|

시장보고서

상품코드

1910442

가죽 화학 제품 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Leather Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

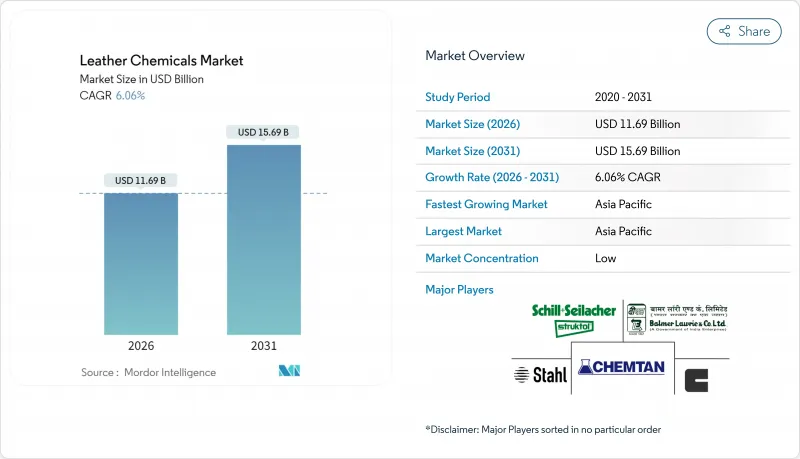

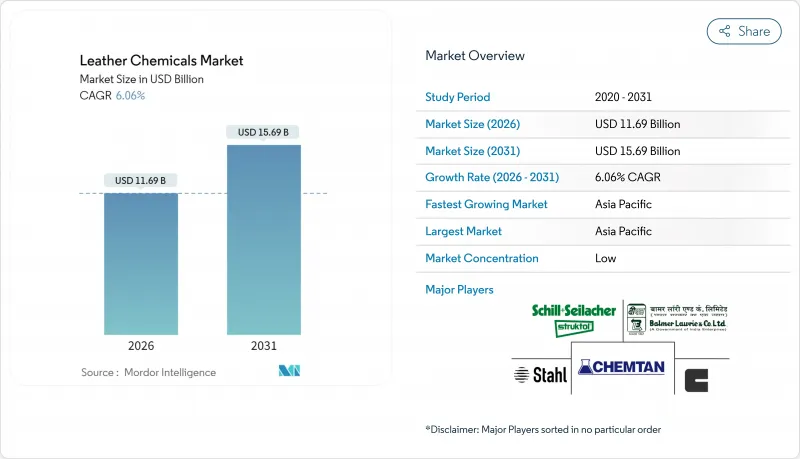

가죽 화학 제품 시장은 2025년의 110억 2,000만 달러에서 2026년에는 116억 9,000만 달러로 성장할 것으로 보입니다. 2026-2031년에 걸쳐 CAGR 6.06%로 성장할 것으로 예상되며, 2031년까지 156억 9,000만 달러에 달할 전망입니다.

상승 추세는 크롬 기반 태닝의 꾸준한 대체, 프리미엄 신발 및 자동차 내장재 수요 증가, 바이오 기반 보조제의 광범위한 채택에 의해 주도되고 있습니다. 크롬 프리 화학 기능은 이미 글로벌 수요를 주도하고 있으며, 마감 제형은 더욱 엄격해진 제품 성능 요구 사항 덕분에 주목을 받고 있습니다. 아시아태평양 지역은 생산량과 혁신 모두에서 선두를 달리고 있으며, 규모와 지속 가능성을 결합하려는 최근의 통합 노력에도 불구하고 경쟁 분야는 여전히 분산된 상태입니다.

세계의 가죽 화학 제품 시장 동향 및 인사이트

크롬 프리 및 금속 프리 태닝 기술의 급증

규제 기관들은 엄격한 크롬 허용 기준을 설정하며 제조업체들이 유기 및 무광물 태닝제로 전환하도록 촉진하고 있습니다. 캘리포니아주의 2023년 크롬 도금 ATCM(대체 기술 및 관리 규정)은 신규 6가 크롬 시설을 금지하고 장식용 크롬 도금을 단계적으로 폐지하여 크롬 프리 채택에 박차를 가하고 있습니다. 그루포 마스트로토(Gruppo Mastrotto)와 같은 생산자들은 생분해성 향상과 탄소 발자국 축소를 이유로 식물성 기반 방법에 투자하고 있습니다. 실험실 연구에 따르면 바이오매스 기반 제제는 크롬염보다 높은 분해율을 보여 폐기물 처리 문제를 완화합니다. 스탈(Stahl)의 그라노핀 이지 F-90 리큐어(Granofin Easy F-90 Liq)는 독자적인 배합으로 6가 크롬 잔류물을 제거하면서 물과 에너지를 절약하는 사례를 보여줍니다.

신발산업과 섬유산업의 급속한 성장

라리오하 지역 테스트에서 신발 내장재의 효과적인 미생물 살균률이 확인된 후 항균 성능은 이제 표준 기능이 되었다. 중국 본토는 연간 약 40억 평방피트의 가죽을 가공하여 가죽 화학 제품 시장 내 비엠하우스 및 마무리 화학 제품의 최대 단일 수요처로 자리매김했습니다. 섬유 부문은 혼합 소재 갑피에 유사한 마감제를 활용함으로써 두 번째 수요 흐름을 창출합니다. 브라질 공급망은 현지 자동차 가죽 수요 증가에 대응해 중국으로 더 많은 태닝 가죽을 수출하며 신속히 대응했습니다.

엄격한 6가 크롬 배출, 배수 기준

ECHA는 매년 생태계로 유입되는 6가 크롬 17톤을 차단할 계획으로, 제혁업체의 마진을 압박하는 규정 준수 투자를 요구하고 있습니다. 캘리포니아의 제65호 법안(Proposition 65)은 2025년 12월까지 100% 크롬 안전 인증 가죽을 의무화하여 브랜드들이 업스트림 공급망을 감사하도록 강제하고 있습니다. 독일 연방위험평가원(BfR) 보고서에 따르면 검사 대상 가죽 제품의 절반 이상이 REACH 기준인 3mg/kg을 초과하여 리콜 및 법적 위험을 초래했습니다. 전기화학적 산화 또는 펜튼 공정으로 폐수 처리 시설을 업그레이드하면 물 사용량을 대폭 절감할 수 있으나, 수백만 달러 규모의 자본 투자가 필요하다. 소규모 작업장은 이러한 비용을 감당하지 못하거나 크롬 프리 기술력을 확보하지 못할 경우 생존 위기에 직면할 수 있습니다.

부문 분석

마감 화학제품은 2026-2031년에 걸쳐 6.72%의 최고 연평균 성장률(CAGR)을 기록한 반면, 태닝 및 염색 화학 제품은 025년 기준 전체 시장의 44.78%를 유지했습니다. 제조업체들은 불소화 첨가물 없이도 내마모성과 항균 특성을 부여하는 다기능 탑코트를 채택하고 있습니다. Activated Silk L1은 생물 기반 폴리머가 용제 기반 래커를 대체하면서도 광택 지표를 충족시킬 수 있음을 보여줍니다.

태닝 부문은 식물성 및 합성 유기 시스템으로의 전환을 지속하며, 6가 크롬 배출 우려를 완화하고 라벨 인증 제도를 충족시키고 있습니다. 비엠하우스 세제는 낮은 pH에서도 세척 및 탈지 기능을 수행하는 효소 복합체로 진화하여 폐수 감축 목표와 부합합니다. 이에 마감 공급업체들은 프리미엄 마진을 확보하는 반면, 웻엔드 업체들은 공정 주기를 단축하는 턴키 방식의 친환경 레시피로 포트폴리오를 강화하고 있습니다.

가죽 화학 제품 보고서는 제품 유형(태닝 및 염색 화학 제품, 비엠하우스 화학제품, 마감 화학제품), 화학기능(크롬계, 크롬 프리 미네랄계, 합성 유기계), 최종사용자 산업(구두, 가구, 자동차, 섬유 및 패션, 기타 최종사용자 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류

지역별 분석

아시아태평양 지역은 2025년 매출의 48.37%를 차지했으며, 2026-2031년에 걸쳐 연평균 6.65%의 성장률을 보일 것으로 예상됩니다. 인도는 2023 회계연도에 52억 6천만 달러 상당의 가죽 제품을 수출했으며, 442만 명의 근로자를 고용하여 비엠하우스 보조제 및 마감용 수요를 확대하고 있습니다. 지역적 비용 우위, 통합된 공급망, 증가하는 내수 소비로 인해 아시아태평양 지역은 신규 생산 능력 확장의 중심지로 자리매김하고 있습니다. 일본 및 한국 구매자들은 물량은 적지만 고순도 합성탄닌 및 탑코트를 요구하며, ISO 14001 인증 공장과 VOC 무첨가 레시피를 보유한 공급업체를 선호합니다.

북미와 유럽은 성숙했으나 프리미엄 가격의 시장으로, 리터당 할인보다 규정 준수 지원이 더 중요하게 작용합니다. 유럽은 완제품 내 크롬 함량 기준을 3mg/kg 미만으로 강화하여 이탈리아, 스페인, 독일에서 크롬 프리 주문이 증가했습니다. 캘리포니아주는 2025년 중반까지 크롬 안전 기준 75% 준수를 의무화하여 업스트림 공급망 감사와 친환경 인증서 확보를 촉진하고 있습니다. 이러한 규제는 바이오 기반 합성물, 저안개성 가죽유지제, 단주기 재활용 시스템으로 지출을 유도합니다. 북미 자동차 트림 공장은 USMCA 인증 원자재를 요구하며 지역 혼합 스테이션을 제공하는 공급업체를 선호합니다. 두 지역은 지속 가능한 고성능 화학물질에 대한 수요를 함께 유지합니다.

남미는 전 세계에 원피를 공급하지만 현지 가공을 확대 중입니다. 환율 변동과 EU 추적성 규정이 비용 구조에 도전장을 내밀지만, 동시에 자동화 비엠하우스 라인 투자도 촉진합니다. 중동 제혁소는 특수 합성 탄닌제 생산을 위해 석유화학 원료를 활용하는 반면, 아프리카 신규 프로젝트들은 웻블루 수출에서 크러스트 또는 완제품 가죽으로 전환을 모색하며 종합 가공 솔루션의 고객 기반을 확대하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 크롬 프리 및 금속 프리 태닝 기술의 급증

- 신발, 섬유 산업의 급속한 성장

- 자동차 및 항공기용 내장재 수요 증가

- 생물 기반 유화제 및 합성 태닝제 선호도 상승

- 디지털 가죽 인쇄용 화학약품 수요 증가

- 시장 성장 억제요인

- 6가 크롬 배출량 및 폐수 처리에 관한 엄격한 규제

- 높은 에너지 및 폐수 처리 비용

- 합성 및 비건 가죽 화학 물질과의 경쟁

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 제품 유형별

- 태닝 및 염색용 화학약품

- 비엠하우스 화학 제품

- 마감 화학약품

- 화학적 기능별

- 크롬 기반

- 크롬 프리 미네랄

- 합성 유기

- 최종 사용자 업계별

- 신발

- 가구

- 자동차

- 섬유, 패션

- 기타 최종 사용자 산업(중공업 가죽 제품, 안장 등)

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- AMIT

- Balmer Lawrie & Co. Ltd.

- Buckman

- Chemtan Company, Inc.

- CLARIANT

- Dyna Glycols

- DyStar Singapore Pte Ltd.

- Fashion Chemicals GmbH & Co. KG

- Indofil Industries Limited.

- SCHILL SEILACHER GMBH

- Sisecam

- Stahl Holdings BV

- Syn-Bios SpA

- TEXAPEL SA

- TFL

- YILDIRIM Group Of Companies

- Zschimmer & Schwarz Chemie GmbH

제7장 시장 기회와 장래의 전망

HBR 26.02.04The Leather Chemicals Market is expected to grow from USD 11.02 billion in 2025 to USD 11.69 billion in 2026 and is forecast to reach USD 15.69 billion by 2031 at 6.06% CAGR over 2026-2031.

The uptrend is driven by the steady replacement of chromium-based tanning, increased demand from premium footwear and automotive interiors, and wider adoption of bio-based auxiliaries. Chrome-free chemical functions already dominate global demand, while finishing formulations are gaining traction thanks to stricter product-performance requirements. Asia-Pacific leads in both output and innovation, and the competitive field remains fragmented despite recent consolidation initiatives that seek to pair scale with sustainability.

Global Leather Chemicals Market Trends and Insights

Surge in Chrome-Free and Metal-Free Tanning Technologies

Regulators are setting strict chromium thresholds, spurring manufacturers to shift toward organic and mineral-free tanning agents. California's 2023 Chrome Plating ATCM bans new hexavalent chromium facilities and phases out decorative chrome plating, adding momentum to chrome-free adoption. Producers such as Gruppo Mastrotto have invested in vegetable-based methods, citing better biodegradability and shrinking carbon footprints. Laboratory studies confirm that biomass-based agents deliver higher degradation rates than chromium salts, easing end-of-life treatment challenges. Stahl's Granofin Easy F-90 Liq showcases how proprietary formulations save water and energy while eliminating Cr(VI) residues.

Rapid Growth of Footwear and Textile Industries

Antibacterial performance features are now routine after testing in La Rioja confirmed effective microbe kill rates for in-shoe compounds. Mainland China processes nearly 4 billion ft2 of hides per year, making it the largest single customer of beam-house and finishing chemicals in the leather chemicals market. The textile sector adds a second demand stream by utilizing similar finishing agents on mixed material uppers. Brazil's supply reacted quickly, exporting more tanned hides to China as local auto leather volumes escalated.

Strict Chromium VI Emission and Wastewater Norms

ECHA plans to stop 17 tonnes of Cr(VI) from entering ecosystems each year, imposing compliance investments that strain tanners' margins. California's Proposition 65 requires 100% certified chrome-safe leather by December 2025, forcing brands to audit upstream supply chains. The German Federal Institute for Risk Assessment reported that more than half of the tested leather items exceed the 3 mg/kg REACH limit, sparking recalls and legal exposure. Upgrading effluent plants with electrochemical oxidation or Fenton processes can slash water draw-off, but it involves multimillion-dollar capital outlay. Smaller workshops face existential risks if they cannot absorb these costs or secure chrome-free expertise.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Automotive and Aviation Upholstery

- Rising Preference for Bio-Based Fatliquors and Syntans

- Competition from Synthetic and Vegan Leather Chemistries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Finishing chemicals registered the highest 6.72% CAGR between 2026 and 2031, while tanning and dyeing agents retained 44.78% of the 2025 volume. Manufacturers adopt multifunctional topcoats that grant abrasion resistance and antimicrobial traits without fluorinated inputs. Activated Silk L1 demonstrates how bio-based polymers can replace solvent-driven lacquers while matching gloss metrics.

The tanning segment continues to pivot toward vegetable and synthetic organic systems, easing Cr(VI) discharge worries and satisfying label certification schemes. Beam-house detergents have moved toward enzyme complexes that clean and degrease at lower pH, aligning with wastewater reduction goals. Finishing suppliers thus capture premium margins, while wet-end players strengthen portfolios with turnkey eco-recipes that shorten process cycles.

The Leather Chemicals Report is Segmented by Product Type (Tanning and Dyeing Chemicals, Beam-House Chemicals, and Finishing Chemicals), Chemical Function (Chrome-Based, Chrome-Free Mineral, and Synthetic Organic), End-User Industry (Footwear, Furniture, Automotive, Textile and Fashion, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific controlled 48.37% of 2025 revenue and is forecast to grow at a 6.65% CAGR during 2026-2031. India exported USD 5.26 billion worth of leather goods in FY 2023 and employs 4.42 million workers, amplifying demand for beam-house auxiliaries and finishing agents. Regional cost advantages, integrated supply pools, and rising domestic consumption keep APAC at the epicenter of new capacity expansions. Japanese and South Korean buyers, though smaller in volume, demand high-purity syntans and topcoats, favoring suppliers with ISO 14001 plants and VOC-free recipes.

North America and Europe present mature but premium-priced outlets where compliance support often outweighs per-liter discounts. Europe tightened chromium limits to below 3 mg/kg in finished goods, driving chrome-free orders in Italy, Spain, and Germany. California prescribed 75% compliance to chrome-safe standards by mid-2025, adding urgency for upstream audits and green-tag certificates. These rules channel spending into bio-based synthetics, low-fogging fatliquors, and short-cycle recycling systems. North American auto trim plants require USMCA-proven content and favor suppliers offering regional blending stations. Together, the two regions sustain demand for sustainable high-performance chemicals.

South America supplies raw hides globally yet is increasing local finishing. Currency swings and EU traceability rules challenge cost structures but also encourage investments in automated beam-house lines. Middle Eastern tanneries leverage petrochemical feedstocks for specialty syntans, while new African projects look to shift from wet-blue exports to crust or finished leather, widening the client base for comprehensive processing solutions.

- AMIT

- Balmer Lawrie & Co. Ltd.

- Buckman

- Chemtan Company, Inc.

- CLARIANT

- Dyna Glycols

- DyStar Singapore Pte Ltd.

- Fashion Chemicals GmbH & Co. KG

- Indofil Industries Limited.

- SCHILL+SEILACHER GMBH

- Sisecam

- Stahl Holdings B.V.

- Syn-Bios S.p.A.

- TEXAPEL S.A.

- TFL

- YILDIRIM Group Of Companies

- Zschimmer & Schwarz Chemie GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Chrome-Free and Metal-Free Tanning Technologies

- 4.2.2 Rapid Growth of Footwear and Textile Industries

- 4.2.3 Increasing Demand for Automotive and Aviation Upholstery

- 4.2.4 Rising Preference for Bio-Based Fatliquors and Syntans

- 4.2.5 Digital Leather Printing Chemicals Gaining Traction

- 4.3 Market Restraints

- 4.3.1 Strict Chromium VI Emission and Wastewater Norms

- 4.3.2 High Energy and Wastewater-Treatment Cost

- 4.3.3 Competition From Synthetic and Vegan Leather Chemistries

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Tanning and Dyeing Chemicals

- 5.1.2 Beam-house Chemicals

- 5.1.3 Finishing Chemicals

- 5.2 By Chemical Function

- 5.2.1 Chrome-based

- 5.2.2 Chrome-free Mineral

- 5.2.3 Synthetic Organic

- 5.3 By End-user Industry

- 5.3.1 Footwear

- 5.3.2 Furniture

- 5.3.3 Automotive

- 5.3.4 Textile and Fashion

- 5.3.5 Other End-user Industries (Heavy Leather and Saddlery, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AMIT

- 6.4.2 Balmer Lawrie & Co. Ltd.

- 6.4.3 Buckman

- 6.4.4 Chemtan Company, Inc.

- 6.4.5 CLARIANT

- 6.4.6 Dyna Glycols

- 6.4.7 DyStar Singapore Pte Ltd.

- 6.4.8 Fashion Chemicals GmbH & Co. KG

- 6.4.9 Indofil Industries Limited.

- 6.4.10 SCHILL+SEILACHER GMBH

- 6.4.11 Sisecam

- 6.4.12 Stahl Holdings B.V.

- 6.4.13 Syn-Bios S.p.A.

- 6.4.14 TEXAPEL S.A.

- 6.4.15 TFL

- 6.4.16 YILDIRIM Group Of Companies

- 6.4.17 Zschimmer & Schwarz Chemie GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment