|

시장보고서

상품코드

1906027

의료 분석 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Healthcare Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

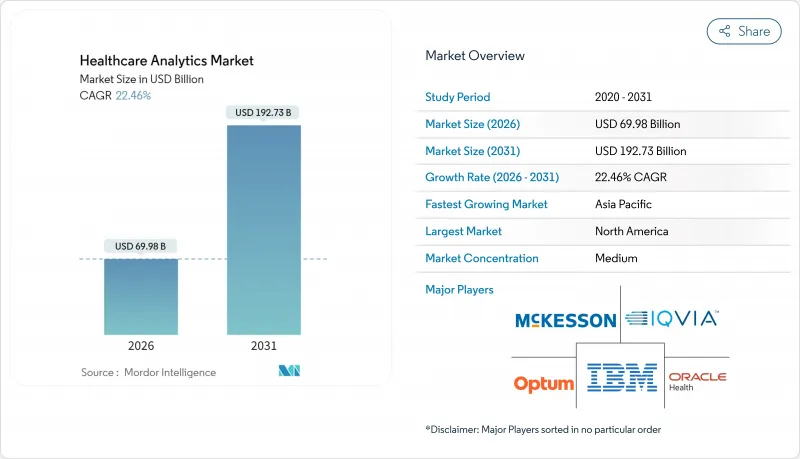

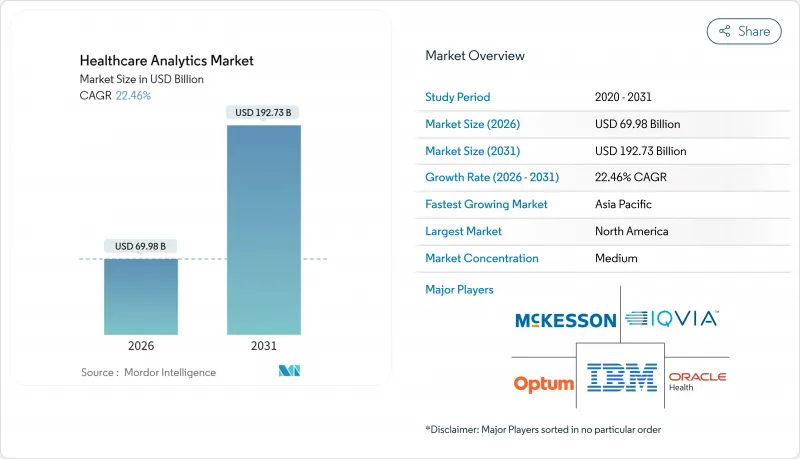

의료 분석 시장은 2025년 571억 6,000만 달러에서 2026년에는 699억 8,000만 달러로 성장하여 2026년부터 2031년에 걸쳐 CAGR 22.46%로 성장을 지속하고, 2031년까지 1,927억 3,000만 달러에 이를 전망입니다.

지불자와 공급자 간의 협력 확대, AI 기반 데이터 파이프라인의 광범위한 도입, 클라우드 네이티브 분석 환경으로의 꾸준한 전환이 수익 성장을 가속화하고 있습니다. 의료 제공자 네트워크는 예측 리스크 점수에 의존하는 지역 주민 건강 프로그램을 확대하는 한편, 생명 과학 기업은 규제 승인을 가속화하기 위해 임상시험 설계에 실세계 근거를 계속 도입하고 있습니다. 동시에, 벤처 투자자는 과부하 상태에 있는 병원의 IT 팀을 위한 로우코드 데이터 통합 툴을 제공하는 분석 스타트업을 지원하고 있으며, 기존 플랫폼 벤더에게 활발한 인수 파이프라인을 형성하고 있습니다. 하이퍼스케일 클라우드 제공업체, 레거시 EHR 기업, 순수 분석 전문 기업이 생성형 AI 및 도메인 특화형 대규모 언어 모델을 기존 워크플로와 통합하려고 경쟁하는 가운데 경쟁이 치열해지고 있습니다.

세계의 의료 분석 시장의 동향 및 인사이트

가치 기반 의료로의 전환

종량제 보상에서 가치 기반 의료(VBC) 모델로의 전환은 의료 분석 요건을 근본적으로 변화시키고 있습니다. 조직이 임상 성과와 재무 실적을 연결하는 분석 솔루션을 추구하는 가운데 VBC 시장은 5,000억 달러에서 1조 달러로 두배로 성장할 것으로 예측됩니다. 이러한 성장 궤도에도 불구하고, 2024년 7월 커먼웰스 기금 조사에 따르면 1차 의료 의사의 불과 46%만 가치 기반 지급 제도에 참여하고 있었으며, 도입을 막는 재무적 장벽과 관리 부담에 대처할 수 있는 분석 솔루션 벤더들 간에 큰 시장 격차가 발생하고 있습니다. 이 전환으로 인해 비용 절감을 넘어서는 성과(특히 환급과 연관된 건강 격차 지표 포함)를 측정하면서 환자의 동적 요구에 적응할 수 있는 보다 진보된 환자 중심의 의료 분석가 요구되고 있어 의료 분석 시장의 중요성을 한층 더 높이고 있습니다.

의약품 개발과 환자 안전 강화를 위한 실세계 데이터 의무화

미국, 유럽연합, 일본의 규제당국은 생명과학기업의 스폰서에게 무작위화 시험 데이터에 실세계 근거를 보완하도록 권장하고 있습니다. 제약 회사는 익명화된 청구 데이터 및 레지스트리 정보를 통합하여 적응 확대, 안전 모니터링 및 희귀질환 연구를 뒷받침합니다. 생명과학분석팀은 학술의료센터와의 연계를 강화하고 프라이버시 기준을 충족시키면서 종단적 상세 정보를 손상시키지 않는 연합 데이터 네트워크를 구축하고 있습니다. 이 협업은 강력한 데이터 시스템 추적 기능을 갖춘 페타바이트 규모의 데이터 세트를 처리할 수 있는 고성능 분석 플랫폼에 대한 투자를 촉진합니다. 미국 식품의약국(FDA)의 전자 도출 엔드포인트에 대한 신규 지침은 투명성이 높고 감사 가능한 알고리즘의 필요성을 재확인하는 노력이며, 벤더 각사는 바이오의약품 고객에 대한 마케팅에서 이 기능을 핵심 차별화 포인트로 강조하고 있습니다.

단편화된 데이터 표준 및 규정 준수 비용

보편적으로 채택된 상호 운용성 프레임워크의 부족은 여러 사이트에 걸친 분석 솔루션 도입에서 데이터 추출 및 변환 비용을 증가시키고 있습니다. HIPAA, GDPR(EU 개인정보보호규정) 및 국가별 현지화 규정을 비롯한 서로 다른 개인정보 보호 법률은 첨단 동의 관리 워크플로가 필요합니다. 국경을 넘는 원격 의료 프로그램을 운영하는 병원은 주권 클라우드 간에 데이터 세트를 복제해야 하며 이는 스토리지 예산을 늘리고 액세스 거버넌스를 복잡하게 합니다. 이러한 구조적 마찰은 도입 일정을 늦추고 예산을 첨단 분석에서 컴플라이언스 도구로 이동시키기 때문에 단기적인 지출의 기세를 둔화시키고 있습니다.

부문 분석

기술 분석은 2025년에도 최대의 수익원으로 의료 분석 시장 점유율의 45.80%를 차지했습니다. 조직은 기본 규제 보고 및 청구 검토 요구사항을 충족하기 위해 여전히 사후 분석 대시보드에 의존합니다. 예산 제약이 있는 지역 병원은 데이터 거버넌스 기반을 구축하는 과정에서 기술 모듈을 입문 수준의 솔루션으로 이용하고 있습니다. 한편, 예측 분석은 분석 부문에서 가장 높은 23.90%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 헬스케어 팀은 위험 추세 점수를 도입하고 고위험 회원을 파악하여 지원 자원을 우선순위화합니다. 공급업체 로드맵은 솔루션이 전자 의무 기록 워크플로에 통합된 후 모델의 유지보수를 용이하게 하기 위해 자동 머신러닝(Auto-ML)과 설명 가능한 AI 기능에 특히 중점을 둡니다.

농혈증의 준실시간 경보, 울혈성 심부전 악화의 조기 경고 시스템, 수술실 스케줄링 최적화 도구에 대한 수요가 예측 분석 분야의 성장 궤도를 더욱 뒷받침합니다. 병원 네트워크가 베드사이드 모니터의 스트리밍 텔레메트리를 활용함에 따라 예측 분석 수준에서의 의료 분석 시장의 규모가 확대될 것으로 예측됩니다. 신규 진출기업은 데이터 사이언스 전문 교육을 받지 않은 임상의를 대상으로 한 드래그 앤 드롭 모델 빌더를 제공함으로써 차별화를 도모하고 있습니다. 용도 카탈로그가 확장됨에 따라 플랫폼 통합의 움직임이 현저해지고 있으며, 하이엔드 공급자는 기술, 진단 및 처방 모듈을 통합한 구독 계층을 제공합니다.

소프트웨어 라이선스는 2025년 총 수익의 59.40%를 차지하였으며 고가의 전사적 플랫폼 계약 체결이 성장을 견인했습니다. 이러한 계약은 일반적으로 데이터 통합, 시각화 및 첨단 모델링 엔진을 번들로 제공하며 공급업체에게 지속적인 계정 관리 권한을 부여합니다. 그러나 고객이 공급업체 주도 설정, 데이터 품질 복구 및 관리 모델 성능 지원을 요구하는 가운데 서비스 계약은 24.90%의 연평균 복합 성장률(CAGR)로 확대되고 있습니다. 아웃소싱 서비스는 인력 부족에 직면하는 병원과 24시간 분석 감시를 필요로 하는 세계 규모 시험 네트워크를 운영하는 생명 과학 기업에서 수요가 발생합니다.

많은 공급업체는 초기 도입 시 내부 팀을 보완하는 모듈형 서비스를 선택합니다. 이 하이브리드 접근법은 시스템 가동 시간을 보장하면서 초기 자본 지출을 줄입니다. 서비스 제공업체는 데이터 매핑 작업을 간소화하고 가치 실현까지의 시간을 단축하기 위해 자동화를 점점 더 통합하고 있습니다. 병원의 최고재무책임자(CFO)가 예측 가능한 운영경비를 요구하는 가운데 구독형 관리 서비스가 인기를 얻고 있으며 예측기간 내에 컴포넌트 서비스 라인이 소프트웨어와의 수익 격차를 줄일 전망입니다. 레거시 소프트웨어의 도입 수명에 따라 서비스로 인한 의료 분석 시장의 규모는 업데이트 예산에서 더 큰 비율을 차지할 것으로 예측됩니다.

지역별 분석

북미는 성숙한 전자의무기록(EHR) 도입, 광범위한 가치 기반 결제 방식, 유리한 벤처캐피탈 유입으로 2025년 세계 수익의 48.10%를 차지했습니다. 의료 제공자의 통합이 진행됨에 따라 구매력이 확대되는 한편, 21세기 치료법(21st Century Cures Act) 등의 엄격한 상호 운용성 규제가 API(Application Programming Interface) 벤더의 활기찬 생태계를 조성하고 있습니다. 품질보고에 대한 환급 규정은 일상 업무에서 분석의 중요성을 더욱 높여주고 있으며, 이 지역의 주도적 지위를 유지하고 있습니다.

유럽은 견조한 수요로 뒤따르고 있습니다. 특히 스칸디나비아 국가들은 국가등록제도와 성과연동형 조달모델을 우선시하고 있습니다. 지역 데이터 보호 규칙이 조달 주기를 연장하는 반면, 공통 의료 데이터 공간 구축을 위한 범유럽 이니셔티브는 중기적으로 기준 간의 조화를 목표로 합니다. 공공 부문의 연구 컨소시엄도 희귀질환과 팬데믹 대책에 초점을 맞춘 크로스보더 데이터 공유 프로젝트에 대한 자금 제공을 통해 도입을 추진하고 있습니다.

아시아태평양은 CAGR 22.85%로 가장 빠르게 성장하고 있습니다. 인도, 인도네시아, 태국의 정부 자금을 통한 보험 제도 확대는 확장 가능한 분석 인프라를 필요로 하는 새로운 데이터세트를 만들어내고 있습니다. 중국 각 성에서는 재입원 페널티를 포함한 가치 기반 환급제도의 시험 운용이 이루어지고 있으며, 국내 분석 벤더가 예측 모델을 지역의 병원 정보 시스템에 통합하는 움직임을 촉진하고 있습니다. 호주와 싱가포르는 클라우드 우선 국가 의료 IT 전략을 추진하여 세계 플랫폼 제공업체에 개방하고 있습니다. 그 결과, 현재의 성장 궤도에 따르면, 아시아태평양의 의료 분석 시장의 규모는 2031년 이후 절대 수익에서 유럽을 추월할 것으로 예측되고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 가치 기반 의료로의 전환

- 의약품 개발과 환자 안전성 향상을 위한 실세계 근거의 의무화

- 클라우드 도입과 AI 탑재 헬스케어 툴

- 벤처 캐피탈 투자와 보험 프로세스의 디지털화

- 벤처 캐피탈의 분석 스타트업 기업에 대한 자금 투자

- 보험의 디지털화로 사기 분석 촉진

- 억제요인

- 단편화된 데이터 기준 및 데이터 보호 규정에 대한 컴플라이언스 비용

- 숙련된 전문가의 부족과 사이버 보안 위협

- HIPAA/GDPR(EU 개인정보보호규정) 컴플라이언스 비용 상승

- 병원 데이터 레이크에 대한 사이버 공격 격화

- 규제 전망

- 기술 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 분석 유형별

- 기술 분석

- 진단 분석

- 예측 분석

- 처방 분석

- 인지 분석

- 컴포넌트별

- 하드웨어

- 소프트웨어

- 서비스

- 제공방법별

- 온프레미스

- 클라우드 기반

- 하이브리드

- 용도별

- 임상 분석

- 재무 및 수익 관리 분석

- 업무 및 관리 분석

- 인구 건강 관리

- 사기 탐지 및 리스크 분석

- 생명과학 및 연구개발 분석

- 최종 사용자별

- 의료 제공자

- 의료보험 지불자

- 생명과학기업

- 공중보건기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- 3M Company

- Veradigm Inc.

- Oracle Health

- Digital Reasoning Systems Inc.

- Information Builders, Inc.(IBI)

- International Business Machines Corporation(IBM)

- IQVIA Holdings Inc.

- McKesson Corporation

- MedeAnalytics, Inc.

- Optum, Inc.

- Koninklijke Philips NV

- Health Catalyst, Inc.

- VitreosHealth, Inc.

- Inovalon, Inc.

- SAS Institute Inc.

- Verisk Analytics, Inc.

- CitiusTech, Inc.

- Merative

- SAP SE

- Microsoft Corporation

- Siemens Healthineers AG

- Deloitte Consulting LLP

제7장 시장 기회 및 미래 전망

CSM 26.01.21The Healthcare Analytics market is expected to grow from USD 57.16 billion in 2025 to USD 69.98 billion in 2026 and is forecast to reach USD 192.73 billion by 2031 at 22.46% CAGR over 2026-2031.

Expanded payer-provider collaboration, wider deployment of AI-driven data pipelines, and a steady shift toward cloud-native analytic environments are accelerating revenue growth. Provider networks are scaling population health programs that rely on predictive risk scores, while life-science companies continue to embed real-world evidence in clinical trial designs to speed regulatory approvals. At the same time, venture investors are favoring analytics start-ups that bring low-code data-integration tools to overstretched hospital IT teams, creating an active acquisition pipeline for incumbent platform vendors. Competition is intensifying as hyperscale cloud providers, legacy EHR firms, and pure-play analytics specialists race to integrate generative AI and domain-specific large language models into existing workflows.

Global Healthcare Analytics Market Trends and Insights

Transition to Value-Based Care

The shift from fee-for-service to value-based care (VBC) models is fundamentally altering healthcare analytics requirements, with the VBC market projected to double from USD 500 billion to USD 1 trillion as organizations seek analytics solutions that connect clinical outcomes to financial performance. Despite this growth trajectory, only 46% of primary care practitioners currently participate in value-based payment arrangements, creating a significant market gap for analytics vendors who can address the financial barriers and administrative burdens that impede adoption, as per the Commonwealth Fund, July 2024. The transition demands more sophisticated patient-centered care management analytics that can adapt to dynamic patient needs while measuring outcomes beyond cost reduction, including health equity metrics that are increasingly tied to reimbursement, strengthening the healthcare analytics market relevance.

Real-World Evidence Mandates to Enhance Drug Development and Patient Safety

Regulators in the United States, European Union, and Japan encourage life-science sponsors to supplement randomized-trial data with real-world evidence. Pharmaceutical firms are integrating de-identified claims and registry information to support label expansions, safety surveillance, and rare-disease studies. Life-science analytics teams increasingly partner with academic medical centers to build federated data networks that meet privacy standards without sacrificing longitudinal detail. This collaboration drives spending on high-performance analytic platforms capable of processing petabyte-scale datasets with robust lineage tracking. New guidance from the U.S. Food & Drug Administration on electronically derived endpoints reinforces the need for transparent, auditable algorithms, a capability vendors highlight as a core differentiation point when marketing to biopharma customers.

Fragmented Data Standards and Compliance Costs

The lack of universally adopted interoperability frameworks raises extraction and transformation costs for multi-site analytics deployments. Divergent privacy statutes such as HIPAA, GDPR, and country-specific localization rules require sophisticated consent-management workflows. Hospitals operating cross-border telehealth programs must duplicate datasets across sovereign clouds, inflating storage budgets and complicating access governance. These structural frictions slow deployment timetables and redirect budget away from advanced analytics toward compliance tooling, dampening near-term spending momentum.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Adoption and AI-Enabled Health Tools

- Venture Capital Investments and the Digitization of Insurance Processes

- Skilled Professional Shortage and Cybersecurity Threats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Descriptive analytics remained the largest revenue contributor, holding 45.80% of the healthcare analytics market share in 2025. Organizations continue to rely on retrospective dashboards to satisfy basic regulatory reporting and claims adjudication requirements. Budget-constrained community hospitals also view descriptive modules as entry-level solutions while they build data governance foundations. In parallel, predictive analytics is clocking a 23.90% CAGR, the highest among analytic categories. Care-management teams deploy risk-propensity scores to flag high-risk members and to prioritize outreach resources. Vendor roadmaps place special emphasis on auto-ML and explainable-AI functions to ease model maintenance once solutions are embedded in electronic health record workflows.

Demand for near-real-time sepsis alerts, early-warning systems for congestive-heart-failure exacerbations, and operating-room scheduling optimizers further underpins the predictive segment's trajectory. The healthcare analytics market size at the predictive level is projected to expand as hospital networks unlock streaming telemetry from bedside monitors. Market entrants differentiate by offering drag-and-drop model builders aimed at clinicians who lack formal data-science training. As application catalogs grow, platform consolidation looms, with high-end providers bundling descriptive, diagnostic, and prescriptive modules into unified subscription tiers.

Software licenses generated 59.40% of total revenue in 2025 thanks to high-priced, enterprise-wide platform agreements. These contracts typically bundle data integration, visualization, and advanced modeling engines, giving vendors durable account control. Nonetheless, service engagements are expanding at a 24.90% CAGR as clients seek vendor-led configuration, data-quality remediation, and managed-model-performance support. Outsourced services appeal to hospitals facing workforce shortages and to life-science firms that operate global trial networks requiring around-the-clock analytic oversight.

Many providers opt for modular services to augment in-house teams during initial deployments. This hybrid approach reduces upfront capital expenditure while ensuring system uptime. Service providers increasingly incorporate automation to streamline data-mapping tasks, accelerating time to value. As hospital CFOs press for predictable operating expenses, subscription-based managed services gain favor, positioning the component services line to narrow the revenue gap with software over the forecast period. The healthcare analytics market size attributable to services is expected to capture larger renewal budgets as legacy software installations reach end-of-life.

The Healthcare Analytics Market is Segmented by Technology Type (Predictive Analytics, and More), Component (Hardware, Software, and More), Delivery Mode (On-Premise Model, and Morel), Application (Clinical Data Analytics, Financial Data Analytics, and More), End User (Healthcare Providers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 48.10% of global revenue in 2025 thanks to mature EHR adoption, widespread value-based payment schemes, and favorable venture-capital flows. Provider consolidation amplifies spending power, while stringent interoperability regulations such as the 21st Century Cures Act foster a vibrant ecosystem of application-programming-interface vendors. Reimbursement mandates for quality reporting further entrench analytics in day-to-day operations, sustaining the region's leadership position.

Europe follows with solid demand, led by Scandinavian nations that prioritize national registries and outcome-based procurement models. Regional data-protection rules do lengthen procurement cycles, but pan-European initiatives to establish common health-data spaces promise to harmonize standards over the medium term. Public-sector research consortia also drive uptake by funding cross-border data-sharing projects focused on rare diseases and pandemic preparedness.

Asia Pacific is the fastest-growing region at 22.85% CAGR. Government-funded insurance expansions in India, Indonesia, and Thailand create new datasets requiring scalable analytic infrastructure. Chinese provinces pilot value-based reimbursement schemes that incorporate hospital readmission penalties, spurring domestic analytics vendors to integrate predictive models into local hospital information systems. Australia and Singapore advance cloud-first national health-IT strategies, opening doors for global platform providers. As a result, the healthcare analytics market size in Asia Pacific is projected to overtake Europe in absolute revenue shortly after 2031, given current growth trajectories.

- 3M

- Veradigm Inc.

- Oracle Health

- Digital Reasoning Systems

- Information Builders, Inc. (IBI)

- IBM

- IQVIA

- Mckesson

- MedeAnalytics

- Optum

- Koninklijke Philips

- Health Catalyst, Inc.

- VitreosHealth, Inc.

- Inovalon, Inc.

- SAS Institute

- Verisk Analytics, Inc.

- CitiusTech, Inc.

- Merative

- SAP

- Microsoft

- Siemens Healthineers

- Deloitte Consulting LLP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Transition to Value-Based Care

- 4.2.2 Real-World Evidence Mandates to Enhance Drug Development and Patient Safety

- 4.2.3 Cloud Adoption and AI-Enabled Health Tools

- 4.2.4 Venture Capital Investments and the Digitization of Insurance Processes

- 4.2.5 VC Influx into Analytics Start-ups

- 4.2.6 Insurance Digitization Fueling Fraud Analytics

- 4.3 Market Restraints

- 4.3.1 Fragmented Data Standards and Compliance Cost to Data Protection Regulations

- 4.3.2 Shortage of Skilled Professionals and Cybersecurity Threats

- 4.3.3 Rising HIPAA /GDPR Compliance Costs

- 4.3.4 Escalating Cyber-attacks on Hospital Data Lakes

- 4.4 Regulatory Outlook

- 4.5 Technology Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Analytics Type

- 5.1.1 Descriptive Analytics

- 5.1.2 Diagnostic Analytics

- 5.1.3 Predictive Analytics

- 5.1.4 Prescriptive Analytics

- 5.1.5 Cognitive Analytics

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Delivery Mode

- 5.3.1 On-Premise

- 5.3.2 Cloud-Based

- 5.3.3 Hybrid

- 5.4 By Application

- 5.4.1 Clinical Analytics

- 5.4.2 Financial & RCM Analytics

- 5.4.3 Operational & Administrative Analytics

- 5.4.4 Population Health Management

- 5.4.5 Fraud Detection & Risk Analytics

- 5.4.6 Life Sciences / R&D Analytics

- 5.5 By End User

- 5.5.1 Healthcare Providers

- 5.5.2 Healthcare Payers

- 5.5.3 Life Science Companies

- 5.5.4 Public Health Agencies

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 3M Company

- 6.3.2 Veradigm Inc.

- 6.3.3 Oracle Health

- 6.3.4 Digital Reasoning Systems Inc.

- 6.3.5 Information Builders, Inc. (IBI)

- 6.3.6 International Business Machines Corporation (IBM)

- 6.3.7 IQVIA Holdings Inc.

- 6.3.8 McKesson Corporation

- 6.3.9 MedeAnalytics, Inc.

- 6.3.10 Optum, Inc.

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 Health Catalyst, Inc.

- 6.3.13 VitreosHealth, Inc.

- 6.3.14 Inovalon, Inc.

- 6.3.15 SAS Institute Inc.

- 6.3.16 Verisk Analytics, Inc.

- 6.3.17 CitiusTech, Inc.

- 6.3.18 Merative

- 6.3.19 SAP SE

- 6.3.20 Microsoft Corporation

- 6.3.21 Siemens Healthineers AG

- 6.3.22 Deloitte Consulting LLP

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment