|

시장보고서

상품코드

1905982

유럽의 콜라겐 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Collagen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

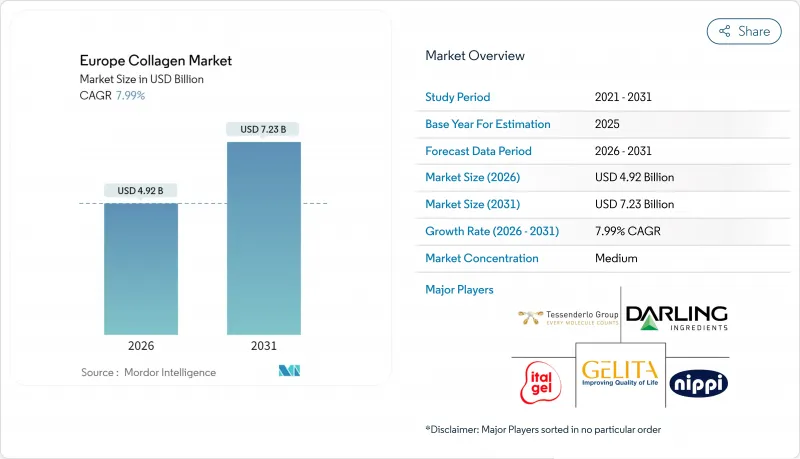

유럽의 콜라겐 시장은 2025년의 45억 6,000만 달러로 평가되었고, 2026년에는 49억 2,000만 달러로 성장하여 2026-2031년에 걸쳐 CAGR 7.99%로 성장할 것으로 보이며, 2031년까지 72억 3,000만 달러에 이를 전망입니다.

소비자들의 적극적인 건강 관리, 피부 개선 효과, 관절 건강 효능에 대한 관심이 높아지면서 해당 카테고리의 지속적인 고급화 추세가 이어지고 있으며, 허용 가능한 건강 관련 표시 사항에 대한 규제 명확화로 프리미엄 제품 혁신이 가속화되고 있습니다. 수요는 기존의 소 및 돼지 유래 원료에서 우수한 생체 이용률과 낮은 환경 영향을 제공하는 추적 가능한 해양 원료로 전환되고 있습니다. 임상적 입증과 책임 있는 원료 조달을 결합한 브랜드 소유자들은 비례 이상의 진열대 가시성을 확보하고 있으며, 독일, 프랑스, 네덜란드 소매업체들은 카테고리 평균보다 높은 가격대에도 불구하고 해양 콜라겐 제품군의 지속적인 두 자릿수 판매 증가를 보고하고 있습니다. 정밀 발효 및 재조합 플랫폼의 혁신은 의료 기기 및 기능성 식품 분야에서 적용 가능한 사용 사례를 확대하고 있으며, 통합 생산자들은 규모를 활용하여 유럽연합의 까다로운 규정 준수 환경을 헤쳐 나가고 있습니다.

유럽의 콜라겐 시장 동향 및 인사이트

건강 및 웰니스 제품에 대한 소비자 수요 증가

유럽 소비자들은 예방적 건강 관리 전략을 점점 더 채택하며, 사후 대응형 의료에서 사전 예방적 웰니스 관리로 초점을 전환하고 있습니다. 이러한 변화로 콜라겐의 사용 영역이 전통적인 미용 분야에서 기능성 영양 분야로 확대되었습니다. 특히 35-55세의 교육 수준이 높은 소비자들은 관절 가동성과 피부 탄력 유지에 콜라겐 보충이 필수적이라고 생각합니다. 고령화 인구와 높아지는 건강 의식이 결합되어 프리미엄 콜라겐 제품에 대한 꾸준한 수요를 이끌고 있습니다. 유럽 소비자들은 과학적으로 검증된 제형에 대해 25-40% 더 높은 가격을 지불할 의사가 뚜렷합니다. 또한 EFSA(유럽식품안전청) 지침 하의 규제 프레임워크가 콜라겐 펩타이드에 대한 건강 기능성 주장을 점점 더 인정함에 따라, 제조사들은 제품 포지셔닝과 마케팅 커뮤니케이션에 대한 명확한 기회를 얻고 있습니다.

관절 케어 솔루션을 요구하는 고령화 사회

유럽의 고령화 인구는 관절 관리 솔루션 수요 급증을 촉진하고 있습니다. 유로스타트(Eurostat) 전망에 따르면 유럽의 노인 부양비율은 2023년 33.4%에서 2100년까지 무려 59.7%로 상승할 전망입니다. 통합의학 및 보완의학 저널(Journal of Integrative and Complementary Medicine)에 소개된 임상 연구에 따르면, 비변성 II형 콜라겐 보충은 무릎 관절 유연성을 현저히 향상시킬 수 있음이 입증되었습니다. 구체적으로, 24주간의 보충 후 피험자들은 굴곡 각도가 3.23°, 신전 각도가 2.21° 각각 개선된 것으로 나타났습니다. 이러한 인구 구조적 변화는 특히 활동으로 인한 관절 통증에 시달리는 50세 이상 유럽인들 사이에서 콜라겐 함유 관절 건강 제품에 대한 꾸준한 수요를 촉진하고 있습니다. 유럽 시장은 생체 이용률과 입증된 임상적 이점으로 높이 평가받는 콜라겐 가수분해물 제형으로 기울고 있습니다. 특히 관절 건강 적용 분야에서는 일일 10g 복용량이 기준치로 자리 잡았습니다. 더불어 유럽 전역의 의료 시스템은 콜라겐 보충을 관절 기능 유지뿐만 아니라 장기적인 정형외과 치료 비용 절감 가능성까지 고려한 경제적인 전략으로 점점 더 인식하고 있습니다.

식물성 단백질 대체물의 상승

유럽 시장은 식물성 단백질 대체재의 성장과 합성 생물학의 발전으로 인해 기존 콜라겐 조달 모델에 도전받으며 점점 더 큰 압박을 받고 있습니다. 플랜트폼 코퍼레이션(PlantForm Corporation)의 식물 기반 시스템을 활용한 재조합 인간 콜라겐 생산은 비건 대체재의 상업적 실현 가능성을 입증하며, 해당 시장은 2030년까지 114억 달러 규모로 성장할 것으로 전망됩니다. 특히 환경 영향과 동물 복지를 중시하는 젊은 층을 중심으로 소비자 선호도가 윤리적이고 지속 가능한 옵션으로 전환되고 있습니다. 비건 콜라겐 대체재가 동물 유래 제품과 기능적 동등성을 달성하면서도 더 나은 일관성과 규제상의 이점을 제공함에 따라 경쟁은 더욱 치열해지고 있습니다. 이에 대응해 유럽 제조사들은 발효 기반 생산 기술에 투자하고, 윤리적 우려를 해소하면서 시장 지위를 유지하기 위해 전통적 단백질 원료와 대체 원료를 통합한 하이브리드 제형을 개발하고 있습니다.

부문 분석

동물성 콜라겐은 확립된 공급망과 소 및 돼지 유래 원료에 대한 소비자 친숙도를 반영하여 2025년 65.05% 점유율로 시장 주도권을 유지합니다. 그러나 해양성 콜라겐은 지속가능성 이점과 추적 가능한 해양 원료를 전통적 동물 유래물보다 선호하는 규제 환경에 힘입어 2031년까지 연평균 10.11%의 우수한 성장 동력을 보여줍니다. 해양 부문은 추출 방법의 기술적 진보와 생체 이용률 이점에 대한 소비자 인식 증가로 혜택을 보며, 어류 콜라겐은 포유류 대체재 대비 1.5배 높은 흡수율을 보여줍니다.

유럽의 규제 프레임 워크는 BSE 위험 감소 및 명확한 추적성 요건으로 해양 원료를 점점 더 선호하며, EFSA 평가를 통해 반추동물 유래 콜라겐 대비 안전성 우위가 확인되었습니다. 어류 가공 부산물로부터 해양 콜라겐을 추출하는 혁신 기술은 지속가능성 문제를 해결하는 동시에 폐기물 흐름에서 경제적 가치를 창출하며, 연구에 따르면 유럽 어업만으로도 연간 6,500톤 이상의 생산 잠재력이 있는 것으로 나타났습니다. 전통적인 동물성 콜라겐 생산자들이 해양 가공 역량에 투자하는 한편, 전문 해양 생명공학 기업들이 프리미엄 포지셔닝과 지속가능성 인증을 통해 시장 점유율을 확대하면서 경쟁 구도가 변화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 건강 및 웰니스 제품에 대한 소비자 수요 증가

- 관절 케어 솔루션을 요구하는 고령화 인구

- 미용 및 퍼스널케어 분야의 확대

- 영양 보조 식품에서의 응용 확대

- 지속 가능한 해양성 콜라겐 원료로의 이행

- 연구 및 생산 분야의 혁신 증가

- 시장 성장 억제요인

- 비건 단백질 대체재의 부상

- 엄격한 규제 준수 및 인증 요건

- 동물 유래 콜라겐에 관련된 윤리적 및 알레르기성 우려

- 고품질 콜라겐 원료 조달 및 가공 비용 상승

- 공급망 분석

- 규제 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유래별

- 동물 유래

- 해양 유래

- 최종 사용자/용도별

- 식품 및 음료

- 영양보조식품

- 퍼스널케어 및 화장품

- 의약품

- 동물용 사료

- 지역별

- 독일

- 영국

- 이탈리아

- 프랑스

- 스페인

- 네덜란드

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 랭킹 분석

- 기업 프로파일

- Gelita AG

- Darling Ingredients Inc.(Rousselot)

- PB Leiner(Tessenderlo Group)

- Italgel Srl

- Nippi, Incorporated

- Lapi Gelatine SpA

- Collagen Solutions Plc

- DSM-Firmenich

- Symrise AG

- Weishardt Group

- Gelnex

- Lonza Group Ltd.

- BioCell Technology LLC

- Jellagen Ltd

- CollaSwiss(Swiss Nutrivalor)

- Medichema GmbH

- Evonik Industries AG

- Essentia Protein Solutions

- PB Gelatins

- NovaColl(Geltor)

제7장 시장 기회와 장래의 전망

HBR 26.01.26The European collagen market is expected to grow from USD 4.56 billion in 2025 to USD 4.92 billion in 2026 and is forecast to reach USD 7.23 billion by 2031 at 7.99% CAGR over 2026-2031.

Heightened consumer focus on proactive health, visible skin benefits, and joint-care efficacy underpins steady category trading up, while regulatory clarity on permissible health claims accelerates premium innovation. Demand is shifting from conventional bovine and porcine ingredients to traceable marine sources that offer superior bioavailability and a smaller environmental footprint. Brand owners that combine clinical substantiation with responsible sourcing capture disproportionate shelf visibility, and German, French, and Dutch retailers report sustained double-digit sell-out for marine collagen lines despite above-category price points. Innovation in precision fermentation and recombinant platforms is widening the addressable use-case set in medical devices and functional foods, while integrated producers leverage their scale to navigate the European Union's demanding compliance landscape.

Europe Collagen Market Trends and Insights

Increasing Consumer Demand for Health and Wellness Products

European consumers are increasingly adopting preventive health strategies, shifting their focus from reactive healthcare to proactive wellness management. This shift has expanded the use of collagen from traditional beauty applications to functional nutrition. Educated consumers aged 35-55, in particular, consider collagen supplementation essential for maintaining joint mobility and skin elasticity. The combination of aging demographics and rising health awareness is driving consistent demand for premium collagen products. European consumers are notably willing to pay 25-40% more for scientifically validated formulations. Additionally, regulatory frameworks under EFSA guidance are increasingly endorsing health claims for collagen peptides, providing manufacturers with clearer opportunities for product positioning and marketing communications.

Ageing Population Seeking Joint-Care Solutions

Europe's aging population is fueling a surge in demand for joint-care solutions. Projections from Eurostat indicate that the old-age dependency ratio in Europe will rise from 33.4% in 2023 to a staggering 59.7% by 2100. Clinical studies, as highlighted in the Journal of Integrative and Complementary Medicine, have shown that supplementation with undenatured type II collagen can notably enhance knee joint flexibility. Specifically, after 24 weeks of supplementation, subjects exhibited a 3.23° improvement in flexion and a 2.21° boost in extension. This demographic evolution is propelling a consistent demand for collagen-infused joint health products, especially among Europeans over 50 who often grapple with activity-induced joint discomfort. The European market is leaning towards collagen hydrolysate formulations, prized for their bioavailability and proven clinical benefits. Notably, a daily dosage of 10g has emerged as the benchmark for joint health applications. Furthermore, healthcare systems across Europe are increasingly viewing collagen supplementation as a budget-friendly strategy, not only to uphold joint function but also to potentially curtail long-term orthopedic care expenses.

Rise of Vegan Protein Alternatives

The European market is under increasing pressure from the growth of plant-based protein alternatives and advancements in synthetic biology, which challenge traditional collagen sourcing models. PlantForm Corporation's production of recombinant human collagen using plant-based systems highlights the commercial feasibility of vegan alternatives, with the market projected to reach USD 11.4 billion by 2030. Consumer preferences are shifting toward ethical and sustainable options, particularly among younger demographics who emphasize environmental impact and animal welfare. The competition intensifies as vegan collagen alternatives achieve functional equivalence with animal-derived products while offering better consistency and regulatory benefits. In response, European manufacturers are investing in fermentation-based production technologies and creating hybrid formulations that integrate traditional and alternative protein sources to retain their market position while addressing ethical concerns.

Other drivers and restraints analyzed in the detailed report include:

- Expansion in the Beauty and Personal Care Sector

- Increasing Applications in Dietary Supplements

- Stringent Regulatory Compliance and Certification Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Animal-based collagen maintains market leadership with a 65.05% share in 2025, reflecting established supply chains and consumer familiarity with bovine and porcine sources. However, marine-based collagen demonstrates superior growth dynamics at 10.11% CAGR through 2031, driven by sustainability advantages and regulatory preferences that favor traceable marine sources over traditional animal derivatives. The marine segment benefits from technological advances in extraction methods and growing consumer awareness of bioavailability advantages, with fish collagen demonstrating 1.5 times higher absorption rates than mammalian alternatives.

European regulatory frameworks increasingly favor marine sources due to reduced BSE risk and clearer traceability requirements, with EFSA assessments confirming safety advantages over ruminant-derived collagen. Innovation in marine collagen extraction from fish processing by-products addresses sustainability concerns while creating economic value from waste streams, with research demonstrating potential annual production exceeding 6,500 tons from European fisheries alone. The competitive landscape evolves as traditional animal collagen producers invest in marine processing capabilities while specialized marine biotechnology companies gain market share through premium positioning and sustainability credentials.

The Europe Collagen Market Report is Segmented by Source (Animal-Based, Marine-Based), End User/Application (Food & Beverages, Dietary Supplements, Personal Care & Cosmetics, Pharmaceuticals, Animal Nutrition), and Geography (Germany, United Kingdom, Italy, France, Spain, Netherlands, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Gelita AG

- Darling Ingredients Inc. (Rousselot)

- PB Leiner (Tessenderlo Group)

- Italgel S.r.l.

- Nippi, Incorporated

- Lapi Gelatine S.p.A.

- Collagen Solutions Plc

- DSM-Firmenich

- Symrise AG

- Weishardt Group

- Gelnex

- Lonza Group Ltd.

- BioCell Technology LLC

- Jellagen Ltd

- CollaSwiss (Swiss Nutrivalor)

- Medichema GmbH

- Evonik Industries AG

- Essentia Protein Solutions

- PB Gelatins

- NovaColl (Geltor)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing consumer demand for health and wellness products,

- 4.2.2 Ageing population seeking joint-care solutions

- 4.2.3 Expansion in the beauty and personal care sector

- 4.2.4 Increasing Applications in Dietary Supplements

- 4.2.5 Shift toward sustainable marine collagen sources

- 4.2.6 Rising Innovation in research and production

- 4.3 Market Restraints

- 4.3.1 Rise of vegan protein alternatives

- 4.3.2 Stringent regulatory compliance and certification requirements

- 4.3.3 Ethical and allergenic concerns related to animal-derived collagen

- 4.3.4 High costs of sourcing and processing high-quality collagen raw materials

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECAST

- 5.1 By Source

- 5.1.1 Animal-based

- 5.1.2 Marine-based

- 5.2 By End User / Application

- 5.2.1 Food & Beverages

- 5.2.2 Dietary Supplements

- 5.2.3 Personal Care & Cosmetics

- 5.2.4 Pharmaceuticals

- 5.2.5 Animal Nutrition

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 Italy

- 5.3.4 France

- 5.3.5 Spain

- 5.3.6 Netherlands

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Gelita AG

- 6.4.2 Darling Ingredients Inc. (Rousselot)

- 6.4.3 PB Leiner (Tessenderlo Group)

- 6.4.4 Italgel S.r.l.

- 6.4.5 Nippi, Incorporated

- 6.4.6 Lapi Gelatine S.p.A.

- 6.4.7 Collagen Solutions Plc

- 6.4.8 DSM-Firmenich

- 6.4.9 Symrise AG

- 6.4.10 Weishardt Group

- 6.4.11 Gelnex

- 6.4.12 Lonza Group Ltd.

- 6.4.13 BioCell Technology LLC

- 6.4.14 Jellagen Ltd

- 6.4.15 CollaSwiss (Swiss Nutrivalor)

- 6.4.16 Medichema GmbH

- 6.4.17 Evonik Industries AG

- 6.4.18 Essentia Protein Solutions

- 6.4.19 PB Gelatins

- 6.4.20 NovaColl (Geltor)