across packaging, filtration and biomedical devices. Carbohydrate-based grades, while smaller in volume, accelerate at a 27% CAGR as end-users pursue biodegradable, bio-sourced alternatives aligned with global circular-economy mandates. Cellulose nanofibers rival aramid tensile strength yet biodegrade under ambient conditions, compelling packaging suppliers to adopt them in single-use applications. Chitin nanofibers attract wound-care producers due to inherent antimicrobial traits, spurring investment in shellfish-waste valorization. Carbon nanofibers find significant use in specialty energy and electronics applications; however, production scale and cost challenges are restraining immediate growth.

Momentum for carbohydrate-based products is amplified by brand-owner commitments to cut fossil plastic use. Legislative bans on single-use synthetic fibers in several EU states compound this pull. Composite nanofibers, which blend polymer and ceramic phases, play a significant role in high-temperature filtration niches. Metal and metal-oxide grades serve catalytic and sensing applications where elevated conductivity or photocatalytic activity is critical. Ceramic nanofibers retain demand for thermal insulation in aerospace and furnace linings. As raw-material R&D migrates toward forestry and agricultural waste streams, cost curves are expected to converge, bolstering the broader nanofiber market.

The Nanofiber Market Report is Segmented by Product Type (Polymeric Nanofiber, Carbon Nanofiber, and More), Application (Water and Air Filtration, Medical, and More), Manufacturing Technology (Electrospinning (Needle-Based), Needle-Less Electrospinning, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commands 38% of 2024 revenue, with China, Japan and South Korea benefitting from deep electronic supply chains and government-backed nanotech initiatives. Robust EV production bases in China elevate local demand for nanofiber separators, while strict environmental guidelines accelerate uptake in air-filtration retrofits. Regional stimulus funds earmarked for sustainable materials further de-risk investment in lignin-derived nanofiber plants. This ecosystem underpins a 22% regional CAGR, ensuring Asia-Pacific continues to anchor global volume growth.

North America, driven by the U.S. with its USD 2.2 billion FY-25 National Nanotechnology Initiative budget, which allocates grants to medical, defense, and energy sectors, plays a significant role in global revenue generation. High-value healthcare projects dominate demand; clinical trials for nanofiber-based regenerative implants secure FDA fast-track status, accelerating commercialization. Defense agencies sponsor filtration and protective-wear R&D, fortifying domestic supply chains. Canada's clean-technology incentives and proximity to automotive hubs kindle cross-border collaboration in battery materials.

Europe, driven by Germany and France's stringent sustainability frameworks, leads in the market for biodegradable nanofiber packaging and HVAC solutions. Horizon Europe grants foster university-industry clusters that fast-track scale-up and standardization, while REACH compliance guidelines supply regulatory certainty. Although growth rates trail Asia-Pacific, EU directives banning select single-use plastics are opening replacement opportunities in food-service and personal-care products. In South America, the Middle East, and Africa, where programs addressing potable-water scarcity and enhancing agricultural efficiency are gaining traction, revenue is driven by the early adoption of nanofiber membranes in desalination and controlled-release fertilizers.

- Applied Sciences Inc.

- Argonide Corporation

- Asahi Kasei Corporation

- Chuetsu Pulp & Paper Co. Ltd.

- Donaldson Company Inc.

- DuPont

- Esfil Tehno AS

- eSpin Technologies Inc.

- FibeRio Technology Corp.

- Hollingsworth & Vose

- IREMA-Filter GmbH

- Japan Vilene Company Ltd.

- NanoLayr Ltd

- Nanoval GmbH & Co. KG

- NIPPON PAPER INDUSTRIES CO., LTD.

- Pardam SRO

- Rengo Co., Ltd.

- Sappi Ltd.

- SNC Fiber

- Spur AS

- Teijin Limited

- Toray Industries Inc.

- US Global Nanospace Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand from the Medical and Pharmaceutical Industries

- 4.2.2 Demand for High-Surface-Area Battery Separators in EV Gigafactories

- 4.2.3 Demand for High-Efficiency Filtration Materials

- 4.2.4 Growth in the Automotive Industry

- 4.2.5 Expansion in the Textile Industry

- 4.3 Market Restraints

- 4.3.1 Volatile PAN Feedstock Prices

- 4.3.2 Difficulty in Shift of Carbon Nanofibers from Lab Scale to Plant Scale due to Small Size and Complexity

- 4.3.3 Health and Safety Concerns

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Technology Snapshot

- 4.7 Patent Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Polymeric Nanofiber

- 5.1.2 Carbon Nanofiber

- 5.1.3 Composite Nanofiber

- 5.1.4 Metal and Metal Oxide Nanofiber

- 5.1.5 Ceramic Nanofiber

- 5.1.6 Carbohydrate-based Nanofiber

- 5.2 By Application

- 5.2.1 Water and Air Filtration

- 5.2.2 Medical

- 5.2.3 Energy Storage

- 5.2.4 Automotive and Transportation

- 5.2.5 Electronics

- 5.2.6 Textiles

- 5.2.7 Other Applications

- 5.3 By Manufacturing Technology

- 5.3.1 Electrospinning (Needle-Based)

- 5.3.2 Needle-less Electrospinning

- 5.3.3 Solution Blow Spinning

- 5.3.4 ForceSpinning/Rotary Jet Spinning

- 5.3.5 Melt Blowing

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-Level Overview, Market-Level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Applied Sciences Inc.

- 6.4.2 Argonide Corporation

- 6.4.3 Asahi Kasei Corporation

- 6.4.4 Chuetsu Pulp & Paper Co. Ltd.

- 6.4.5 Donaldson Company Inc.

- 6.4.6 DuPont

- 6.4.7 Esfil Tehno AS

- 6.4.8 eSpin Technologies Inc.

- 6.4.9 FibeRio Technology Corp.

- 6.4.10 Hollingsworth & Vose

- 6.4.11 IREMA-Filter GmbH

- 6.4.12 Japan Vilene Company Ltd.

- 6.4.13 NanoLayr Ltd

- 6.4.14 Nanoval GmbH & Co. KG

- 6.4.15 NIPPON PAPER INDUSTRIES CO., LTD.

- 6.4.16 Pardam SRO

- 6.4.17 Rengo Co., Ltd.

- 6.4.18 Sappi Ltd.

- 6.4.19 SNC Fiber

- 6.4.20 Spur AS

- 6.4.21 Teijin Limited

- 6.4.22 Toray Industries Inc.

- 6.4.23 US Global Nanospace Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Increasing R&D and High-potential Market for Cellulosic Nanofibers