|

시장보고서

상품코드

1852186

바이러스 여과 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Virus Filtration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

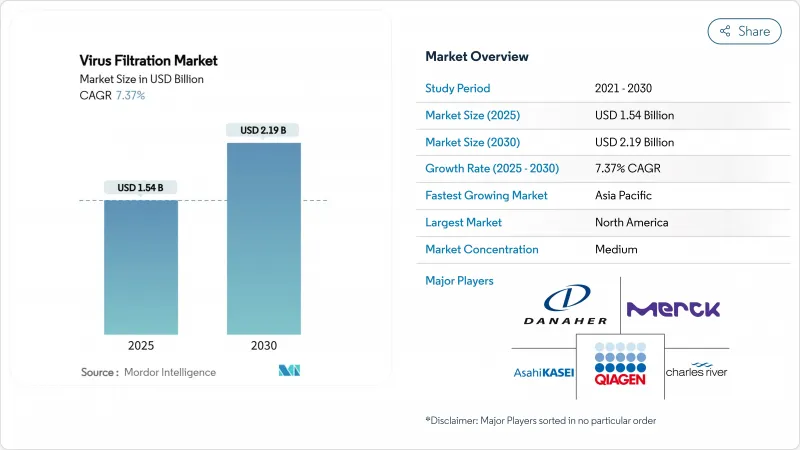

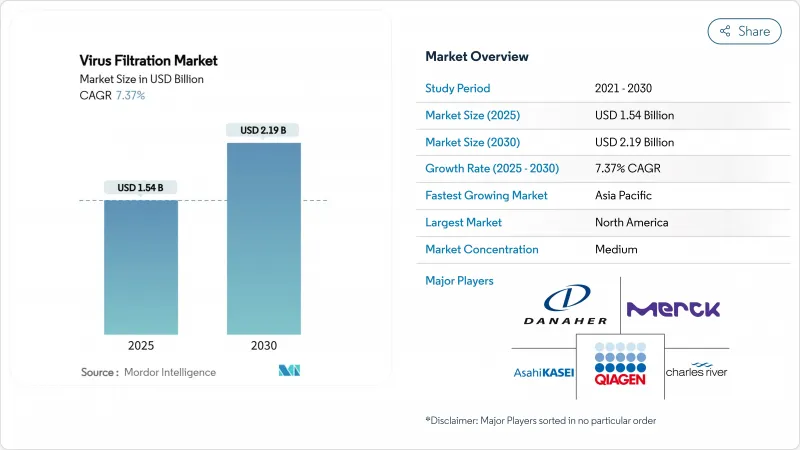

바이러스 여과 시장 규모는 2025년에 15억 4,000만 달러로 평가되었고, 2030년에 21억 9,000만 달러에 이를 것으로 예측되며, CAGR은 7.37%를 나타낼 전망입니다.

바이러스 안전성에 대한 규제 강화, 급속히 증가하는 생물학적 제제 파이프라인, 일회용 시스템의 광범위한 채택, 연속 생물공정 처리로의 전환이 바이러스 여과 시장을 주도하는 주요 동력입니다. 공급업체들은 멤브레인 소재 업그레이드, 자동화 통합, 밸리데이션 주기 단축을 위한 인라인 분석 기술 내장 등으로 대응하고 있습니다. mRNA 백신 및 유전자 치료에 대한 투자 확대는 북미, 유럽, 특히 아시아태평양 지역에서 강력한 클리어런스 기술에 대한 수요를 지속적으로 증폭시키고 있습니다. 한편, 주요 업체들 간의 전략적 인수는 업계가 엔드투엔드 포트폴리오 확대, 공급망 회복탄력성 강화, 차세대 필터 성능 향상에 주력하고 있음을 보여줍니다.

세계의 바이러스 여과 시장 동향 및 인사이트

생물학적 제제 및 유전자 치료에 대한 수요 증가

T세포 치료제 부문만 해도 2025년 103억 달러에서 2034년 1,612억 1천만 달러로 급증할 것으로 예상되며, 이는 구조적 손실 없이 정제되어야 하는 바이러스 벡터의 전례 없는 양을 유발합니다. 700개 이상의 활성 AAV 프로그램은 점점 더 높은 역가에서도 캡시드 무결성을 유지할 수 있는 필터를 필요로 합니다. 렌티바이러스 생산은 더욱 심각한 오염 문제를 겪고 있어, 허용 가능한 회수율을 위해 저흡착성 멤브레인이 필수적입니다. 이에 업계 참여자들은 필터 후보를 사전 선별하고 광범위한 습식 실험실 반복 작업을 줄이기 위해 예측 모델링 도구에 투자하고 있습니다. 이러한 생물학적 제제의 급증은 차세대 치료제 개발에서 바이러스 여과 시장의 핵심적 중요성을 강조합니다.

일회용 여과 기술 채택

계약 개발 및 제조 기관(CDMO)은 캠페인 유연성과 세척 밸리데이션 오버헤드 감소를 위해 일회용 어셈블리를 선호합니다. 고처리량 마이크로캐리어 배양은 이제 다중 장벽 제거 등급의 일회용 바이러스 필터와 결합할 수 있습니다. 2024년 출시된 아사히 가세이(Asahi Kasei)의 플라노바 FG1(Planova FG1)은 기존 홀더와의 호환성을 유지하면서 전작 대비 7배 빠른 유량을 달성합니다. 자동 압력 모니터링 및 무결성 테스트 소켓이 표준으로 제공되어 사용 전 멸균 후 테스트에 대한 부속서 1 요구사항을 충족합니다.

엄격한 밸리데이션 및 규제 승인 일정

FDA 개정 Q5A(R2) 지침은 심화된 바이러스 패널 테스트를 명시하고 새로운 검출 기술을 권장하여 기업들이 밸리데이션 프로토콜과 기록 보관을 업데이트하도록 요구합니다. Cygnus Technologies의 MockV 키트는 비감염성 대용물을 활용한 초기 제거 예측을 지원하지만, 허가를 위해서는 여전히 본격적인 스파이크 연구가 필수입니다. 따라서 개발사는 다단계 파일럿 작업, 통계적 견고성 평가, 규제 기관 협의 세션에 대한 예산을 편성해야 하며, 이는 시장 출시 기간을 연장시킵니다.

부문 분석

2024년 바이러스 여과 시장 규모에서 키트, 시약 및 소모품이 58.43%를 차지했으며, 이는 모든 생산 공정에서 반복적으로 사용됨을 입증합니다. 일회용 어셈블리로의 전환으로 수요가 확대되고 있으며, 각 로트마다 새로운 캡슐, 무결성 테스트 시약 및 프리필터가 필요합니다. 생물학적 제제의 역가 증가로 오염이 심화되어 카트리지 교체율이 높아지고 소모품 매출이 증가하고 있습니다. 반면 시스템 매출은 일회성이지만 차세대 스키드에 데이터 히스토리안, 자동 플러싱 기능, 디지털 트윈 호환성이 통합되면서 급속히 증가하고 있습니다. PFAS 무함유 폴리아미드 복합재와 같은 막 혁신은 흡착 손실에 취약한 유전자 치료 벡터를 겨냥한 프리미엄 모델을 더욱 차별화합니다.

여과 시스템은 2030년까지 연평균 9.65% 성장률로 해당 부문을 주도하고 있습니다. 공급업체들은 전단력을 최소화하고 바이러스 벡터 감염력을 유지하는 평면 유로 설계를 강조합니다. 아사히 가세이의 FG1 출시가 이를 대표적으로 보여주며, 동등한 로그 감소 값에서 7배 높은 처리량을 제공합니다. 하드웨어 모듈화는 스테인리스 하우징과 일회용 캡슐 간 간편한 교체를 가능케 하여 다양한 고객 파이프라인을 관리하는 CDMO의 관심을 끌고 있습니다. 여과 가능성 스크리닝부터 종단 간 밸리데이션 문서화에 이르는 자문 서비스가 번들로 제공되면서 장비 중심 공급업체에게도 정기 수익원이 창출되고 있습니다.

기존 스테인리스 시설이 전면적 재설계보다 밸리데이션된 방법 확장을 선택함에 따라 2024년 바이러스 여과 시장 점유율의 55.43%를 배치 여과가 유지했습니다. 운영자들은 배치 공정이 보유한 방대한 역사적 데이터를 높이 평가하여 규제 당국과의 협의 및 승인 후 변경 관리를 용이하게 합니다. 또한 일회용 필터는 기존 배치 저장 탱크에 쉽게 개조 적용되어 시설 전체 개조 없이도 증설이 가능합니다. 그러나 고유한 시작-정지 특성으로 인한 노동력 집중과 제품 보관 시간은 총설비효율성(TEE)을 저해합니다.

연속 여과와 인라인 여과는 관류 세포 배양으로의 광범위한 전환을 활용하며 9.88%의 연평균 성장률(CAGR)로 발전 중입니다. 2,000L 상업 규모에서 안정 상태 여과액 흐름은 이미 글로벌 약전 무균 기준을 충족시키면서 완충액 소비량을 절반으로 줄입니다. 병렬 필터 어레이는 유량 감소를 완화하고, 센서가 오염 징후를 감지하면 스마트 밸브가 유량을 전환하여 처리량 중단 없이 제품 무결성을 보호합니다. 규제 기관은 통합 실시간 분석을 통해 연속 플랫폼이 자연스럽게 지원하는 종합적 제어 전략 제출을 점점 더 권장하고 있습니다.

지역 분석

북미는 2024년 전 세계 매출의 43.23%를 차지했으며, 이는 미국의 방대한 생물학적 제제 연구개발(R&D) 파이프라인과 바이러스 안전성 기준 설정에서 FDA의 역할에 기인합니다. 후지필름 디오신스의 노스캐롤라이나주 12억 달러 규모 세포 배양 시설 확장 등 주요 생산 능력 투자는 국내 인프라에 대한 지속적인 신뢰를 시사합니다. 성숙한 공급망은 무균 캡슐 및 밸리데이션 바이러스 접근성을 용이하게 하여 현지 공장의 시장 출시 시간 우위를 제공합니다. mRNA 및 유전자 치료 후보물질이 후기 단계로 진입함에 따라 필터 공급업체들은 국경 간 차질 방지를 위해 지역 내 멤브레인 캐스팅 라인을 확장하고 있습니다.

아시아태평양 지역은 2030년까지 연평균 8.54% 성장률(CAGR)을 기록할 전망으로, 전 지역 중 가장 빠른 성장세를 보일 것입니다. 한국, 일본, 싱가포르는 mRNA 백신 및 바이러스 벡터 생산 능력 확장의 선두주자로, 팬데믹 대비를 목표로 한 국가 차원의 인센티브가 뒷받침되는 경우가 많습니다. 팔 코퍼레이션의 1억 5,000만 달러 규모 싱가포르 공장은 해당 지역의 인재 풀과 물류 역량에 대한 다국적 기업의 신뢰를 보여주는 사례입니다. 지역 CDMO(계약 개발 및 제조 기관)들은 매력적인 비용 구조와 첨단 일회용 설비를 결합하여, 위험 분산형 공급 전략을 모색하는 서구 후원사들을 유치하고 있습니다.

유럽은 오랜 GMP(우수제조관리기준) 준수 역량과 광범위한 혈장분획 생산 능력을 바탕으로 견고한 입지를 유지하고 있습니다. 그러나 유럽화학물질청(ECHA)의 PFAS(불소화합물) 제한 제안이 임박함에 따라 PVDF(폴리비닐디플루오로에틸렌) 막 공급에 심각한 차질이 발생할 수 있어, 필터 설계사들은 PFAS 무함유 대체재 개발을 가속화해야 할 것입니다. 고유량 및 조절 가능한 기공 크기를 제공하는 나노섬유 막이 실용적인 대체재로 부상했으며, Matregenix는 바이러스 제거에 맞춤화된 플랫폼을 보고했습니다. 소재 대체에 대한 규제 불확실성으로 주요 바이오제조업체들은 공급 연속성을 미래에 대비하기 위한 병행 밸리데이션 프로그램을 추진 중입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 의약품 및 바이오의약품의 연구개발비 증가

- 생물학적 제제와 유전자 치료에 대한 수요 증가

- 일회용 여과 기술의 채용

- CDMO/CMO 아웃소싱 모델 확대

- 연속 생물공정 및 인라인 바이러스 여과로의 전환

- 제품 출시 가속화를 위한 AI 기반 막 공학

- 시장 성장 억제요인

- 엄격한 밸리데이션 및 규제 당국의 승인 일정

- 대용량 여과 스키드의 높은 자본 비용

- PFAS 관련 막재료 공급의 혼란

- TMPS 내 높은 벡터 불순물 부하로 인한 필터 오염

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 여과 시스템

- 멤브레인 필터

- 심층 필터

- 중공 섬유 필터

- 나노 여과 모듈

- 키트, 시약, 소모품

- 무결성 시험 시약

- 프리 필터 & 멤브레인

- 서비스

- 바이러스 클리어런스 시험

- 밸리데이션 & 컨설팅

- 여과 시스템

- 여과 모드별

- 배치 여과

- 연속 여과/인라인 여과

- 용도별

- 생물학적 제제

- 백신 및 치료제

- 혈액 및 혈장 제품

- 세포 및 유전자 치료

- 조직 유래 제품

- 기타 생물학적 제제

- 의료기기

- 정수

- 공기 정화

- 생물학적 제제

- 최종 사용자별

- 제약 및 생명공학 기업

- 계약 개발 및 제조 기관(CDMO)

- CRO(의약품 개발 업무 계약 기관)

- 학술 및 정부연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Asahi Kasei Medical Co. Ltd

- Danaher Corporation(Pall)

- Merck KGaA(MilliporeSigma)

- Sartorius AG

- Thermo Fisher Scientific Inc.

- Charles River Laboratories International Inc.

- Lonza Group Ltd

- Wuxi Biologics

- 3M Purification

- Repligen Corp.

- Parker Hannifin(Bioscience)

- Meissner Filtration Products

- FUJIFILM Wako Pure Chemical

- PendoTECH

- Clean Cells SAS

- Alfa Laval

- GE Healthcare Life Sciences

- 3S Bio(Synartro)

- TSI Scientific

- GEA Group

제7장 시장 기회와 장래의 전망

HBR 25.11.27The virus filtration market size was USD 1.54 billion in 2025 and is projected to reach USD 2.19 billion by 2030, reflecting a 7.37% CAGR.

Heightened regulatory focus on viral safety, fast-rising biologics pipelines, wider adoption of single-use systems, and the transition toward continuous bioprocessing are the principal engines propelling the virus filtration market. Suppliers are responding by upgrading membrane materials, integrating automation, and embedding in-line analytics to shorten validation cycles. Heightened investments in mRNA vaccines and gene therapies continue to amplify demand for robust clearance technologies across North America, Europe, and especially Asia-Pacific. Meanwhile, strategic acquisitions among leading vendors illustrate an industry intent on broadening end-to-end portfolios, shoring up supply resilience, and advancing next-generation filter performance.

Global Virus Filtration Market Trends and Insights

Rising Demand for Biologics & Gene Therapies

The T-cell therapy segment alone is forecast to balloon from USD 10.30 billion in 2025 to USD 161.21 billion by 2034, driving unprecedented volumes of viral vectors that must be purified without structural loss. More than 700 active AAV programs require filters capable of maintaining capsid integrity at ever-higher titers. Lentiviral production faces even sharper fouling challenges, making low-adsorptive membranes essential for acceptable recovery. Industry participants consequently invest in predictive modeling tools to pre-screen filter candidates and cut extensive wet-lab iterations. This surge in biologics underscores the virus filtration market's centrality to next-generation therapeutics.

Adoption of Single-Use Filtration Technologies

Contract development and manufacturing organizations (CDMOs) favor single-use assemblies for campaign flexibility and lower cleaning validation overheads. High-throughput microcarrier cultures can now pair with disposable virus filters rated for multi-barrier removal. Asahi Kasei's Planova FG1, released in 2024, achieves seven-fold faster flux versus its predecessor while retaining compatibility with existing holders. Automated pressure monitoring and integrity-test sockets come standard, aligning with Annex 1 requirements for pre-use post-sterilization testing.

Stringent Validation & Regulatory Approval Timelines

The FDA's revised Q5A(R2) guidance specifies deeper virus panel testing and endorses new detection technologies, pushing firms to update validation protocols and archival records. Cygnus Technologies' MockV kits help predict clearance early using non-infectious surrogates, yet full-scale spiking studies remain mandatory for licensure. Developers must therefore budget for multi-phase pilot work, statistical robustness evaluations, and regulator engagement sessions, lengthening time to market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of CDMO/CMO Outsourcing Models

- AI-Driven Membrane Engineering Accelerating Product Launches

- High Capital Cost of High-Capacity Filtration Skids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Kits, reagents, and consumables generated 58.43% of the virus filtration market size in 2024, a testament to their recurring use in every production run. Demand is magnified by the turn toward disposable assemblies, where each lot requires fresh capsules, integrity-test reagents, and prefilters. Rising biologics titers intensify fouling, elevating cartridge replacement rates and bolstering consumables revenue. In contrast, systems revenue is one-time yet rising briskly as next-generation skids integrate data historians, auto-flush features, and digital twin compatibility. Membrane innovations-such as PFAS-free polyamide composites-further differentiate premium models aimed at gene-therapy vectors susceptible to adsorption losses.

Filtration systems are pacing the segment with a 9.65% CAGR through 2030. Vendors highlight planar flow paths that minimize shear and maintain viral vector infectivity. Asahi Kasei's FG1 launch epitomizes this trajectory, delivering seven-fold higher throughput at equivalent log-reduction values. Hardware modularity permits straightforward swap-outs between stainless housings and single-use capsules, appealing to CDMOs juggling diverse client pipelines. Advisory services-ranging from filterability screening to end-to-end validation documentation-are becoming bundled, creating annuity revenue streams even for equipment-centric suppliers.

Batch filtration retained 55.43% of the virus filtration market share in 2024 as legacy stainless facilities opt to extend validated methods rather than embrace wholesale redesigns. Operators value the extensive historical data that batch processes hold, easing regulatory dialogue and post-approval change management. Moreover, disposables readily retrofit existing batch hold tanks, allowing incremental capacity boosts without full facility refit. Nevertheless, the inherent start-stop nature imposes labor peaks and product hold times that hamper total equipment effectiveness.

Continuous and in-line filtration is advancing at a 9.88% CAGR, capitalizing on the broader shift to perfusion cell culture. At 2,000 L commercial scale, steady-state filtrate streams already satisfy global pharmacopoeia sterility norms while halving buffer consumption. Parallel filter arrays mitigate flux decay, and smart valves divert flow when sensors detect impending fouling-safeguarding product integrity without interrupting throughput. Regulators increasingly advocate holistic control-strategy filings, which continuous platforms naturally support via integrated, real-time analytics.

The Virus Filtration Market Report is Segmented by Product (Filtration Systems, and More), Filtration Mode (Batch and Continuous/In-line), Application (Biologicals, Medical Devices, and Water/Air Purification), End User (Pharmaceutical/Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East/Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America delivered 43.23% of global revenue in 2024, anchored by the United States' deep biologics R&D pipelines and the FDA's role in setting viral-safety benchmarks. Major capacity investments-such as Fujifilm Diosynth's USD 1.2 billion cell-culture expansion in North Carolina-signal ongoing confidence in domestic infrastructure. Mature supply chains ease access to sterile capsules and validation viruses, giving local plants a time-to-market edge. As more mRNA and gene-therapy candidates move to late stage, filter suppliers are scaling membrane casting lines inside the region to safeguard against cross-border disruptions.

Asia-Pacific is on track for an 8.54% CAGR to 2030, the fastest among all regions. South Korea, Japan, and Singapore headline capacity expansions for mRNA vaccines and viral vectors, often backed by state incentives aimed at pandemic readiness. Pall Corporation's USD 150 million Singapore plant exemplifies multinational faith in the region's talent pool and logistics reach. Regional CDMOs combine attractive cost structures with cutting-edge single-use suites, drawing Western sponsors seeking risk-diversified supply strategies.

Europe preserves a robust footprint underpinned by long-standing GMP rigor and extensive plasma-fractionation capacity. Yet the looming European Chemicals Agency proposal to restrict PFAS could significantly disrupt PVDF membrane availability, compelling filter designers to accelerate PFAS-free alternatives. Nanofiber membranes that deliver high flow and tunable pore size have surfaced as practical substitutes, with Matregenix reporting customizable platforms tailored for virus removal. Regulatory uncertainty around material substitution is prompting parallel validation programs across leading biomanufacturers to future-proof supply continuity.

- Asahi Kasei

- Danaher Corporation (Pall)

- Merck KGaA (MilliporeSigma)

- Sartorius

- Thermo Fisher Scientific

- Charles River

- Lonza Group

- Wuxi Biologics

- 3M Purification

- Repligen Corp.

- Parker Hannifin (Bioscience)

- Meissner Filtration Products

- FUJIFILM Wako Pure Chemical

- PendoTECH

- Clean Cells SAS

- Alfa Laval

- GE Healthcare Life Sciences

- 3S Bio (Synartro)

- TSI Scientific

- GEA Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Pharmaceutical & Biopharma R&D Spending

- 4.2.2 Rising Demand for Biologics & Gene Therapies

- 4.2.3 Adoption of Single-Use Filtration Technologies

- 4.2.4 Expansion of CDMO/CMO Outsourcing Models

- 4.2.5 Shift Toward Continuous Bioprocessing & In-Line Virus Filtration

- 4.2.6 AI-Driven Membrane Engineering Accelerating Product Launches

- 4.3 Market Restraints

- 4.3.1 Stringent Validation & Regulatory Approval Timelines

- 4.3.2 High Capital Cost of High-Capacity Filtration Skids

- 4.3.3 PFAS-Related Membrane Material Supply Disruptions

- 4.3.4 Filter Fouling from High-Vector Impurity Loads in Atmps

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Filtration Systems

- 5.1.1.1 Membrane-based filters

- 5.1.1.2 Depth filters

- 5.1.1.3 Hollow-fiber filters

- 5.1.1.4 Nanofiltration modules

- 5.1.2 Kits, Reagents & Consumables

- 5.1.2.1 Integrity test reagents

- 5.1.2.2 Prefilters & membranes

- 5.1.3 Services

- 5.1.3.1 Virus clearance studies

- 5.1.3.2 Validation & consulting

- 5.1.1 Filtration Systems

- 5.2 By Filtration Mode

- 5.2.1 Batch Filtration

- 5.2.2 Continuous / In-line Filtration

- 5.3 By Application

- 5.3.1 Biologicals

- 5.3.1.1 Vaccines & Therapeutics

- 5.3.1.2 Blood & Plasma Products

- 5.3.1.3 Cellular & Gene Therapies

- 5.3.1.4 Tissue-derived Products

- 5.3.1.5 Other Biologics

- 5.3.2 Medical Devices

- 5.3.3 Water Purification

- 5.3.4 Air Purification

- 5.3.1 Biologicals

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Contract Development & Manufacturing Organizations (CDMOs/CMOs)

- 5.4.3 Contract Research Organizations (CROs)

- 5.4.4 Academic & Government Labs

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Asahi Kasei Medical Co. Ltd

- 6.3.2 Danaher Corporation (Pall)

- 6.3.3 Merck KGaA (MilliporeSigma)

- 6.3.4 Sartorius AG

- 6.3.5 Thermo Fisher Scientific Inc.

- 6.3.6 Charles River Laboratories International Inc.

- 6.3.7 Lonza Group Ltd

- 6.3.8 Wuxi Biologics

- 6.3.9 3M Purification

- 6.3.10 Repligen Corp.

- 6.3.11 Parker Hannifin (Bioscience)

- 6.3.12 Meissner Filtration Products

- 6.3.13 FUJIFILM Wako Pure Chemical

- 6.3.14 PendoTECH

- 6.3.15 Clean Cells SAS

- 6.3.16 Alfa Laval

- 6.3.17 GE Healthcare Life Sciences

- 6.3.18 3S Bio (Synartro)

- 6.3.19 TSI Scientific

- 6.3.20 GEA Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment