|

시장보고서

상품코드

1906010

전자의무기록 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Electronic Medical Records - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

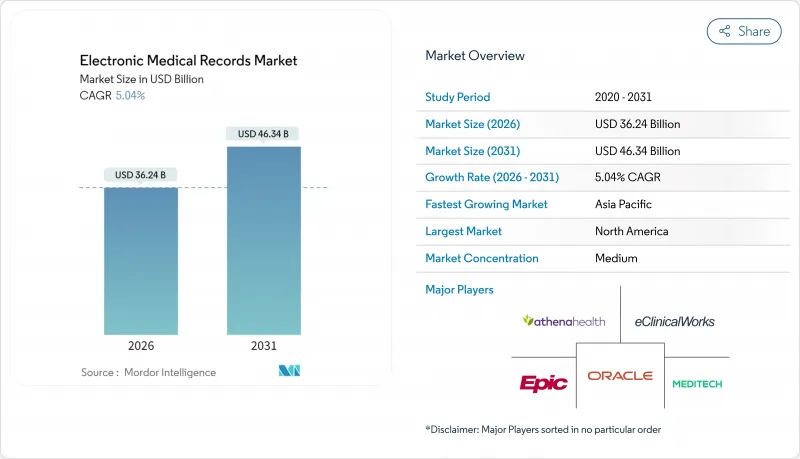

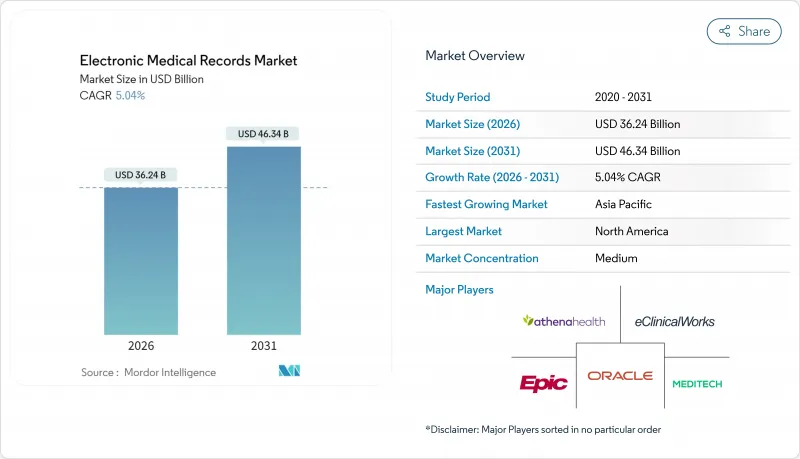

전자의무기록 시장은 2025년 345억 달러에서 2026년 362억 4,000만 달러로 성장하고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 5.04%로 성장을 지속하여 2031년까지 463억 4,000만 달러에 달할 것으로 예측되고 있습니다.

성장을 뒷받침하는 여러 요인 가운데 현대 환급 제도는 데이터 중심 의료를 평가하고, 병원 및 클리닉이 AI 대응 능력을 획득하기 위해 1세대 시스템을 업데이트하며, 지불 기관은 사전 승인 결정을 위해 상호 운용 가능한 기록을 점점 더 요구하고 있습니다. 클라우드 인프라에 대한 투자 증가로 의료 제공자는 IT 비용을 줄이면서 다직종 팀에 대한 접근을 확대할 수 있습니다. 게다가 이용 사례가 증가함에 따라 적절하게 구현된 EMR이 약물 오투여 감소, 입원기간 단축, 수익주기 개선에 기여하는 것으로 입증되었으며, 도입이 지연된 의료기관에서도 도입을 가속화하고 있습니다. 이러한 동향을 종합하면 전자의무기록 시장은 디지털 건강 변화의 기초가 되는 중요한 축으로 자리매김하고 있습니다.

세계의 전자의무기록 시장의 동향 및 인사이트

AI를 활용한 임상 의사결정 지원이 EMR의 가치 제안을 강화

의료기관 경영진은 인공지능을 최우선 투자 대상 중 하나로 고려하고 있습니다. 인공지능에 내장된 알고리즘은 수동적인 기록을 능동적인 임상 파트너로 전환합니다. 미국 식품의약국(FDA)은 이미 부정맥 검출에서 자동 이미지 라벨링에 이르기까지 EMR 워크플로와 직접 협력하는 1,000대 이상의 AI 탑재 장비를 승인했습니다. 예를 들어 마운트 사이나이 병원의 GLUCOSE 모델은 집중 치료실(ICU) 시험에서 경험이 풍부한 임상의를 능가하는 정확도로 인슐린 투여 오차를 줄이고 원활한 기록 통합을 실현하고 있습니다. Oracle 헬스의 차세대 클라우드 기반 전자의무기록(EHR)은 2025년 본격적으로 출시되었으며, 대화형 AI를 통합하여 문서 작성 시간을 줄이고 가이드라인 편차를 실시간으로 보고합니다. 정밀도가 향상되고 규제 당국의 이해가 깊어짐에 따라 AI는 EMR을 능동적인 의사결정 지원 플랫폼으로 변화시켜 임상적 및 상업적 가치를 확대하고 있습니다.

규제 상의 재정적 인센티브가 전자의무기록 도입을 촉진

정부 보조금은 여전히 전자의무기록 도입의 촉진요소입니다. 미국에서는 2025년 시행된 '상호 운용성 촉진 프로그램'에서 메디케어 환급을 공인 기술과 연계하여 의료 기관에 종합적인 데이터 수집 및 교환을 촉구하고 있습니다. 유럽에서는 2025년에 발효된 유럽 건강 데이터 공간(EHDS)을 통해 2차 데이터 이용의 일관적인 틀을 구축하고, 표준화된 전자 파일을 보유한 병원에 보상을 제공합니다. 일본과 호주에서도 유사한 인센티브 제도가 도입되어 국가의 상호 운용성 기준을 충족한 시설에 환급이 이루어지면서 중소 병원의 자금 부족이 해소되고 있습니다. 성과 연동형 보상 모델이 보급되고 있는 가운데, 의사결정자는 EMR을 단순한 컴플라이언스 달성 수단이 아니라 수익 보호 도구로 파악하고 있습니다. 이러한 예산 배분은 성숙 경제권과 신흥 경제권을 불문하고 전자의무기록 시장의 꾸준한 확대를 뒷받침합니다.

사이버 보안 책임 위험 및 보험 비용

의료 산업은 여전히 랜섬웨어가 가장 표적으로 삼는 산업이며, 2025년에만 1,710건의 보안 사고가 발생했습니다. 기록 유출로 인해 의료기관은 규제 당국에 의한 벌금, 집단 소송, 그리고 대규모 시스템에서는 연간 800만 달러를 넘는 수준으로 상승한 사이버 보험의 보험료 증대 등의 리스크에 노출됩니다. 2025년 초 발생한 대형 클라우드 벤더의 대규모 정보 유출 사건은 공급망 위험에 대한 모니터링을 강화하고 이사회가 독립적인 침입 테스트와 24시간 체제 모니터링을 요구하는 계기가 되었습니다. 지방 병원은 특히 취약하며 그 중 60%가 지난 3년 동안 사이버 사고를 1건 이상 보고하였고, 대부분의 경우 구식 기록 소프트웨어를 계속 유지하고 있습니다. 이러한 압력으로 인해 조달 사이클이 지연되고 실사가 장기화되어 전자의무기록 시장 전체의 성장이 다소 둔화되고 있습니다.

부문 분석

2025년 시점의 전자의무기록 시장에서 소프트웨어의 수익 점유율은 54.22%를 차지했습니다. 이는 첨단 차트 생성 엔진, 분석 대시보드 및 임베디드 AI 모듈이 임상 가치의 핵심이 되었기 때문입니다. 그러나 도입 및 최적화 서비스는 2031년까지 연평균 복합 성장률(CAGR) 6.22%라는 가장 빠른 성장 궤도를 기록할 전망입니다. 팬데믹 동안 기술 도입이 가속화된 의료 시스템은 도입 성공률이 40% 미만인 것으로 보고되어 워크플로의 재설계, 데이터 변환, 사용자 교육에 대한 새로운 지출을 촉진하고 있습니다. HL7 표준과 임상 현장 워크플로 모두에 익숙한 컨설팅 팀은 고액의 보상을 받고 있으며, 이는 서비스 수요의 급증을 뒷받침합니다. 반면 브라우저 기반 클라이언트로의 전환으로 인해 하드웨어 수요가 감소하고 온프레미스 서버 예산이 줄어들어 의료용 태블릿과 같은 틈새 장치에 대한 수요는 여전히 유지되고 있습니다.

서비스 확대는 새로운 환급 실태를 반영하고 있습니다. 가치 기반 결제 계약은 재입원 및 부작용이 페널티 대상이 되기 때문에 의료기관은 임상 의사결정 지원 제도를 조정하고 데이터 품질을 지속적으로 감사하는 엔지니어를 채택합니다. 이러한 가동 후 최적화는 시스템 통합사업자에게 지속적인 수익원이 되어 전자 의료기기 시장에서 서비스 분야의 성장을 가속하고 있습니다. 여러 대형 병원 체인은 현재 공급업체 계약에 성과 연동형 인센티브를 통합하여 외부 파트너의 전문성을 더욱 강화하고 있습니다.

2025년 시점에서 범용 EMR은 전자의무기록 시장 점유율의 59.55%를 차지하였으며, 이는 주로 종합 병원이 기업 보고를 위한 단일 출처를 요구하기 때문입니다. 이 시스템은 입원, 외래 및 청구 워크플로를 통합하여 감사 추적을 간소화합니다. 그러나 정형외과, 종양학, 불임치료 클리닉에서는 모놀리식 설계가 부담이 되는 경우가 증가하고 있어 전문 분야별 템플릿을 기반으로 한 틈새 솔루션이 CAGR 6.49%로 확대되고 있습니다. 하위 전문가 공급업체는 질병 특화형 주문 세트를 통합하고 진단 장비를 네이티브로 통합하여 임상의의 운영 횟수를 줄입니다.

도입의 기세가 가장 강한 부문은 하나의 주요 전문 분야가 수익을 견인하는 외래 네트워크입니다. 경량의 전문 EMR 내에 발작 추적 대시보드와 원격 뇌파 스트리밍을 도입한 신경학 그룹은 문서 작성 속도가 15% 향상되어 환자 만족도도 높아졌다고 보고했습니다. 경쟁력을 유지하기 위해 엔터프라이즈 벤더는 전문 기능을 핵심 데이터베이스에 통합하는 모듈식 마이크로 앱을 출시하기 시작했습니다. 이렇게 하면 부문 간의 경계가 모호해지고 서비스 라인 간 데이터 연속성이 유지됩니다. 이 하이브리드 접근법은 향후 5년간 전자의무기록 시장 규모를 재구성할 것으로 예측됩니다.

지역별 분석

2025년 북미는 전자의무기록 시장 수익의 43.30%를 차지했습니다. HITECH법 이후 연방 자극책으로 인해 병원에서는 최대한 보편적인 도입을 확립하고 현재의 성장은 시스템 갱신과 최적화에 초점을 맞추었습니다. 상호 운용성 인증 기한이 지출을 밀어 올리고 있지만, 이 지역의 2031년까지의 연평균 복합 성장률(CAGR) 4.25%는 다른 지역보다 낮습니다. 의료 제공자의 M&A 활동은 구매 결정을 통합하고 주요 공급업체의 협상력을 강화하여 플랫폼 표준화를 가속화하고 있습니다.

한편 아시아태평양은 6.99%의 연평균 복합 성장률(CAGR)로 성장해 세계에서 가장 빠른 성장 속도를 나타낼 전망입니다. 중국, 인도, 일본 각국의 보건부는 클라이언트 서버 세대를 뛰어넘는 클라우드 도입 파일럿 사업을 조성해, 지방 시설이 원격 의료를 통해 전문의와 연계하는 능력을 뒷받침하고 있습니다. 또한 모바일 퍼스트 설계가 보급되며 이는 임상의의 스마트폰 이용 습관에 적합합니다. 이에 따른 데이터센터와 사이버 보안 서비스에 대한 수요가 지역의 IT 에코시스템을 활성화하여 전자의무기록 시장을 지원하는 지속적인 자기 순환 흐름을 강화하고 있습니다.

유럽에서는 EHDS 이니셔티브가 회원국 간의 기록 아키텍처를 조화시켜 혁신과 엄격한 GDPR(EU 개인정보보호규정) 보호 조치 간의 균형을 맞추기 때문에 4.82%의 꾸준한 CAGR을 보여주고 있습니다. 독일 및 북유럽 국가에서는 AI 지원 진단 비용을 환급하는 국가 프로그램이 더욱 활성화되고 있습니다. 라틴아메리카는 브라질 국가 디지털 건강 계획 및 아르헨티나의 민간 종양학 네트워크가 견인하여 6.36%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 중동 및 아프리카도 뒤를 잇고 있으며 걸프 협력 회의(GCC) 회원국의 병원에서는 합작 투자 계약에 따라 미국의 벤더 플랫폼이 채택되었습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- AI를 활용한 임상 의사결정 지원에 의한 전자의무기록의 가치 제안 강화

- 디지털 기록 도입을 촉진하는 규제 상의 재정적 인센티브

- 레거시 클라이언트 서버 환경에서 클라우드 네이티브 플랫폼으로의 전환으로 총 소유 비용 절감

- 환자 중심의 상호 운용성 의무가 벤더 중립성을 촉진

- 통합형 원격 의료-전자 의료 워크플로에 의한 의료 제공자의 생산성 향상

- 종단적 데이터 연속성을 필요로 하는 만성 질환 관리 프로그램

- 억제요인

- 사이버 보안 책임 위험과 보험 비용

- 의사의 과로와 부적절한 사용자 인터페이스 설계 간의 관련성

- 중소규모 의료 제공 조직의 자본 예산 제약

- 다중 공급업체 환경에서의 데이터 거버넌스의 복잡성

- 기술 전망

- 규제 전망

- Porter's Five Forces

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 컴포넌트별

- 하드웨어

- 소프트웨어

- 서비스

- 전자의무기록(EMR) 유형별

- 종합 전자의무기록(EMR)

- 전문분야별 전자의무기록(EMR)

- 제공 형태별

- 클라우드 기반

- 온프레미스

- 용도별

- 순환기학

- 신경학

- 방사선의학

- 종양학

- 응급 및 외상

- 산부인과

- 기타 용도

- 최종 사용자별

- 병원 내 전자의무기록(EMR)

- 의사 및 외래 진료 센터

- 전문 의원

- 진단 및 영상 센터

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 비즈니스 모델 분석

- 시장 점유율 분석

- 기업 프로파일

- AdvancedMD Inc.

- Altera Digital Health

- Athenahealth Inc.

- Cantata Health LLC

- CareCloud Inc.

- DrChrono Inc.

- eClinicalWorks

- Epic Systems Corporation

- GE HealthCare Technologies Inc.

- Greenway Health LLC

- InterSystems Corporation

- Kareo Inc.

- McKesson Corporation

- Medhost Inc.

- MEDITECH

- Medsphere Systems Corporation

- NextGen Healthcare Inc.

- Oracle Corporation

- TruBridge, Inc.

- Veradigm Inc.

제7장 시장 기회 및 미래 전망

CSM 26.01.21The electronic medical records market is expected to grow from USD 34.50 billion in 2025 to USD 36.24 billion in 2026 and is forecast to reach USD 46.34 billion by 2031 at 5.04% CAGR over 2026-2031.

Several forces keep growth on track: modern reimbursement rules reward data-driven care; hospitals and clinics replace first-generation systems to gain AI-ready functionality; and payers increasingly require interoperable records for prior-authorization decisions. Rising investment in cloud infrastructure allows providers to trim IT overhead while expanding access for multidisciplinary teams. At the same time, mounting use-case evidence shows that well-implemented EMRs lower medication errors, shorten length of stay, and improve revenue-cycle performance, pushing laggards to accelerate adoption. Taken together, these trends position the electronic medical records market as a foundational pillar of broader digital-health transformation.

Global Electronic Medical Records Market Trends and Insights

AI-Powered Clinical Decision Support Enhancing EMR Value Proposition

Health-system executives rank artificial intelligence among their top investment targets because embedded algorithms turn passive records into active clinical partners. The U.S. Food and Drug Administration has already cleared more than 1,000 AI-enabled devices that integrate directly with EMR workflows, ranging from arrhythmia detection to automated image labeling. Mount Sinai's GLUCOSE model, for instance, cut insulin-dosing errors in ICU trials by outperforming experienced clinicians and is built for seamless record integration. Oracle Health's next-generation cloud EHR, scheduled for broad release in 2025, embeds conversational AI to reduce documentation time and flag guideline deviations in real time. As accuracy rates climb and regulatory comfort grows, AI turns EMRs into proactive decision-support platforms, enlarging their clinical and commercial appeal.

Regulatory Financial Incentives Driving Digital Record Adoption

Government subsidies remain a catalyst for EMR rollouts. In the United States, the 2025 Promoting Interoperability Program continues to tie Medicare reimbursement to certified technology use, pushing providers toward comprehensive data capture and exchange. In Europe, the European Health Data Space (EHDS) takes effect in 2025, creating a unified framework for secondary data use that rewards hospitals holding standardized electronic files. Similar incentive schemes in Japan and Australia reimburse facilities that meet national interoperability benchmarks, closing the funding gap for smaller hospitals. As pay-for-performance models proliferate, decision makers view EMRs as revenue protection tools rather than compliance checkboxes. The resulting budget allocations underpin steady expansion of the electronic medical records market across mature and emerging economies.

Cyber-Security Liability Exposure & Insurance Costs

Healthcare remains the most-targeted industry for ransomware, logging 1,710 security incidents in 2025 alone. Breached records expose providers to regulatory fines, class-action litigation, and rising cyber-insurance premiums that now eclipse USD 8 million annually for large systems. A high-profile breach at a major cloud vendor in early 2025 intensified scrutiny of supply-chain risk, prompting boards to demand independent penetration testing and round-the-clock monitoring. Rural hospitals are especially vulnerable, with 60% reporting at least one cyber-incident within three years, often while still running outdated record software. These pressures slow procurement cycles, lengthen due diligence, and marginally dampen overall growth in the electronic medical records market.

Other drivers and restraints analyzed in the detailed report include:

- Migration from Legacy Client-Server to Cloud-Native Platforms Reducing Total Cost of Ownership

- Patient-Centric Interoperability Mandates Catalyzing Vendor Neutrality

- Physician Burnout Linked to Poor User Interface Design

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The electronic medical records market share for software was 54.22% of total revenue in 2025, because advanced charting engines, analytics dashboards, and embedded AI modules remain critical to clinical value. Implementation and optimization services, however, now log the fastest trajectory at a 6.22% CAGR through 2031. Health systems that rushed rollouts during the pandemic report success rates below 40%, prompting fresh spending on workflow redesign, data conversion, and user training. Consultancy teams conversant with both HL7 standards and bedside routines command premium rates, underpinning the services boom. Meanwhile, lower hardware demand accompanies the shift to browser-based clients, trimming on-premise server budgets but not eliminating niche device opportunities such as medical-grade tablets.

Service expansion also mirrors new reimbursement realities. Value-based payment contracts penalize readmissions and adverse events, so providers hire engineers to tune clinical decision-support rules and audit data quality continuously. This post-go-live optimization translates into sticky annuity revenue for integrators and fuels the services slice of the electronic medical records market. Several leading hospital chains now embed outcome-based incentives in their vendor agreements, further entrenching the expertise of external partners.

General EMRs held 59.55% of the electronic medical records market share in 2025, mainly because multi-specialty hospitals seek a single source of truth for enterprise reporting. These systems bundle inpatient, outpatient, and billing workflows, simplifying audit trails. Yet orthopedics, oncology, and fertility clinics increasingly view mono-lithic designs as burdensome, stoking 6.49% CAGR growth in niche solutions built around specialty templates. Vendors catering to subspecialties embed disease-specific order sets and integrate diagnostic devices natively, reducing clicks for clinicians.

Adoption momentum is strongest in ambulatory networks where one dominant specialty drives revenue. Neurology groups deploying seizure-tracking dashboards and tele-EEG streaming inside lightweight specialty EMRs report 15% faster documentation and higher patient satisfaction. To stay competitive, enterprise vendors have begun releasing modular micro-apps that slot specialty features into the core database, blurring lines between categories and preserving data continuity across service lines. This hybrid approach is expected to recalibrate the electronic medical records market size over the next five years.

The Electronic Medical Records Market Report is Segmented by Component (Hardware, Software, Services), EMR Type (General EMRs, Specialty-Specific EMRs), Mode of Delivery (Cloud-Based, On-Premise), Application (Cardiology, Neurology, and More), End-User (Hospital-Based EMR, Specialty Clinics, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 43.30% of electronic medical records market revenue in 2025. Federal stimulus programs after the HITECH Act established near-universal hospital adoption, leaving current growth to focus on system replacement and optimization. Interoperability certification deadlines keep spending buoyant, but the region's 4.25% CAGR to 2031 trails all others. Provider M&A activity consolidates purchasing decisions, strengthening the bargaining power of top vendors and accelerating platform standardization.

Asia-Pacific, by contrast, will compound at 6.99% CAGR, the fastest worldwide. Health ministries in China, India, and Japan subsidize cloud pilots that leapfrog client-server generations, helping rural facilities connect to specialists via telehealth. Mobile-first designs proliferate, aligning with clinicians' smartphone habits. The associated demand for data centers and cybersecurity services feeds local IT ecosystems, reinforcing the self-sustaining cycle that underpins the electronic medical records market in the region.

Europe shows steady 4.82% CAGR as the EHDS initiative harmonizes record architectures across member states, balancing innovation with stringent GDPR safeguards. National programs in Germany and the Nordics that reimburse AI-supported diagnostics provide incremental tailwinds. Latin America grows 6.36% CAGR, led by Brazil's national digital-health plan and Argentina's private-sector oncology networks. The Middle East & Africa follow closely, with Gulf Cooperation Council hospitals adopting U.S. vendor platforms under joint-venture arrangements.

- AdvancedMD

- Altera Digital Health

- Athenahealth

- Cantata Health LLC

- CareCloud

- DrChrono Inc.

- eClinicalWorks

- Epic Systems

- GE HealthCare Technologies Inc.

- Greenway Health

- Intersystems

- Kareo Inc.

- Mckesson

- Medhost Inc.

- Meditech

- Medsphere Systems

- NextGen Healthcare

- Oracle

- TruBridge, Inc.

- Veradigm Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Powered Clinical Decision Support Enhancing EMR Value Proposition

- 4.2.2 Regulatory Financial Incentives Driving Digital Record Adoption

- 4.2.3 Migration from Legacy Client-Server to Cloud-Native Platforms Reducing Total Cost of Ownership

- 4.2.4 Patient-Centric Interoperability Mandates Catalyzing Vendor Neutrality

- 4.2.5 Integrated Telehealth-EMR Workflows Improving Provider Productivity

- 4.2.6 Chronic Disease Management Programs Requiring Longitudinal Data Continuity

- 4.3 Market Restraints

- 4.3.1 Cyber-Security Liability Exposure & Insurance Costs

- 4.3.2 Physician Burnout Linked to Poor User Interface Design

- 4.3.3 Capital Budget Constraints in Small & Mid-Size Provider Organizations

- 4.3.4 Data Governance Complexity in Multi-Vendor Ecosystems

- 4.4 Technological Outlook

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By EMR Type

- 5.2.1 General EMRs

- 5.2.2 Specialty-Specific EMRs

- 5.3 By Mode of Delivery

- 5.3.1 Cloud-based

- 5.3.2 On-premise

- 5.4 By Application

- 5.4.1 Cardiology

- 5.4.2 Neurology

- 5.4.3 Radiology

- 5.4.4 Oncology

- 5.4.5 Emergency & Trauma

- 5.4.6 Obstetrics & Gynecology

- 5.4.7 Other Applications

- 5.5 By End-User

- 5.5.1 Hospital-based EMR

- 5.5.2 Physician/Ambulatory Care Centers

- 5.5.3 Specialty Clinics

- 5.5.4 Diagnostic & Imaging Centers

- 5.5.5 Other End Users

- 5.6 By Geography (Value)

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Business Model Analysis

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 AdvancedMD Inc.

- 6.4.2 Altera Digital Health

- 6.4.3 Athenahealth Inc.

- 6.4.4 Cantata Health LLC

- 6.4.5 CareCloud Inc.

- 6.4.6 DrChrono Inc.

- 6.4.7 eClinicalWorks

- 6.4.8 Epic Systems Corporation

- 6.4.9 GE HealthCare Technologies Inc.

- 6.4.10 Greenway Health LLC

- 6.4.11 InterSystems Corporation

- 6.4.12 Kareo Inc.

- 6.4.13 McKesson Corporation

- 6.4.14 Medhost Inc.

- 6.4.15 MEDITECH

- 6.4.16 Medsphere Systems Corporation

- 6.4.17 NextGen Healthcare Inc.

- 6.4.18 Oracle Corporation

- 6.4.19 TruBridge, Inc.

- 6.4.20 Veradigm Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment