|

시장보고서

상품코드

1905981

부직포 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Non-woven Fabric - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

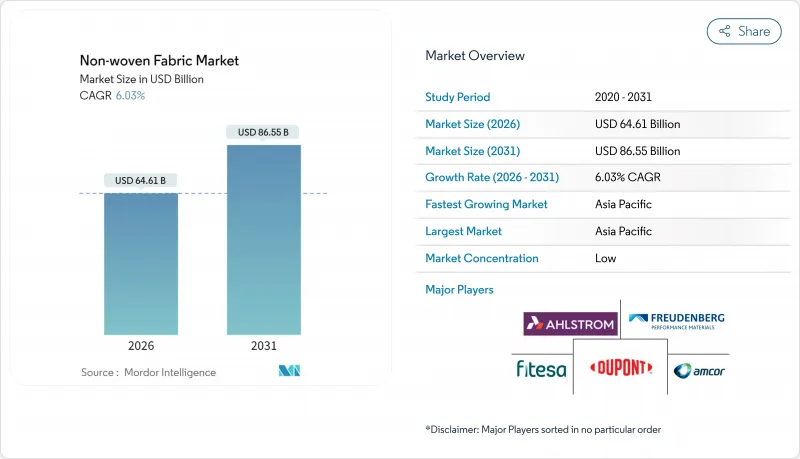

부직포 시장은 2025년에 609억 3,000만 달러로 평가되었고, 2026년 646억 1,000만 달러에서 2031년까지 865억 5,000만 달러에 이를 것으로 예측되고 있습니다.

예측기간(2026-2031년)의 CAGR은 6.03%를 나타낼 전망입니다.

의료, 건설 및 자동차 응용 분야의 지속적인 수요는 스펀본드 생산 라인에 대한 투자를 가속화하는 한편, 일렉트로스펀 나노섬유의 획기적인 발전은 상처 치료, 여과 및 고체 배터리 분리막 분야에서 프리미엄 틈새 시장을 열어주고 있습니다. 폴리프로필렌 기반 등급은 프로필렌 원료 가격 상승에도 직물 대비 비용 우위를 유지하여 가공업체의 마진 방위에 기여합니다. 미세 플라스틱 유출 및 재활용 가능 포장재에 대한 규제 동향은 제품 설계를 생분해성 또는 순환형 솔루션으로 전환시키고 있으며, 이로 인해 레이온, 리오셀 및 천연 섬유 혼방 제품이 주류 사양으로 부상하고 있습니다.

세계의 부직포 시장 동향 및 인사이트

일회용 위생 용품 수요 급증

아시아태평양 일부 지역의 출산율 급증과 북미 및 유럽의 지속적인 인구 고령화로 인해 가볍고 흡수성 높은 부직포를 사용하는 기저귀, 성인용 요실금 패드, 여성 위생용품의 판매량이 증가하고 있습니다. 제어된 증기 투과 필름과 초흡수성 코어를 통합한 스마트 상처 관리 기판이 파일럿 단계에서 대량 생산으로 전환되며 치유 환경을 개선하고 드레싱 교체 횟수를 줄이고 있습니다. 제조사들은 액체 처리 성능을 최적화하면서도 평중량을 낮게 유지하기 위해 스펀본드와 멜트블로운 층을 조합하고 있으며, 이러한 구성은 변환업체가 성능 저하 없이 가격 경쟁력을 확보하는 데 도움이 됩니다. 브랜드 소유주들은 또한 소매업체의 지속가능성 평가 기준에 부합하기 위해 염소 처리되지 않은 플러프 펄프와 바이오 기반 바인더를 선호합니다. 이러한 트렌드들은 종합하여 2020년대 중반까지 위생 분야에서 부직포 시장의 성장 궤도를 강화하고 있습니다.

의료용 개인보호장비(PPE) 및 상처 관리 분야의 급속한 채택

팬데믹 기간 동안 공급 부족을 경험한 병원 공급망은 인증된 차단 성능을 갖춘 마스크, 가운, 드레이프에 대한 재고 확보 요구 사항을 확대했습니다. NIOSH의 2020-2030년 목표는 국내 비상 생산 능력 확충을 강조하며, 실시간 품질 모니터링 기능을 갖춘 고생산성 스펀-멜트 복합재에 대한 투자를 촉진하고 있습니다. 폴리이미드 또는 PEEK 기반 전기방사 나노섬유는 향상된 내열성을 제공하여 동력 공기 정화 호흡기 및 이식형 기기에 사용됩니다. 은 나노입자 또는 성장 인자를 통합한 다기능 상처 드레싱은 전임상 시험에서 99.99% 이상의 세균 감소율과 더 빠른 상피화를 보여줍니다. 입원 기간 단축을 보상하는 보험급여 개혁은 감염 위험과 치유 시간을 단축하는 고급 부직포 수요를 더욱 뒷받침합니다.

PP 및 PET 가격 변동

예상치 못한 정유소 가동 중단과 신규 프로필렌 설비 증설 지연으로 공급이 긴축되면서, 2025년 초 남아시아 지역 폴리프로필렌 계약 가격이 톤당 10-20달러 상승했습니다. 동시에 홍해 우회 운송에 따른 운임 할증료가 주요 가공 허브로의 인도 비용을 부풀렸습니다. 중국과 유럽의 생산자들이 마이너스 스프레드 속에서 노후 폴리머 라인을 가동 중단하면서 PET 시장도 동일한 양상을 보였습니다. 이러한 변동은 위생용품 브랜드사와 고정가격 공급계약을 체결한 가공업체들의 마진을 압박하여 수지 헤징 또는 소재 대체 전략 모색으로 이어지고 있습니다.

부문 분석

2025년 부직포 시장에서는 스펀본드 부문이 52.88%를 차지했습니다. 이는 높은 처리량과 위생용 라미네이트, 의료용 가운, 지오텍스타일에 대한 입증된 적합성을 반영합니다. 세대별 업그레이드를 통해 현재는 에너지 사용을 억제하기 위해 중량 제어 스캐너와 폐쇄형 공기 재순환 시스템을 통합하고 있습니다. 부드러운 탑시트와 3층 SMX 기반 복합재 분야에서 성장 기회가 나타나고 있으며, 이는 차단 성능을 저하시키지 않으면서도 천과 같은 촉감을 향상시킵니다.

기타 기술들은 2031년까지 연평균 8.74% 성장률을 기록하며, 나노섬유 웹, 농도 그라데이션 매트, 3D 로프트 펠트를 생산하는 전기방사, 원심방사, 고강도 니들링 플랫폼을 통해 부직포 시장 규모에 대한 기여도를 높일 전망입니다. PAN/PS/PMMA 혼합물을 사용한 전기방사 분리막은 150°C에서 75.87%의 다공성과 3% 미만의 수축률을 달성하여 고안전성 배터리 팩에 요구되는 특성을 충족합니다. 멜트블로운 제조업체들은 나노입자 도핑과 정전기 충전 기술을 결합하여 0.3μm 에어로졸 포집률을 97% 이상 유지함으로써 공기 여과 및 호흡기 보호 장비 계약을 확보하고 있습니다.

지역별 분석

아시아태평양 지역은 2025년 부직포 시장 점유율의 48.10%를 차지했으며, 기저귀 및 마스크 소비 증가에 대응하기 위해 중국, 인도, 인도네시아에서 변환기 업체들이 확장함에 따라 2031년까지 연평균 7.50%의 성장률을 보일 전망입니다. 지역 공급망은 프로필렌 분해 장치, 섬유 방적, 최종 제품 조립을 근접한 위치에 통합하여 물류 비용을 최소화합니다. 중국 업체들은 국내 전기차(EV) 공장용 방음 및 단열재 전용 니들펀치 생산라인을 추가하고 있으며, 인도 생산업체들은 물티슈 수출업체 공급을 위해 스펀레이스 설비를 확대하고 있습니다.

북미는 킴벌리-클라크가 오하이오 및 사우스캐롤라이나 시설에 인공지능 기반 물류 시스템을 도입하며 20억 달러 규모로 확장하는 등 핵심 의료용 개인보호장비(PPE) 및 배터리 분리막 공급망의 리쇼어링(국내 복귀) 혜택을 누리고 있습니다. 아사히 가세이가 캐나다에 건설 예정인 분리막 공장은 2027년부터 미국 전기차 생태계에 공급할 예정입니다. 인력 시장 경직으로 고자동화 스펀본드 라인의 도입이 가속화되며 장비 공급업체에 기회가 창출됩니다.

유럽의 엄격한 규제는 생분해성 섬유 및 폐쇄형 재활용 시범사업 투자를 촉진합니다. 프로이덴베르크의 헤이텍스 인수는 코팅 기술 섬유 시장 진출을 확대하는 한편, 렌징의 리오셀 설비 업그레이드는 바이오 기반 원료의 장기적 공급을 확보합니다. 중동 및 아프리카는 해안 보호 및 위생용품 현지화와 연계된 수요가 부상하는 반면, 라틴아메리카는 근거리 생산을 활용해 북미 위생 브랜드에 경쟁력 있는 가격의 복합재를 공급합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 일회용 위생 용품 수요 급증

- 의료용 개인보호장비(PPE) 및 상처 관리 분야에서의 빠른 채택

- 인프라 정비 확대가 지오텍 스타일 수요를 주도

- 직물 및 편물 대비 비용 경쟁력

- 고체 상태 전기차 배터리 분리막

- 시장 성장 억제요인

- PP 및 PET의 가격 변동성

- 미세 플라스틱/매립지 규제 강화

- 직물에 비해 열악한 인장 및 인열 강도

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 기술별

- 스펀본드

- 습식 레이드

- 건식 레이드

- 기타 기술

- 재료별

- 폴리에스테르

- 폴리프로필렌

- 폴리에틸렌

- 레이온(비스코스)

- 기타

- 최종 사용자 산업별

- 건설

- 섬유

- 헬스케어

- 자동차

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 튀르키예

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 나이지리아

- 이집트

- 카타르

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/순위 분석

- 기업 프로파일

- Ahlstrom

- Amcor plc

- Asahi Kasei Advance Corporation

- Autotech Nonwovens Pvt Ltd

- Avgol Industries 1953 Ltd

- Cygnus Group

- DuPont

- Eximius Innovative Pvt. Ltd.

- Fibertex Nonwovens A/S

- Fitesa SA and Affiliates

- Freudenberg Performance Materials

- Hollingsworth & Vose

- Indorama Ventures Public Company Limited

- Johns Manville

- KCWW

- Lydall, Inc.

- Magnera

- Mitsui Chemicals, Inc.

- paramountnonwoven

- PFNonwovens Holding sro

- Toray Industries Inc.

- TWE GmbH & Co. KG

제7장 시장 기회와 장래의 전망

HBR 26.01.26The Non-woven Fabric Market was valued at USD 60.93 billion in 2025 and estimated to grow from USD 64.61 billion in 2026 to reach USD 86.55 billion by 2031, at a CAGR of 6.03% during the forecast period (2026-2031).

Sustained demand from healthcare, construction, and automotive applications continues to accelerate investment in spun-bond manufacturing lines, while electrospun nanofiber breakthroughs open premium niches in wound care, filtration, and solid-state battery separators. Polypropylene-based grades preserve a cost edge over woven fabrics even as propylene feedstock prices rise, helping converters defend margins. Regulatory momentum around microplastic leakage and recyclable packaging is reshaping product design toward biodegradable or circular solutions, pushing rayon, lyocell, and natural-fiber blends into mainstream specifications.

Global Non-woven Fabric Market Trends and Insights

Exploding Demand for Disposable Hygiene Products

Soaring birth rates in parts of Asia-Pacific and steadily aging populations in North America and Europe are lifting unit sales of diapers, adult incontinence pads, and feminine hygiene articles that rely on lightweight, absorbent non-wovens. Smart wound-care substrates incorporating controlled vapor transmission films and super-absorbent cores are moving from pilot to high-volume production, improving healing environments and reducing dressing changes. Producers are pairing spun-bond and melt-blown layers to optimize fluid handling while keeping basis weight low, a configuration that helps converters meet price points without sacrificing performance. Brand owners also favor chlorine-free fluff pulps and bio-based binders to align with retailer sustainability scorecards. Together, these trends reinforce the non-woven fabric market trajectory in hygiene through mid-decade.

Rapid Adoption in Medical PPE and Wound-Care

Hospital supply chains that experienced shortages during the pandemic have expanded stocking requirements for masks, gowns, and drapes with certified barrier performance. NIOSH targets for 2020-2030 emphasize domestic surge capacity, prompting investment in high-output spun-melt composites equipped with real-time quality monitoring. Electrospun nanofibers based on polyimide or PEEK deliver elevated heat resistance, allowing their use in powered air-purifying respirators and implantable devices. Multifunctional wound dressings integrating silver nanoparticles or growth factors show more than 99.99% bacterial reduction and faster epithelialization in pre-clinical trials. Reimbursement reforms that reward shorter hospital stays further support demand for advanced non-wovens that cut infection risk and healing time.

PP and PET Price Volatility

Unplanned refinery outages and delayed new propylene capacities have tightened supply, lifting polypropylene contract prices in South Asia by USD 10-20 per ton in early 2025. At the same time, freight surcharges tied to Red Sea rerouting inflate delivered costs into key converting hubs. PET markets mirror the pattern as producers in China and Europe shut older polymer lines amid negative spreads. Such swings compress margins for converters locked into fixed-price supply contracts with hygiene brand owners, prompting them to explore resin hedging or material substitution strategies.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Boom Driving Geotextile Uptake

- Cost Advantage Over Woven and Knitted Fabrics

- Microplastic and Landfill Regulations Tightening

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The spun-bond segment accounted for 52.88% of the non-woven fabric market in 2025, reflecting its high throughput and proven suitability for hygiene laminates, medical gowns, and geotextiles. Generational upgrades now integrate weight-control scanners and closed-loop air recirculation to curb energy use. Growth opportunities emerge in ultra-soft topsheets and 3-layer SMX-based composites that enhance cloth-like feel without sacrificing barrier integrity.

Other technologies are set to expand at an 8.74% CAGR to 2031, lifting their contribution to the non-woven fabric market size through electrospinning, centrifugal spinning, and intense needling platforms that deliver nanofiber webs, gradient density mats, and 3D lofted felts. Electrospun separators using PAN/PS/PMMA blends achieve 75.87% porosity and less than 3% shrinkage at 150 °C, features valued in high-safety battery packs. Melt-blown producers combine electret charging with nanoparticle doping to maintain more than 97% capture of 0.3 µm aerosols, securing air-filtration and respirator contracts.

The Non-Woven Fabric Market Report is Segmented by Technology (Spun-Bond, Wet Laid, Dry Laid, and Other Technologies), Material (Polyester, Polypropylene, Polyethylene, Rayon (Viscose), and Others), End-User Industry (Construction, Textiles, Healthcare, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 48.10% of non-woven fabric market share in 2025 and is on course for a 7.50% CAGR to 2031 as converters expand in China, India, and Indonesia to serve growing diaper and mask consumption. Regional supply chains integrate propylene crackers, fiber spinning, and end-product assembly within close proximity, minimizing logistics cost. Chinese lines add needlepunch capacity dedicated to acoustic and thermal insulation for domestic EV factories, while Indian producers scale spun-lace installations to supply wipes exporters.

North America benefits from reshoring of critical medical-PPE and battery-separator supply, supported by Kimberly-Clark's USD 2 billion expansion across Ohio and South Carolina facilities that feature AI-enabled logistics. Canada's forthcoming separator plant from Asahi Kasei will feed the U.S. EV ecosystem beginning in 2027. Tight labor markets push the adoption of high-automation spun-bond lines, creating opportunities for equipment vendors.

Europe's stringent regulations spur investment in biodegradable fibers and closed-loop recycling pilots. Freudenberg's acquisition of Heytex deepens exposure to coated technical textiles, while Lenzing's lyocell upgrades secure long-term supply of bio-based inputs. Middle East and Africa show emerging demand linked to coastal protection and sanitary product localization, whereas Latin America leverages nearshoring to supply North American hygiene brands with competitively priced composites.

- Ahlstrom

- Amcor plc

- Asahi Kasei Advance Corporation

- Autotech Nonwovens Pvt Ltd

- Avgol Industries 1953 Ltd

- Cygnus Group

- DuPont

- Eximius Innovative Pvt. Ltd.

- Fibertex Nonwovens A/S

- Fitesa SA and Affiliates

- Freudenberg Performance Materials

- Hollingsworth & Vose

- Indorama Ventures Public Company Limited

- Johns Manville

- KCWW

- Lydall, Inc.

- Magnera

- Mitsui Chemicals, Inc.

- paramountnonwoven

- PFNonwovens Holding s.r.o.

- Toray Industries Inc.

- TWE GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exploding demand for disposable hygiene products

- 4.2.2 Rapid adoption in medical PPE and wound-care

- 4.2.3 Infrastructure boom driving geotextile uptake

- 4.2.4 Cost-advantage over woven and knitted fabrics

- 4.2.5 Solid-state EV battery separators

- 4.3 Market Restraints

- 4.3.1 PP and PET price volatility

- 4.3.2 Micro-plastic / landfill regulations tightening

- 4.3.3 Inferior tensile and tear strength vs woven fabric

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Spun-bond

- 5.1.2 Wet Laid

- 5.1.3 Dry Laid

- 5.1.4 Other Technologies

- 5.2 By Material

- 5.2.1 Polyester

- 5.2.2 Polypropylene

- 5.2.3 Polyethylene

- 5.2.4 Rayon (Viscose)

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Construction

- 5.3.2 Textiles

- 5.3.3 Healthcare

- 5.3.4 Automotive

- 5.3.5 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Turkey

- 5.4.3.7 Russia

- 5.4.3.8 Nordic Countries

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Egypt

- 5.4.5.5 Qatar

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Ahlstrom

- 6.4.2 Amcor plc

- 6.4.3 Asahi Kasei Advance Corporation

- 6.4.4 Autotech Nonwovens Pvt Ltd

- 6.4.5 Avgol Industries 1953 Ltd

- 6.4.6 Cygnus Group

- 6.4.7 DuPont

- 6.4.8 Eximius Innovative Pvt. Ltd.

- 6.4.9 Fibertex Nonwovens A/S

- 6.4.10 Fitesa SA and Affiliates

- 6.4.11 Freudenberg Performance Materials

- 6.4.12 Hollingsworth & Vose

- 6.4.13 Indorama Ventures Public Company Limited

- 6.4.14 Johns Manville

- 6.4.15 KCWW

- 6.4.16 Lydall, Inc.

- 6.4.17 Magnera

- 6.4.18 Mitsui Chemicals, Inc.

- 6.4.19 paramountnonwoven

- 6.4.20 PFNonwovens Holding s.r.o.

- 6.4.21 Toray Industries Inc.

- 6.4.22 TWE GmbH & Co. KG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment