|

시장보고서

상품코드

1906045

에폭시 수지 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Epoxy Resin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

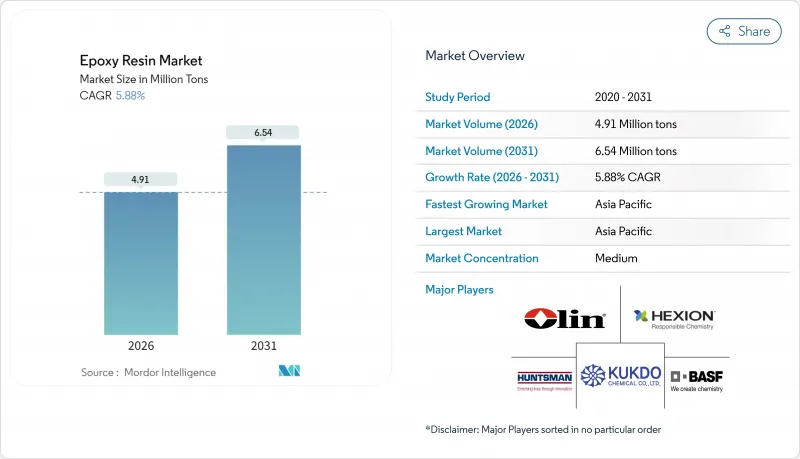

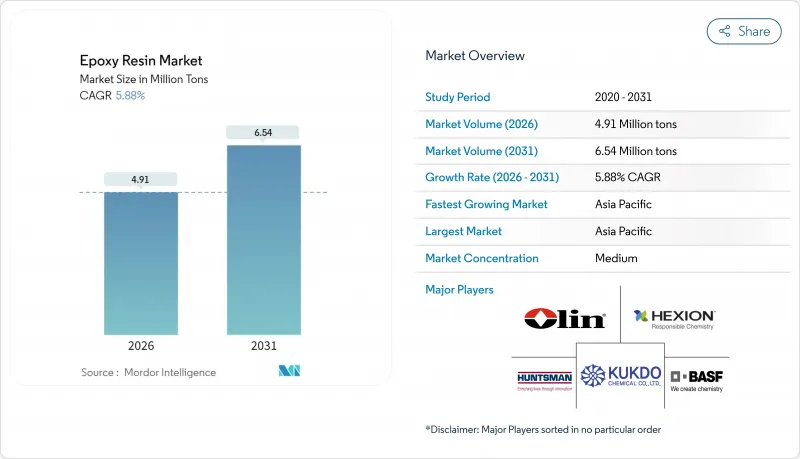

2026년 에폭시 수지 시장의 규모는 491만 톤으로 추정되며, 2025년 464만 톤에서 성장할 전망입니다.

2031년에는 654만톤에 달할 전망으로 2026년부터 2031년에 걸쳐 CAGR 5.88%로 확대될 전망입니다.

지속적인 수요는 풍력 터빈 블레이드에서 반도체 패키징에 이르는 중요한 용도를 지원하는 탁월한 기계적, 화학적, 열적 성능에 뿌리를 두고 있습니다. 비스페놀 A(BPA)와 휘발성 유기화합물(VOC)에 대한 규제 강화에 따라 수성, 바이오순환형, 저VOC 화학기술의 개발이 가속화되고 있습니다. 신재생에너지 인프라의 확대, 전기동향, 신흥국의 인프라 투자가 수요 증가의 원동력이 되는 한편, 무역관세의 인상과 원재료 가격의 변동이 조달 부문에 있어서 단기적인 불확실성을 가져오고 있습니다. 에폭시 수지 시장은 여전히 중간 정도의 집중 상태이지만, 재생 가능 및 식물 유래 배합에 관한 획기적인 연구 개발이 진행되어 기존 기업과 전문 신규 참가 기업 모두에게 기회가 확대되고 있습니다.

세계의 에폭시 수지 시장의 동향 및 인사이트

페인트 및 코팅 분야에서의 수요 증가

페인트 및 코팅 분야는 2024년 에폭시 수지 시장의 60.15%를 차지했으며 계속해서 주요 용도가 되고 있습니다. 동남아시아와 아프리카의 인프라 사업뿐만 아니라 고차단성 및 내식성 도막을 필요로 하는 선박 및 포장 분야의 틈새 수요가 성장을 뒷받침하고 있습니다. 웨스트레이크사가 2025년에 출시한 바이오 순환형 수지 'EpoVIVE'는 공급자가 지속가능성과 성능 간의 균형을 어떻게 도모하고 있는지를 나타내는 좋은 예입니다. 저VOC 제형으로의 전환은 고가의 UV 차단제를 필요로 하지 않고 햇빛 안정성을 향상시키는 양자점 촉매 광화학 기술에 의해 촉진됩니다. Amerlock 400과 같은 선박 등급 시스템은 도킹 간격을 연장하여 선박 운영자의 총 수명주기 비용을 절감합니다. 이로 인해 2030년까지 연평균 복합 성장률(CAGR) 6.51%가 전망되며 코팅 분야는 에폭시 수지 시장 전체에서 양과 혁신의 양면에서 핵심적인 역할을 담당할 것으로 예상되고 있습니다.

풍력 터빈 블레이드 복합재의 도입 확대

해상 풍력 발전 설비 증가, 로터 직경 증가, 하이브리드 탄소섬유 및 유리섬유 설계에 의해 에폭시 수지의 성능 요건이 높아지고 있습니다. 세계풍력에너지협회는 신규 설비용량의 연간 8.8% 성장을 예측하고 있으며, 이는 장기적인 수지 수요를 지원합니다. TPI 컴포지트사의 고객 기반은 2025년 미국 내 육상 블레이드의 88%를 공급하고 있으며 프로세스 노하우가 조달을 통합하는 중요성을 보여줍니다. 지멘스 가메사는 약산성 조건 하에서 박리 가능한 재활용 대응 에폭시 블레이드를 이미 상품화하여 폐기 시의 과제를 줄이고 있습니다. 블레이드 경화 스케줄의 머신러닝을 통한 최적화는 폐기물 및 에너지 사용량을 더욱 줄이고, 풍력에너지 밸류체인에서의 선택으로서 에폭시 수지의 이점을 강화합니다.

원재료 가격의 변동성

중국은 2024년 상반기에 BPA 생산능력을 12.31% 확대해 연간 548만t에 이르렀지만 가동률은 떨어지고 지역 가격은 전기 대비 4.6% 하락했습니다. 국도화학공장 폭발 등의 혼란으로 인해 BPA 가격은 일시적으로 두배로 뛰었고 다운스트림 배합업체는 마진 리스크에 노출됐습니다. 비정상적인 기후와 관련된 불가항력성은 공급 불확실성을 더욱 증가시켰습니다. 이러한 이유로 여러 에폭시 제조업체는 원료 확보 및 가격 변동 위험 회피를 목적으로 자체 에피클로로히드린 및 BPA 제조 설비를 건설하고 있습니다.

부문 분석

DGBEA 수지는 풍력발전 블레이드와 자동차용 복합재의 주력 등급으로 2025년에도 에폭시 수지 시장 점유율의 36.35%를 유지했습니다. CAGR은 6.32%로 예상되어 시장 확대에 필수적인 존재로 남아 있는 반면, 고객 감사는 생산자들이 추적성이 있는 저탄소 BPA 공급을 입증하도록 요구하고 있습니다. 이에 대응하여 구미 및 일본의 공급업체는 에폭시 수지 시장에서 DGBEA의 지위를 유지하기 위해 물질 수지 회계와 바이오 순환 원료의 시험 도입을 진행하고 있습니다.

특수 수지는 명확한 성능 격차를 메웁니다. DGBEF는 선박 유지보수용 도료용으로 저점도를 실현하고 노볼락계 화학제품은 용광로 라이닝의 내열충격성을 발휘합니다. 지방족 에폭시는 건축 외관에 필수적인 UV 안정성을 제공합니다. 글리시딜아민계는 전자기기 케이스에서 뛰어난 금속 밀착성을 발휘합니다. 기타 원료로 분류되는 바이오베이스 및 환형 지방족계 화학제품은 순환형 재활용과 탄소 회계가 주주의 관심을 모으는 가운데 2031년까지 에폭시 수지 시장에서 현저한 점유율을 획득하는 가장 빠른 성장 분야로 예측됩니다.

에폭시 수지 시장의 보고서는 원재료별(비스페놀 A와 ECH, 비스페놀 F와 ECH, 노볼락(포름알데히드 및 페놀), 지방족계(지방족 알코올), 글리시딜아민(방향족 아민 및 ECH), 기타), 용도(페인트 및 코팅, 접착제 및 실란트, 복합재료, 전기 및 전자기기, 기타), 지역(아시아태평양, 북미, 유럽, 기타)별로 분석했습니다.

지역별 분석

아시아태평양은 에폭시 수지 시장의 중심지이며, 2025년 수요의 47.55%를 차지하였고 2031년까지 연평균 복합 성장률(CAGR) 6.08%로 추이할 것으로 예측되고 있습니다. 중국의 수지 수출은 미국에 의한 최대 354.99%의 반덤핑 관세에 직면하고 있으며, DCM 슈리람사의 1억 2,500만 달러 규모 인도 신규 공장 등, 보다 지역적으로 분산된 고객 기반을 통한 대응이 촉구되고 있습니다. 태국과 베트남은 신규 PCB(프린트 기판) 및 풍력 블레이드 생산 능력을 획득하는 한편, 일본과 한국은 반도체 및 해상 풍력 용도를 위한 초고 Tg(유리 전이 온도) 및 재생 가능한 화학물질의 개발을 추진하고 있습니다.

북미에서는 리쇼어링, 인프라 투자, 신재생에너지 세액공제를 활용하여 수입 수지 공급의 변동을 완화하고 있습니다. 1.01%에서 547.76%에 이르는 상쇄 관세로 국내 제조업체는 휴지 중인 반응 장치를 재가동시켜 새로운 원료 자산에 대한 투자를 촉진하고 있습니다. 캐나다의 풍력 발전소 개발 사업자는 북극권 대응 에폭시 수지 시스템을 지정하고, 멕시코의 자동차 산업 클러스터는 구조용 접착제 수요를 가속화하고 있습니다. NREL(미국 재생에너지 연구소)의 식물 유래 에폭시 연구는 이 지역의 지속가능성에 대한 리더십을 뒷받침하고 있습니다.

유럽에서는 엄격한 BPA 규제와 첨단 R&D 간의 균형을 맞추고 있습니다. 독일의 자동차 부품 공급업체는 현지 수지 배합 제조업체와 공동으로 열전도성 EMC를 개발하고 있습니다. 영국의 해상풍력 붐은 에폭시 도장 모노파일의 25년 내구성 요구를 뒷받침하며, 프랑스의 원자력 부문은 내방사선 등급을 추진하고 있습니다. 스콧 베이더사의 영국 내 3,000만 파운드 규모 생산 능력 증강은 세계적인 물류 변동 가운데 현지 공급에 대한 대처를 드러내고 있습니다. 북유럽은 순환형 경제 정책에 이미 선행하고 있으며 EU 자금 프로그램 하에서 폐루프형 에폭시 재활용 시험을 추진하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 페인트 및 코팅 분야에서의 수요 증가

- 풍력 터빈 블레이드용 복합재료의 도입 상황

- 전기 및 전자기기 분야에서의 수요 증가

- 인프라 주도에 의한 접착제 수요 증가

- 3D 프린팅용 에폭시 포토폴리머 도입

- 억제요인

- 원재료 가격의 변동성

- 휘발성 유기 화합물(VOC) 및 비스페놀 A(BPA)에 관한 규제 강화

- 반덤핑 관세에 의한 무역의 흐름에 대한 영향

- 밸류체인 분석

- Porter's Five Forces

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체 제품 및 서비스의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측(금액 및 수량)

- 원재료별

- DGBEA(비스페놀 A 및 ECH)

- DGBEF(비스페놀 F 및 ECH)

- 노볼락(포름알데히드와 페놀)

- 지방족(지방족 알코올)

- 글리시딜아민(방향족 아민 및 ECH)

- 기타 원재료(지환족, 바이오 에폭시 수지)

- 물리 형태별

- 액체

- 고체

- 솔루션

- 수성 분산액

- 용도별

- 도료 및 코팅

- 접착제 및 실란트

- 복합재료

- 전기 및 전자기기

- 풍력 터빈

- 해양

- 기타 용도(건설, 3D 프린팅용 포토폴리머 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 튀르키예

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 카타르

- 아랍에미리트(UAE)

- 나이지리아

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 순위 분석

- 기업 프로파일

- Atul Ltd

- Bodo Moller Chemie GmbH

- Cardolite Corporation

- Chang Chun Group

- DIC Corporation

- Dow

- Grasim Industries Limited

- Hexion Inc.

- Huntsman International LLC

- Jiangsu Sanmu Group Co., Ltd.

- Kolon Industries

- Kukdo Chemical Co., Ltd

- Mitsui Chemicals, Inc.

- Nama

- Nan Ya Plastics Corporation

- Olin Corporation

- Robnor ResinLab Ltd,

- Sika AG

- Sinochem Holdings Corporation Ltd.

- Association for Chemical and Metallurgical Production(SPOLCHEMIE)

- Westlake Corporation

제7장 시장 기회 및 미래 전망

CSM 26.01.28Epoxy Resin Market size in 2026 is estimated at 4.91 Million tons, growing from 2025 value of 4.64 Million tons with 2031 projections showing 6.54 Million tons, growing at 5.88% CAGR over 2026-2031.

Sustained demand is rooted in the material's unmatched mechanical, chemical, and thermal performance that underpins critical uses ranging from wind-turbine blades to semiconductor packaging. Innovation is accelerating as stricter regulations on bisphenol A (BPA) and volatile organic compounds (VOCs) advance waterborne, bio-circular, and low-VOC chemistries. Expanding renewable-energy infrastructure, electrification trends, and infrastructure spending in emerging economies add positive volume momentum, while escalating trade duties and raw-material price swings present near-term uncertainties for procurement teams. The epoxy resins market remains moderately concentrated, yet breakthrough work on recyclable and plant-derived formulations is widening the opportunity set for both incumbents and specialist newcomers.

Global Epoxy Resin Market Trends and Insights

Increasing Demand from Paints and Coatings

Paints and coatings continued to dominate the epoxy resins market with a 60.15% revenue share in 2024. Growth is reinforced by infrastructure programs in Southeast Asia and Africa and by marine and packaging niches that depend on high-barrier, corrosion-resistant finishes. Westlake's 2025 launch of EpoVIVE bio-circular resins illustrates how suppliers are balancing sustainability with performance. The shift to low-VOC formulations is aided by quantum-dot-catalyzed photochemistry that improves sunlight stability without costly UV blockers Marine-grade systems such as Amerlock 400 lengthen dry-dock cycles, lowering total lifecycle cost for fleet operators.The resulting 6.51% CAGR to 2030 positions coatings as both volume and innovation anchors for the broader epoxy resins market.

Wind-Turbine Blade Composites Uptake

Growing offshore wind installations, larger rotor diameters, and hybrid carbon-glass designs are raising epoxy performance thresholds. The Global Wind Energy Council forecasts 8.8% annual growth in new capacity, which underpins long-run resin demand. TPI Composites' customer base supplied 88% of 2025 US onshore blades, underscoring how process know-how consolidates purchasing. Siemens Gamesa has already commercialized recyclable epoxy blades that de-bond under mild acidic conditions, easing end-of-life challenges. Machine-learning optimization of blade cure schedules further cuts waste and energy use, reinforcing epoxy's position as the matrix of choice in the wind energy value chain.

Raw-Material Price Volatility

China expanded BPA capacity by 12.31% in H1 2024 to 5.48 million t pa, yet utilization dipped and regional prices fell 4.6% quarter-on-quarter. Disruptions such as the Guodu Chemical plant explosion temporarily doubled BPA prices, exposing downstream formulators to margin risk. Force-majeure declarations following extreme weather events added further supply uncertainty. Several epoxy majors are therefore building captive epichlorohydrin and BPA units to secure feedstock and hedge volatility.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand from Electrical and Electronics

- Growing Infrastructure-Led Adhesive Demand

- Stricter VOC and BPA Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DGBEA resins retained 36.35% epoxy resin market share in 2025 as the workhorse grade for wind-energy blades and automotive composites. At a 6.32% CAGR they remain integral to market expansion, yet customer audits are pushing producers to demonstrate traceable, lower-carbon BPA supply. In response, Western and Japanese suppliers are piloting mass-balance accounting and bio-circulating feedstocks to preserve DGBEA's position in the epoxy resins market.

Specialty resins fill clear performance gaps. DGBEF offers lower viscosity for marine maintenance coatings, while novolac chemistries withstand thermal shock inside furnace linings. Aliphatic epoxies deliver UV stability essential for architectural facades. Glycidylamine versions provide superior metal adhesion in electronics housings. Bio-based and cycloaliphatic chemistries, grouped under other raw materials, are projected to be the fastest movers and could capture a measurable slice of the epoxy resins market by 2031 as closed-loop recycling and carbon accounting gain shareholder focus.

The Epoxy Resin Market Report is Segmented by Raw Material (DGBEA (Bisphenol A and ECH), DGBEF (Bisphenol F and ECH), Novolac (Formaldehyde and Phenols), Aliphatic (Aliphatic Alcohols), Glycidylamine (Aromatic Amines and ECH), and More), Application (Paints and Coatings, Adhesives and Sealants, Composites, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, and More).

Geography Analysis

Asia-Pacific remained the epicenter of the epoxy resin market, securing 47.55% of 2025 demand and pointing to a 6.08% CAGR through 2031. China's resin exports face US anti-dumping duties as high as 354.99%, prompting ventures like DCM Shriram's USD 125 million Indian greenfield unit to serve a more regionally diversified customer base. Thailand and Vietnam capture fresh PCB and wind-blade capacity, while Japan and South Korea push ultra-high-Tg and recyclable chemistries for semiconductors and offshore wind applications.

North America leverages reshoring, infrastructure investment, and renewable-energy tax credits to buffer volatility in imported resin flows. Countervailing duties ranging from 1.01% to 547.76% spur domestic producers to reactivate idled reactors and invest in new feedstock assets. Canadian wind-farm developers specify Arctic-grade epoxy systems, and Mexico's automotive clusters accelerate demand for structural adhesives. NREL's plant-derived epoxy research underscores the region's sustainability leadership.

Europe balances stringent BPA rules with cutting-edge R&D. German automotive suppliers co-engineer thermally conductive EMCs with local resin formulators. The United Kingdom's offshore wind boom sustains 25-year service life requirements for epoxy-primed monopiles, and France's nuclear sector pushes radiation-resistant grades. Scott Bader's GBP 30 million UK capacity addition highlights commitments to local supply amid global logistics flux. The Nordic region, already well advanced in circular-economy policy, pilots closed-loop epoxy recycling trials under EU-funded programs.

- Atul Ltd

- Bodo Moller Chemie GmbH

- Cardolite Corporation

- Chang Chun Group

- DIC Corporation

- Dow

- Grasim Industries Limited

- Hexion Inc.

- Huntsman International LLC

- Jiangsu Sanmu Group Co., Ltd.

- Kolon Industries

- Kukdo Chemical Co., Ltd

- Mitsui Chemicals, Inc.

- Nama

- Nan Ya Plastics Corporation

- Olin Corporation

- Robnor ResinLab Ltd,

- Sika AG

- Sinochem Holdings Corporation Ltd.

- Association for Chemical and Metallurgical Production (SPOLCHEMIE)

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand from Paints and Coatings

- 4.2.2 Wind-Turbine Blade Composites Uptake

- 4.2.3 Increasing Demand from Electrical and Electronics

- 4.2.4 Growing Infrastructure-Led Adhesive Demand

- 4.2.5 3-D Printed Epoxy Photopolymers Adoption

- 4.3 Market Restraints

- 4.3.1 Raw-Material Price Volatility

- 4.3.2 Stricter VOC and BPA Regulations

- 4.3.3 Anti-Dumping Duties Disrupting Trade Flows

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Raw Material

- 5.1.1 DGBEA (Bisphenol A and ECH)

- 5.1.2 DGBEF (Bisphenol F and ECH)

- 5.1.3 Novolac (Formaldehyde and Phenol)

- 5.1.4 Aliphatic (Aliphatic Alcohols)

- 5.1.5 Glycidylamine (Aromatic Amines and ECH)

- 5.1.6 Other Raw Materials (Cycloaliphatic, Bio-based Epoxies)

- 5.2 By Physical Form

- 5.2.1 Liquid

- 5.2.2 Solid

- 5.2.3 Solution

- 5.2.4 Waterborne Dispersion

- 5.3 By Application

- 5.3.1 Paints and Coatings

- 5.3.2 Adhesives and Sealants

- 5.3.3 Composites

- 5.3.4 Electrical and Electronics

- 5.3.5 Wind Turbines

- 5.3.6 Marine

- 5.3.7 Other Applications (Construction, 3-D Printing Photopolymers, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordics

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%) Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Atul Ltd

- 6.4.2 Bodo Moller Chemie GmbH

- 6.4.3 Cardolite Corporation

- 6.4.4 Chang Chun Group

- 6.4.5 DIC Corporation

- 6.4.6 Dow

- 6.4.7 Grasim Industries Limited

- 6.4.8 Hexion Inc.

- 6.4.9 Huntsman International LLC

- 6.4.10 Jiangsu Sanmu Group Co., Ltd.

- 6.4.11 Kolon Industries

- 6.4.12 Kukdo Chemical Co., Ltd

- 6.4.13 Mitsui Chemicals, Inc.

- 6.4.14 Nama

- 6.4.15 Nan Ya Plastics Corporation

- 6.4.16 Olin Corporation

- 6.4.17 Robnor ResinLab Ltd,

- 6.4.18 Sika AG

- 6.4.19 Sinochem Holdings Corporation Ltd.

- 6.4.20 Association for Chemical and Metallurgical Production (SPOLCHEMIE)

- 6.4.21 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment