|

시장보고서

상품코드

1852176

이온 교환 수지 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Ion Exchange Resin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

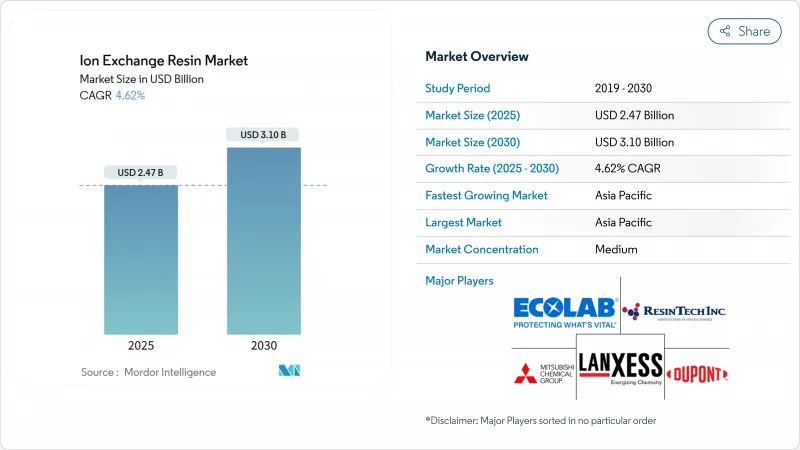

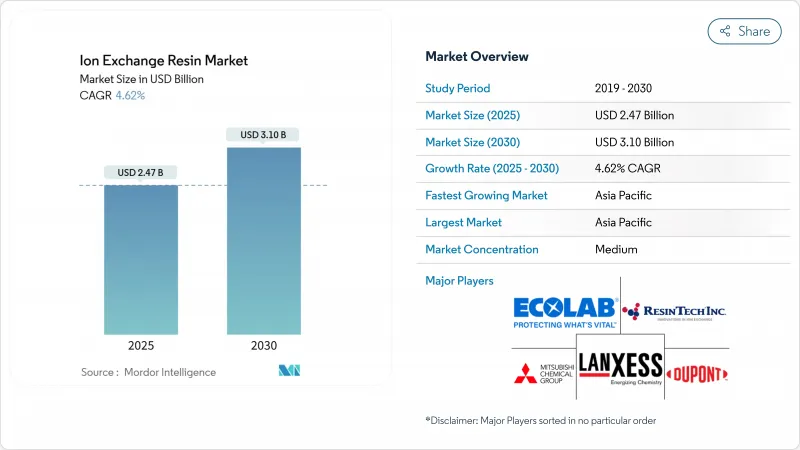

이온 교환 수지 시장 규모는 2025년에 24억 7,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 4.62%를 나타낼 것으로 예측되며, 2030년에 31억 달러에 달할 전망입니다.

수요 증가는 전 세계적으로 강화되는 수질 규제, 급속한 반도체 생산 능력 확대, 그리고 초순수 공정 스트림을 필요로 하는 제약 생산 확대에 기반을 두고 있습니다. 규제 복잡성 증가로 최종 사용자의 성능 기대치가 확대되면서, 공급업체들은 이온 선택성 범위가 좁고, 가동 주기가 길며, 재생 화학약품 수요가 낮은 수지를 제공해야 하는 압박을 받고 있습니다. 담수화, 산업 폐수, 자원 회수 프로젝트에서 무배출(ZLD) 시스템에 대한 자본 지출은 혼합층 및 킬레이트 등급에 대한 2차 수요를 창출하고 있습니다. 한편, 원자재 가격 변동(특히 스티렌 및 아크릴 단량체)은 수직 통합 조달로의 전환과 장기 조달 전략을 재편할 수 있는 바이오 기반 대체재 탐색을 촉진하고 있습니다. 이러한 요인들은 종합적으로 경쟁 강도를 높이고 있으며, 지역별 사양에 대응하기 위해 화학 대기업, 장비 통합업체, 지역 전문업체 간의 협력을 장려하고 있습니다.

세계의 이온 교환 수지 시장 동향 및 인사이트

아시아태평양 반도체 등급 초순수 수요

대만, 한국, 중국 본토의 칩 제조업체들은 3nm 미만의 노드 기하 구조를 추구하는 파운드리 업체들이 규정한 사양에 따라, 붕소와 미량 금속을 1조분의 1 단위로 제거하는 이온 교환 베드를 인증하고 있습니다. 이러한 수준의 연속적인 붕소 검출이 가능한 2025 Sievers Boron Ultra와 같은 분석기 도입으로 수지 교체 시점이 개선되고 화학 폐기물이 감소했습니다. 오가노 코퍼레이션은 이 독점 수요를 포착하기 위해 수지 용량 병목 현상 해소 등을 포함해 2024-2026년 초순수 자본 지출로 1,750억 엔을 배정했습니다. 반도체 수율 손실은 수백만 달러 규모의 기회 비용으로 직결되므로, 구매 결정 시 수지 가격 변동성보다 검증된 성능을 중시합니다. 결과적으로 이온 교환 수지 시장은 전반적인 제조업 침체기에도 반도체 구매의 탄력성 덕분에 혜택을 보며, 다른 분야의 경기 순환적 침체로부터 공급업체를 보호합니다.

PFAS와 중금속 배출규제가 북미의 킬레이트 수지를 뒷받침

2024년 미국 환경보호청(EPA) 잠정 지침은 대부분의 PFAS를 잔류성 유해 성분으로 분류하며, 음용수 취수구 기준 4 ng/L 미만의 제거 목표를 요구합니다. 이에 지방자치단체 및 산업 배출업체들은 단쇄 및 장쇄 PFAS에 특화된 수지를 적용한 이온교환 트레인 시범 운영에 나서고 있으며, 현장 연구 결과 단일 통과 공정에서 90% 이상의 제거 효율을 보고하고 있습니다. 란크세스(LANXESS)의 Lewatit MDS TP 108은 기존 거대공극 음이온 수지에 비해 돌파 주기를 2배 연장하여 처리 총비용을 낮추면서도 사용 후 매체의 폐기 제한을 준수합니다. PFAS 초과 시 규제 벌금이 급격히 증가함에 따라 유틸리티 업체들은 조달을 가속화하고 있으며, 이온 교환 수지 시장은 선택성과 긴 운영 수명을 위해 설계된 고마진 킬레이트 등급으로 전환되고 있습니다.

변동성 큰 스티렌 및 아크릴 단량체 가격

이온 교환 수지 제조업체들은 원자재 가격 변동성, 특히 스티렌 및 아크릴 단량체 가격 변동으로 인해 상당한 마진 압박에 직면해 있으며, 이는 가치 사슬 전반에 영향을 미치고 있습니다. 2024년 5월, 미국 환경보호청(EPA)이 합성 유기 화학 제조 산업에 대한 배출 기준을 개정함에 따라 단량체 생산 업체들의 준수 비용이 추가되어 가격 불안정성이 더욱 심화되었습니다. 중국 에버그린 신소재 기술(Evergreen New Material Technology)은 이온 교환 수지 원료를 포함한 정밀 화학 제품 생산에 14억 달러를 투자하여 수직 통합을 통해 공급망 위험을 완화할 계획입니다. 대형 수지 제조업체들은 규모의 경제와 장기 공급 계약을 활용해 변동성을 관리하는 반면, 중소 업체들은 마진 압박 또는 가격 인상으로 고객 이탈 위험에 직면하며 시장 통합이 가속화되고 있습니다.

부문 분석

2024년 글로벌 매출의 74%를 차지한 일반 등급 제품은 단위 비용과 검증된 재생 프로토콜을 우선시하는 지방자치단체의 수질 연화 및 보일러 탈염 수요가 확고히 자리 잡았음을 입증합니다. 이온 교환 수지 시장은 인도와 동남아시아 전역에서 진행 중인 수자원 인프라 확장에 힘입어 성장하고 있습니다. 공급업체들은 산화 안정성 가교제와 LewaPlus 같은 클라우드 기반 설계 도구를 통합하여 수명을 연장하고 있습니다. 이를 통해 유틸리티 업체들은 컬럼 재고를 적정 규모로 조정하고 염 사용량을 절감할 수 있습니다. 규모에도 불구하고, 일반 수지들은 스티렌 가격 급등 시 마진 압박에 직면하여, 검증된 탄소 배출 감축으로 소폭의 가격 프리미엄을 정당화하는 ISCC PLUS 같은 친환경 인증 획득을 모색하게 됩니다.

특수 수지는 시장 점유율은 낮지만, 높은 선택성, 낮은 추출물 함량, 생물학적 제제와의 호환성을 요구하는 응용 분야로 인해 2030년까지 연평균 5.3% 성장률로 전체 이온 교환 수지 시장 성장률을 앞지를 전망입니다. 듀폰이 2025년 출시한 AmberChrom TQ1은 연속 공정 중 올리고뉴클레오티드 결합 용량을 두 배로 늘리면서 컬럼 압력 손실을 절반으로 줄여 이 추세를 입증합니다. 프리미엄 바이오제약 및 마이크로전자공학 사용자들은 수지 안정성이 가동 중단 시간을 줄이고, 규제 준수를 보장하며, 배치 수율을 보호할 경우 일반 수지보다 3-5배 높은 가격대를 수용합니다. 규제 감독이 나노그램/리터 수준의 오염물질까지 확대됨에 따라 분자 각인 수지 및 거대공질 킬레이트 수지에 대한 수요가 가속화되어 광범위한 이온 교환 수지 시장 내 수익 구성 다각화가 이루어질 것입니다.

지역 분석

아시아태평양 지역은 2024년 매출의 36%를 차지하며 가장 높은 5.4% CAGR(연평균 성장률)을 기록할 것으로 예상됩니다. 이는 국가 차원의 첨단 폐수 처리 의무와 함께 급속한 산업화를 반영한 것입니다. 중국의 에버그린 뉴 머티리얼(Evergreen New Material)은 지역 수지 생산자들의 원료 공급 안정성을 확보하기 위해 설계된 스티렌 복합체에 14억 달러를 투자하고 있으며, 이는 이온 교환 수지 시장을 태평양 횡단 물류 차질로부터 보호하는 공급망 현지화를 보여줍니다. 대만과 한국의 반도체 파운드리 업체들은 새로운 초순수 시스템 도입을 지속하며, 오가노(Organo)와 퓨로라이트(Purolite)가 해당 지역 내 생산 기반을 확장해 납기 단축과 원산지 조달 규정 준수를 추진하도록 하고 있습니다. 인도의 로하(Roha) 신규 공장 가동으로 2027년까지 국내 생산 능력이 두 배로 증가할 전망이며, 이는 현지 조달 요건이 글로벌 흐름을 재편하고 있음을 보여줍니다.

북미는 성숙하면서도 혁신 주도형 환경으로, 환경 규정 준수 및 제약 생산이 수지 사양을 결정합니다. 매사추세츠, 노스캐롤라이나, 퀘벡의 바이오제약 클러스터는 크로마토그래피 매트릭스에 대한 지속적인 수요를 창출하고 있으며, 듀폰의 2025년 북미 AmberChrom TQ1 출시로 이 추세가 강화될 전망입니다. 일반 수지 물량은 정체될 수 있으나, 검증된 성능에 대한 지불 의사가 확고한 이 지역의 입지는 글로벌 이온 교환 수지 시장 내 중요성을 공고히 합니다.

유럽은 여전히 규제 중심적이며, 화학물질 제한 조치와 녹색 수소 인센티브를 균형 있게 적용해 멤브레인 등급 PFSA 수요를 높이고 있습니다. EU의 사용 후 수지 매립 제한은 서비스 수명을 20-30% 연장할 수 있는 첨단 재생 프로토콜 연구 개발을 촉진하고 있으며, 이는 통합 솔루션 제공업체의 서비스 계약 수익을 증가시키고 있습니다. 도시 폐수 처리 지침의 지속적인 시행과 맞물려, 유럽은 상대적으로 소규모의 물량 점유율에도 불구하고 이온 교환 수지 시장에 대해 꾸준하고 가치 중심의 영향력을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아태평양의 반도체 등급 초순수 수요

- PFAS와 중금속 배출 규제가 북미의 킬레이트 수지를 밀어 올린다

- 중동의 담수화 및 ZLD 프로젝트로 인한 혼합층 수지 채택 증가

- 유럽 수소 전기분해기 인센티브로 인한 PFSA 이온 교환막 수요 증가

- 라틴아메리카 설탕 탈색 붐으로 인한 식품 등급 수지 수요 증가

- 시장 성장 억제요인

- 변동성 있는 스티렌 및 아크릴 단량체 가격

- 생물 기반 흡착제가 수지 경제성을 저해

- EU에서 사용한 수지의 매립 규제

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 업계 간 경쟁

제5장 시장 규모와 성장 예측

- 유형별

- 일반 수지

- 특수 수지

- 최종 이용 산업별

- 수처리

- 전력

- 식품 및 음료

- 의약품

- 화학처리

- 광업 및 야금

- 기타 최종 사용자 산업

- 용도 기능별

- 연화 및 탈염

- 초순수 제조

- 중금속 제거 및 PFAS 완화

- 촉매 및 분리(비수)

- 설탕의 탈색과 식품 및 음료 정제

- 귀금속 회수와 습식 야금

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Anhui Sanxing Resin Co., Ltd.

- Bio-Rad Laboratories, Inc.

- DOSHION POLYSCIENCE PVT. LTD.

- DuPont

- Ecolab

- Eichrom Technologies, LLC

- IEI

- JACOBI CARBONS GROUP

- LANXESS

- Mitsubishi Chemical Group Corporation

- Polymex

- Pure Resin Co., Ltd.

- ResinTech, Inc.

- Samyang Corporation

- Sunresin New Materials Co.Ltd.

- Suqing Group

- Suzhou bojie resin technology Co.,Ltd

- Thermax Limited

- Xylem

제7장 시장 기회와 장래의 전망

HBR 25.11.27The Ion Exchange Resin Market size is estimated at USD 2.47 billion in 2025, and is expected to reach USD 3.10 billion by 2030, at a CAGR of 4.62% during the forecast period (2025-2030).

Demand growth is anchored in tightening global water-quality rules, rapid semiconductor capacity additions, and expanding pharmaceutical production that all require ultrapure process streams. Regulatory complexity is expanding the performance envelope that end users expect, pushing suppliers to deliver resins with narrower ionic selectivity windows, longer operating cycles, and lower regeneration chemical demand. Capital spending on zero-liquid-discharge (ZLD) systems in desalination, industrial wastewater, and resource-recovery projects is creating secondary pull for mixed-bed and chelating grades. Meanwhile, raw-material cost swings-especially for styrene and acrylic monomers-are catalyzing a shift toward vertically integrated sourcing and the exploration of bio-based alternatives that could reshape long-term procurement strategies. Collectively, these drivers are keeping competitive intensity high and encouraging partnerships between chemical majors, equipment integrators, and regional specialists to keep pace with localized specifications.

Global Ion Exchange Resin Market Trends and Insights

Semiconductor-grade Ultrapure Water Demand in Asia Pacific

Chip-fabs in Taiwan, South Korea, and Mainland China are qualifying ion-exchange beds that remove boron and trace metals to single-digit parts-per-trillion, a specification codified by foundries chasing sub-3 nm node geometries. The adoption of analyzers such as the 2025 Sievers Boron Ultra, which allows continuous boron detection at those levels, has improved resin change-out timing and reduced chemical waste. Organo Corporation has earmarked JPY 175 billion in ultrapure-water capital outlays for 2024-2026, including resin capacity debottlenecking to capture this captive demand. Because semiconductor yield losses translate directly into multi-million-dollar opportunity costs, purchasing decisions emphasize proven performance over resin price volatility. Consequently, the ion exchange resin market benefits from resilient semiconductor procurement even during broader manufacturing slowdowns, insulating suppliers from cyclical downturns elsewhere.

PFAS and Heavy-Metal Discharge Limits Boosting Chelating Resins in North America

The 2024 U.S. EPA interim guidance classifies most PFAS as persistent hazardous constituents, requiring removal targets below 4 ng/L for drinking-water intakes. Municipalities and industrial dischargers have responded by piloting ion-exchange trains featuring resins tailored for short- and long-chain PFAS, with field studies reporting more than 90% removal efficiencies in single-pass operation. LANXESS's Lewatit MDS TP 108 extends breakthrough cycles two-fold compared with conventional macroporous anion resins, lowering total cost of treatment while complying with disposal restrictions on spent media. Because regulatory penalties escalate rapidly for PFAS exceedances, utilities are accelerating procurement, pushing the ion exchange resin market toward higher-margin chelating grades engineered for selectivity and longer operational life.

Volatile Styrene and Acrylic Monomer Prices

Ion exchange resin manufacturers face significant margin pressures due to raw material price volatility, particularly styrene and acrylic monomers, impacting the value chain. In May 2024, the Environmental Protection Agency's amended emission standards for the Synthetic Organic Chemical Manufacturing Industry added compliance costs for monomer producers, further destabilizing prices. China's Evergreen New Material Technology's USD 1.4 billion investment in fine chemicals production, including ion exchange resin raw materials, aims to mitigate supply chain risks through vertical integration. Larger resin manufacturers leverage economies of scale and long-term supply agreements to manage volatility, while smaller players face margin compression or price hikes, risking customer loss and accelerating market consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Desalination and ZLD Projects in the Middle East Elevating Mixed-Bed Resin Uptake

- Europe Hydrogen Electrolyzer Incentives Lifting PFSA Ion-Exchange Membranes

- Bio-based Adsorbents Undercutting Resin Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commodity grades anchored 74% of global revenue in 2024, a testament to entrenched municipal water-softening and boiler-demineralization demand that prioritize unit cost and proven regeneration protocols. The ion exchange resin market is driven by ongoing water-infrastructure buildouts across India and Southeast Asia. Suppliers are stretching lifetimes by integrating oxidative-stable cross-linkers and cloud-based design tools such as LewaPlus, which let utilities right-size column inventories and cut salt usage. Despite their scale, commodity resins face margin compression when styrene prices spike, compelling producers to seek green certifications, such as ISCC PLUS, that justify modest price premiums with verified carbon-emission reductions.

Specialty resins, though accounting for a smaller base, will outpace overall ion exchange resin market growth at 5.3% CAGR through 2030 as applications demand higher selectivity, lower extractables, and compatibility with biologics. The 2025 release of AmberChrom TQ1 by DuPont underscores this trend, doubling oligonucleotide binding capacity while halving column pressure losses during continuous processing. Premium bio-pharma and microelectronics users accept price points 3-5 times those of commodity beads when resin stability reduces downtime, ensures regulatory compliance, and shields batch yields. As regulatory scrutiny widens to nanogram-per-liter contaminants, demand for molecularly imprinted and macroporous chelating grades will accelerate, diversifying the revenue mix within the broader ion exchange resin market.

The Ion Exchange Resins Market Report Segments the Industry by Type (Commodity Resins and Specialty Resins), End-Use Industry (Water Treatment, Power, Pharmaceutical, and More), Application Function (Softening and Demineralization, Ultrapure Water Production, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific dominates with 36% 2024 revenue and the highest forecast 5.4% CAGR, reflecting rapid industrialization alongside national mandates for advanced wastewater treatment. China's Evergreen New Material is channeling USD 1.4 billion into a styrenics complex designed to lock in feedstock security for regional resin producers, demonstrating supply-chain localization that shields the ion exchange resin market from trans-Pacific logistic disruptions. Taiwanese and South Korean chip foundries continue to commission new ultrapure-water systems, compelling Organo and Purolite to expand manufacturing footprints in the region to shorten lead times and comply with country-of-origin procurement rules. India's upcoming Roha greenfield plant will double domestic capacity by 2027, underscoring how local content requirements are reshaping global flow patterns.

North America presents a mature yet innovation-led environment where environmental compliance and pharmaceutical production shape resin specifications. Biopharma clustering in Massachusetts, North Carolina, and Quebec is driving sustained demand for chromatography matrices, a trend reinforced by DuPont's 2025 North America launch of AmberChrom TQ1. While commodity resin volumes may plateau, the region's willingness to pay for validated performance cements its relevance within the global ion exchange resin market.

Europe remains regulation-centric, balancing chemical-restriction measures with green-hydrogen incentives that elevate membrane-grade PFSA demand. EU landfill constraints on spent resins are fueling research and development on advanced regeneration protocols capable of extending service life by 20-30%, thereby lifting service-contract revenue for integrated solution providers. Coupled with ongoing enforcement of the Urban Wastewater Treatment Directive, Europe maintains steady, value-weighted influence over the ion exchange resin market despite its comparatively modest volume share.

- Anhui Sanxing Resin Co., Ltd.

- Bio-Rad Laboratories, Inc.

- DOSHION POLYSCIENCE PVT. LTD.

- DuPont

- Ecolab

- Eichrom Technologies, LLC

- IEI

- JACOBI CARBONS GROUP

- LANXESS

- Mitsubishi Chemical Group Corporation

- Polymex

- Pure Resin Co., Ltd.

- ResinTech, Inc.

- Samyang Corporation

- Sunresin New Materials Co.Ltd.

- Suqing Group

- Suzhou bojie resin technology Co.,Ltd

- Thermax Limited

- Xylem

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Semiconductor-grade Ultrapure Water Demand in Asia Pacific

- 4.2.2 PFAS and Heavy-Metal Discharge Limits Boosting Chelating Resins in North America

- 4.2.3 Desalination and ZLD Projects in Middle East Elevating Mixed-Bed Resin Uptake

- 4.2.4 Europe Hydrogen Electrolyzer Incentives Lifting PFSA Ion-Exchange Membranes

- 4.2.5 LATAM Sugar-Decolorization Boom Raising Food-Grade Resins Demand

- 4.3 Market Restraints

- 4.3.1 Volatile Styrene and Acrylic Monomer Prices

- 4.3.2 Bio-based Adsorbents Undercutting Resin Economics

- 4.3.3 EU Land-fill Restrictions on Spent Resins

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Commodity Resins

- 5.1.2 Specialty Resins

- 5.2 By End-Use Industry

- 5.2.1 Water Treatment

- 5.2.2 Power

- 5.2.3 Food and Beverage

- 5.2.4 Pharmaceutical

- 5.2.5 Chemical Processing

- 5.2.6 Mining and Metallurgy

- 5.2.7 Other End-user Industries

- 5.3 By Application Function

- 5.3.1 Softening and Demineralization

- 5.3.2 Ultrapure Water Production

- 5.3.3 Heavy-Metal Removal and PFAS Mitigation

- 5.3.4 Catalysis and Separation (Non-Water)

- 5.3.5 Sugar Decolorization and Food and Beverage Purification

- 5.3.6 Precious-Metal Recovery and Hydrometallurgy

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Anhui Sanxing Resin Co., Ltd.

- 6.4.2 Bio-Rad Laboratories, Inc.

- 6.4.3 DOSHION POLYSCIENCE PVT. LTD.

- 6.4.4 DuPont

- 6.4.5 Ecolab

- 6.4.6 Eichrom Technologies, LLC

- 6.4.7 IEI

- 6.4.8 JACOBI CARBONS GROUP

- 6.4.9 LANXESS

- 6.4.10 Mitsubishi Chemical Group Corporation

- 6.4.11 Polymex

- 6.4.12 Pure Resin Co., Ltd.

- 6.4.13 ResinTech, Inc.

- 6.4.14 Samyang Corporation

- 6.4.15 Sunresin New Materials Co.Ltd.

- 6.4.16 Suqing Group

- 6.4.17 Suzhou bojie resin technology Co.,Ltd

- 6.4.18 Thermax Limited

- 6.4.19 Xylem

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growing Demand For Fuel Cells