|

시장보고서

상품코드

1852192

수산화리튬 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Lithium Hydroxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

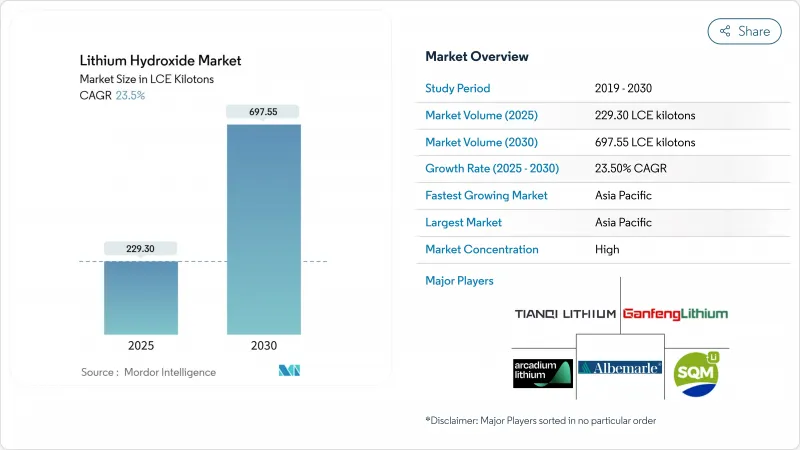

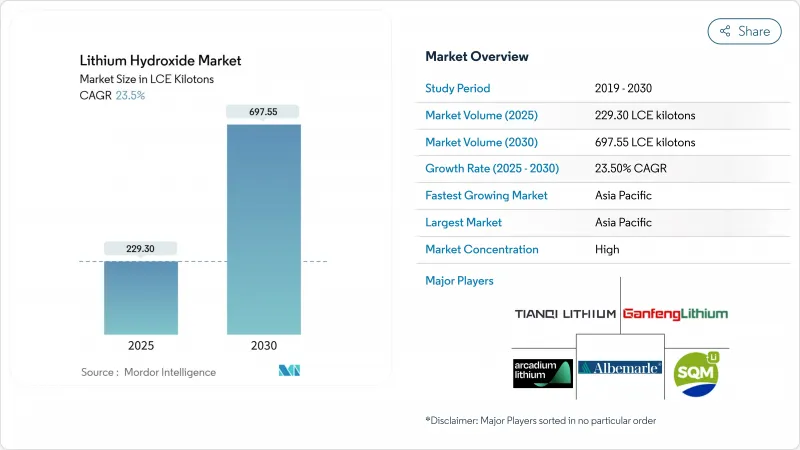

수산화리튬 시장 규모는 2025년에 229.30LCE 킬로톤, 2030년에는 697.55LCE 킬로톤에 이르고, 예측 기간(2025-2030년) CAGR은 23.5%를 나타낼 전망입니다.

전지 화학을 둘러싼 경쟁 격화, 전기자동차(EV) 판매 급증, 리튬 직접 추출(DLE) 기술의 급속한 스케일 업으로 세계 공급망이 재구성되고 있습니다. 아시아태평양은 세계 소비량의 40%를 차지하는 가장 규모가 큰 지역으로, 2030년까지의 성장률은 27.66%로 가장 빠릅니다. 자동차 제조업체는 고순도 원료를 확보하기 위해 2024년 장기 조달 계약을 체결했으며 일부 배터리 제조업체는 가격 변동을 헤지하기 위해 수직 통합 전략을 가속화했습니다. 동시에 2023년에는 8만1,500달러/톤에서 2만2,500달러/톤으로 원료가격의 변동이 심해지기 때문에 프로젝트 파이낸스 모델에 대한 과제도 남습니다.

세계 수산화리튬 시장 동향과 통찰

전동 공구 수요 증가

무선 전동 공구는 리튬 이온 팩이 더 긴 가동 시간과 우수한 파워 웨이트 레시오를 실현하기 위해 건설 및 산업 유지 보수에서 코드가있는 대체품을 대체하고 있습니다. 제조업체 각사는 고방전 사이클용으로 최적화된 셀 형식을 발매하고 있으며, 수산화리튬이 풍부한 니켈루코발토망간 양극이 선호되고 있습니다. 북미와 유럽에서는 노동 시장의 박박에 따라 생산성 향상이 중시되기 때문에 전문공사업자들 사이에서의 보급이 가장 진행되고 있습니다. 건축 정보 모델링 워크 플로우의 지속적인 채택은 작업자가 현장에서 구속되지 않는 기동성을 필요로하기 때문에 무선 공구의 보급을 더욱 가속화합니다. EV 수요보다 작은 것,이 틈새 시장은 특수 양극 합재를 공급하는 수산화물 제조업체에게 평균을 초과하는 가격 실현을 가져옵니다.

직접 리튬 추출(DLE)의 상업화로 저비용 원료를 확보

IBAT의 유타 공장에서는 모듈식 흡착 컬럼을 이용한 필드 스케일의 성공으로 기존의 연못 증발에 필요한 수개월에 대해 수시간에 80-90%의 리튬 회수가 실증되었습니다. 캘리포니아의 프로젝트 ATLIS는 지열 감수로부터 연산 2만 톤의 수산화리튬을 공급하기 위해 13억 6,000만 달러의 조건부 대출 보증을 확보하여 DLE의 확장성에 대한 대출자의 신뢰를 확실히 했습니다. 수율이 높으면 1톤당 자본 집약도가 내려 물 부족 지역에서의 조업이 가능해집니다. 이것은 이온 교환이나 멤브레인의 많은 유형가 연못 방식보다 보급수의 소비량이 적기 때문입니다. 이러한 경제성은 환경 발자국을 줄이는 동시에 수산화 리튬 시장의 장기적인 공급 전망을 강화합니다.

높은 생산 비용

배터리 등급 수산화 리튬 플랜트는 고급 불순물 제어와 고가의 결정화 회로를 필요로 합니다. 알베마르는 호주 케머턴 공장의 확장을 중단하고 예정된 생산 능력을 절반으로 줄이고 현장 인력을 40% 줄였습니다. 다년간의 투자 회수 기간, 엄격한 환경 허가, 한정된 수력 야금의 인재 풀이, 높은 진입 장벽을 유지해, 특히 에너지 관세가 높은 지역에서는 신설의 기세를 둔화시키고 있습니다.

부문 분석

리튬 이온 배터리는 2024년 수요의 63%를 창출하고 2030년까지 연평균 복합 성장률(CAGR) 26.77%로 확대될 것으로 예측됩니다. 이 분야에서만 수산화리튬 시장 규모의 최대 부분을 차지하고 증가 톤수도 최대입니다. 니켈루코발토 망간(NCM)이나 니켈루코발토알루미늄(NCA)과 같은 범위 지향 화학제품은 탄산염이 아닌 수산화리튬을 합성에 필요로 하고 구조 수요를 지원하고 있습니다. 이와는 대조적으로, 윤활 그리스, 순화 공기 시스템, 특수 합성은 안정적이지만 소폭 기여에 머물고 있습니다. 유럽연합(EU)에서는 재활용 의무화가 진행되고 있으며, 예측기간 후반에는 2차적인 공급채널이 형성되어 1차적인 수요는 완화될 것이며, 대체될 수 없을 것으로 예측됩니다.

에너지 저장의 도입은 가장 빠르게 성장하는 서브 용도를 형성합니다. 신재생에너지 자산과 연동하는 대규모 배터리 팜에는 사이클 수명이 긴 화학물질이 필요합니다. 캘리포니아의 몇 기가와트 시간 규모의 설비와 같은 프로젝트에서는 니켈을 많이 포함하는 캐소드를 지정하는 것이 늘어나고, 수산화물의 소비를 강화하고 있습니다. 비용이 낮아짐에 따라 소규모 상업용 및 산업용 비하인드 미터 시스템도 이 기회에 참여하여 수산화리튬 시장은 거치형 및 모바일형에 걸쳐 다양한 성장 엔진을 유지하고 있습니다.

배터리 등급 재료는 2024년에 70%의 점유율을 차지하고 CAGR은 25.55%로 예측됩니다. 나트륨, 칼슘, 중금속에 대한 엄격한 불순물 규제는 기술 등급과의 가격 차이를 지원합니다. 리벤트와 같은 제조업체는 100ppm 미만의 불순물 총량 규제를 달성하기 위해 재결정 및 이온 교환 모듈에 추가 투자를 하고 있습니다. 이 투자는 자본 집약도를 높이지만 동시에 경쟁을 심화시킵니다. 기술 등급은 공차 임계값이 느슨한 그리스 및 세라믹 시장에 해당하며 산업 등급은 수처리 및 특정 합성 경로를 지원합니다.

배터리 등급 수산화리튬 시장 점유율은 OEM 사양이 길어짐에 따라 계속 상승할 것으로 보입니다. 차세대 솔리드 스테이트 및 고실리콘 음극 설계는 정밀한 화학양론과 초저함수율에 의존하며 품질 프리미엄을 증폭시키는 요인이 되고 있습니다. 수직 통합 식염수 또는 경질 암석 원료 외에도 사내 정제를 수행하는 생산자는이 마진 풀을 획득하기에 가장 적합한 위치에 있습니다.

수산화리튬 시장 보고서는 용도(리튬 이온 배터리, 윤활 그리스 등), 최종 이용 산업(자동차, 가전, 기타), 등급(배터리 등급, 기술 등급, 산업 등급), 형태(일수화물, 무수물), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 구분됩니다.

지역 분석

2024년 수산화리튬 시장 점유율 40%를 차지하는 아시아태평양은 다른 추종을 허락하지 않는 셀 제조 능력과, 강하의 정극, 부극, 팩 조립업자의 밀집한 클러스터의 혜택을 받고 있습니다. 중국의 정책지령은 현재 국내 조달을 우선해 내륙의 시오코칸수의 적극적인 개발과 해외출자를 촉구하고 있으며, 일본과 한국은 오랜 재료 과학의 전문지식을 활용해 경쟁력을 유지하고 있습니다. 인도는 2025-26년도 연방 예산 하에 국가 제조업 임무와 중요한 광물의 관세 면제로 이 싸움에 진출하여 현지 수산화물 전환 제안을 자극했습니다.

북미의 확대는 대규모 자금 패키지에 달려 있습니다. DOE가 알베마르에 교부한 1억 5,000만 달러는 연간 160만대의 EV에 공급 가능한 킹스 마운틴의 스포쥬멘 농축 장치를 지원하는 것입니다. 현대자동차그룹과 SK온은 조지아주에 50억 달러의 배터리 셀 공장을 건설하는 것을 승인하고 현지산 수산화물에 대한 지역의 양극 수요를 지원하고 있습니다. 이러한 이니셔티브는 아시아 공급망에 대한 의존도를 줄이고 미국 인플레이션 감소법의 조달 기준을 충족하는 것을 목표로 하고 있습니다.

남미는 여전히 주요 공급 기지입니다. 칠레의 국가 리튬 전략은 국가 감시를 지키면서 민간 진입을 유치하고 새로운 지질 조사에 의해 추정 매장량이 28% 증가했습니다. 아르헨티나는 리오 틴트의 25억 달러의 광산 투자와 여러 OEM 인수를 유치했습니다. 브라질의 EV 판매량은 2024년에 85% 급증했으며, BYD가 70%의 점유율을 차지하며 미래 국내 수산화물 전환의 필요성을 시사했습니다.

유럽은 엄격한 CO2 규제와 종합적인 재활용 의무화에 의해 생산 능력을 가속. 독일은 차세대 캐소드의 연구개발을 선도하고 EU 전지규칙에서는 2025년 이후 리튬 회수의 최저 할당량이 설정되어 있습니다. 핀란드, 프랑스, 포르투갈에서는 2027년까지 여러 그린필드 전환 플랜트가 가동을 시작할 예정이며, 수산화리튬 시장공급 기반에 다양성이 더해지고 있습니다. 특히 중국이 기술 수출 규제안을 실시한 경우 전략적 자치를 추진하는 권역은 무역의 흐름을 재조합할 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전기자동차 수요 증가

- 전동 공구 수요 증가

- 직접 리튬 추출(DLE)의 상용화, 저가 수산화물 공급 원료 확보

- OEM 지원 장기 계약으로 라틴 아메리카에서 새로운 수산화물 용량 위험 감소

- 배터리 공급망을 지원하는 정부 정책

- 시장 성장 억제요인

- 높은 생산 비용

- 프로젝트 자금 조달을 방해하는 원료 가격 변동

- 독성에 대한 우려 증가

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(수량 및 금액)

- 용도별

- 리튬 이온 배터리

- 윤활 그리스

- 정제

- 기타 용도(폴리머?특수화학 합성)

- 최종 이용 산업별

- 자동차

- 소비자 가전 제품

- 에너지 저장 시스템

- 기타(산업기계 및 오프로드 기계)

- 등급별

- 배터리 등급(56.5% 이상의 LiOH*H2O)

- 기술 등급

- 공업용 등급

- 형태별

- 일수화물

- 무수

- 지역별

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Albemarle Corporation

- Arcadium Lithium

- Chengxin Lithium

- Ganfeng Lithium Group Co. Ltd.

- IGO Limited

- LevertonHELM Limited

- Nemaska Lithium(Investissement Quebec)

- Piedmont Lithium Inc.

- Shandong Ruifu Lithium Co., Ltd.

- Sinomine Resource Group

- SQM SA

- Tianqi Lithium Corporation

- Yahua Industrial Group Co.

제7장 시장 기회와 장래의 전망

SHW 25.11.19The Lithium Hydroxide Market size is estimated at 229.30 LCE kilotons in 2025, and is expected to reach 697.55 LCE kilotons by 2030, at a CAGR of 23.5% during the forecast period (2025-2030).

Intensifying competition for battery-grade chemicals, fast-rising electric vehicle (EV) sales, and the rapid scale-up of direct lithium extraction (DLE) technologies are reshaping supply networks worldwide. Asia-Pacific commands the largest regional position with 40% of global consumption, delivering the fastest growth rate of 27.66% through 2030. Automakers locked in long-term procurement contracts in 2024 to secure high-purity feedstock, and several battery manufacturers accelerated vertical-integration strategies to hedge price swings. At the same time, stark feedstock price volatility-from USD 81,500/t to USD 22,500/t during 2023-continues to challenge project finance models.

Global Lithium Hydroxide Market Trends and Insights

Increasing Demand for Power Tools

Cordless power tools are replacing corded alternatives in construction and industrial maintenance because lithium-ion packs deliver longer run-time and a superior power-to-weight ratio. Manufacturers have launched cell formats optimized for high-discharge cycles, a profile that favors lithium hydroxide-rich nickel-cobalt-manganese cathodes. Uptake is strongest among professional contractors in North America and Europe, where tight labor markets place a premium on productivity gains. Continuous adoption of building-information-modeling workflows further accelerates cordless tool penetration because crews require untethered mobility on-site. Though smaller than EV demand, this niche yields above-average price realization for hydroxide producers supplying specialty cathode blends.

Commercialization of Direct Lithium Extraction (DLE) Unlocking Low-Cost Feedstock

Field-scale success at IBAT's Utah plant, utilizing modular adsorption columns, demonstrated 80-90% lithium recovery in hours versus the months needed for conventional pond evaporation. Project ATLiS in California secured a USD 1.36 billion conditional loan guarantee to deliver 20,000 t/y of lithium hydroxide from geothermal brine, affirming lender confidence in DLE scalability. Higher yields cut capital intensity per ton and enable operations in water-stressed regions because many ion-exchange and membrane variants consume less make-up water than pond systems. These economics bolster the long-run supply outlook for the lithium hydroxide market while reducing environmental footprints.

High Production Costs

Battery-grade lithium hydroxide plants demand sophisticated impurity control and costly crystallization circuits. Albemarle halted expansion of its Kemerton facility in Australia, slicing planned nameplate capacity in half and reducing onsite headcount by 40%. Multiyear payback periods, strict environmental licensing, and a limited pool of hydro-metallurgical talent maintain high entry barriers and slow new-build momentum, especially in regions with elevated energy tariffs.

Other drivers and restraints analyzed in the detailed report include:

- OEM-Backed Long-Term Contracts De-Risking New Capacity in Latin America

- Government Policies Supporting Battery Supply Chains

- Feedstock Price Volatility Hindering Project Financing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion batteries generated 63% of 2024 demand and are forecast to expand at 26.77% CAGR through 2030. This segment alone accounts for the largest slice of the lithium hydroxide market size and delivers the highest incremental tonnage. Range-oriented chemistries such as nickel-cobalt-manganese (NCM) and nickel-cobalt-aluminum (NCA) require lithium hydroxide for synthesis rather than carbonate, anchoring structural demand. In contrast, lubricating greases, purified-air systems, and specialty synthesis remain steady but modest contributors. Growing recycling mandates in the European Union are expected to generate a secondary supply channel later in the forecast period, tempering but not displacing primary demand.

Energy storage deployments form the fastest-rising sub-application. Large-scale battery farms linked to renewable assets need long cycle-life chemistries. Projects such as California's multi-gigawatt-hour installations increasingly specify nickel-rich cathodes, reinforcing hydroxide consumption. As costs decline, smaller commercial and industrial behind-the-meter systems join the opportunity set, ensuring the lithium hydroxide market retains a diversified growth engine across stationary and mobile domains.

Battery-grade material held a commanding 70% share in 2024 and posts a forecast 25.55% CAGR, the highest within this segmentation. Stringent impurity controls on sodium, calcium, and heavy metals underpin price differentials over technical grade. Manufacturers such as Livent have invested in additional recrystallization and ion-exchange modules to achieve less than 100 ppm aggregate impurity limits. That investment raises capital intensity but also deepens competitive moats. Technical grade serves grease and ceramic markets where tolerance thresholds are looser, while industrial grade addresses water treatment and select synthesis routes.

The lithium hydroxide market share for battery-grade will keep rising as OEM specification sheets lengthen. Next-generation solid-state and high-silicon-anode designs rely on precise stoichiometry and ultra-low moisture content, factors that amplify quality premiums. Producers with vertically integrated brine or hard-rock feedstock plus in-house purification are best placed to capture this margin pool.

The Lithium Hydroxide Market Report is Segmented by Application (Lithium-Ion Batteries, Lubricating Grease, and More), End-Use Industry (Automotive, Consumer Electronics, and More), Grade (Battery Grade, Technical Grade, and Industrial Grade), Form (Monohydrate and Anhydrous), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific, with a 40% lithium hydroxide market share in 2024, benefits from unrivaled cell-manufacturing capacity and a dense cluster of downstream cathode, anode, and pack assemblers. Chinese policy directives now favor domestic sourcing, prompting active development of inland salt-lake brine as well as overseas equity stakes, while Japan and South Korea leverage long-standing material science expertise to stay competitive. India entered the fray with a National Manufacturing Mission and duty exemptions for critical minerals under the 2025-26 Union Budget, stimulating local hydroxide conversion proposals.

North America's expansion rests on large-scale funding packages. The DOE's USD 150 million grant to Albemarle supports a spodumene concentrator at Kings Mountain capable of feeding 1.6 million EVs annually. Hyundai Motor Group and SK On approved a USD 5 billion battery cell plant in Georgia, anchoring regional cathode demand for locally produced hydroxide. These initiatives aim to cut reliance on Asian supply chains and meet US Inflation Reduction Act sourcing thresholds.

South America remains the primary feedstock hub. Chile's National Lithium Strategy invites private participation while safeguarding state oversight, and new geological surveys lifted estimated reserves by 28%. Argentina attracted Rio Tinto's USD 2.5 billion mine investment and multiple OEM offtakes. Brazil saw EV sales jump 85% in 2024, led by BYD with 70% share, hinting at future domestic hydroxide conversion requirements.

Europe accelerates capacity with stringent CO2 regulations and comprehensive recycling mandates. Germany spearheads R&D on next-generation cathodes, while the EU Battery Regulation sets minimum lithium recovery quotas from 2025 onward. Several greenfield conversion plants in Finland, France, and Portugal are scheduled for commissioning by 2027, adding diversity to the lithium hydroxide market supply base. The bloc's push for strategic autonomy may reshape trade flows, especially if China enacts proposed technology export restrictions.

- Albemarle Corporation

- Arcadium Lithium

- Chengxin Lithium

- Ganfeng Lithium Group Co. Ltd.

- IGO Limited

- LevertonHELM Limited

- Nemaska Lithium (Investissement Quebec)

- Piedmont Lithium Inc.

- Shandong Ruifu Lithium Co., Ltd.

- Sinomine Resource Group

- SQM S.A.

- Tianqi Lithium Corporation

- Yahua Industrial Group Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Electric Vehicles

- 4.2.2 Increasing Demand for Power Tools

- 4.2.3 Commercialisation of Direct Lithium Extraction (DLE) Unlocking Low-Cost Hydroxide Feedstock

- 4.2.4 OEM-Backed Long-Term Contracts De-Risking New Hydroxide Capacity in Latin America

- 4.2.5 Government Policies Supporting Battery Supply Chains

- 4.3 Market Restraints

- 4.3.1 High Production Costs

- 4.3.2 Feedstock Price Volatility Hindering Project Financing

- 4.3.3 Rising concern About the Toxicity

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume and Value)

- 5.1 By Application

- 5.1.1 Lithium-ion Batteries

- 5.1.2 Lubricating Greases

- 5.1.3 Purification

- 5.1.4 Other Application (Polymer and Specialty Chemical Synthesis)

- 5.2 By End-use Industry

- 5.2.1 Automotive

- 5.2.2 Consumer Electronics

- 5.2.3 Energy Storage Systems

- 5.2.4 Others (Industrial and Off-Road Machinery)

- 5.3 By Grade

- 5.3.1 Battery Grade (Greater than or equal to 56.5% LiOH*H2O)

- 5.3.2 Technical Grade

- 5.3.3 Industrial Grade

- 5.4 By Form

- 5.4.1 Monohydrate

- 5.4.2 Anhydrous

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 South Korea

- 5.5.1.4 India

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Albemarle Corporation

- 6.4.2 Arcadium Lithium

- 6.4.3 Chengxin Lithium

- 6.4.4 Ganfeng Lithium Group Co. Ltd.

- 6.4.5 IGO Limited

- 6.4.6 LevertonHELM Limited

- 6.4.7 Nemaska Lithium (Investissement Quebec)

- 6.4.8 Piedmont Lithium Inc.

- 6.4.9 Shandong Ruifu Lithium Co., Ltd.

- 6.4.10 Sinomine Resource Group

- 6.4.11 SQM S.A.

- 6.4.12 Tianqi Lithium Corporation

- 6.4.13 Yahua Industrial Group Co.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Rising Demand for Portable Electronic Devices