|

시장보고서

상품코드

1906002

라이딩 기어 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Riding Gear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

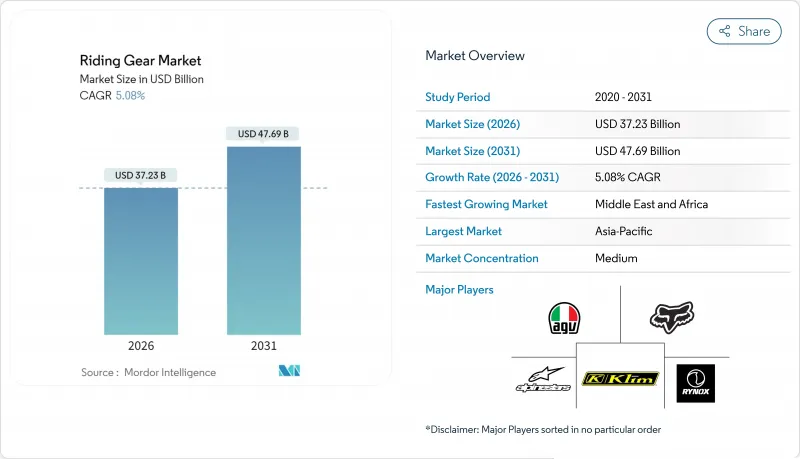

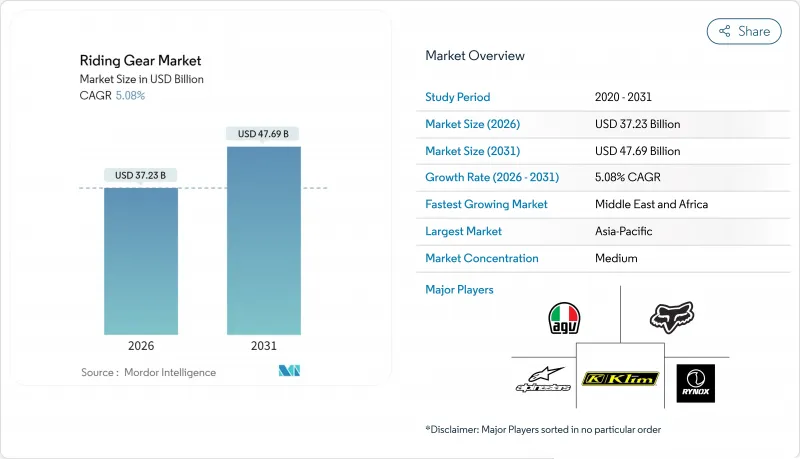

라이딩 기어 시장은 2025년에 354억 3,000만 달러로 평가되었고, 2026년 372억 3,000만 달러에서 2031년까지 476억 9,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년) 동안의 CAGR은 5.08%로 전망되고 있습니다.

헬멧 착용 의무화, 여성 라이더 증가, 에어백 재킷의 급속한 보급으로 수요 패턴이 변화하면서 이 부문은 기본적인 보호에서 혁신적이고 연결된 안전 생태계로 전환하고 있습니다. 탄소섬유 복합재나 전자센서와 같은 기술이 엘리트용 레이싱기어에서 일반제품으로 이동하는 가운데, 기술 주도의 차별화에 의해 프리미엄 부문과 일반 부문의 차이는 줄어들고 있습니다. 규제의 조화와 특히 EU 규칙 2016/425에 따른 CE 마킹의 도입으로 인증 기어가 라이프스타일의 선택이 아닌 법적 의무가 되면서 대상 시장이 확대되었습니다. 동시에 할리 데이비슨과 트라이엄프 등의 브랜드에 의한 OEM 라이프스타일 상품의 전개는 보호복과 패션의 경계를 허물어 거시 경제의 변동에도 불구하고 높은 평균 판매 가격을 뒷받침하고 있습니다. 분산된 경쟁환경은 가격경쟁을 지속적으로 높이고 있지만, 영국 운전자 및 차량 표준 기관(DVSA) 등 기관에 의한 모조품 단속은 소비자를 신뢰할 수 있는 브랜드로 회귀시켜 품질 중시의 구매행동을 강화하고 있습니다.

세계의 라이딩 기어 시장의 동향 및 인사이트

신흥 시장에서의 오토바이 소유 대수 증가

인도, 인도네시아, 베트남에서의 이륜차의 급격한 보급은 인증 헬멧, 재킷, 글러브의 신규 구매 수요를 창출하고, 선진국에서 수십년이 걸린 시장 형성을 불과 몇 시즌만에 달성하고 있습니다. 지난 1년간 인도의 전동이륜차 시장은 급성장하였고 소비자의 수용도 향상과 안전 장비의 잠재 고객층 확대가 현저합니다. 중국은 2024년에 방대한 수의 오토바이를 수출해 세계 출하 대수의 절반 이상을 차지하였으며, 라이딩 기어 시장의 양산 거점으로서의 지위를 강화하고 있습니다. 이들 국가에서는 자동차화와 병행하여 현대적인 안전규칙이 도입되기 때문에 보급곡선이 급속히 가파르게 변하여 인증 기어가 비브랜드 대체품을 역대 최대의 속도로 대체하고 있습니다. 열대 기후 및 가격에 민감한 고객을 위해 기능이 다양한 중간 가격대 제품 라인을 조정할 수 있는 제조업체는 소유 주기를 통해 지속되는 경향이 있는 조기 고객 충성도를 확보합니다.

보호 장비를 의무화하는 세계 안전 규제 강화

규제의 흐름은 권고에서 의무화로 이행을 계속하고 있습니다. 유럽위원회의 EN 17092 규격(2018년 시행)에서는 소매점이 판매 시점에서 표시를 의무화할 수 있는 검증 가능한 마모, 충격, 솔기 강도 단계가 도입되었습니다. 개인보호구 규칙(PPE)은 규정 미달에 대한 벌금을 강화하고 세관 검사장에서 기준 미달품의 수입을 사전에 차단하고 있습니다. 북미 기관은 유사한 ANSI/UL 프로토콜을 참고하고 있으며, 브라질과 인도네시아에서는 2026년 시행 예정인 유사 법령을 작성 중입니다. 컴플라이언스 요구사항은 최저 기술 기준을 끌어올려 자체 시험소 및 오랜 인증 기관 파트너십을 보유한 생산자에게 우위를 제공합니다. 인증 예산이 부족한 신규 진출기업은 확립된 브랜드의 프라이빗 브랜드 계약으로 이동하는 경향이 있으며, 제조 노하우가 소수의 기업에 집약되는 결과가 되고 있습니다. 중기적으로는 통일된 세계 기준에 의해 모조품 거래를 조장해 온 그레이 존이 축소되어, 프리미엄 기업은 법적 책임 리스크를 줄이면서, 종래의 고급 기술을 양산 모델에 전개하는 것이 가능하게 됩니다.

인증된 프리미엄 보호 장비의 높은 비용

인증 비용, 다층 소재의 비용, 브랜드 사용료가 합쳐 대폭적인 프리미엄이 발생하고, 신흥 시장의 일부 구입층을 가격면에서 배제하고 있습니다. 에어백 대응 가죽 재킷은 소매 가격 1,100달러(인도에서는 기본적인 통근용 오토바이의 가격에 해당)에 이르며, 라이더는 차량 구매와 종합적인 보호 사이에서 선택할 수 밖에 없습니다. 모듈 설계로 인해 교체 부품의 비용이 시간이 지남에 따라 감소하지만 초기 비용은 여전히 장벽이 되고, 특히 헬멧 착용 의무 규제가 주류 지역에서는 현저합니다. 제조업체는 마이크로 파이낸스 제휴나 구독 모델(복수 시즌에 지불을 분산)을 시험 도입하고 있지만, 북미 및 유럽 이외에서의 보급은 한정적입니다. 대규모 비용 혁신이 없이 조기 도입층이 포화 상태에 도달하면 프리미엄 부문의 성장이 둔화될 수 있습니다.

부문 분석

2025년 라이딩 기어 시장 규모에서 헬멧이 24.46%의 수익을 차지하여 여전히 주도적인 지위를 유지했습니다. 규제 요건과 보편적인 위험 인식을 통해 헬멧은 임의 구매품이 아니며, 사고 발생 시 또는 5년 사용 기한에 따른 예측 가능한 교환 주기를 보장합니다. 헬멧 기술은 고밀도 라이너, 회전력 완화 시스템, 통합형 헤드업 디스플레이로 진화하고 있으며, 각 기능은 평균 판매 가격을 밀어 올리면서도 판매 대수의 성장을 뒷받침합니다. 동시에 에어백 재킷 및 조끼 하위 부문은 5.29%의 연평균 복합 성장률(CAGR)로 확대가 전망되어, 모든 오토바이 스타일에 대응 가능한 인체 보호 솔루션에 대한 프리미엄 수요를 견인하고 있습니다.

통근자의 증가에 따라, 우선 엔트리 레벨의 풀 페이스 헬멧을 구입하고 가처분 소득이 향상되기 전에 풀 라이딩 슈트의 구입을 앞당기는 경향이 강해지고 있습니다. 이로 인해 구매주기가 분산되어 평생 고객 가치가 확대되고 있습니다. 레이싱 및 오프로드 경기는 계속 최첨단 기술 혁신을 견인하고 있으며 MotoGP 및 WorldSBK용 FIM 공인 규격이 2-3 시즌 이내에 소비자용 모델로의 기술 이전을 불러오고 있습니다. 유럽의 여러 서킷에서 헬멧 장착형 액션 카메라가 금지되면서 공기 역학 성능과 안전 인증에 대한 중시를 부각하고 간접적으로 제조업체의 순정 카메라 포트 수요를 밀어 올리고 있습니다. 이는 쉘 강도를 유지하면서 컨텐츠 제작자를 지원하는 동향입니다. 이러한 제품 유형의 차이는 헬멧이 라이딩 기어 시장의 기반을 뒷받침하는 반면 전자 에어백 시스템이 프리미엄 보호 시장을 형성하는 존재가 되고 있음을 보여줍니다.

2025년 시점에서 라이딩 기어 시장의 53.11%를 가죽 제품이 차지하였으며, 내마모성과 모터사이클 문화의 결합에 기초한 불변의 매력이 시장을 뒷받침하고 있습니다. 태닝 가공된 소가죽과 캥거루 가죽은 레이스 경기에서의 내구성으로 여전히 선호되고 있습니다. 그러나 환경문제에 대한 주목과 피혁비용의 상승에 의해 결정 구조를 모방하면서 CO2 배출량을 저감하는 배양 피혁이나 식물 유래 합성 소재로의 길이 열리고 있습니다. 탄소섬유 복합재는 CAGR 5.26%가 예상되며 가죽 중량의 불과 몇 분의 1로 충돌 에너지를 분산할 수 있습니다. 또한 이는 경량화를 조향 능력 향상으로 인식하는 고성능 라이더의 관심을 모으고 있습니다. 장갑과 부츠에 통합된 탄소 아라미드 직물은 초박형 보호층을 형성하여 충격 완화 성능을 손상시키지 않고 조작성을 뒷받침합니다. 케블러, 노멕스, 코듀라 섬유는 중간 가격대의 틈새 시장을 채우고 있으며, 세탁 가능하고 내후성이 뛰어난 대체품으로 온난한 기후에서의 라이딩 시즌을 확대합니다.

하이브리드 제조 기술에서는 활주 영역에 가죽 외장을 도입하면서, 충격 포인트에는 카본 파이버나 케블러 패널을 조합하여 안전성과 중량의 균형을 실현하고 모든 가격대에서 인기를 얻고 있습니다. 이 융합으로 공급망에 모듈성이 생겨 벤더는 규제 대상 지역이나 고객의 예산에 따라 소재 비율을 조정할 수 있게 되었습니다. 기존에는 폐기처분되고 있던 복합재에 대해 열분해나 화학적 탈중합에 의한 재활용 경로가 확립되고 있으며, 프리미엄 혁신성과 지속가능성에 대한 대처가 결합되어 젊은 라이더층의 공감을 불러오고 있습니다. 전반적으로 소재 기술의 진보로 전통적인 가죽 제품이 판매 수량으로 우위를 유지하면서 이익률과 브랜드 가치는 최첨단 복합 소재에 집중되는 추세에 있습니다.

지역별 분석

2025년 아시아태평양은 세계 수익의 38.55%를 차지하였고 중국의 3,676만대의 이륜차 수출과 인도의 급증하는 전동 이륜차 보급에 의해 다른 지역을 압도하는 단위 밀도를 실현했습니다. 이 지역의 라이딩 기어 시장의 규모는 정부가 라이더와 동승자 모두에게 규정 헬멧 착용을 의무화함으로써 혜택을 받아 보호 기준이 즉시 향상되었습니다. 현지 제조업체는 T-Mall이나 Flipkart 등 규제 대상 EC 플랫폼과의 제휴에 의해 급속하게 규모를 확대해, 종래는 비공식 유통에 의존하고 있던 교외 도시권으로의 도달을 확대하고 있습니다. 실 방적에서 최종 조립까지의 수직 통합으로 아시아 기업은 CE 적합성을 손상시키지 않고 수입품보다 낮은 가격설정이 가능해지면서 지역의 자급자족을 확고하게 하고 있습니다.

중동 및 아프리카는 2031년까지 연평균 복합 성장률(CAGR) 5.37%로 가장 빠른 성장을 보일 전망입니다. 카이로, 나이로비, 라고스에서는 인프라 정비와 라이드 공유 플랫폼의 보급에 의해 이륜 통근이 정착되고 있습니다. 걸프 국가의 부유층 애호가들은 유럽의 고급 브랜드를 선호하는 반면, 급성장하는 아프리카의 배송업체용 플릿은 열대 호우를 견디는 견고한 섬유 장비를 선호합니다. 개발기관은 기부금에 의한 헬멧 지원과 연동한 웨어러블 안전 장비의 조성을 추진해, 긱 이코노미의 라이더층에서 보호 재킷의 조기 보급을 촉진하고 있습니다. 한편, 라틴아메리카에서는 브라질과 콜롬비아를 중심으로 중간 정도의 단일 자릿수 성장을 기록하고 있습니다. 국내 의류 생산 능력이 수요의 5분의 3밖에 충족할 수 없기 때문에 인증된 유럽 및 아시아 제품의 수입 루트가 열리고 있습니다.

북미와 유럽은 성숙 시장이면서 수익성이 높으며, 교환 사이클은 평균 4-6년이지만 라이더는 안전성의 향상에 대해서 추가 비용을 기꺼이 지불합니다. 유로존의 인플레이션도 레벨 2 보호구와 내장 에어백에 대한 수요를 둔화시키지 못했으며 이는 고소득층에서의 가격 탄력성을 보여줍니다. 독일이 동계 통근용 온열 장갑에 2025년까지 적용하는 에코 보너스 등의 정책 틀은 자치체 규제가 재킷이나 헬멧 이외의 액세서리 보급을 촉진하는 좋은 예입니다. 전 지역에서 안전 기준의 세계화가 진행되면서 공급망은 균질화하면서도 기후의 다양성이 제품 개발에 지역별 특색을 남기고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 신흥 시장에서 오토바이 소유 대수 증가

- 보호구를 의무화하는 세계의 안전규제 강화

- 어드벤처 투어링 및 장거리 라이딩 문화 확산

- 오토바이 브랜드에 의한 OEM 라이프스타일 상품의 확대

- 에어백 내장 재킷의 가격 저하에 수반하는 급속한 보급

- 여성 라이더층의 확대에 수반하는 특화형 의류 수요

- 억제요인

- 인증된 프리미엄 보호 장비의 높은 비용

- 위조 CE 마크 제품의 만연에 의한 신뢰의 저하

- 한랭 지역에서의 계절성 수요의 감소

- 동물 유래 피혁 소재에 대한 지속가능성 반발

- 가치 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측(금액, 달러)

- 제품 유형별

- 재킷

- 헬멧

- 장갑

- 바지

- 부츠 및 슈즈

- 바디아머 및 프로텍터

- 에어백 재킷 및 조끼

- 재료별

- 가죽

- 섬유

- 메쉬

- 탄소섬유 복합재료

- 케블러 및 아라미드 혼방

- 기타 자료

- 유통 채널별

- 온라인

- 오프라인

- 최종 사용자별

- 온로드 주행

- 오프로드 및 모토 크로스

- 어드벤처 & 투어링

- 통근자

- 가격대별

- 프리미엄

- 미드레인지

- 이코노미

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- AGVSport

- Alpinestars SpA

- Dainese SpA

- Fox Racing Inc.

- Klim Technical Riding Gear

- REV'IT! Sport International

- ScorpionEXO

- Icon Motorsports

- Royal Enfield Gear

- HJC Helmets

- Shoei Co., Ltd.

- Arai Helmet Ltd.

- Bell Helmets

- Rynox Gears India Pvt. Ltd.

- Spartan ProGear Co.

- Kushitani Co., Ltd.

- Held GmbH

- Sena Technologies Inc.

- LS2 Helmets

- Studds Accessories Ltd.

- Komine Co., Ltd.

- Oxford Products Ltd.

- Thor MX

제7장 시장 기회 및 미래 전망

CSM 26.01.21The Riding Gear Market was valued at USD 35.43 billion in 2025 and estimated to grow from USD 37.23 billion in 2026 to reach USD 47.69 billion by 2031, at a CAGR of 5.08% during the forecast period (2026-2031).

Mandatory helmet laws, widening female rider participation, and rapid adoption of air-bag jackets have reshaped demand patterns, pivoting the category from basic protection toward innovative, connected safety ecosystems. Technology-led differentiation tightens the gap between premium and mass segments as carbon-fiber composites and electronic sensors migrate from elite racing gear to mainstream products. Regulatory harmonization, most notably CE Marking under Regulation (EU) 2016/425, has expanded the addressable base by making certified gear a legal necessity rather than a lifestyle choice. At the same time, OEM lifestyle merchandising by brands such as Harley-Davidson and Triumph is blurring the divide between protective apparel and aspirational fashion, sustaining higher average selling prices despite macro-economic volatility. Fragmented competition continues to spur price rivalry, yet counterfeit crackdowns by agencies like the U.K. Driver and Vehicle Standards Agency are steering consumers back to reputable labels, reinforcing quality-driven purchasing behavior.

Global Riding Gear Market Trends and Insights

Rising Motorcycle Ownership In Emerging Markets

Spiraling two-wheeler uptake in India, Indonesia, and Vietnam translates into first-time purchases of certified helmets, jackets, and gloves, compressing what took decades in developed economies into a few selling seasons. Over the past year, sales in India's electric two-wheeler market have surged, underscoring robust growth and heightened consumer acceptance, instantly widening the safety-gear addressable base. China exported a huge number of motorcycles in 2024, more than half of global unit shipments, strengthening the country's status as the volume engine of the riding gear market. Because these countries implement modern safety rules concurrently with motorization, penetration curves steepen quickly, letting certified gear displace unbranded alternatives in record time. Manufacturers able to calibrate feature-rich mid-range lines for tropical climates and price-sensitive customers are capturing early loyalty that tends to persist through the ownership cycle.

Stricter Global Safety Regulations Mandating Protective Gear

Regulatory momentum continues to move from recommendation toward obligation. The European Commission's EN 17092 classification, effective 2018, introduced verifiable abrasion, impact, and seam-strength gradations that retailers must display at point of sale. The Personal Protective Equipment Regulation amplifies penalties for non-compliance, pre-emptively banning sub-standard imports at customs checkpoints. North American agencies reference similar ANSI/UL protocols, while Brazil and Indonesia are drafting mirror statutes slated for 2026. Compliance requirements raise the minimum technological baseline and create a moat around producers with in-house testing labs or long-standing notified-body partnerships. Market entrants lacking certification budgets now pivot toward private-label contracts for established brands, effectively consolidating manufacturing know-how under fewer roof-tops. Over the medium term, uniform global standards shrink the gray zone that fueled counterfeit trade, allowing premium players to cascade former high-end technologies into volume ranges with reduced liability exposure.

High Cost Of Certified Premium Protective Gear

Certification fees, multi-layer material bills, and brand royalties add sizable premiums that price out a portion of emerging-market buyers. An airbag-ready leather jacket can retail at USD 1,100-nearly the same as a basic commuter motorcycle in India-forcing riders to choose between vehicle acquisition and comprehensive protection. While modular design lowers replacement part costs over time, initial outlay remains a sticking point, particularly where helmet-only laws dominate. Manufacturers experiment with micro-financing partnerships and subscription models that spread payments across riding seasons, but adoption has been limited outside North America and Europe. Absent large-scale cost innovation, premium growth could decelerate once early adopters saturate.

Other drivers and restraints analyzed in the detailed report include:

- Boom In Adventure-Touring And Long-Distance Riding Culture

- OEM Lifestyle Merchandise Expansion By Motorcycle Brands

- Proliferation Of Counterfeit Ce-Marked Products Eroding Trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The riding gear market size attributed to helmets remained dominant in 2025 as the category captured 24.46% of revenue. Regulatory mandates and universal risk acknowledgment ensure helmets remain non-discretionary, delivering predictable replacement cycles tied to crash events and five-year age limits. Helmet technology is evolving toward multi-density liners, rotational-force mitigation systems, and integrated heads-up displays, each feature nudging average selling prices upward without deterring unit growth. Simultaneously, the airbag jackets and vests sub-segment, forecast to expand at a 5.29% CAGR, channels premium demand toward torso protection solutions that can pair with any motorcycle style.

A growing segment of commuters now buys entry-level integral helmets first and postpones full riding suits until disposable income improves, creating staggered purchase cycles that enlarge lifetime customer value. Racing and off-road disciplines continue to dictate top-tier innovation, with FIM homologation for MotoGP and WorldSBK feeding trickle-down tech to consumer models within two to three seasons. Helmet-mounted action-camera bans in several European tracks emphasize the premium placed on aerodynamics and safety certification, indirectly lifting demand for factory-integrated camera ports, which maintain shell integrity while serving content creators. Collectively, these product-type nuances affirm that while helmets secure the broad base of the riding gear market, electronic airbag systems increasingly frame the narrative around premium protection.

Leather accounted for 53.11% of the riding gear market share in 2025, underscoring its enduring appeal built on abrasion resistance and cultural association with motorcycling. Tanned cowhide and kangaroo leather remain favored in racing for their slide durability. Still, environmental scrutiny and rising hide costs are opening avenues for lab-grown or plant-based synthetics that mimic grain structure while lowering CO2 footprints. Carbon-fiber composites, projected for a 5.26% CAGR, achieve crash energy dispersion at fractions of leather's weight, capturing the imagination of performance riders who equate reduced mass with handling gains. Integrated carbon-aramid weaves in gloves and boots yield ultra-thin protective layers, supporting dexterity without sacrificing impact mitigation. Kevlar, Nomex, and Cordura textiles fill the mid-market niche, offering washable, weather-proof alternatives that expand riding seasons in temperate climates.

Hybrid manufacturing combines leather exteriors for slide zones with carbon-fiber or Kevlar panels over impact points, achieving a safety-weight equilibrium that appeals across price tiers. Such fusion builds modularity into supply chains, letting vendors dial material splits based on regulatory destination and customer budget. Recycling pathways for composite off-cuts traditionally landfill waste are emerging through pyrolysis and chemical depolymerization, aligning premium innovation with sustainability credentials that resonate with younger riders. Altogether, material advancements ensure that heritage-rich leather continues to dominate unit volumes, yet cutting-edge composites are where margins and branding prestige now concentrate.

The Riding Gear Market Report is Segmented by Product Type (Jackets and More), Material (Leather, Textile, and More), Distribution Channel (Online and Offline), End-User (On-Road Riding, Off-road/Motocross, and More), Price Range (Premium, Mid-Range, and Economy), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 38.55% of global revenue in 2025, rivaled by no other region in sheer unit density due to China's 36.76 million motorcycle exports and India's surging electric two-wheeler adoption. The riding gear market size in the area benefits from governments enforcing the use of certified helmets for riders and pillion riders alike, instantly elevating baseline protection standards. Local manufacturers scale rapidly by partnering with regulated e-commerce platforms, such as T-Mall and Flipkart, thereby amplifying their reach to peri-urban clusters that were previously dependent on informal channels. Vertical integration-from yarn spinning to final assembly enables Asian companies to undercut imported gear without compromising CE compliance, thereby cementing regional self-sufficiency.

The Middle East and Africa region registers the fastest 5.37% CAGR through 2031 as infrastructural upgrades and ride-sharing platforms normalize two-wheel commuting across Cairo, Nairobi, and Lagos. Gulf states' affluent hobbyist riders gravitate toward premium European labels, yet burgeoning African courier fleets prefer rugged textile gear capable of enduring tropical downpours. Development agencies advocate wearable safety grants in conjunction with donor-funded helmets, fostering early adoption of protective jackets among gig-economy riders. Meanwhile, Latin America records mid-single digit growth anchored by Brazil and Colombia, where domestic apparel capacity meets only three-fifth of demand, opening import lanes for certified European and Asian products.

North America and Europe remain mature but lucrative; replacement cycles average 4-6 years, but riders willingly pay premiums for incremental safety gains. Eurozone inflation has not dampened demand for Level-2 armor and integrated airbags, indicating price elasticity in upper-income segments. Policy tools such as Germany's 2025 eco-bonus for electrically heated gloves during winter commuting illustrate how municipal regulations can nudge accessory uptake beyond core jackets and helmets. Across all geographies, convergence toward global safety standards homogenizes supply chains, yet climatic diversity keeps product development regionally nuanced.

- AGVSport

- Alpinestars S.p.A.

- Dainese S.p.A.

- Fox Racing Inc.

- Klim Technical Riding Gear

- REV'IT! Sport International

- ScorpionEXO

- Icon Motorsports

- Royal Enfield Gear

- HJC Helmets

- Shoei Co., Ltd.

- Arai Helmet Ltd.

- Bell Helmets

- Rynox Gears India Pvt. Ltd.

- Spartan ProGear Co.

- Kushitani Co., Ltd.

- Held GmbH

- Sena Technologies Inc.

- LS2 Helmets

- Studds Accessories Ltd.

- Komine Co., Ltd.

- Oxford Products Ltd.

- Thor MX

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Motorcycle Ownership In Emerging Markets

- 4.2.2 Stricter Global Safety Regulations Mandating Protective Gear

- 4.2.3 Boom In Adventure-Touring And Long-Distance Riding Culture

- 4.2.4 OEM Lifestyle Merchandise Expansion By Motorcycle Brands

- 4.2.5 Rapid Adoption Of Airbag-Integrated Jackets After Price Drop

- 4.2.6 Growing Female Rider Segment Demanding Tailored Apparel

- 4.3 Market Restraints

- 4.3.1 High Cost Of Certified Premium Protective Gear

- 4.3.2 Proliferation Of Counterfeit Ce-Marked Products Eroding Trust

- 4.3.3 Seasonality Dampening Demand In Cold Regions

- 4.3.4 Sustainability Backlash Against Animal-Based Leather Materials

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Product Type

- 5.1.1 Jackets

- 5.1.2 Helmets

- 5.1.3 Gloves

- 5.1.4 Pants / Trousers

- 5.1.5 Boots / Shoes

- 5.1.6 Body Armor & Protectors

- 5.1.7 Airbag Jackets & Vests

- 5.2 By Material

- 5.2.1 Leather

- 5.2.2 Textile

- 5.2.3 Mesh

- 5.2.4 Carbon-Fiber Composites

- 5.2.5 Kevlar / Aramid Blends

- 5.2.6 Other Materials

- 5.3 By Distribution Channel

- 5.3.1 Online

- 5.3.2 Offline

- 5.4 By End-user

- 5.4.1 On-road Riding

- 5.4.2 Off-road / Motocross

- 5.4.3 Adventure & Touring

- 5.4.4 Commuter

- 5.5 By Price Range

- 5.5.1 Premium

- 5.5.2 Mid-range

- 5.5.3 Economy

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 AGVSport

- 6.4.2 Alpinestars S.p.A.

- 6.4.3 Dainese S.p.A.

- 6.4.4 Fox Racing Inc.

- 6.4.5 Klim Technical Riding Gear

- 6.4.6 REV'IT! Sport International

- 6.4.7 ScorpionEXO

- 6.4.8 Icon Motorsports

- 6.4.9 Royal Enfield Gear

- 6.4.10 HJC Helmets

- 6.4.11 Shoei Co., Ltd.

- 6.4.12 Arai Helmet Ltd.

- 6.4.13 Bell Helmets

- 6.4.14 Rynox Gears India Pvt. Ltd.

- 6.4.15 Spartan ProGear Co.

- 6.4.16 Kushitani Co., Ltd.

- 6.4.17 Held GmbH

- 6.4.18 Sena Technologies Inc.

- 6.4.19 LS2 Helmets

- 6.4.20 Studds Accessories Ltd.

- 6.4.21 Komine Co., Ltd.

- 6.4.22 Oxford Products Ltd.

- 6.4.23 Thor MX

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment