|

시장보고서

상품코드

1852203

미용 레이저 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Aesthetic Lasers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

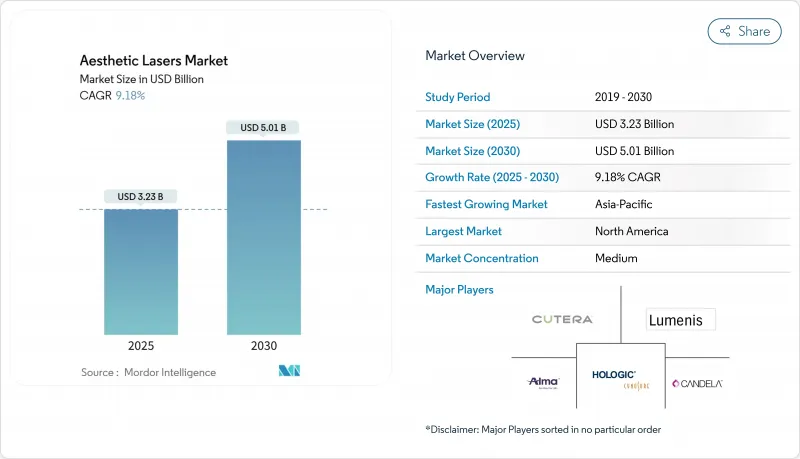

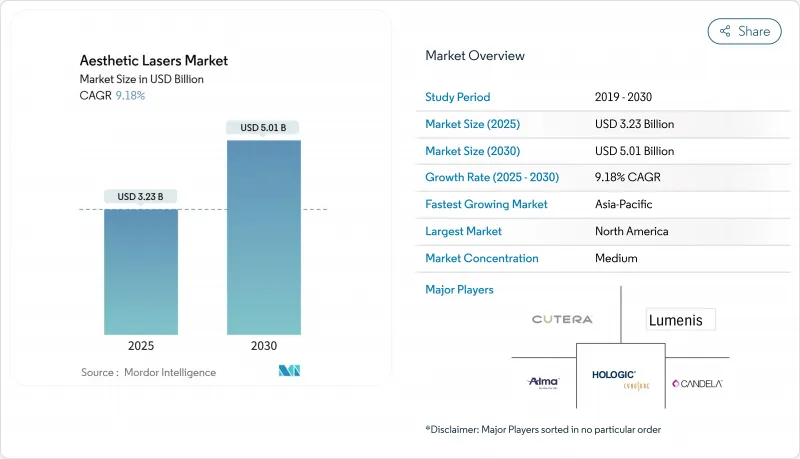

세계의 미용 레이저 시장 규모는 2025년에 32억 3,000만 달러로 평가되었고, 2030년까지의 CAGR은 9.18%를 나타낼 전망입니다.

제한된 회복 기간으로 가시적인 결과를 제공하는 최소 침습적 미용 시술에 대한 소비자 수요 증가가 피부과 진료 현장의 자본 장비 구매 기준을 지속적으로 재정의하고 있습니다. 동일한 성장 동력에서 파생된 추가적 함의는, 시술자의 학습 곡선을 단축시킬 수 있는 장비 공급업체들이 이제 임상적 효능과만 연관되던 가격 프리미엄을 요구할 수 있게 되었다는 점입니다.

세계의 미용 레이저 시장 동향 및 인사이트

정밀 표적 치료를 주도하는 고령화 인구 구조

급속히 확대되는 65세 이상 인구 집단은 이제 레이저 타이트닝을 통한 피부 이완 교정을 우선시하며, 외래 치료로 수술적 안면 리프트를 대체하고 있습니다. 노년층 진피는 회복 속도가 더 느리기 때문에, 장비 제조사들은 과도한 치료 위험을 완화하기 위해 더 정밀한 에너지 증분 설정과 폐쇄 루프 온도 피드백을 통합하고 있습니다. 이러한 프로토콜을 허영심 충족이 아닌 “활력 유지”로 포지셔닝하는 클리닉은 이동성과 회복 시간에 깊은 관심을 가진 고령 환자들 사이에서 더 높은 수용도를 보이고 있습니다.

기술 융합이 혁신의 사이클을 가속화

제조사들은 단일 섀시에 다중 파장과 고주파 채널을 통합하여 4-5대의 독립형 장비를 하나로 압축하고 있습니다. 이로 인해 단일 모드 장비의 성능이 부족해 보이며 교체 주기가 단축되는 직접적 결과가 발생하지만, 부수적 효과로 하드웨어 셸이 아닌 소프트웨어 업그레이드 가능성이 진정한 락인 메커니즘으로 부상하고 있습니다. 알마 하이브리드의 CO2 레이저와 1570nm 레이저 조합은 미래 경쟁 우위가 광원 자체보다 펌웨어 업데이트로 제어되는 치료 알고리즘으로 전환될 수 있음을 보여줍니다.

제한된 보험 적용이 시장 계층화를 초래

주사비와 여드름 레이저 치료는 여전히 선택적 치료로 분류되며, 유나이티드헬스케어의 의료 정책은 이를 “의학적으로 필요하지 않음”으로 규정합니다. 결과적으로 고소득 도시 거주자들이 프리미엄 클리닉 수익을 주도하는 반면, 중저가 시장 제공업체들은 접근성 확대를 위해 창의적인 금융 상품이나 세션당 결제 방식을 활용합니다. 이러한 계층화는 플래그십 시스템 구매 자금이 부족한 신흥 시장 기업가를 대상으로 한 저비용 휴대용 장치의 틈새 시장을 열어줍니다.

부문 분석

비절제형 시스템은 일상생활에 지장을 주지 않는 치료에 대한 소비자 요구에 힘입어 2024년 미용 레이저 시장 규모에서 65%의 점유율을 차지했습니다. 분할 툴륨 파이버 레이저가 아시아계 광노화 사례에서 표피 두께를 개선한다는 증거는 인종 간 적용 가능성을 입증합니다. 이러한 우위는 또한 클리닉들이 회복 기간 없는 결과를 강조하기 위해 마케팅 예산의 불균형적인 비중을 할당할 수 있음을 시사하며, 경쟁 논의를 단일 세션 효능에서 누적적 피부 질 개선으로 미묘하게 전환시키고 있습니다.

2024년 독립형 레이저가 72% 점유율을 유지했으나, 멀티플랫폼 하이브리드 제품은 13.5%의 연평균 복합 성장률(CAGR)을 기록 중입니다. 이는 금융사들이 곧 감가상각 일정을 재조정하여 멀티플랫폼 장비를 기존 자본재보다 소프트웨어 업그레이드가 가능한 자산으로 취급할 수 있음을 시사합니다. 경제적 수명 연장은 리스 모델의 매력을 높여 임대사와 제조사 모두에게 반복적 수익 흐름을 창출합니다.

지역 분석

북미는 강력한 공급자 네트워크와 조기 기술 도입에 힘입어 2024년 글로벌 시장 점유율의 40%를 차지했습니다. 미국의 최소 침습적 ‘트윅먼트(tweakment)’ 시술 시장 규모는 의료진이 극적인 변신보다는 점진적 교정에 중점을 둔다는 점을 보여줍니다. 이와 유사하게 주요 대도시 지역 환자들의 기대는 점차 주사제와 부분적 박리 레이저를 결합한 시너지 프로토콜 중심으로 변화하고 있어, 통합 진료에 대한 교차 판매 기회를 시사합니다.

아시아태평양 지역은 2030년까지 연평균 12.2%의 성장률(CAGR)을 기록할 것으로 전망되며, 이는 전 세계에서 가장 빠른 속도다. 균일한 피부톤을 문화적 이상으로 강조하는 국가들은 피코초 및 나노초 색소 레이저의 평균 이상의 도입률을 이끌고 있습니다. 기미와 혈관성 홍반 모두를 치료할 수 있는 장비를 보유한 클리닉은 시장 점유율을 확보할 수 있을 전망입니다. 시술 가격 경쟁이 치열한 시장에서 이중 적응증의 다용도성은 자본 투자 회수 속도를 높이기 때문입니다.

유럽은 성숙하면서도 확장 중인 시장으로, 자연스러운 결과에 대한 선호로 인해 여러 세션에 걸쳐 저에너지 패스를 병행하는 프로토콜이 선호됩니다. 이는 특히 입소문 추천이 큰 비중을 차지하는 독일, 프랑스, 영국에서 많은 클리닉의 주요 수익 창출 수단이 신규 환자 유치보다 기존 환자 유지가 될 수 있음을 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화 인구 및 피부 이완 증가로 인한 레이저 타이트닝 수요 증가

- 기술 발전 가속화

- AI 기반 레이저 파라미터 최적화로 부작용 감소

- 밀레니얼 세대를 중심으로 색소 병변 치료용 피코초 레이저 채택 증가

- 의료 관광 주도 레이저 제모 붐

- 라이프 스타일의 변화와 가처분 소득 증가

- 시장 성장 억제요인

- 공공 의료 시스템 내 제한된 보험 적용

- 제품 출시 지연을 초래하는 엄격한 레이저 안전 규정

- 미용 시술과 관련된 사회적 낙인

- 신신흥국에서의 훈련된 레이저 기술자 부족

- 공급망 분석

- 규제 시나리오

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유형별

- 절제 레이저

- 이산화탄소(CO2) 레이저

- 에르븀 레이저

- 비절제 레이저

- 펄스 색소 레이저(PDL)

- Nd : YAG 레이저

- 알렉산드라이트 레이저

- 다이오드 레이저

- 절제 레이저

- 모달리티별

- 독립형 레이저 시스템

- 멀티 플랫폼/하이브리드 시스템

- 휴대성별

- 비 휴대용

- 휴대용

- 용도별

- 피부 재생 및 리쥬베네이션

- 탈모

- 여드름 및 흉터 치료

- 문신 제거

- 바디 스컬프팅 & 스킨 타이트닝

- 혈관 및 색소성 병변 치료제

- 최종 사용자별

- 병원

- 피부과 & 미용 클리닉

- 메디컬 스파 & 뷰티 센터

- 외래수술센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동

- GCC

- 남아프리카

- 기타 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Alma Lasers

- Candela Medical

- Cynosure

- Lumenis

- Cutera

- Solta Medical

- Aerolase Corporation

- Sciton Inc.

- El.En. Group

- IRIDEX Corporation

- sharplight technologies

- Fotona doo

- Jeisys Medical

- Lutronic Corporation

- Venus Concept Inc.

- InMode Ltd.

- Quanta System SpA

- Zimmer MedizinSysteme

- BTL Industries

제7장 시장 기회와 장래의 전망

HBR 25.11.27The global aesthetic lasers market was valued at USD 3.23 billion in 2025 and is projected to advance at a 9.18% CAGR through 2030.

Rising consumer demand for minimally invasive cosmetic interventions that deliver visible results with limited downtime continues to redefine capital-equipment purchase criteria among dermatology practices. An additional implication, derived from the same growth dynamic, is that equipment vendors able to shorten practitioner learning curves may now command pricing premiums that were previously associated only with clinical efficacy.

Global Aesthetic Lasers Market Trends and Insights

Aging Demographics Driving Precision-Targeted Treatments

A rapidly expanding 65-plus cohort now prioritizes skin laxity correction through laser tightening, substituting surgical facelifts with outpatient regimens. Because geriatric dermis heals more slowly, device makers are integrating finer energy-increment settings and closed-loop temperature feedback to mitigate overtreatment risk . Clinics that position these protocols as "maintenance of vitality" rather than vanity appeal find higher acceptance among older patients intimately concerned with mobility and recovery time.

Technological Convergence Accelerates Innovation Cycles

Makers are stacking multiple wavelengths and radiofrequency channels into single chassis, effectively collapsing four or five standalone devices into one. The direct result is shorter replacement cycles as single-modality workhorses appear under-spec'd, but the secondary effect is that software upgradability becomes the real lock-in mechanism, not the hardware shell. Alma Hybrid's CO2 + 1570 nm pairing illustrates how future competitive advantage may pivot from light sources to treatment algorithms controlled by firmware updates.

Limited Reimbursement Creates Market Stratification

Laser treatment for rosacea and acne remains widely classified as elective, with UnitedHealthcare's medical policy deeming it "not medically necessary" . Consequently, high-income urban dwellers propel premium clinic revenues, while mid-market providers rely on creative financing or pay-per-session plans to broaden access. The stratification opens a niche for low-cost portable units targeting emerging-market entrepreneurs who lack capital for flagship systems.

Other drivers and restraints analyzed in the detailed report include:

- Picosecond Technology Transforms Millennial Aesthetic Priorities

- Medical Tourism Reshapes Global Treatment Distribution

- Regulatory Complexity Delays Innovation Commercialization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-ablative systems held 65 % market share of the aesthetic lasers market size in 2024, propelled by consumer insistence on treatments that do not interfere with daily routines. Evidence showing that fractional thulium fiber lasers improve epidermal thickness in Asian photodamage cases underscores their cross-ethnic applicability. This dominance also implies that clinics may allocate a disproportionate share of marketing budgets to highlight downtime-free outcomes, subtly shifting competitive discourse away from single-session efficacy toward cumulative skin-quality upgrades.

Standalone lasers retained 72 % share in 2024, yet multiplatform hybrids are posting a 13.5 % CAGR. The embedded inference is that financing companies could soon recalibrate depreciation schedules, treating multiplatform units more like software-upgradable assets than conventional capital equipment. Longer economic life increases the appeal of leasing models, creating recurring-revenue streams for both lessors and manufacturers.

The Aesthetic Laser Market Report Segments the Industry Into by Type (Ablative Laser, Non-Ablative Laser), by Modality (Standalone Laser Systems, and More), by Portability (Non-Portable and Portable), by Application (Skin Resurfacing/Skin Rejuvenation, Hair Removal, and More), End-User (Hospitals, Ambulatory Surgical Centers, and More), and by Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 40% of global market share in 2024, supported by robust provider networks and early technology adoption. The market size of U.S. minimally invasive "tweakment" procedures reinforces the importance practitioners place on incremental corrections rather than dramatic makeovers. A parallel observation is that patient expectations in major metropolitan areas increasingly revolve around synergistic protocols combining injectables with sub-ablative lasers, suggesting cross-selling opportunities for integrated practices.

Asia-Pacific is forecast to register 12.2% CAGR through 2030, the fastest pace of any region. Countries emphasizing even skin tone as a cultural ideal drive above-average adoption of picosecond and nano-second pigment lasers. Clinics that stock devices capable of addressing both melasma and vascular redness stand to capture share, because dual-indication versatility defrays capital investment more quickly in markets where procedure pricing is tightly competitive.

Europe remains a mature yet expanding market, where preference for natural-appearing outcomes encourages protocols that blend low-energy passes over multiple sessions. An indirect implication is that patient retention may supersede new-patient acquisition as the primary revenue lever for many clinics, particularly in Germany, France, and the UK where word-of-mouth referrals carry considerable weight.

- Alma Lasers

- Candela Medical

- Cynosure

- Lumenis

- Cutera

- Solta Medical

- Aerolase

- Sciton

- El.En.

- Iridex

- sharplight technologies

- Fotona d.o.o.

- Jeisys Medical

- Lutronic

- Venus Concept Inc.

- InMode Ltd.

- Quanta System S.p.A.

- Zimmer MedizinSysteme

- BTL

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population & Rise in Skin-Laxity-Driven Laser Tightening

- 4.2.2 Growing Technological Advancements

- 4.2.3 AI-Enabled Laser Parameter Optimization Reducing Adverse Events

- 4.2.4 Uptake of Picosecond Lasers for Pigmented Lesions Among Millennials

- 4.2.5 Medical-Tourism-Led Boom in Laser Hair Removal

- 4.2.6 Changing Lifestyle and Growing Disposable Income

- 4.3 Market Restraints

- 4.3.1 Limited Reimbursement in Public Healthcare Systems

- 4.3.2 Stringent Laser Safety Regulations Delaying Product Launches

- 4.3.3 Social Stigma Associated With Cosmetic Treatments

- 4.3.4 Shortage of Trained Laser Technicians in Emerging Nations

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Scenario

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Ablative Lasers

- 5.1.1.1 Carbon Dioxide (CO2) Laser

- 5.1.1.2 Erbium Laser

- 5.1.2 Non-Ablative Lasers

- 5.1.2.1 Pulsed-Dye Laser (PDL)

- 5.1.2.2 Nd:YAG Laser

- 5.1.2.3 Alexandrite Laser|

- 5.1.2.4 Diode Laser

- 5.1.1 Ablative Lasers

- 5.2 By Modality

- 5.2.1 Standalone Laser Systems

- 5.2.2 Multiplatform / Hybrid Systems

- 5.3 By Portability

- 5.3.1 Non-Portable

- 5.3.2 Portable

- 5.4 By Application

- 5.4.1 Skin Resurfacing & Rejuvenation

- 5.4.2 Hair Removal

- 5.4.3 Acne & Scar Management

- 5.4.4 Tattoo Removal

- 5.4.5 Body Sculpting & Skin Tightening

- 5.4.6 Vascular & Pigmented Lesion Treatmen

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Dermatology & Aesthetic Clinics

- 5.5.3 Medical Spas & Beauty Centres

- 5.5.4 Ambulatory Surgical Centres

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 GCC

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Alma Lasers

- 6.4.2 Candela Medical

- 6.4.3 Cynosure

- 6.4.4 Lumenis

- 6.4.5 Cutera

- 6.4.6 Solta Medical

- 6.4.7 Aerolase Corporation

- 6.4.8 Sciton Inc.

- 6.4.9 El.En. Group

- 6.4.10 IRIDEX Corporation

- 6.4.11 sharplight technologies

- 6.4.12 Fotona d.o.o.

- 6.4.13 Jeisys Medical

- 6.4.14 Lutronic Corporation

- 6.4.15 Venus Concept Inc.

- 6.4.16 InMode Ltd.

- 6.4.17 Quanta System S.p.A.

- 6.4.18 Zimmer MedizinSysteme

- 6.4.19 BTL Industries

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment