|

시장보고서

상품코드

1906022

의약품 포장 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

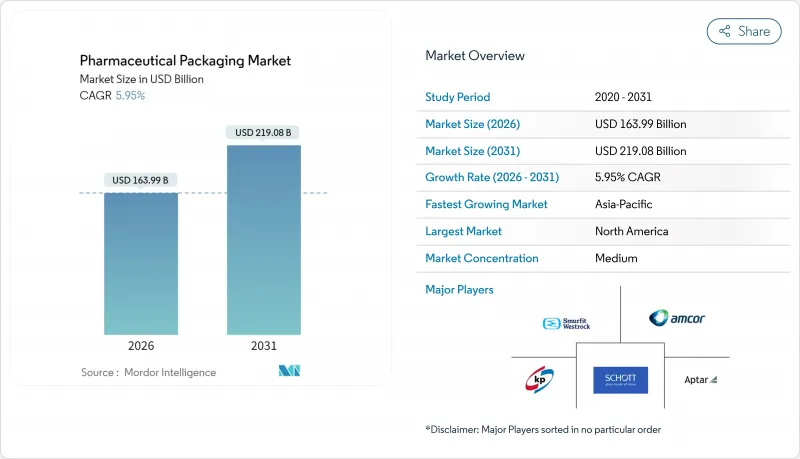

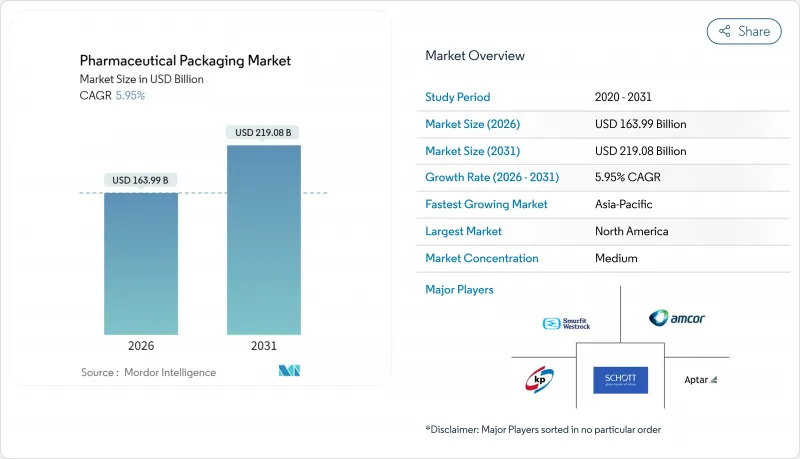

의약품 포장 시장은 2025년 1,547억 8,000만 달러에서 2026년에는 1,639억 9,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 5.95%로 성장을 지속하여 2031년까지 2,190억 8,000만 달러에 이를 전망입니다.

향후 5년간 바이오의약품에 대한 수요 증가, 세계의 추적성 규제 강화, 지속가능성 목표의 확대가 새로운 충전 및 포장 라인, 고차단성 재료, 순환형 대응 설계에 대한 자본 투자를 지속적으로 촉진할 전망입니다. 유전자 및 세포 치료가 상업적 규모에 도달함에 따라, 소규모 맞춤 치료 배치에 대응하는 연질 포장 용량에 대한 수요가 확대될 것으로 예측됩니다. 북미는 DSCSA(의약품 유통안전법)에 근거한 직렬화 추진에 의해 최대의 지역 공헌도를 유지하는 한편, 아시아태평양은 8.96%라는 높은 CAGR을 나타내고 있으며, 이는 국내 의약품 생산 증가와 의료 보험 적용 범위의 확대를 반영하고 있습니다. 재료 전략은 유동적으로 시행됩니다. 플라스틱이 여전히 주류인 반면 EU와 미국의 PFAS 규제 시행이 다가오고 있는 가운데, 바이오 폴리머, 알루미늄 프리 블리스터, 사용 후 재생 필름이 시험 단계에서 양산으로 급속히 이행하고 있습니다. 한편, 폴리에틸렌, 폴리프로필렌, PET의 가격 변동에 의해 이익률은 축소하지만, 장기공급 계약이나 대규모 컨버터에 의한 수직 통합이 촉진되고 있습니다.

세계의 의약품 포장 시장의 동향 및 전망

고령화와 만성 질환의 확산

평균 연령이 증가함에 따라 장기적인 치료 수요가 증가하고 있으며 캘린더 블리스터 포장, 대문자 라벨, 신체 능력이 감소한 환자의 복약 준수를 지원하는 한 손 개봉 바이알 등에 대한 안정적인 수요를 지원하고 있습니다. 독일의 2024년 예방접종 계획 변경(폐렴구균 백신 23% 증가, 수막염균 B형 백신 52% 증가)은 노인층에서의 예방의료의 보급 확대를 나타내고 있습니다. 포장 공급업체는 개봉 기록 기능을 갖춰 의료 팀에 복약 준수 데이터를 전송하는 연결 팩을 지원합니다. 지불기관이 환급을 실세계에서의 치료 성과와 연동시키는 가운데 스마트 마개 및 NFC 대응 카톤의 성장은 더욱 가속할 것으로 예측됩니다.

생물학적 제형 및 주사제의 파이프라인 확장

프리필드 시린지는 자가투여의 간소화, 오염 리스크의 최소화, 충전 및 마무리 공정에서의 폐기물 감축을 실현하여, 신규 바이오로직스 제품의 핵심이 되는 존재입니다. BD사의 iDFill 주사기는 즉각적인 검증을 가능하게 하는 RFID를 내장하고, Neopak XtraFlow 설계는 종래 바이알에 한정되었던 고점도 제제에도 대응합니다. GMP Annex 1의 개정에 의해 세정이나 탈열원처리 공정을 생략할 수 있는 즉시 사용 유리 튜브나 폴리머 용기 수요가 급증하고 있으며, CDMO는 새로운 클린 룸을 건설하지 않고도 생산 능력의 확대가 가능하게 됩니다.

석유 유래 수지의 가격 변동성

공급 장애와 불가항력적인 사건으로 인해 2024년 6월 PET 가격은 1.1% 상승하였으며 이미 좁은 컨버터 마진을 더욱 압박했습니다. 의약품 수탁 제조의 재료 사양은 등급의 신속한 전환을 제한하기 때문에 많은 컨버터는 급증하는 비용을 흡수하거나 장기 계약의 재협상에 내몰리고 있습니다. 골판지 운송업체도 섬유 비용 상승에 직면하고 있으며, 2025년 1월에는 톤당 70달러의 가격 인상이 발표되었습니다.

부문 분석

2025년 플라스틱은 의약품 포장 시장에서 45.05%의 점유율을 유지했습니다. 이는 주로 비용과 장벽 특성의 균형이 뛰어난 HDPE 병, PP 캡, PET 블리스터가 견인하고 있습니다. 그러나 브랜드 소유자가 순환 목표를 추구하는 가운데 부문 성장은 둔화세에 있습니다. 플라스틱 산업 내에서는 내파손성이 뛰어난 환형 올레핀계 소재에 의해 PP제 주사기의 의약품 포장 시장 내 규모가 꾸준히 확대되고 있습니다. 유리는 빛과 습도에 민감한 생물학적 제형에서 여전히 필수적입니다. 무게와 파손 위험이 높음에도 불구하고, 제1종 붕규산 유리 바이알은 세포 독성 충전제 시장을 독점하고 있습니다. 금속은 에어로졸제나 이식형 의료기기에서 틈새 역할을 담당하고 있습니다.

바이오 수지, 재생 PET 중차단성 웹, 종이제 약병(예 : 알레게니 헬스 네트워크의 Tully 튜브 시험 도입)에 대한 주목이 높아지고 있습니다. 개발회사는 시장 출시 전에 보존 기간 보증, 추출물 프로파일 및 라인 전환 비용을 신중하게 검토하지만, 조기 도입 기업은 지속가능성 평가를 공급업체 감사에 통합하는 병원에서 조달 입찰을 획득하는 경우가 많습니다.

지역별 분석

2025년 시점에서 북미는 의약품 포장 시장에서 35.01%의 점유율을 차지했습니다. 이는 바이오 의약품에 대한 대규모 투자와 첨단 DSCSA 직렬화 의무화가 주요 요인입니다. 미국의 제조업체에서만 2025년까지 신규 충전 및 마무리 공장 및 API 플랜트에 1,600억 달러를 투자하는 동향이 나타나고 있으며, 이 동향이 멸균 가능한 폴리머, 즉시 사용 유리 용기, 대용량 콜드체인 수송 용기의 수요를 견인하고 있습니다. 이 지역에서는 또한 라인 속도로 100마이크로미터 미만의 미립자를 스캔하는 AI 비전 시스템의 시험 운용이 진행되고 있어, 리콜 위험 감소와 브랜드 신뢰성 향상에 기여하고 있습니다.

유럽에서는 야심찬 지속가능성 규제와 에너지 비용 압력 간의 균형을 맞추고 있습니다. 2030년까지 모든 포장 형태의 재활용을 의무화하는 '포장 및 포장 폐기물 규제'의 시행을 앞두고, 단일 소재의 블리스터 포장이나 종이제 약병에 대한 관심이 높아지고 있습니다. 독일의 의약품 생산량은 2024년 1.5% 감소했으나 mRNA 요법과 유전자 치료 등 초저온 포장을 필요로 하는 R&D 파이프라인은 여전히 풍부합니다. 2026년에 시행되는 PFAS 규제에 의해 재료의 재인증이 의무화되면서, 불소 프리 차단 필름을 공급하는 기업에는 선행 우위성이 탄생합니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 8.73%로 가장 높은 성장률을 나타낼 전망입니다. 중국과 인도에서의 CDMO(의약품 수탁 개발 제조)의 확대, 공공 의료 보험의 적용 범위 확대가 견인역입니다. 현지 규제 당국은 무균 기준을 ICH(국제 약품 규제 회의) 및 PIC/S(약품 규제 조화에 관한 국제 회의) 가이드라인과 일치시켜, 포장 공장에 대해 ISO 5레벨 차단 성능과 전체 라인 직렬화 도입을 추진하고 있습니다. 그러나 이 지역은 지정학적 역풍에도 직면하고 있습니다. 중국의 스파이 방지법 개정에 의해 추적 시스템의 기술 이전이 복잡해지면서 다국적 기업은 ASEAN 시장으로의 조달처 분산을 추진하고 있습니다. 정밀 성형 기술로 알려진 일본의 컨버터 기업은 세계 브랜드가 단일 국가 의존을 회피하는 움직임으로 인해 COP 주사기의 수출 수주를 획득하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 고령화와 만성질환의 확산

- 바이오의약품 및 주사제 파이프라인의 확대

- 지속가능성을 중시한 재료 대체

- 디지털 추적성 의무화(예 : DSCSA, EU-FMD)

- AI 탑재형 적응 충전 및 마무리 라인

- 택배 대응 포장을 필요로 하는 재택 및 분산형 시험 증가

- 억제요인

- 석유 유래 수지의 가격 변동성

- 자본 집약적인 무균성 및 검증 요건

- EU 및 미국에서의 PFAS 및 불소 수지 규제의 우려

- 업계 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 소재별

- 플라스틱

- HDPE

- LDPE 및 LLDPE

- PET

- 기타 플라스틱 제품

- 유리

- 제I형 붕규산 유리

- 제II형 처리 소다 석회

- 제III형 소다 석회

- 금속

- 종이 및 판지

- 바이오 폴리머 및 기타 재료

- 플라스틱

- 포장 레벨별

- 1차 포장

- 병

- 프리필드 주사기

- 바이알 및 앰풀

- 블리스터 포장

- 2차 포장

- 카톤 및 슬리브

- 라벨 및 삽입물

- 3차 포장

- 골판지 수송 용기

- 파렛트 및 보호 시스템

- 1차 포장

- 제품 유형별

- 병

- 프리필드 주사기

- 바이알 및 앰풀

- 블리스터 포장

- 뚜껑 및 마개

- 튜브 및 파우치

- 기타 제품 유형

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor plc

- Gerresheimer AG

- Schott AG

- West Pharmaceutical Services Inc.

- AptarGroup Inc.

- Smurfit WestRock

- Becton, Dickinson & Company

- Catalent Inc.

- CCL Industries Inc.

- Klockner Pentaplast Group

- Nipro Corporation

- Vetter Pharma International GmbH

- McKesson Corporation

- FlexiTuff International Ltd.

- WL Gore & Associates Inc.

- Stevanato Group

- Corning Incorporated

- Owen-Illinois Inc.

- SGD Pharma

제7장 시장 기회 및 미래 전망

CSM 26.01.28The pharmaceutical packaging market is expected to grow from USD 154.78 billion in 2025 to USD 163.99 billion in 2026 and is forecast to reach USD 219.08 billion by 2031 at 5.95% CAGR over 2026-2031.

Over the next five years, the increasing demand for biologics, stricter global traceability regulations, and widespread sustainability targets will continue to drive capital investment in new fill-finish lines, high-barrier materials, and circular-ready designs. Demand for flexible pack volumes that match smaller, personalized therapy batches is expected to expand as gene and cell therapies reach commercial scale. North America remains the largest regional contributor, supported by DSCSA-driven serialization, while the Asia-Pacific's sizable 8.96% CAGR reflects rising domestic drug production and broadening health coverage.Material strategies are in flux: plastics still dominate, yet bio-based polymers, aluminum-free blisters, and post-consumer-recycled films are quickly transitioning from pilot to production as EU and US PFAS curbs near enforcement. Meanwhile, price swings in polyethylene, polypropylene, and PET keep margins tight, encouraging longer supplier contracts and vertical integration by larger converters.

Global Pharmaceutical Packaging Market Trends and Insights

Aging population and chronic disease prevalence

Rising median ages drive up long-term therapy volumes, underpinning consistent demand for calendar blisters, large-print labels, and one-hand-open vials that aid adherence among patients with reduced dexterity. Germany's 2024 vaccination shifts, with pneumococcal doses up 23% and meningococcal B up 52%, illustrate broader preventive care uptake among seniors. Packaging suppliers respond with connected packs that log opening events and forward adherence data to care teams. Growth in smart closures and NFC-enabled cartons is expected to intensify as payers link reimbursement to real-world outcomes.

Biologics and injectable pipeline expansion

Prefilled syringes sit at the core of new biologic launches because they simplify self-administration, minimize contamination risks, and reduce waste during the fill-finish process. BD's iDFill syringe embeds RFID for instant verification, while its Neopak XtraFlow design handles viscous formulations that were once vial-only. GMP Annex 1 revisions are accelerating demand for ready-to-use glass tubing and polymer containers that bypass washing and depyrogenation steps, helping CDMOs scale capacity without the need to construct new cleanrooms.

Petro-derivative resin price volatility

Supply disruptions and force majeure events led to a 1.1% increase in PET prices in June 2024, further tightening already narrow converter margins. Pharmaceutical contract material specs restrict rapid grade switches, forcing many converters to absorb cost spikes or renegotiate long contracts. Corrugated shippers also face higher fibre costs, with a USD 70 per-ton increase announced for January 2025.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability-driven material substitution

- Digital traceability mandates (DSCSA, EU-FMD)

- Capital-intensive sterility and validation requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics retained 45.05% of the pharmaceutical packaging market share in 2025, primarily driven by HDPE bottles, PP closures, and PET blisters that strike a balance between cost and barrier needs. Yet the segment's growth moderates as brand owners court circularity objectives. Within the plastics industry, the pharmaceutical packaging market size for PP-based syringes is rising steadily, thanks to break-resistant cyclic olefin options. Glass remains indispensable for light- and moisture-sensitive biologics; Type I borosilicate vials dominate cytotoxic fills, despite their higher weight and shatter risk. Metals play a niche role in aerosol and implantable devices.

Momentum is gathering around bio-attributed resins, recycled PET mid-barrier webs, and paper-based pill bottles, such as Allegheny Health Network's Tully Tube pilot. Developers weigh shelf-life assurance, extractables profiles, and line changeover costs before a wide release, yet early adopters often win procurement tenders from hospitals, incorporating sustainability scoring into vendor audits.

The Pharmaceutical Packaging Market Report is Segmented by Material (Plastics, Glass, Metal, and More), Packaging Level (Primary Packaging, Secondary Packaging, and More), Product Type (Bottles, Prefilled Syringes, Vials and Ampoules, Blister Packs, Caps and Closures, and More), and Geography (North America, South America, Europe, Asia Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 35.01% of the pharmaceutical packaging market share in 2025, driven by significant investments in biologics and advanced DSCSA serialization mandates. U.S. manufacturers alone are investing USD 160 billion in new fill-finish and API plants through 2025, a trend that drives demand for sterilizable polymers, ready-to-use glass, and high-capacity cold-chain shippers. The region also pilots AI vision systems that scan for sub-100 µm particulates at line speed, lowering recall risk and strengthening brand trust.

Europe balances ambitious sustainability regulations with energy cost pressures. The forthcoming Packaging and Packaging Waste Regulation requires every format to be recyclable by 2030, escalating interest in monomaterial blisters and paper-based pill bottles. Germany's pharmaceutical output slipped 1.5% in 2024, yet its R&D pipelines remain rich in mRNA and gene therapies that require ultra-low-temperature packaging. PFAS restrictions, effective in 2026, force material requalification, offering an early-mover advantage to suppliers with fluorine-free barrier films.

The Asia-Pacific region grows at the fastest rate of 8.73% CAGR through 2031, driven by the expanding CDMO footprints of China and India, as well as the widening of public health coverage. Local regulators align sterility rules with ICH and PIC/S guides, pushing packaging plants to adopt ISO 5 barriers and full-line serialization. Yet the region faces geopolitical headwinds; China's updated Anti-Espionage Law complicates technology transfer for track-and-trace systems, prompting multinationals to diversify sourcing across ASEAN markets. Japanese converters, renowned for their precision molding, secure export orders for COP syringes as global brands hedge against dependence on a single country.

- Amcor plc

- Gerresheimer AG

- Schott AG

- West Pharmaceutical Services Inc.

- AptarGroup Inc.

- Smurfit WestRock

- Becton, Dickinson & Company

- Catalent Inc.

- CCL Industries Inc.

- Klockner Pentaplast Group

- Nipro Corporation

- Vetter Pharma International GmbH

- McKesson Corporation

- FlexiTuff International Ltd.

- W. L. Gore & Associates Inc.

- Stevanato Group

- Corning Incorporated

- Owen-Illinois Inc.

- SGD Pharma

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing population and chronic disease prevalence

- 4.2.2 Biologics and injectable pipeline expansion

- 4.2.3 Sustainability-driven material substitution

- 4.2.4 Digital traceability mandates (e.g., DSCSA, EU-FMD)

- 4.2.5 AI-enabled adaptive fill-finish lines

- 4.2.6 Rise of at-home/decentralised trials needing mail-ready packs

- 4.3 Market Restraints

- 4.3.1 Petro-derivative resin price volatility

- 4.3.2 Capital-intensive sterility and validation requirements

- 4.3.3 Looming PFAS/fluoropolymer restrictions in EU and US

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastics

- 5.1.1.1 HDPE

- 5.1.1.2 LDPE and LLDPE

- 5.1.1.3 PET

- 5.1.1.4 Other Plastics

- 5.1.2 Glass

- 5.1.2.1 Type I Borosilicate

- 5.1.2.2 Type II Treated Soda-lime

- 5.1.2.3 Type III Soda-lime

- 5.1.3 Metal

- 5.1.4 Paper and Paperboard

- 5.1.5 Biopolymers and Other Materials

- 5.1.1 Plastics

- 5.2 By Packaging Level

- 5.2.1 Primary Packaging

- 5.2.1.1 Bottles

- 5.2.1.2 Prefilled Syringes

- 5.2.1.3 Vials and Ampoules

- 5.2.1.4 Blister Packs

- 5.2.2 Secondary Packaging

- 5.2.2.1 Cartons and Sleeves

- 5.2.2.2 Labels and Inserts

- 5.2.3 Tertiary Packaging

- 5.2.3.1 Corrugated Shippers

- 5.2.3.2 Pallets and Protective Systems

- 5.2.1 Primary Packaging

- 5.3 By Product Type

- 5.3.1 Bottles

- 5.3.2 Prefilled Syringes

- 5.3.3 Vials and Ampoules

- 5.3.4 Blister Packs

- 5.3.5 Caps and Closures

- 5.3.6 Tubes and Pouches

- 5.3.7 Other Product Types

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 Middle East

- 5.4.4.1.1 United Arab Emirates

- 5.4.4.1.2 Saudi Arabia

- 5.4.4.1.3 Turkey

- 5.4.4.1.4 Rest of Middle East

- 5.4.4.2 Africa

- 5.4.4.2.1 South Africa

- 5.4.4.2.2 Nigeria

- 5.4.4.2.3 Egypt

- 5.4.4.2.4 Rest of Africa

- 5.4.4.1 Middle East

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Gerresheimer AG

- 6.4.3 Schott AG

- 6.4.4 West Pharmaceutical Services Inc.

- 6.4.5 AptarGroup Inc.

- 6.4.6 Smurfit WestRock

- 6.4.7 Becton, Dickinson & Company

- 6.4.8 Catalent Inc.

- 6.4.9 CCL Industries Inc.

- 6.4.10 Klockner Pentaplast Group

- 6.4.11 Nipro Corporation

- 6.4.12 Vetter Pharma International GmbH

- 6.4.13 McKesson Corporation

- 6.4.14 FlexiTuff International Ltd.

- 6.4.15 W. L. Gore & Associates Inc.

- 6.4.16 Stevanato Group

- 6.4.17 Corning Incorporated

- 6.4.18 Owen-Illinois Inc.

- 6.4.19 SGD Pharma

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment