|

시장보고서

상품코드

1852187

암 악액질 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cancer Cachexia - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

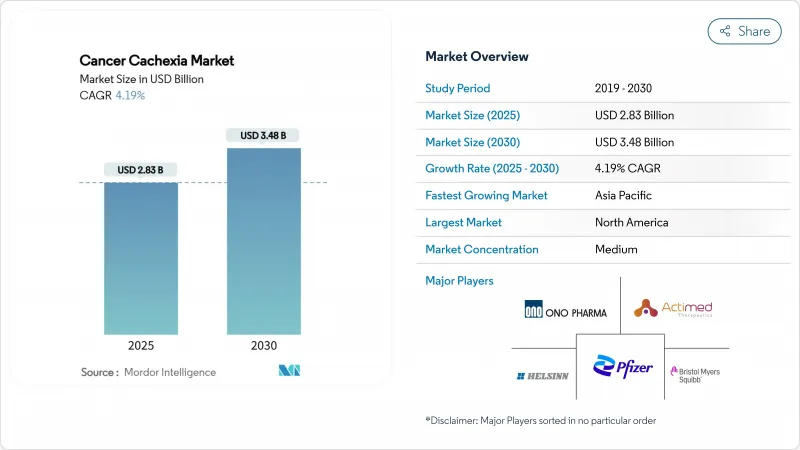

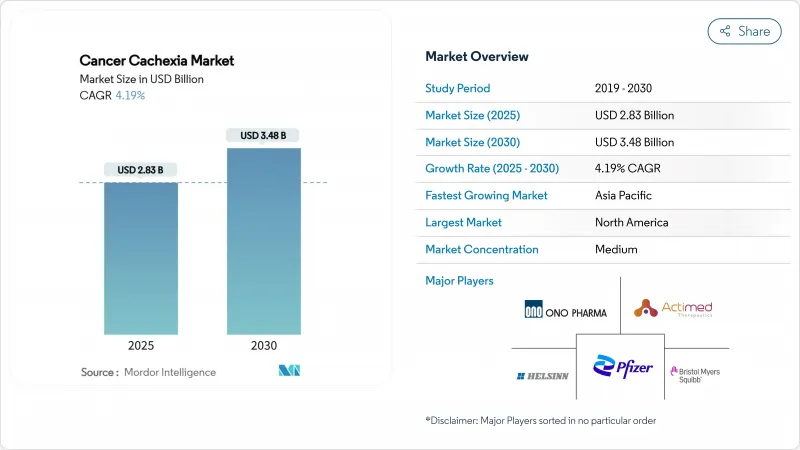

암악액질 시장 규모는 2025년에 28억 3,000만 달러로 평가되었고, 획기적인 치료제이 개념 실증에서 등록 시험으로 이행해, 조기 진단 프로그램에 의해 대상이 되는 환자층이 확대하는 것으로부터, CAGR은 4.19%를 나타낼 것으로 예측되며, 2030년에 34억 8,000만 달러에 달할 전망입니다.

종양 생존율 향상, 바이오마커 기반 환자 식별, 명확한 규제 지침의 지속적인 융합으로 암 악액질 시장은 지속적인 성장을 위한 기반을 마련하고 있습니다. 이미 임상적 영향력을 확보한 그렐린 수용체 작용제가 성장을 주도하고 있으나, GDF-15, 미오스타틴 또는 이중 동화-이화 경로를 차단하는 차세대 제제들이 경쟁 구도를 다각화할 전망입니다. 복잡한 투여 시작 프로토콜로 인해 병원 약국이 여전히 주요 조제 장소이지만, 디지털 재고 관리 솔루션으로 온라인 채널의 점유율 확대가 가속화되고 있습니다. 지역별 성장 동력은 미국, 일본, 중국에 달려 있으며, 이들 국가에서는 정부 지원 보상 시범 사업이 시작되어 악액질을 완화적 종말이 아닌 별도의 치료 가능 질환으로 분류하기 시작했습니다.

세계의 암악액질 시장 동향 및 인사이트

암 유병률 상승과 환자 생존율 향상

2024년 전 세계 신규 암 진단 건수는 2천만 건 이상으로 증가했으며, 5년 생존율은 평균 68%에 달해 위험군 인구가 확대되고 대사 기능 저하 기간이 연장되었습니다. 생존 기간 연장으로 악액질은 말기 증상보다 만성 동반 질환으로 전환되어 지속적인 약물 관리가 필수적입니다. 면역항암제는 체중 감소 경로를 추가로 변화시켜 반복적 개입이 필요한 간헐적 근육 소모 단계를 유발합니다. 고령화 인구와 암 발생률 증가가 겹치면서 누적 유병률은 해마다 증가하고 있습니다. 이러한 구조적 요인들은 암 악액질 시장을 광범위한 종양학 성장 곡선에 묶어 놓습니다.

체중 및 근력 유지에 대한 높은 미충족 요구

미국 및 유럽 시장에서 FDA 승인 약물이 부재함에 따라 의사들은 비승인 용도로 코르티코스테로이드와 메게스트롤을 사용하게 되는데, 이 둘 모두 제 지방 체중이나 기능적 능력을 유지하지 못합니다. 종양학자들은 악액질을 화학요법 투여량 강도와 면역요법 반응의 제한 요인으로 점점 더 인식하며, 이에 따라 근육 위축을 예방하는 약제에 대한 수요가 증가하고 있습니다. 건강 관련 삶의 질 설문조사에서는 체중 안정성이 환자에게 최우선 순위임을 일관되게 보여주고 있지만, 현재의 치료법은 미미한 효과만을 제공합니다. 진단 기준의 불투명성은 다기관 임상시험과 보험급여 심사를 방해하는 상이한 기준들로 인해 치료 격차를 더욱 심화시킵니다.

제한된 승인 약물 치료

유럽의약품청(EMA)이 기능적 혜택 부족을 이유로 아나모렐린 승인을 거부한 사례는 종점 기대치의 변동성이 개발사 신뢰도를 위축시키는 방식을 보여줍니다. 체중 및 식욕 지표만으로는 입원률이나 생존율과의 검증된 상관관계를 요구하는 보험사들을 만족시키기 어렵습니다. 명확한 선례 부재로 파이프라인 기업들은 더 큰 재정적 위험을 감수해야 하며, 종종 대형 파트너사와 공동 개발을 선택해 전반적인 혁신 속도를 저하시킵니다. 라벨 승인 선택지 부재는 임상 실무의 이질성을 지속시켜 진정한 수요를 가립니다.

부문 분석

그렐린 수용체 작용제는 2024년 암 악액질 시장 점유율 34.56%를 차지했으며, 이는 일본에서 아나모렐린에 대한 임상적 친숙도와 6,000명 이상의 치료 환자에서 수집된 실세계 데이터가 뒷받침합니다. 이 계열의 암 악액질 시장 규모는 신규 승인을 기다리는 시장에서 점진적인 도입을 통해 꾸준한 성장세를 유지할 것으로 전망됩니다. 그러나 베타 차단제 기반 동화-이화 전환제(ACTAs)는 S-핀돌롤의 대장암 환자군에서 단백질 분해 억제와 근육 단백질 합성 촉진을 동시에 보여준 2상 성공에 힘입어 6.56%의 연평균 복합 성장률(CAGR)을 기록할 전망입니다.

제약사들은 효능 향상을 위해 그렐린 작용제를 항염증제나 안드로겐 수용체 조절제와 결합하는 사례가 증가하고 있습니다. 프로게스토겐과 코르티코스테로이드는 진행성 질환에서 틈새 시장을 유지하지만, 대사 독성으로 장기 투여 일정이 제한되어 추가 매출 기여도는 미미합니다. 에노보사름과 같은 선택적 안드로겐 수용체 조절제는 기전적 혁신성을 제공하나, 규제 당국은 만성 투여 안전성에 대한 검토를 지속하고 있습니다. 이에 따라 포트폴리오 전략은 기전적 다각화로 기울어지며, 기업들은 검증된 식욕 자극 경로와 신흥 ACTA 조합 간 균형을 모색 중입니다.

식욕 자극제는 2024년 매출 풀의 46.54%를 차지했으나, 이화작용 경로 억제제가 6.83%의 가장 빠른 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다. 이는 열량 섭취만으로는 근감소증을 막을 수 없다는 임상의들의 인식 증가를 반영합니다. 규제 승인이 잘 연구된 분자를 선호하는 지역에서는 식욕 기반 제제가 여전히 1차 치료의 핵심을 이루겠지만, 2세대 치료제는 이제 섭식 행동 자체를 우회하여 근육 프로테아좀 활성화를 차단합니다. 이에 따라 암 악액질 산업은 유비퀴틴 리가아제 활성 또는 하류 염증 캐스케이드를 차단하는 제제로의 전환을 목격하고 있습니다.

선택적 안드로겐 수용체 결합 및 미오스타틴 억제를 통한 동화 작용 지원은 다중 모드 요법에서 종종 파이프라인 자리를 계속 채우고 있습니다. IL-1 또는 TNF-알파 표적 면역조절제는 그렐린 작용제와 병용 시 가산적 효과를 보여, 단일요법 우위에서 복합 치료 생태계로의 전환 가능성을 시사합니다. 이중작용 ACTA 계열은 체중 증가와 함께 유럽에서 규제 기관이 인정하는 기능적 평가 지표인 손잡이 근력 향상을 동시에 제공함으로써 이러한 변화를 대표합니다. 업계 분석가들은 기업들이 프랜차이즈 가치를 보호하기 위해 융합된 작용기전을 특허화함에 따라 범주 간 경계가 모호해질 것으로 전망합니다.

지역 분석

북미는 탄탄한 R&D 자금 지원, 광범위한 임상 시험 네트워크, 주요 등록 연구에 악액질 평가 지표를 조기에 포함시킨 덕분에 2024년 글로벌 매출의 43.45%를 창출했습니다. 학술 센터들은 종양학 치료 경로에 대사 모니터링을 일상적으로 포함시켜 조기 진단과 지원 치료 클리닉으로의 의뢰를 촉진하고 있습니다. 이러한 우위에도 불구하고, 민간 보험사들이 아직 정량화되지 않은 입원 비용 절감 효과와 단기 약물 비용을 비교 평가함에 따라 보험 적용 관련 어려움은 지속되고 있습니다.

아시아태평양 지역은 일본의 획기적인 아나모렐린(anamorelin) 등재와 중국의 급속히 확장되는 종양학 인프라에 힘입어 2030년까지 연평균 5.43%의 성장률을 보일 전망입니다. 한국, 호주, 싱가포르의 조화된 가이드라인으로 해외 제출 서류의 심사 기간이 단축되고 있습니다. 현지 바이오테크 파이프라인은 마이오스타틴 및 GDF-15 경로를 표적으로 삼고 있으며, 이는 최초 출시(first-in-class)에 대한 정부의 강력한 인센티브를 반영합니다. 공공-민간 파트너십은 영양 상담과 약물 치료를 결합한 근육 건강 프로그램에 투자하며 종합 솔루션 수요를 가속화하고 있습니다.

유럽은 분산된 보험급여 환경으로 출시가 지연되며 완만한 성장세를 보입니다. 유럽의약품청(EMA)의 기능적 평가 지표 요구로 여러 후보물질의 시장 진입이 지연되었으나, 국가 암 계획에 악액질 선별 지표가 추가되면서 진단률이 상승할 전망입니다. 독일과 이탈리아의 선도 기관들은 물리치료사와 약물 요법을 결합한 다중모드 클리닉을 시범 운영 중이며, 이는 실제 임상 데이터를 생성해 비용효과성 평가에서 도입을 지지하는 근거가 될 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 암 유병률의 상승과 환자 생존율

- 체중 및 근육 보존에 대한 높은 미충족 임상 수요

- 악액질 병리생리학 이해의 진전

- 확대되는 항암제 파이프라인 및 병용 치료 기회

- 주요 시장의 유리한 보험급여 및 규제 지원

- 다중 치료 접근법의 확산

- 시장 성장 억제요인

- 승인된 약물 치료법의 제한

- 신약의 안전성과 효능에 대한 우려

- 표준화된 진단 기준과 임상시험 엔드포인트의 부족

- 높은 개발 비용 및 보험급여 불확실성

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 임상시험의 상황

제5장 시장 규모와 성장 예측

- 치료 클래스별

- 그렐린 수용체 작용제

- 선택적 안드로겐 수용체 조절제(SARMs)

- β차단제/ACTA

- 프로게스토겐

- 코르티코스테로이드

- 병용 요법

- 기타 치료 클래스

- 작용기전별

- 식욕 자극제

- 단백질 동화제

- 이화경로 억제제

- 항염증제/면역조절제

- 다중 표적 ACTA

- 암 유형별

- 폐암

- 소화기암

- 유방암

- 전립선암

- 혈액 악성 종양

- 기타 암 유형

- 악액질 스테이지별

- 전악액질

- 악액질기

- 불응성 악액질

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 지리

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Helsinn Group

- Ono Pharmaceutical

- Actimed Therapeutics

- Pfizer Inc.

- Bristol-Myers Squibb

- Merck KGaA

- Artelo Biosciences

- Novartis AG

- CatalYm GmbH

- NGM Bio

- Aveo Oncology

- Aeterna Zentaris

- Fresenius Kabi

- TCI Peptide Therapeutics

- Cannabics Pharmaceuticals

- Tetra Bio-Pharma

- PsiOxus Therapeutics

- Aavogen Inc.

제7장 시장 기회와 장래의 전망

HBR 25.11.27The cancer cachexia market size generated USD 2.83 billion in 2025 and is forecast to advance at a 4.19% CAGR, reaching USD 3.48 billion by 2030, as breakthrough therapeutics move from proof-of-concept into registration studies and early diagnosis programs widen the eligible patient pool.

Ongoing convergence of oncology survivorship gains, biomarker-enabled patient identification, and clear regulatory guidance positions the cancer cachexia market for durable expansion. Growth is anchored by ghrelin receptor agonists that already hold clinical traction, yet next-generation agents blocking GDF-15, myostatin, or dual anabolic-catabolic pathways are set to diversify the competitive field. Hospital pharmacies remain the dominant dispensing venue because of complex initiation protocols, although digital inventory solutions let online channels accelerate share capture. Regional momentum hinges on the United States, Japan, and China, where government-backed reimbursement pilots have begun to classify cachexia as a distinct treatable condition rather than a palliative endpoint.

Global Cancer Cachexia Market Trends and Insights

Rising Cancer Prevalence and Patient Survival

Global incidence rose to more than 20 million new diagnoses in 2024 and 5-year survival now averages 68%, effectively enlarging the at-risk population and prolonging the window for metabolic decline. Longer survival turns cachexia into a chronic comorbidity rather than a terminal sign, making durable pharmacologic control essential. Immuno-oncology agents further alter weight-loss trajectories, creating episodic muscle-wasting phases that require repeat intervention. Since ageing populations overlap with higher cancer incidence, cumulative prevalence stacks year over year. These structural forces bind the cancer cachexia market to the broader oncology growth curve.

High Unmet Clinical Need for Weight and Muscle Preservation

Absence of FDA-approved drugs in the American and European markets leaves physicians with off-label corticosteroids and megestrol, neither of which sustain lean body mass or functional capacity. Oncologists increasingly view cachexia as a limiting factor for chemotherapy dose intensity and immunotherapy response, thereby elevating demand for agents that prevent muscle atrophy. Health-related quality-of-life surveys consistently rank weight stability as a top priority for patients, yet current regimens offer marginal benefit. Diagnostic opacity compounds the treatment gap because dissimilar criteria obstruct multicenter trials and reimbursement audits.

Limited Approved Pharmacotherapies

The European Medicines Agency's rejection of anamorelin on grounds of insufficient functional benefit demonstrates how variable endpoint expectations chill developer confidence. Weight and appetite metrics alone rarely satisfy payers that seek validated correlations with hospitalization rates or survival. Without clear precedents, pipeline companies shoulder heavier financial risk and often opt to co-develop with larger partners, slowing overall innovation velocity. Absence of label-approved choices also perpetuates heterogeneity in clinical practice, masking true demand.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Cachexia Pathophysiology Understanding

- Expanding Oncology Drug Pipeline and Combination Opportunities

- Safety and Efficacy Concerns of Novel Agents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ghrelin receptor agonists held 34.56% cancer cachexia market share in 2024, reflecting Japan's clinical familiarity with anamorelin and supportive real-world data collected from more than 6,000 treated patients. The cancer cachexia market size for this class is projected to maintain steady momentum through incremental uptake in markets that await novel approvals. However, beta-blocker-based anabolic-catabolic transforming agents (ACTAs) are on course for a 6.56% CAGR, propelled by S-pindolol's Phase 2 success in colorectal cancer cohorts showing simultaneous attenuation of proteolysis and stimulation of muscle protein synthesis.

Drug developers increasingly bundle ghrelin agonists with anti-inflammatory or androgen receptor modulators to enhance efficacy. Progestogens and corticosteroids retain niche utility in advanced disease but contribute marginal incremental revenue because metabolic toxicity limits long-term dosing schedules. Selective androgen receptor modulators like enobosarm offer mechanistic novelty, though regulators continue to scrutinize safety for chronic administration. Portfolio strategies therefore gravitate toward mechanistic diversification, with companies balancing the validated appetite route against emerging ACTA combinations.

Appetite stimulators secured 46.54% of the 2024 revenue pool, yet catabolic-pathway inhibitors are forecast for the fastest 6.83% CAGR, mirroring rising clinician belief that caloric intake alone cannot halt sarcopenia. Appetite-based agents will still anchor first-line therapy in regions where regulatory clearance favors well-studied molecules, but second-generation treatments now bypass feeding behavior altogether to block muscle proteasome activation. The cancer cachexia industry thus witnesses a pivot toward agents that interrupt ubiquitin ligase activity or downstream inflammatory cascades.

Anabolic support through selective androgen receptor binding and myostatin inhibition continues to fill pipeline slots, often in multimodal regimens. Immunomodulators targeting IL-1 or TNF-alpha show additive effects when paired with ghrelin agonists, suggesting a future in which combination ecosystems replace monotherapy dominance. Dual-acting ACTAs epitomize this shift by delivering weight gain alongside improved hand-grip strength, a regulatory-recognized functional endpoint in Europe. Industry analysts anticipate that categorical boundaries will blur as companies patent merged mechanisms to defend franchise value.

The Cancer Cachexia Market Report is Segmented by Therapeutic Class (Ghrelin Receptor Agonists, and More), Mechanism of Action (Appetite Stimulators, Anabolic Agents, and More), Cancer Type (Lung Cancer, and More), Stage of Cachexia (Pre-Cachexia, and More), Distribution Channel (Hospital Pharmacies, and More), Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 43.45% of global revenue in 2024 thanks to resilient R&D financing, extensive clinical trial networks, and early inclusion of cachexia endpoints within major registrational studies. Academic centers routinely embed metabolic monitoring within oncology pathways, driving timely diagnosis and referral to supportive care clinics. Despite this edge, reimbursement headwinds linger because private payers weigh short-term drug costs against yet-to-be-quantified hospitalization savings.

Asia-Pacific is advancing at a 5.43% CAGR through 2030, propelled by Japan's landmark anamorelin listing and China's rapidly scaling oncology infrastructure. Harmonized guidelines across Korea, Australia, and Singapore are shortening review timelines for foreign dossiers. Local biotech pipelines target myostatin and GDF-15 pathways, reflecting strong government incentives for first-in-class launches. Public-private partnerships invest in muscle health programs that bundle nutritional counseling with pharmacotherapy, accelerating demand for comprehensive solutions.

Europe shows moderate growth as fragmented reimbursement landscapes slow rollout. The EMA's insistence on functional endpoints has delayed market entry for several candidates, yet national cancer plans are now adding cachexia screening metrics, which should lift diagnosis rates. Leading institutions in Germany and Italy pilot multimodal clinics pairing physiotherapists with pharmacologic regimens, generating real-world data that could tip cost-effectiveness evaluations in favor of adoption.

- Helsinn Group

- Ono Pharmaceutical

- Actimed Therapeutics

- Pfizer

- Bristol-Myers Squibb

- Merck

- Artelo Biosciences

- Novartis

- CatalYm GmbH

- NGM Bio

- AVEO Pharmaceuticals

- Aeterna Zentaris

- Fresenius

- TCI Peptide Therapeutics

- Cannabics Pharmaceuticals

- Tetra Bio-Pharma

- PsiOxus Therapeutics

- Aavogen

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Cancer Prevalence and Patient Survival

- 4.2.2 High Unmet Clinical Need for Weight and Muscle Preservation

- 4.2.3 Advancements in Cachexia Pathophysiology Understanding

- 4.2.4 Expanding Oncology Drug Pipeline and Combination Opportunities

- 4.2.5 Favorable Reimbursement and Regulatory Support in Key Markets

- 4.2.6 Growing Adoption of Multimodal Care Approaches

- 4.3 Market Restraints

- 4.3.1 Limited Approved Pharmacotherapies

- 4.3.2 Safety and Efficacy Concerns of Novel Agents

- 4.3.3 Lack of Standardized Diagnostic Criteria and Trial Endpoints

- 4.3.4 High Development Costs and Reimbursement Uncertainty

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Clinical-Trial Landscape

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapeutic Class

- 5.1.1 Ghrelin Receptor Agonists

- 5.1.2 Selective Androgen Receptor Modulators (SARMs)

- 5.1.3 Beta-blockers / ACTAs

- 5.1.4 Progestogens

- 5.1.5 Corticosteroids

- 5.1.6 Combination Therapy

- 5.1.7 Other Therapeutic Classess

- 5.2 By Mechanism of Action

- 5.2.1 Appetite Stimulators

- 5.2.2 Anabolic Agents

- 5.2.3 Catabolic-Pathway Inhibitors

- 5.2.4 Anti-inflammatory / Immunomodulators

- 5.2.5 Multi-target ACTAs

- 5.3 By Cancer Type

- 5.3.1 Lung Cancer

- 5.3.2 Gastro-intestinal Cancers

- 5.3.3 Breast Cancer

- 5.3.4 Prostate Cancer

- 5.3.5 Hematologic Malignancies

- 5.3.6 Other Cancer Types

- 5.4 By Stage of Cachexia

- 5.4.1 Pre-cachexia

- 5.4.2 Established Cachexia

- 5.4.3 Refractory Cachexia

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies

- 5.5.3 Online Pharmacies

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Helsinn Group

- 6.3.2 Ono Pharmaceutical

- 6.3.3 Actimed Therapeutics

- 6.3.4 Pfizer Inc.

- 6.3.5 Bristol-Myers Squibb

- 6.3.6 Merck KGaA

- 6.3.7 Artelo Biosciences

- 6.3.8 Novartis AG

- 6.3.9 CatalYm GmbH

- 6.3.10 NGM Bio

- 6.3.11 Aveo Oncology

- 6.3.12 Aeterna Zentaris

- 6.3.13 Fresenius Kabi

- 6.3.14 TCI Peptide Therapeutics

- 6.3.15 Cannabics Pharmaceuticals

- 6.3.16 Tetra Bio-Pharma

- 6.3.17 PsiOxus Therapeutics

- 6.3.18 Aavogen Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment