|

시장보고서

상품코드

1906009

의료용 가스 및 장비 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Medical Gases And Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

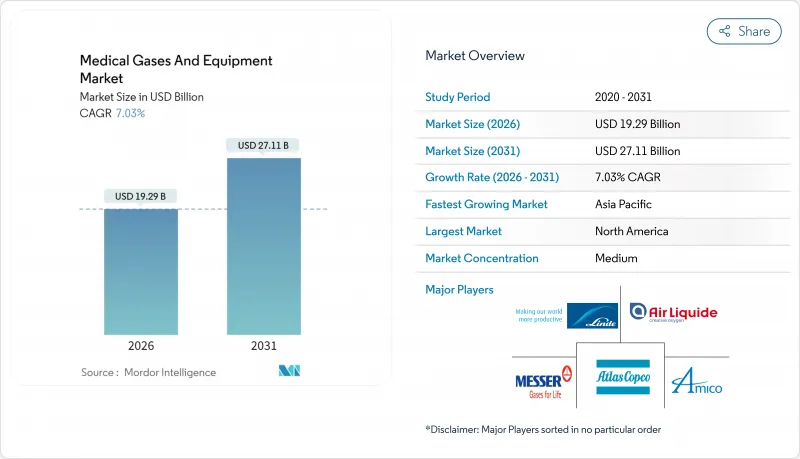

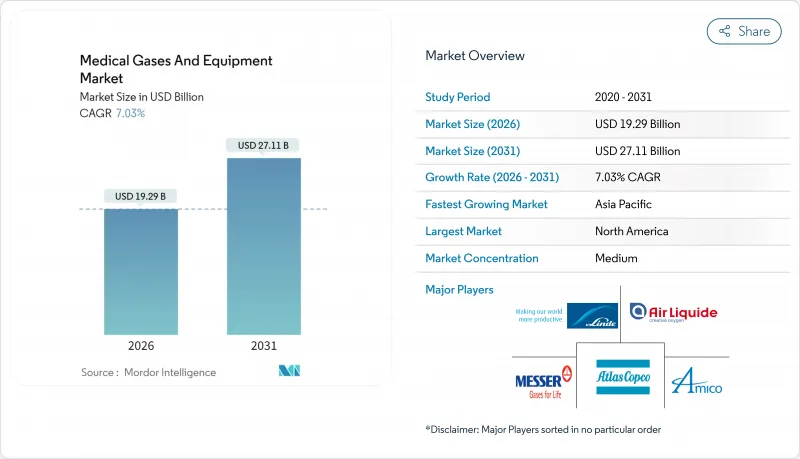

의료용 가스 및 장비 시장은 2025년의 180억 2,000만 달러에서 2026년에는 192억 9,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR7.03%로 성장을 지속하여, 2031년까지 271억 1,000만 달러에 달할 전망입니다.

고령화에 따른 치료 수요 증가, COVID-19 이후 병원 인프라의 꾸준한 업데이트, 휴대용 농축기의 급속한 혁신은 의료용 가스 및 장비 시장의 지속적인 확대를 뒷받침합니다. 정부가 지원하는 산소 공급 안정화 프로젝트, 웨어러블 센서의 소형화, 저GWP 마취 혼합 가스의 상업화가 수요 증가를 촉진하는 한편, 가스 공급업체는 서로 간의 통합을 통해 규모의 경제를 활용하여 급성기 의료시설 전체에서 장기 계약을 확보하고 있습니다. 장비 제조업체는 여전히 분산 상태에 있으며, 특히 고성장 아시아태평양 시장에서 제품 포트폴리오의 심화와 지리적으로 분산된 서비스 네트워크 구축을 목적으로 한 볼트온 인수의 여지가 발생하고 있습니다. 재택 치료로의 지속적인 전환은 봄베 충전, 소규모 현장 생산, AI를 활용한 모니터링 수요를 확대하고, 이들 전체가 의료용 가스 및 장비 시장의 경쟁 구도를 형성하고 있습니다.

세계의 의료용 가스 및 장비 시장의 동향 및 전망

재택 치료 및 POC 산소 요법의 수요 증가

메디케어의 36개월 렌탈 프레임워크는 예측 가능한 환급을 뒷받침하고 공급자의 휴대형 기기에 대한 투자를 촉진함과 동시에 가정용 산소 요법에 대한 환자의 수용성을 강화하고 있습니다. FlexO2 플로우 셀렉터와 같은 기술은 사용자의 조정 능력을 두 배로 확대하여 임상 도입 후 활동 능력 점수의 인식치를 80포인트 향상시켰습니다. 최적화된 제올라이트 베드를 탑재한 휴대형 농축기는 현재 98.68%의 산소 정밀도를 실현하여 거치형 시스템과의 성능 격차를 점점 줄이고 있습니다. 재택 치료 분야에서 예상되는 13.01%의 연평균 복합 성장률(CAGR)은 이러한 개선이 환자의 친숙한 환경에 대한 선호도와 일치하는 것을 보여줍니다. CMS의 2025년 지불 개정에 의한 2.5%의 재택 치료 수가 인상은 분산형 의료 모델에 한층 더 추진력을 부여합니다. 린데사의 수면 무호흡증 환자용 AIRGENIOUS 파일럿 사업은 CPAP 비준수율을 저감시켜 만성 질환 치료의 준수를 위한 예측 분석의 효능을 입증했습니다.

호흡기 질환 증가세

산소 입원의 주요인은 여전히 COPD이며 3차 병원에서 호흡기 병동 환자 수의 44.5%를 차지하고 있습니다. 전형적인 침상 패널 가스 수요는 연간 평균 산소 350m3, 의료용 공기 325m3이며, 이는 퇴원 환자 수와 수술 건수에 비례하여 증가합니다. 유럽의 정책 수립기관은 이미 오스트리아의 마스터 플랜 2025에 밝혀진 대로 의료 가스 시스템의 업그레이드를 국가 호흡기 전략과 통합하고 있습니다. 팬데믹 동안의 수요 급증을 분석한 결과 산소 소비량은 최대 20배까지 증가하여 공급 인프라에서 영구적인 잉여량 확보의 필요성이 밝혀졌습니다. 폴란드의 '의료 요구 맵' 이니셔티브는 호흡기 질환의 매핑이 병원 수준에서 가스 시스템 투자를 어떻게 유도하는지를 보여줍니다.

다중 관할 구역에 걸친 엄격한 cGMP 및 약전 규정 준수

2025년 12월에 발효된 FDA 최종 규정으로 의료용 가스에 대한 현행의 적절한 제조 규범(cGMP) 및 표시 프로토콜의 완전한 준수가 의무화되어 공급자에게는 충전 및 분석 시스템의 업그레이드 투자가 요구됩니다. 홍콩에서는 2026년 6월부터 의료용 가스를 의약품으로 분류하여 유통업체를 위한 새로운 라이선싱 제도를 도입합니다. 병렬 개정은 ISO 기반 의료기기 품질 관리와 cGMP의 명확화를 조화시켜 크로스보더 컴플라이언스 비용이 상승하고 세계 표준의 수렴을 촉진합니다.

부문 분석

의료용 고순도 가스는 2025년 시점에서 의료용 가스 및 장비 시장의 37.12%를 차지하였고 이는 병원에서 가정 환경에 이르는 필수적인 치료 용도를 반영하고 있습니다. 산소는 재택 치료의 보급 확대와 호흡기 질환 증가를 배경으로 8.82%의 연평균 복합 성장률(CAGR)이 전망됩니다. 의료용 공기, 이산화탄소, 헬륨 및 특수 가스는 외과적 통기, 진단, MRI의 요구에 대응하고 있지만, 헬륨 공급의 불안정성이 가격 상승을 초래해 병원 예산을 압박하고 있습니다. 아산화질소의 소비는 UCSF가 80-90% 저감에 성공한 사례에 따라 각 시설이 배관 라인을 철거하여 폐기물을 줄이는 가운데 휴대용 실린더로 이행하고 있습니다.

보완적인 의료용 가스 장비는 압축기 및 실린더에서 배관 모니터링 시스템에 이르기까지 다양합니다. 2023년 Atlas Copco의 Medi-teknique 인수는 서비스 폭과 지속적인 유지보수 수익을 목표로 하는 업계 재편의 사례입니다. 비콘 메디에스의 세계 판매망은 신축 병원 건설 시 진공 및 매니폴드 시스템을 통합하여 멀티 모드 광섬유 링 네트워크를 활용한 실시간 경보 기능을 실현하고 있습니다. 지속가능성에 대한 관심이 높아짐에 따라 병원에서는 저GWP 마취혼합 가스의 도입이 진행되고 있습니다. 유럽 규제 당국은 지구 온난화 계수가 상당히 낮은 세보플루란을 데스플루란보다 권장하고 있으며, 이에 따라 공급업체는 휘발성 약제용 회수 및 스캐벤징 시스템의 재설계를 요구받고 있습니다.

2025년 시점에서 패키지 실린더는 45.05%의 점유율을 유지했지만, 환자의 이동성에 대한 요구와 의료 제공자의 비용 효율적인 만성기 의료 모델의 중시에 의해 휴대용 농축 장치는 연률 9.67%의 성장할 것으로 전망되고 있습니다. 텍사스 A&M 대학의 계산 설계는 동적 제올라이트 구성이 변동하는 환자의 요구에 맞게 산소 유량을 조정할 수 있음을 보여주었습니다. 이에 따라 순도를 유지하면서 경량화를 실현하게 되었습니다. 한편 린데는 2024년 59건의 소규모 현장 플랜트 수주를 기록했으며, 이는 공급장애에 대비한 자립형 산소공급능력에 대한 병원의 관심을 반영하고 있습니다.

예측 가능한 단위 비용을 요구하는 대규모 3차 병원에서는 현장에서의 벌크 생산이 계속 뒷받침되고 있습니다. 한편, 초고순도를 필요로 하는 전문의료센터에서는 액체 벌크 공급이 주류입니다. 실린더의 백업 수요가 지속됨에 따라 모든 치료 형태에서 안정적인 수요가 보장되어 의료용 가스 및 장비 시장에서의 수익 구조 다양화가 확고해지고 있습니다.

지역별 분석

북미는 2025년 수익의 35.25%를 차지하였으며 성숙한 지불자 시스템, 엄격한 FDA 감독, 휴대형 농축장치의 보급이 성장 기반이 되고 있습니다. 병원에서는 온사이트 벌크 탱크에 의한 중복 산소 생산 능력을 유지하고 CMS(의료 보험 서비스 센터)가 환급 제도를 정교화하는 가운데 재택 치료의 성장은 지속적으로 높아지고 있습니다. 지역 장비 공급업체는 모호한 시장 접근 규칙 없이 혁신을 평가하는 명확한 규제 경로의 혜택을 누리고 있습니다.

아시아태평양은 대규모 병원 확장, 노령화, 의료 인프라에 대한 적극적인 정부 자금 투입을 통해 전 지역에서 가장 높은 13.19%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 인도에서는 병상 17,800개 증가를 목표로 하는 설계화와 500억 달러 규모의 의료기기 로드맵이 책정되어 배관 시스템과 실린더에 대한 잠재적인 수요 급증을 보여주고 있습니다. 중국에서는 2024년 이후의 지원적인 조달 정책에 의해 2025년에 의료기기 지출이 확대된 것으로 나타났으며, 이 지역의 주요 성장 엔진으로서의 지위를 강화하고 있습니다. 린데와 메사가 인도 및 동남아시아 전역에서 공기 분리장치를 확장하려는 계획은 지역적인 공급 안정성을 유지하는 공급업체의 노력을 보여줍니다.

유럽은 여전히 주요 시장이며 저GWP 마취제의 채택을 가속화하는 엄격한 환경 규제에 주력하고 있습니다. 영국 NHS에 의한 데스플루란 금지 정책은 대륙 전체의 의료 현장으로 파급되어, 공급자에게는 제제 변경을, 병원에는 회복실 시스템의 업그레이드를 촉구하고 있습니다. 에어 리퀴드가 프랑스, 독일, 브라질에서 체결한 저탄소 산소 공급 계약은 공립 병원 조달 기준에서 스코프 3 배출량의 중요성이 높아지고 있음을 나타냅니다.

중동, 아프리카 및 남미는 높은 잠재성을 지니며 모든 부문에서 초기 단계 시장입니다. 3차 의료시설에 대한 투자와 약국 기준의 점진적인 조화에 의해 새로운 기회가 창출될 것으로 예상되나 경제의 변동성 및 환급 제도의 단편화가 단기적인 규모 확대를 억제하는 요인이 됩니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 재택 치료 및 POC 산소 요법의 수요 증가

- 호흡기 질환 증가세

- COVID-19 후의 정부 자금에 의한 산소 인프라 정비

- 휴대형 및 웨어러블형 농축 장치 및 센서의 소형화

- 환경 친화적인 저GWP 마취 혼합 가스의 상업화

- AI를 활용한 예측형 가스 파이프라인 모니터링 및 재고 관리

- 억제요인

- 복수 관할 구역에서의 엄격한 cGMP 및 약전 준수

- 장기적인 가정용 산소 요법에 대한 환급 제한

- 벌크 가스 취급에 대한 안전상 책임 및 보험 비용

- 헬륨 공급의 불안정성으로 인한 특수 가스 비용 상승

- Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측(금액, 달러)

- 제품별

- 의료용 가스

- 의료용 고순도 가스

- 산소

- 아산화질소

- 의료용 공기

- 이산화탄소

- 헬륨 및 특수 가스

- 의료용 혼합 가스

- 생물학적 환경

- 의료용 고순도 가스

- 의료용 가스 기기

- 압축기

- 실린더

- 호스 어셈블리 및 밸브

- 마스크 및 캐뉼라

- 흡입 시스템

- 매니폴드 및 파이프라인 시스템

- 경보 및 감시 시스템

- 의료용 가스

- 모달리티별

- 대량 온사이트 생산

- 패키지 실린더

- 액체 및 벌크 공급

- 휴대용 농축장치

- 용도별

- 치료

- 진단 및 이미징

- 제약 제조 및 연구

- 동결수술 및 동결요법

- 재택 치료

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 재택 의료 환경

- 학술기관 및 연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Linde plc

- Air Liquide

- Air Products & Chemicals

- Messer Group

- Taiyo Nippon Sanso

- Atlas Copco

- BeaconMedaes

- Amico Group

- Matheson Tri-Gas

- GCE Group

- NOVAIR

- Luxfer Gas Cylinders

- Getinge AB

- Dragerwerk AG

- INOX Air Products

- South African Oxygen(Afrox)

- Gulf Cryo

- Coregas Pty

- SOL Group

- Air Water Inc.

- Invacare Corporation

제7장 시장 기회 및 미래 전망

CSM 26.01.21The Medical Gases And Equipment Market is expected to grow from USD 18.02 billion in 2025 to USD 19.29 billion in 2026 and is forecast to reach USD 27.11 billion by 2031 at 7.03% CAGR over 2026-2031.

Rising therapeutic demand from aging populations, steady hospital infrastructure upgrades after COVID-19, and rapid innovation in portable concentrators underpin sustained expansion of the medical gases and equipment market. Government-supported oxygen resilience projects, miniaturization of wearable sensors, and the commercialization of low-GWP anesthetic blends further reinforce volume growth, while consolidated gas suppliers leverage scale to secure long-term contracts across acute-care settings. Equipment makers remain fragmented, creating space for bolt-on acquisitions that deepen product portfolios and geographically diversified service footprints, especially in high-growth Asia-Pacific markets. The continued shift toward home-based care amplifies cylinder refilling, small on-site generation, and AI-enabled monitoring demand, collectively shaping the competitive contours of the medical gases and equipment market.

Global Medical Gases And Equipment Market Trends and Insights

Rising Demand for Home Healthcare & POC Oxygen Therapy

Medicare's 36-month rental framework underpins predictable reimbursement, encouraging supplier investment in portable devices and reinforcing patient acceptance of at-home oxygen therapy.Technology such as FlexO2 flow selectors has doubled user-initiated adjustments, raising perceived activity capacity scores by 80 points after clinical deployment.Portable concentrators that use optimized zeolite beds now deliver 98.68% oxygen accuracy, narrowing the performance gap with stationary systems. A 13.01% CAGR in the home-care segment illustrates how these improvements align with patient preference for familiar environments. CMS's 2025 payment update, lifting home health rates by 2.5% adds further momentum to decentralized care models. Linde's AIRGENIOUS pilot among sleep-apnea users cut CPAP non-compliance, showcasing predictive analytics for chronic-care adherence.

Growing Prevalence of Respiratory Diseases

COPD remains the chief driver of oxygen admissions, representing 44.5% of respiratory ward volume in tertiary hospitals. Typical bed-based gas demand averages 350 m3 oxygen and 325 m3 medical air each year, scaling directly with discharge volumes and surgical intensity. European planners have already embedded medical gas system upgrades into national respiratory strategies, as shown in the Austrian Masterplan 2025. Analysis of pandemic surges revealed oxygen consumption rising up to 20-fold, anchoring the need for permanent redundancy in supply infrastructure. Poland's Maps of Health Needs initiative highlights how respiratory disease mapping guides investment in gas systems at hospital level.

Stringent Multi-Jurisdictional cGMP & Pharmacopeia Compliance

The FDA's final rule, effective December 2025, mandates full current good manufacturing practice and labeling protocols for medical gases, compelling suppliers to invest in upgraded filling and analytical systems. Hong Kong will classify medical gases as pharmaceutical products from June 2026, introducing a new licensing layer for distributors. Parallel amendments harmonize ISO-based device quality management with cGMP clarifications, raising cross-border compliance costs yet fostering global standard convergence.

Other drivers and restraints analyzed in the detailed report include:

- Government-Funded Oxygen Infrastructure Build-Outs Post-COVID

- Miniaturization of Portable/Wearable Concentrators & Sensors

- Limited Reimbursement for Long-Term Home Oxygen Therapy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pure Medical Gases captured 37.12% of the medical gases and equipment market in 2025, reflecting indispensable therapeutic use across hospitals and home settings. Oxygen is projected to record an 8.82% CAGR, aided by expanding home-care adoption and respiratory disease prevalence. Medical Air, Carbon Dioxide, and Helium & Specialty Gases serve surgical insufflation, diagnostics, and MRI needs, though helium supply volatility has driven price escalations that strain hospital budgets. Nitrous Oxide consumption is shifting toward portable cylinders as institutions remove piped lines to curb waste, following UCSF's 80-90% reduction success.

Complementary medical gas equipment ranges from compressors and cylinders to pipeline monitoring systems. Atlas Copco's 2023 Medi-teknique acquisition illustrates consolidation aimed at service breadth and recurring maintenance revenue. BeaconMedaes' global distributor network embeds vacuum and manifold systems within new hospital builds, leveraging multi-mode optical fiber ring networks for real-time alarm capabilities. A rising focus on sustainability is prompting hospitals to adopt low-GWP anesthetic blends. European regulators endorse sevoflurane over desflurane because of its far lower global-warming potential, nudging suppliers to re-engineer recovery and scavenging systems for volatile agents.

Packaged Cylinders retained a 45.05% share in 2025, yet Portable Concentrators are forecast to grow 9.67% annually as patients demand mobility and healthcare providers emphasize cost-effective chronic-care models. Computational design by Texas A&M shows that dynamic zeolite configurations can tailor oxygen flow to fluctuating patient needs, reducing weight without cutting purity. Meanwhile, Linde recorded 59 small on-site plant wins in 2024, reflecting hospital interest in self-reliant oxygen capacity to hedge against supply disruptions.

Bulk on-site generation continues to attract large tertiary hospitals seeking predictable unit costs, whereas liquid bulk delivery supports specialty centers with ultra-high purity requirements. The continued preference for cylinder backup ensures steady demand across every modality, cementing a diversified revenue mix within the medical gases and equipment market.

The Medical Gases and Equipment Market Report is Segmented by Product (Medical Gases [Pure Medical Gases, and More], and Medical Gas Equipment [Compressors, and More]), Modality (Bulk On-Site Generation, and More), Application (Therapeutic, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 35.25% of 2025 revenue, anchored by mature payer systems, strict FDA oversight, and widespread adoption of portable concentrators. Hospitals maintain redundant oxygen generation backed by on-site bulk tanks, while home-care penetration continues to rise as CMS refines reimbursement. Regional equipment vendors benefit from clear regulatory pathways that reward innovation without ambiguous market access rules.

Asia-Pacific is projected to grow at 13.19% CAGR, the highest among all regions, driven by large-scale hospital expansion, aging populations, and proactive government funding for medical infrastructure. India's planned capacity additions of 17,800 beds alongside a USD 50 billion medical device roadmap illustrate the underlying demand surge for pipeline systems and cylinders. China's supportive procurement policies post-2024 are expected to unlock medical device spending in 2025, reinforcing the region's status as the foremost growth engine. Air separation unit expansions by Linde and Messer across India and Southeast Asia signal supplier commitment to sustaining regional supply security.

Europe remains a major market, propelled by stringent environmental mandates that accelerate low-GWP anesthesia adoption. The NHS elimination of desflurane has cascaded across continental practice, compelling suppliers to reformulate and hospitals to upgrade recovery systems. Air Liquide's low-carbon oxygen supply contracts in France, Germany, and Brazil showcase the rising importance of Scope 3 emissions in public hospital procurement criteria.

Middle East & Africa and South America collectively represent high-potential but early-stage markets. Investments in tertiary care facilities and the gradual harmonization of pharmacopeia standards will unlock incremental opportunities, although economic volatility and reimbursement fragmentation temper near-term scale.

- Linde plc

- Air Liquide

- Air Products & Chemicals

- Messer Group

- Taiyo Nippon Sanso

- Atlas Copco

- Beckton Dickinson

- Amico Group

- Matheson Tri-Gas

- GCE Group

- NOVAIR

- Luxfer Gas Cylinders

- Getinge

- Dragerwerk AG

- INOX Air Products

- South African Oxygen (Afrox)

- Gulf Cryo

- Coregas Pty

- SOL Group

- Air Water Inc.

- Invacare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Home Healthcare & POC Oxygen Therapy

- 4.2.2 Growing Prevalence of Respiratory Diseases

- 4.2.3 Government-Funded Oxygen Infrastructure Build-Outs Post-COVID

- 4.2.4 Miniaturization of Portable/ Wearable Concentrators & Sensors

- 4.2.5 Commercialization of Eco-Friendly Low-GWP Anaesthesia Gas Blends

- 4.2.6 AI-Enabled Predictive Gas-Pipeline Monitoring & Inventory Control

- 4.3 Market Restraints

- 4.3.1 Stringent Multi-Jurisdictional cGMP & Pharmacopeia Compliance

- 4.3.2 Limited Reimbursement for Long-Term Home Oxygen Therapy

- 4.3.3 Workplace-Safety Liability & Insurance Costs for Bulk-Gas Handling

- 4.3.4 Helium Supply Volatility Driving Up Specialty-Gas Costs

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product

- 5.1.1 Medical Gases

- 5.1.1.1 Pure Medical Gases

- 5.1.1.1.1 Oxygen

- 5.1.1.1.2 Nitrous Oxide

- 5.1.1.1.3 Medical Air

- 5.1.1.1.4 Carbon Dioxide

- 5.1.1.1.5 Helium & Specialty Gases

- 5.1.1.2 Medical Gas Mixtures

- 5.1.1.3 Biological Atmosphere

- 5.1.1.1 Pure Medical Gases

- 5.1.2 Medical Gas Equipment

- 5.1.2.1 Compressors

- 5.1.2.2 Cylinders

- 5.1.2.3 Hose Assemblies & Valves

- 5.1.2.4 Masks & Cannulas

- 5.1.2.5 Vacuum & Suction Systems

- 5.1.2.6 Manifold & Pipeline Systems

- 5.1.2.7 Alarm & Monitoring Systems

- 5.1.1 Medical Gases

- 5.2 By Modality

- 5.2.1 Bulk On-site Generation

- 5.2.2 Packaged Cylinders

- 5.2.3 Liquid/Bulk Delivery

- 5.2.4 Portable Concentrators

- 5.3 By Application

- 5.3.1 Therapeutic

- 5.3.2 Diagnostic & Imaging

- 5.3.3 Pharmaceutical Manufacturing & Research

- 5.3.4 Cryosurgery & Cryotherapy

- 5.3.5 Home Healthcare

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Home Care Settings

- 5.4.4 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Linde plc

- 6.3.2 Air Liquide

- 6.3.3 Air Products & Chemicals

- 6.3.4 Messer Group

- 6.3.5 Taiyo Nippon Sanso

- 6.3.6 Atlas Copco

- 6.3.7 BeaconMedaes

- 6.3.8 Amico Group

- 6.3.9 Matheson Tri-Gas

- 6.3.10 GCE Group

- 6.3.11 NOVAIR

- 6.3.12 Luxfer Gas Cylinders

- 6.3.13 Getinge AB

- 6.3.14 Dragerwerk AG

- 6.3.15 INOX Air Products

- 6.3.16 South African Oxygen (Afrox)

- 6.3.17 Gulf Cryo

- 6.3.18 Coregas Pty

- 6.3.19 SOL Group

- 6.3.20 Air Water Inc.

- 6.3.21 Invacare Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment