|

시장보고서

상품코드

1910648

황반변성(AMD) 치료 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Macular Degeneration Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

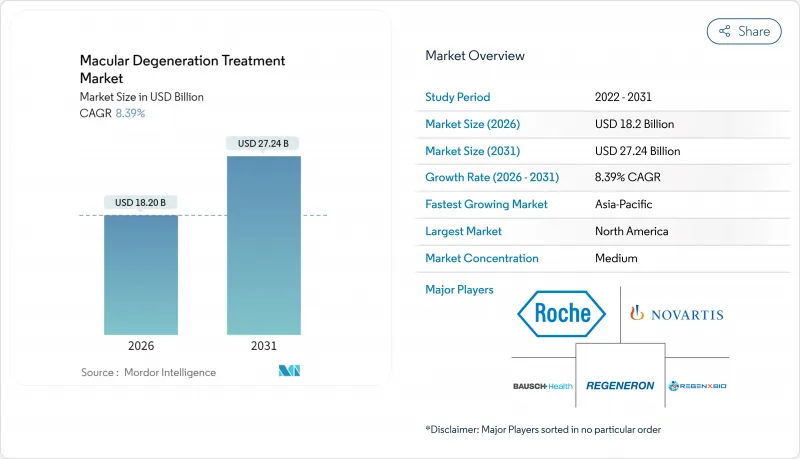

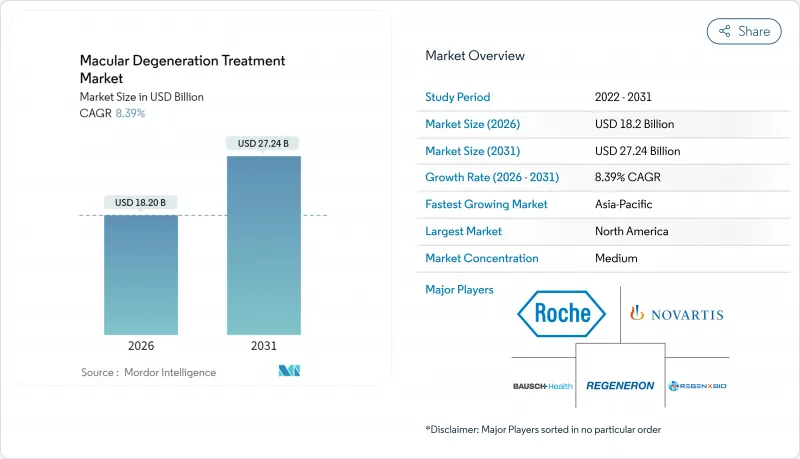

2026년 황반변성 치료 시장의 규모는 182억 달러로 추정되며, 2025년 167억 9,000만 달러에서 성장할 전망입니다.

2031년에는 272억 4,000만 달러에 이르고, 2026년부터 2031년에 걸쳐 CAGR 8.39%로 확대될 전망입니다.

이 전망은 인구 고령화, 획기적인 의약품에 대한 규제 측면의 지원, 기존 안과 진료 경로보다 조기에 질병을 확인하는 디지털 진단 기술의 급속한 보급을 반영합니다. 황반변성(AMD)의 유병률이 인구 증가율보다 25% 빠르게 상승하고 있지만, AI 기반 스크리닝 알고리즘이 94%의 감도와 99%의 특이도를 달성하여 지리적 위축형에 대한 치료 옵션을 여는 보체 경로 억제제로의 전환이 진행되고 있는 점이 수요 증가를 더욱 추진하고 있습니다. 후기 임상시험 단계에 있는 유전자 및 세포요법, 지속방출형 전달 플랫폼, 바이오시밀러의 경쟁이 수익 구조를 재구축하는 한편, 지불 기관은 생물학적 제제 비용 억제를 위해 이용 관리를 강화하고 있습니다. 지역별로 미국은 FDA의 획기적인 치료법 채널을 활용하여 신규 치료에 대한 선행 접근성을 유지하는 한편, 아시아태평양에서는 환급 범위의 확대 가속과 대규모 노인층이 가장 빠른 수량 성장을 지원하고 있습니다.

세계의 황반변성 치료 시장의 동향 및 인사이트

노화 안구 질환의 유병률 상승

황반변성(AMD)의 유병률은 장시간의 화면 시청, 불균형적인 영양 식사, 도시 지역의 대기 오염 악화 등 생활 습관 요인이 유전적 리스크를 복합적으로 작용시킴으로써 기초적인 고령화 동향을 25% 웃도는 속도로 증가하고 있습니다. WHO는 2030년까지 2억 8,800만명이 AMD를 앓을 것으로 예측하고 있으며, 이로써 의료 시스템은 조기 발견 프로토콜로 이행하고, 클리닉 기반 스크리닝과 비교하여 치료 대상 인구는 40% 확대될 전망입니다. 치료되지 않은 AMD는 이미 전 세계적으로 3,430억 달러의 생산성 손실과 의료비를 발생시키고 있으며, 보험사는 정기적인 영상 진단 및 영양 지원을 포함한 예방적 치료 계획을 권장하고 있습니다. 성숙한 진단 네트워크를 보유한 나라에서는 AI를 활용한 스크리닝이 급속히 보급되어 1차 진료 시설이나 약국에까지 도입됨으로써 환자가 보다 조기에 치료 프로세스로 이행하는 효과적인 경로가 구축되고 있습니다. 제약 기업은 적극적인 치료 모델에 적합하고 클리닉의 혼잡을 줄이는 지속성 임플란트의 개발로 이에 대응하고 있습니다.

세계 노인 인구의 급성장

2030년까지 65세 이상의 인구는 세계 인구의 16.5%를 차지할 전망이며, 진행성 황반변성(AMD)의 위험이 가장 높은 85세 이상 층은 고령자 전체 증가율의 2배의 속도로 확대하고 있습니다. 일본과 한국을 중심으로 한 아시아태평양 국가에서는 전문의의 부족을 초래하여 원격 안과 진료의 도입을 가속화하는 미충족 수요에 직면하고 있습니다. 노인 환자는 종종 당뇨병 및 고혈압과 같은 병존 질환을 앓고 있으며, 항-VEGF 주사 요법을 복잡하게 하고 보다 엄격한 안전 모니터링이 필요합니다. 미국 메디케어의 항-VEGF 치료 지출은 2014년 25억 1,000만 달러에서 2019년 40억 2,000만 달러로 증가했습니다. 비용이 적게 드는 옵션이 없으면 2030년까지 두 배로 더 늘어날 것으로 예측됩니다. 이에 따라 각국 정부는 의료 체제의 병목 현상을 완화하고 예산의 급증을 억제하기 위해 자기 투여 가능한 약제나 재택 모니터링 기기의 도입을 추진하고 있습니다.

생물학적 제형 및 유전자 치료의 높은 비용

주요 항-VEGF 주사제는 1회당 1,850-2,000달러로, 연간 6-8회의 표준 투여 스케줄에서는 진단비나 의사 보상을 제외해도 1만 5,000달러를 초과할 수 있습니다. 개발 중인 단일 투여형 유전자 치료는 한눈에 20만-50만 달러를 필요로 할 수 있으며, 평생 비용 절감 효과가 예상됨에도 불구하고 지불자 측의 엄격한 감시를 초래하고 있습니다. 2024년에 출시된 아플리베르셉트 바이오시밀러는 정가보다 15-30% 저렴하지만, 전환 관성이나 제품 고유의 안전성 데이터의 부족이 급속한 보급을 억제하고 있습니다. 지불기관은 단계적 치료 규정, 치료 장소의 제한, 시력 지속성에 기초한 환급을 조건으로 하는 성과 연동형 계약의 시험 도입 등으로 대응하고 있습니다. 이러한 접근 장벽은 고가치 치료법의 단기적인 보급을 억제하고 황반변성 치료 시장의 CAGR을 약 2% 하락시킬 가능성이 있습니다.

부문 분석

습성 AMD가 2025년 매출액의 64.62%를 차지하였으며 이러한 지배적 지위는 항VEGF 요법의 정착을 나타내고 있지만, 바이오시밀러에 의한 가격 및 판매 수량 점유율의 침식에 의해 성장 둔화가 현저합니다. 이러한 동향 변화는 건성 AMD 부문에 유리하게 작용하여 SYFOVRE 및 IZERVAY의 승인에 의해 지리적 위축형에 대한 최초의 약리학적 치료 옵션이 발생하여 병변 확대를 최대 35% 억제했습니다. 건성 AMD는 실임상 데이터에 의한 안전성의 실증에 수반해, 보험 지불자에 의한 도입이 가속하고 10.21%의 연평균 복합 성장률(CAGR)로 추이할 전망입니다. 이로 인해 황반변성 치료 시장 전체의 포트폴리오 우선순위가 재구성되었습니다. 유전자 치료 연구자들은 전체 AMD 증례의 약 85%를 차지하는 환자층과 평생 주사를 피할 수 있는 가능성을 지닌 일회 치료 제공 기회에 주목하여 건성 AMD에 특히 주력하고 있습니다.

현재 경쟁적인 투자는 보체 조절과 광수용체 보호에 치우치고 있어 2027년까지 여러 작용기전으로 제III상 시험 결과가 발표될 전망입니다. 주요 기존 기업은 고용량 아플리베르셉트와 VEGF/Ang-2 복합 억제에 의해 습성 AMD의 점유율 저하를 막고 있지만, 전략적 자본은 인수 및 공동 개발 계약을 통해 건성 AMD 자산으로 점점 이동하고 있습니다. 상업 분석가는 건성 AMD 부문 채택이 현재 속도를 유지하면 2029년까지 습성 및 건성 수익 라인이 수렴할 것으로 예측하고 있으며, 이 이정표는 황반변성 치료 업계 전체의 평가 지표를 재조정할 것입니다.

2025년 황반변성 치료 시장 규모에서 초기 단계 AMD가 71.58%를 차지했습니다. 이는 클라우드 연결형 안저 카메라의 진단이 1차 치료, 검안, 지역 약국 채널로 확대된 것을 반영하고 있습니다. 안과계는 신규 진단 환자에게 AREDS에 기초한 보충 섭취와 생활 습관 개선을 권장하고 있으며, 이는 영양 보조 식품 제조업체나 원격 모니터링 벤더를 지원하는 예방 의료 경제의 기반이 되고 있습니다. 중간기 AMD는 2031년까지 10.78%라는 가장 빠른 부문 CAGR을 나타낼 전망입니다. 이는 보체 억제제가 병변의 성장 억제 효과를 나타내고 환자의 "기능적 시력 기간"을 연장하기 때문입니다. 상업 광고는 시력 회복보다 진행 방지를 강조하고 지불자의 관심과 사회적 비용 회피를 일치시킵니다.

후기 AMD는 반복적인 주사 일정과 보조기구에 대한 수요로 인해 여전히 환자 1인당 수익이 가장 높은 단계입니다. 그러나 지속 방출 임플란트와 유전자 치료는 진찰 횟수를 줄이고 기존의 종량제 비즈니스 모델을 변화시킬 수 있습니다. 실시간 재택 OCT 장치는 트리아지를 효율화하고 악화된 눈만을 신속하게 치료하기 위해 클리닉으로 유도함으로써 진료 자원을 절약하고 황반변성 치료 시장 전체에서 정밀의료를 추진합니다.

지역별 분석

북미는 2025년 수익의 41.88%를 차지하였으며 메디케어 환급제도와 세계 최고 밀도의 안과 전문의 인력이라는 두 가지 원동력에 뒷받침되고 있습니다. FDA의 우선 심사 및 획기적인 치료법 지정 제도는 2025년 3월에 승인된 MacTel 치료제 ENCELTO와 같은 일등급 제품의 출시를 가속화하고 있습니다. 그러나 2024년에 실시된 메디케어 보상 5.4% 삭감은 의료기관의 이익률을 압박하여 망막진료의 통합과 비용 효율적인 바이오시밀러 도입을 촉진하고 있습니다. 지방의 접근성 격차는 여전히 존재하고 AI 평가 화상을 도시로 송신하는 주 주도의 원격 안과 진료 파일럿 사업이 추진되고 있습니다.

유럽은 두 번째로 큰 시장 규모를 보유하지만, 의료 기술 평가의 지역 간 차이에 직면하고 있습니다. 2024년 유럽 의약품청(EMA)의 SYFOVRE 승인 거부는 미국 규제 당국과의 견해 차이를 드러내고 주요 시장에서 접근 지연을 초래하고 있습니다. 독일과 영국은 견고한 보험 제도와 강력한 임상 네트워크를 배경으로 선진 의료 도입을 주도하고 있습니다. 반면 지중해 국가들은 예산 상한으로 인해 약품 목록에 통합이 지연되어 도입이 늦어지고 있습니다. EU에서는 고령화가 진행되고(65세 이상이 인구의 20% 이상) 수요가 확대되는 반면 호라이즌 2030 조성금이 지역 바이오텍 기업에 연구개발 자금을 투입하여 파이프라인의 활력을 유지하고 있습니다.

아시아태평양은 CAGR 9.41%로 가장 빠르게 성장할 것으로 예상되는 시장입니다. 2030년까지 2억 6,000만 명에 이를 전망인 중국의 고령자층이 거대한 수요를 낳지만, 전문의의 부족과 보험 제도의 불균일성이 즉각적인 보급을 억제하고 있습니다. 일본의 초고령사회는 전국민 보험제도 하에서 첨단 치료의 도입을 극대화하고 유전자 치료 전개의 발판으로서 동국을 자리매김하고 있습니다. 인도는 AI 탑재 스마트폰에 의한 안저 화상 진단을 활용해 안과의 부족 지역에서의 접근성을 확대하여 조기 단계의 환자층을 개척하고 있습니다. 호주와 한국은 충실한 환급제도와 임상시험 참여를 결합하여 지역 승인 프로세스를 가속화하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 노화성 안질환의 유병률 상승

- 세계 노인 인구의 급속한 증가

- 안과용 약물 전달 기술의 기술적 진보

- 강력한 후기 개발 단계의 신규 치료법 파이프라인

- 신흥 경제국에서의 의료 접근성 확대

- 의료 분야에서 시력 유지를 위한 의료비 지출 증가

- 억제요인

- 생물학적 제제 및 유전자 치료의 높은 비용

- 저소득지역의 한정적인 환급제도

- 엄격한 규제 및 안전 요건

- 만성적인 치료 부담과 환자의 치료 준수 부족

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 질병 형태별

- 건성 황반변성

- 습성 황반변성

- 질병 스테이지별

- 초기 황반변성(AMD)

- 중기 황반변성(AMD)

- 후기 황반변성(지리적 위축형 및 신생 혈관형)

- 치료 유형별

- 의약품

- 항VEGF제

- 보체 경로 억제제

- 유전자 및 세포 치료

- 영양보조식품 및 항산화제

- 기타 의약품

- 의료기기

- 저시력용 안경

- 콘택트렌즈

- 망막 이식 및 시각 보조 장치

- 수술

- 레이저광응고술

- 광역학치료

- 기타 외과 수술

- 의약품

- 투여 경로별

- 유리체내

- 초맥락막

- 정맥내 투여

- 판매 채널별

- 병원

- 외래수술센터(ASC)

- 전문 약국 및 일반 약국

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- GCC

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- F. Hoffmann-La Roche Ltd

- Novartis AG

- Regeneron Pharmaceuticals Inc.

- Bayer AG

- Bausch Health Companies Inc.

- Alcon Inc.

- Apellis Pharmaceuticals Inc.

- Astellas Pharma Inc.(Iveric Bio)

- Samsung Bioepis

- REGENXBIO Inc.

- 4D Molecular Therapeutics

- Adverum Biotechnologies

- EyePoint Pharmaceuticals

- Ocular Therapeutix Inc.

- Lineage Cell Therapeutics Inc.

- PanOptica

- OLIX Pharmaceuticals

- ONL Therapeutics

- MeiraGTx Holdings plc

- OnPoint Vision Inc.

제7장 시장 기회 및 미래 전망

CSM 26.01.28Macular degeneration treatment market size in 2026 is estimated at USD 18.2 billion, growing from 2025 value of USD 16.79 billion with 2031 projections showing USD 27.24 billion, growing at 8.39% CAGR over 2026-2031.

The outlook reflects demographic aging, regulatory support for breakthrough drugs, and rapid diffusion of digital diagnostics that identify disease earlier than conventional eye-care pathways. Elevated demand is reinforced by the 25% faster-than-aging rise in age-related macular degeneration (AMD) prevalence, the 94% sensitivity and 99% specificity of AI-based screening algorithms, and the pivot to complement pathway inhibitors that open therapy options for geographic atrophy. Gene and cell therapies in late-stage trials, sustained-release delivery platforms, and biosimilar price competition are reshaping revenue streams even as payers tighten utilization controls to contain biologic costs. Regionally, the United States retains first-mover access to novel treatments by leveraging the FDA's breakthrough-therapy channel, while Asia-Pacific's accelerating reimbursement expansion and massive elderly cohort underpin the fastest unit growth.

Global Macular Degeneration Treatment Market Trends and Insights

Rising Prevalence of Age-Related Eye Disorders

AMD prevalence is outpacing baseline aging trends by 25% as lifestyle factors such as prolonged screen time, poor diet quality, and rising urban pollution compound hereditary risks. WHO projects 288 million people living with AMD by 2030, pushing health systems toward earlier detection protocols that enlarge the treatable population by 40% relative to clinic-based screening. Untreated AMD already drains USD 343 billion in global productivity and care costs, spurring insurers to endorse preventive regimens including regular imaging and nutritional support. Nations with mature diagnostic networks are witnessing steep adoption of AI-enabled screening that reaches primary-care settings and pharmacies, effectively re-routing patients into therapy pipelines sooner. Pharmaceutical companies are responding with extended-duration implants that align with proactive care models and reduce office-visit congestion.

Rapid Growth of The Global Geriatric Population

Individuals aged >= 65 will represent 16.5% of humanity by 2030, and the 85+ cohort-most vulnerable to advanced AMD-is expanding at twice the broader elderly growth rate. Asia-Pacific nations led by Japan and South Korea are confronting unprecedented demand that strains specialist availability and catalyzes tele-ophthalmology adoption. Elderly patients often carry comorbid diabetes or hypertension, complicating anti-VEGF injection regimens and mandating closer safety oversight. U.S. Medicare spending on anti-VEGF therapy climbed from USD 2.51 billion in 2014 to USD 4.02 billion in 2019; projections show another doubling by 2030 absent less costly options. Governments thus favor self-administered agents and home-monitoring devices that cushion capacity bottlenecks and temper budget escalation.

High Cost of Biologic and Gene Therapies

Leading anti-VEGF injections are priced at USD 1,850-2,000 per dose, and typical regimens of 6-8 injections per year can exceed USD 15,000 before diagnostics and physician fees. One-time gene therapies under development may demand USD 200,000-500,000 per eye, igniting payer scrutiny despite potential lifetime cost offsets. Aflibercept biosimilars launched in 2024 shave 15-30% off list prices, yet switching inertia and product-specific safety data gaps curb rapid penetration. Payers are responding with step-therapy rules, site-of-care restrictions, and outcomes-based contracting pilots that tie reimbursement to visual-acuity durability. These access frictions temper near-term uptake of high-priced modalities and could drag the macular degeneration treatment market CAGR by nearly two percentage points.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Ocular Drug Delivery

- Strong Late-Stage Pipeline of Novel Therapies

- Limited Reimbursement in Low-Income Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wet AMD's 64.62% 2025 revenue dominance demonstrates the entrenchment of anti-VEGF therapy, yet growth deceleration is evident as biosimilars erode price and volume share. Trajectory shifts favor the dry-AMD segment, where SYFOVRE and IZERVAY approvals generated the first pharmacologic options for geographic atrophy, cutting lesion-expansion by up to 35%. As real-world data validate safety, payer adoption accelerates, propelling a 10.21% CAGR that reshapes portfolio priorities across the macular degeneration treatment market. Gene-therapy researchers concentrate disproportionately on dry AMD, attracted by a patient pool that comprises roughly 85% of total AMD cases and the opportunity to deliver one-time treatments that could circumvent lifelong injections.

Competitive investment now skews toward complement modulation and photoreceptor protection, with Phase III readouts expected across multiple mechanisms by 2027. Leading incumbents staunch wet-AMD share loss through high-dose aflibercept and combined VEGF/Ang-2 suppression, but strategic capital increasingly shifts to dry-AMD assets via acquisition and co-development deals. Commercial analysts anticipate convergence of wet and dry revenue lines by 2029 if dry-segment uptake maintains current velocity, a milestone that would recalibrate valuation metrics across the macular degeneration treatment industry.

Early-stage AMD accounted for 71.58% of the 2025 macular degeneration treatment market size, reflecting diagnostic expansion into primary-care, optometry, and community-pharmacy channels through cloud-connected fundus cameras. Ophthalmic societies endorse AREDS-based supplementation and lifestyle adjustments for newly diagnosed patients, anchoring a preventive-care economy that supports nutraceutical manufacturers and tele-monitoring vendors. Intermediate-stage AMD boasts the fastest segment CAGR at 10.78% through 2031 as complement inhibitors demonstrate lesion-growth suppression and extend "functional vision years" for patients. The commercial narrative emphasizes halting progression rather than restoring lost acuity, aligning payer interest with societal cost-avoidance.

Late-stage AMD remains the highest per-patient revenue tier because of recurring injection schedules and assistive-device demand. Nonetheless, sustained-release implants and gene therapies threaten to compress visit volumes and disrupt traditional fee-for-service business models. Real-time home-OCT devices streamline triage, routing only deteriorating eyes into clinic for prompt rescue, conserving capacity and advancing precision medicine across the macular degeneration treatment market.

The Macular Degeneration Treatment Market Report is Segmented by Disease Form (Dry Age-Related Macular Degeneration and Wet Age-Related Macular Degeneration), Stage of Disease (Early-Stage AMD, and More), Treatment Type (Drugs, and Surgery), Route of Administration (Intravitreal, and More), Sales Channels (Hospitals, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 41.88% of 2025 revenue, riding the twin engines of Medicare reimbursement and the world's densest ophthalmologist workforce. FDA priority-review and breakthrough-therapy pathways accelerate first-in-class launches, such as ENCELTO for MacTel approved in March 2025. Yet 5.4% Medicare fee cuts enacted in 2024 squeeze provider margins, catalyzing consolidation of retina practices and adoption of cost-efficient biosimilars. Rural access gaps persist, prompting state tele-optometry pilots that beam AI-evaluated images to urban hubs.

Europe is the second-largest region but faces heterogeneity in health-technology assessments. The EMA's 2024 denial of SYFOVRE underscores divergence from U.S. regulators and delays access in key markets. Germany and the UK, equipped with robust insurance and strong clinical networks, spearhead uptake of advanced therapies; Mediterranean states lag, constrained by budget ceilings that delay formulary inclusion. EU aging-over 20% of citizens are>= 65-intensifies demand, while Horizon 2030 grants inject R&D funds into regional biotechs, sustaining pipeline vibrancy.

Asia-Pacific is the fastest-growing arena at 9.41% CAGR. China's 260 million seniors by 2030 create colossal demand, but specialist scarcity and uneven insurance temper immediate penetration. Japan's super-aged society maximizes high-tech treatment uptake under its universal-care umbrella, positioning the nation as a launchpad for gene-therapy rollouts. India leverages AI-powered smartphone fundus imaging to extend reach across ophthalmologist-poor districts, unlocking early-stage volumes. Australia and South Korea blend robust reimbursement with clinical-trial participation, expediting regional approval cascades.

- Roche

- Novartis

- Regeneron Pharmaceuticals

- Bayer

- Bausch Health

- Alcon

- Apellis Pharmaceuticals Inc.

- Astellas Pharma Inc. (Iveric Bio)

- Samsung Bioepis

- REGENXBIO

- 4D Molecular Therapeutics

- Adverum Biotechnologies

- EyePoint Pharmaceuticals

- Ocular Therapeutix Inc.

- Lineage Cell Therapeutics

- PanOptica

- OLIX Pharmaceuticals

- ONL Therapeutics

- MeiraGTx Holdings plc

- OnPoint Vision Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Age-Related Eye Disorders

- 4.2.2 Rapid Growth of the Global Geriatric Population

- 4.2.3 Technological Advancements in Ocular Drug Delivery

- 4.2.4 Strong Late-Stage Pipeline of Novel Therapies

- 4.2.5 Expansion of Healthcare Access in Emerging Economies

- 4.2.6 Increasing Healthcare Expenditure on Vision Preservation

- 4.3 Market Restraints

- 4.3.1 High Cost of Biologic and Gene Therapies

- 4.3.2 Limited Reimbursement in Low-Income Regions

- 4.3.3 Stringent Regulatory and Safety Requirements

- 4.3.4 Chronic Treatment Burden and Patient Non-Compliance

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Disease Form

- 5.1.1 Dry Age-Related Macular Degeneration

- 5.1.2 Wet Age-Related Macular Degeneration

- 5.2 By Stage of Disease

- 5.2.1 Early-Stage AMD

- 5.2.2 Intermediate-Stage AMD

- 5.2.3 Late-Stage AMD (Geographic Atrophy & Neovascular)

- 5.3 By Treatment Type

- 5.3.1 Drugs

- 5.3.1.1 Anti-VEGF Agents

- 5.3.1.2 Complement Pathway Inhibitors

- 5.3.1.3 Gene & Cell Therapy

- 5.3.1.4 Dietary Supplements & Antioxidants

- 5.3.1.5 Other Drugs

- 5.3.2 Devices

- 5.3.2.1 Low-Vision Glasses

- 5.3.2.2 Contact Lenses

- 5.3.2.3 Retinal Implants & Vision Aids

- 5.3.3 Surgery

- 5.3.3.1 Laser Photocoagulation

- 5.3.3.2 Photodynamic Therapy

- 5.3.3.3 Other Surgical Procedures

- 5.3.1 Drugs

- 5.4 By Route of Administration

- 5.4.1 Intravitreal

- 5.4.2 Suprachoroidal

- 5.4.3 Intravenous

- 5.5 By Sales Channel

- 5.5.1 Hospitals

- 5.5.2 Ambulatory Surgical Centers

- 5.5.3 Specialty & Retail Pharmacies

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.5.3.1 GCC

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 F. Hoffmann-La Roche Ltd

- 6.3.2 Novartis AG

- 6.3.3 Regeneron Pharmaceuticals Inc.

- 6.3.4 Bayer AG

- 6.3.5 Bausch Health Companies Inc.

- 6.3.6 Alcon Inc.

- 6.3.7 Apellis Pharmaceuticals Inc.

- 6.3.8 Astellas Pharma Inc. (Iveric Bio)

- 6.3.9 Samsung Bioepis

- 6.3.10 REGENXBIO Inc.

- 6.3.11 4D Molecular Therapeutics

- 6.3.12 Adverum Biotechnologies

- 6.3.13 EyePoint Pharmaceuticals

- 6.3.14 Ocular Therapeutix Inc.

- 6.3.15 Lineage Cell Therapeutics Inc.

- 6.3.16 PanOptica

- 6.3.17 OLIX Pharmaceuticals

- 6.3.18 ONL Therapeutics

- 6.3.19 MeiraGTx Holdings plc

- 6.3.20 OnPoint Vision Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment