|

시장보고서

상품코드

1906054

산업용 공기압축기 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Industrial Air Compressors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

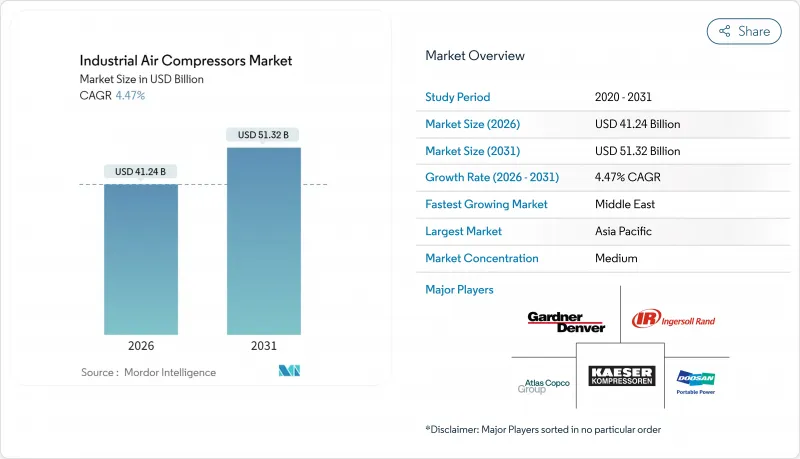

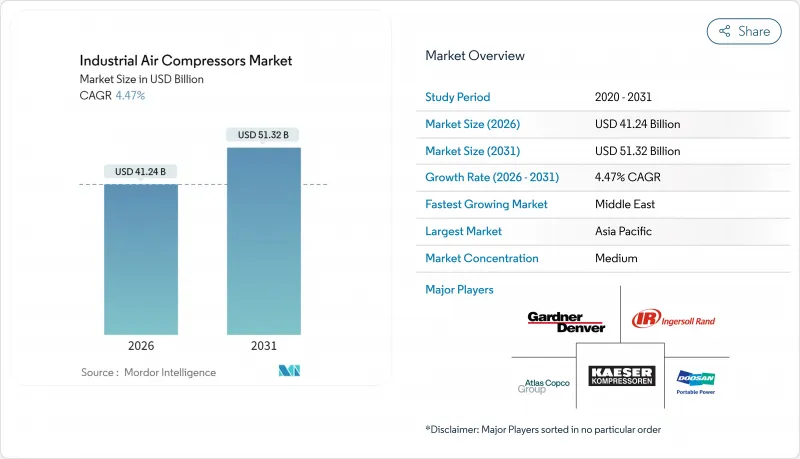

산업용 공기압축기 시장의 규모는 2026년에는 412억 4,000만 달러로 추정되고 있으며, 2025년 394억 8,000만 달러에서 성장할 것으로 예상됩니다.

2031년에는 513억 2,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 4.47%로 확대될 전망입니다.

에너지 효율적인 생산 라인에 대한 투자 증가, LNG 인프라의 급속한 확충 및 엄격한 오염 기준에 따라 주요 최종 용도 부문 전체에서 제품 선호가 변화하고 있습니다. 플랜트 운영자가 배출규제와 총소유비용 목표 간의 균형을 맞추고 있는 가변속기술, 무급유식 구조, IoT 대응 감시 플랫폼이 주목을 받고 있습니다. 지역별로는 아시아태평양의 기세가 가장 강하고 중동은 대규모 가스 프로젝트를 배경으로 가장 빠른 성장을 보이고 있습니다. 한편, 원재료 가격의 변동이나 유럽의 소음 규제 강화에 의해 이익률이 압박되어 투자 회수 기간이 장기화하고 있기 때문에 강재 사용량의 감축과 음향 성능의 향상을 도모하는 설계 변경이 진행되고 있습니다. 산업용 공기압축기 시장은 제품 혁신을 탈탄소화 정책과 산업 구조의 변화에 맞춰 계속 높은 회복력을 보이고 있습니다.

세계의 산업용 공기압축기 시장의 동향 및 인사이트

아시아의 에너지 절약형 제조시설 확대

반도체 붐으로 대만의 2024년 4분기 고정자산 투자는 69% 증가했습니다. 전자기기 공장에서는 오염 방지를 위해 클래스 0 무급유식 시스템을 도입하고 있습니다. 에너지 사용량을 최대 35% 줄이는 가변속 구동 장치는 신규 라인의 기본 사양이 되었습니다. 중국과 인도에서 로봇공학과 적층제조를 확대하는 다국적기업도 비슷한 노력을 추진하고 있으며, 산업용 공기압축기 시장의 장기적인 수요를 뒷받침하고 있습니다.

식품 및 음료 가공 분야에서 무급유식 압축기 수요 증가

ISO 8573-1 Class 0은 많은 관할 구역에서 모범 사례에서 규제 요구사항으로 전환되어 가공업자를 무급유식 스크류 및 스크롤 압축기로 이동시킵니다. 히타치 글로벌사의 에어 파워 DS280-450 kW 출시는 고출력 무급유식 옵션에 대한 요구를 충족합니다. 유지보수 비용 절감과 윤활유 폐기 방지로 초기 비용의 할인율을 상쇄하고 선진국 시장 전반적인 도입을 뒷받침하고 있습니다.

강재 가격 변동이 압축기 부품 원가 구조를 밀어 올립니다.

강재는 압축기 생산 비용의 최대 50%를 차지하므로 가격 급등 시 OEM의 이익률이 변동합니다. 유럽의 제조업체는 2024년 에너지 비용이 강재 조달 가격에 반영된 정가 개정을 다수 실시했습니다. 판 두께 감소나 복합재료로의 전환 설계가 검토되고 있지만, 인증 취득의 장벽에 의해 광범위한 비용 절감의 실현은 늦어지고 있습니다.

부문 분석

용적식 기술은 2025년 시점에서 산업용 공기압축기 시장의 75.40%를 차지하였고, 이는 일반 제조업에서 광업까지 폭넓은 용도에 대응하는 범용성을 반영하고 있습니다. 로터리 스크류 유닛은 효율성과 유지보수성이 균형을 이루므로 수요가 안정적입니다. 동적 원심 압축기는 규모가 작지만, LNG 플랜트나 제철소가 안정된 압력 하에서 고유량을 요구하기 때문에 6.69%의 연평균 복합 성장률(CAGR)로 확대하고 있습니다.

원심 유닛의 산업용 공기압축기 시장 내 규모는 에너지 효율화 규제를 뒷받침함으로써 2026년과 2031년 사이에 27억 3,000만 달러 가량 증가할 것으로 예측됩니다. 예기치 않은 가동 중지 시간을 줄이기 위해 IoT 호환 컨트롤러와 예측 분석 기술이 두 기술에 통합되어 있습니다. Atlas Copco와 같은 OEM 제조업체는 현재 부하 프로파일을 추적하고 에너지 절약 모드를 권장하는 Optimizer 4.0 모듈을 압축기 패키지에 번들로 제공합니다.

유침식 설계는 2025년 시점에서 비용 우위성을 유지해 62.30%의 점유율을 차지하였지만, 의약품 및 식품 분야에서의 오염 허용도 하락에 의해 무급유식 시스템은 CAGR 6.33%로 진전하고 있습니다. 무급유식 스크류 유닛의 산업용 공기압축기 시장 내 규모는 라이프사이클 유지비와 폐기 비용 절감 효과로 2031년까지 154억 달러를 초과할 전망입니다.

신형 이단식 드라이 스크류는 기존 모델 대비 최대 13.5%의 에너지 절약을 실현하여 투자 회수 기간을 단축합니다. 클래스 0 인증 마케팅은 구매 판단에 영향을 미치고 있으며, 음료 병입회사는 입찰 서류에서 이를 명시적으로 요구하는 경우가 많습니다.

지역별 분석

아시아태평양은 2025년 세계 수익의 41.70%를 차지했으며 중국의 급속한 자동화 확대와 인도의 PLI(생산 연동형 인센티브) 제도에 의한 자사 내 공기 생성 촉진이 견인역이 되었습니다. 플랜트 운영자는 에너지 회수 모듈 부착 통합 에어 스테이션을 선호하고 도입하여, 이 동향이 자본 설비 입찰의 양상을 바꾸고 있습니다. 현지 조립업체는 다국적 OEM과 기술 라이선싱 제휴를 맺어 산업용 공기압축기 시장을 더욱 확대하고 있습니다.

북미에서는 리쇼어링과 미국 에너지부(DOE)의 효율화 규제가 구식 고정속도 플릿의 대체를 촉진하고 있습니다. 미국 걸프만의 LNG 수출 터미널에서는 수메가와트급 원심 압축기 라인이 도입되어 고압 용도의 지역 우위를 강화하고 있습니다. 캐나다는 저탄소 수소 프로젝트에 주력함에 따라 무급유식 스크류 패키지 수요가 더욱 증가하고 있습니다.

중동지역은 가스 저장, 석유화학 다각화, 대형 정유소 업그레이드를 원동력으로 5.72%라는 가장 높은 CAGR을 기록하고 있습니다. 유럽에서는 원재료 가격 상승으로 인한 비용 압력이 있지만, 최종 사용자가 소음 규제 대응과 탄소 저감을 우선시하기 때문에 안정적인 수요를 유지하고 있습니다. 라틴아메리카와 아프리카에서는 광업과 인프라 정비의 사이클에 연동된 간헐적인 수요를 볼 수 있으며, 임대 설비가 프로젝트 간의 갭을 메우면서 산업용 공기압축기 시장의 확대에 기여하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 아시아의 에너지 절약형 제조 시설 확대

- 식품 및 음료 가공 분야에서의 무급유식 압축기 수요 증가

- 고압 압축기를 필요로 하는 LNG 인프라에 대한 투자 급증

- 산업용 에너지 감사에 대한 정부의 우대조치가 가변속 압축기를 뒷받침

- 드라이 스크류 압축기를 도입한 EV 배터리용 기가팩토리의 급속한 확대

- 중동 석유화학 플랜트의 기존 설비 업그레이드(브라운필드) 증가 경향

- 억제요인

- 변동하는 강재 가격이 압축기의 부품 원가 구조를 밀어 올림

- 저압 용도의 송풍기 대체품 대비 긴 회수 기간

- 유럽에서의 엄격한 소음 배출 기준이 케이스 비용을 밀어 올림

- 신흥 시장에서의 숙련된 유지보수 인력 부족에 의한 다운타임 증가

- 가치 및 공급망 분석

- 규제 또는 기술적 전망

- 투자분석

- 주요 사례 연구 및 도입 시나리오

- Porter's Five Forces 분석

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 압축기 유형별

- 용적식

- 로터리 스크류

- 왕복식(피스톤)

- 스크롤

- 다이나믹

- 원심

- 축류

- 용적식

- 윤활제별

- 오일 침지식

- 무급유식

- 정격압력별

- 0-20 bar

- 21-100 bar

- 100 bar 이상

- 구동 방식 및 전원별

- 전기

- 디젤

- 가스

- 정격 출력별

- 100 kW 이하

- 101-500 kW

- 500kW 초과

- 최종 이용 산업별

- 제조업

- 일반 제조업

- 금속 및 광업

- 전자기기 및 반도체

- 석유 및 가스

- 업스트림 부문

- 미드스트림 부문(파이프라인 및 LNG)

- 다운스트림 부문(정제)

- 발전

- 화학제품 및 석유화학제품

- 식품 및 음료

- 제약

- 건설

- 기타(의료, 섬유)

- 제조업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 기타 유럽

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Atlas Copco AB

- Ingersoll Rand Inc.

- Kaeser Kompressoren SE

- Sullair LLC(Hitachi Group)

- Gardner Denver Holdings Inc.

- Siemens Energy AG

- Bauer Kompressoren GmbH

- Doosan Portable Power

- ELGi Equipments Ltd.

- Quincy Compressor LLC

- Fusheng Industrial Co. Ltd.

- Kobe Steel Ltd.

- Hanwha Power Systems

- Boge Kompressoren Otto Boge GmbH & Co. KG

- Aerzen Maschinenfabrik GmbH

- CompAir(UK) Ltd.

- Chicago Pneumatic

- VMAC Global Technology Inc.

- Shanghai Screw Compressor Co. Ltd.

- Kobelco KNW(Industrial Air Compressors)

제7장 시장 기회 및 미래 전망

CSM 26.01.28Industrial Air Compressors market size in 2026 is estimated at USD 41.24 billion, growing from 2025 value of USD 39.48 billion with 2031 projections showing USD 51.32 billion, growing at 4.47% CAGR over 2026-2031.

Rising investments in energy-efficient production lines, rapid LNG infrastructure build-outs and stricter contamination standards are reshaping product preferences in every major end-use sector. Variable-speed technology, oil-free architectures and IoT-enabled monitoring platforms are gaining traction as plant operators balance emission mandates with total cost-of-ownership goals. Regional momentum remains strongest in Asia-Pacific, while the Middle East delivers the fastest growth on the back of large-scale gas projects. At the same time, raw-material price volatility and tighter European noise rules are compressing margins and extending payback periods, prompting redesigns that lower steel content and improve acoustic performance. The Industrial Air Compressors market continues to demonstrate resilience by aligning product innovation with decarbonization policies and shifting industrial footprints.

Global Industrial Air Compressors Market Trends and Insights

Expansion of Energy-Efficient Manufacturing Facilities in Asia

The semiconductor boom lifted Taiwan's fixed-asset spending by 69% in Q4 2024, with electronics plants adopting Class 0 oil-free systems to guard against contamination. Variable-speed drives that trim energy use up to 35% are now baseline specifications across new lines. Multinationals scaling robotics and additive manufacturing in China and India mirror this focus, anchoring long-term volume for the Industrial Air Compressors market.

Rising Demand for Oil-Free Compressors in Food & Beverage Processing

ISO 8573-1 Class 0 has moved from best practice to regulatory requirement in many jurisdictions, pushing processors toward oil-free screws and scrolls. Hitachi Global Air Power's DS280-450 kW launch addresses requests for higher-power oil-free options. Lower maintenance and avoided lubricant disposal are offsetting the upfront premium, reinforcing adoption across developed markets.

Volatile Steel Prices Inflating Compressor BOM Cost Structures

Steel accounts for up to 50% of compressor production cost, exposing OEMs to margin swings when prices spike. European makers implemented multiple list-price rises in 2024 as energy costs fed into steel inputs. Design efforts to cut plate thickness and switch to composites are under evaluation, yet certification hurdles delay widespread relief.

Other drivers and restraints analyzed in the detailed report include:

- Surging Investments in LNG Infrastructure Requiring High-Pressure Compressors

- Government Incentives for Industrial Energy Audits Favoring Variable-Speed Compressors

- Stringent Noise Emission Norms Escalating Enclosure Costs in Europe

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Positive displacement technology held 75.40% of the Industrial Air Compressors market share in 2025, reflecting its versatility from general manufacturing to mining. Demand remains stable as rotary screw units balance efficiency and maintenance needs. Dynamic centrifugal compressors, although smaller in volume, are expanding at a 6.69% CAGR as LNG plants and steel mills seek higher flow at consistent pressure.

The Industrial Air Compressors market size for centrifugal units is projected to increase by USD 2.73 billion between 2026 and 2031, supported by energy-efficiency mandates. IoT-enabled controllers and predictive analytics are being embedded across both technologies to lower unplanned downtime. OEMs such as Atlas Copco now bundle Optimizer 4.0 modules with compressor packages to track load profiles and recommend energy-saving modes.

Oil-flooded designs retained cost leadership and 62.30% share in 2025, yet oil-free systems are advancing at 6.33% CAGR as contamination tolerance narrows in pharmaceuticals and food. The Industrial Air Compressors market size for oil-free screws is on course to climb beyond USD 15.4 billion by 2031, aided by lower lifecycle maintenance and disposal savings.

Newer two-stage dry screws trim energy use as much as 13.5% versus prior models, improving payback windows. Class 0 certification marketing is influencing purchasing decisions, and beverage bottlers often specify it outright in bid documents.

The Industrial Air Compressor Market Report is Segmented by Compressor Type (Positive Displacement and More), Lubrication (Oil-Flooded, Oil-Free), Pressure Rating (0-20 Bar, 21-100 Bar, Above 100 Bar), Driver/Power Source (Electric and More), Power Rating (>500 KW and More), End-Use Industry (Manufacturing and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 41.70% of global revenue in 2025, anchored by China's automation surge and India's PLI inducements that encourage in-house air generation. Plant operators favor integrated air stations with energy-recovery modules, a trend reshaping capital-equipment bids. Local assemblers partner with multinational OEMs for technology licensing, further expanding the Industrial Air Compressors market.

North America benefits from reshoring and DOE efficiency rules that spur replacement of legacy fixed-speed fleets. LNG export terminals along the U.S. Gulf Coast order multi-megawatt centrifugal lines, reinforcing regional dominance in high-pressure applications. Canada's focus on low-carbon hydrogen projects adds incremental volume for oil-free screw packages.

The Middle East registers the fastest 5.72% CAGR, driven by gas storage, petrochemical diversification and mega-refinery upgrades. Europe maintains steady demand as end-users prioritize noise compliance and carbon reduction, despite cost pressures from material inflation. Latin America and Africa offer episodic demand tied to mining and infrastructure cycles, with rental fleets bridging project gaps and enlarging the Industrial Air Compressors market footprint.

- Atlas Copco AB

- Ingersoll Rand Inc.

- Kaeser Kompressoren SE

- Sullair LLC (Hitachi Group)

- Gardner Denver Holdings Inc.

- Siemens Energy AG

- Bauer Kompressoren GmbH

- Doosan Portable Power

- ELGi Equipments Ltd.

- Quincy Compressor LLC

- Fusheng Industrial Co. Ltd.

- Kobe Steel Ltd.

- Hanwha Power Systems

- Boge Kompressoren Otto Boge GmbH & Co. KG

- Aerzen Maschinenfabrik GmbH

- CompAir (UK) Ltd.

- Chicago Pneumatic

- VMAC Global Technology Inc.

- Shanghai Screw Compressor Co. Ltd.

- Kobelco KNW (Industrial Air Compressors)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Energy-Efficient Manufacturing Facilities in Asia

- 4.2.2 Rising Demand for Oil-Free Compressors in Food and Beverage Processing

- 4.2.3 Surging Investments in LNG Infrastructure Requiring High-Pressure Compressors

- 4.2.4 Government Incentives for Industrial Energy Audits Favoring Variable-Speed Compressors

- 4.2.5 Rapid Growth of EV Battery Gigafactories Utilizing Dry Screw Compressors

- 4.2.6 Uptick in Brownfield Revamps of Petrochemical Plants in Middle East

- 4.3 Market Restraints

- 4.3.1 Volatile Steel Prices Inflating Compressor BOM Cost Structures

- 4.3.2 Longer Payback Period Versus Blower Alternatives for Low-Pressure Applications

- 4.3.3 Stringent Noise Emission Norms Escalating Enclosure Costs in Europe

- 4.3.4 Skilled Maintenance Labor Shortages Increasing Downtime in Emerging Markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Investment Analysis

- 4.7 Key Case Studies and Implementation Scenarios

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Compressor Type

- 5.1.1 Positive Displacement

- 5.1.1.1 Rotary Screw

- 5.1.1.2 Reciprocating (Piston)

- 5.1.1.3 Scroll

- 5.1.2 Dynamic

- 5.1.2.1 Centrifugal

- 5.1.2.2 Axial

- 5.1.1 Positive Displacement

- 5.2 By Lubrication

- 5.2.1 Oil-Flooded

- 5.2.2 Oil-Free

- 5.3 By Pressure Rating

- 5.3.1 0-20 bar

- 5.3.2 21-100 bar

- 5.3.3 Above 100 bar

- 5.4 By Driver/Power Source

- 5.4.1 Electric

- 5.4.2 Diesel

- 5.4.3 Gas

- 5.5 By Power Rating

- 5.5.1 <=100 kW

- 5.5.2 101-500 kW

- 5.5.3 >500 kW

- 5.6 By End-use Industry

- 5.6.1 Manufacturing

- 5.6.1.1 General Manufacturing

- 5.6.1.2 Metal & Mining

- 5.6.1.3 Electronics & Semiconductors

- 5.6.2 Oil and Gas

- 5.6.2.1 Upstream

- 5.6.2.2 Midstream (Pipeline/LNG)

- 5.6.2.3 Downstream (Refining)

- 5.6.3 Power Generation

- 5.6.4 Chemical and Petrochemical

- 5.6.5 Food and Beverage

- 5.6.6 Pharmaceutical

- 5.6.7 Construction

- 5.6.8 Others (Healthcare, Textiles)

- 5.6.1 Manufacturing

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Nordics

- 5.7.3.7 Rest of Europe

- 5.7.4 Middle East and Africa

- 5.7.4.1 United Arab Emirates

- 5.7.4.2 Saudi Arabia

- 5.7.4.3 South Africa

- 5.7.4.4 Rest of Middle East and Africa

- 5.7.5 Asia-Pacific

- 5.7.5.1 China

- 5.7.5.2 India

- 5.7.5.3 Japan

- 5.7.5.4 South Korea

- 5.7.5.5 Australia

- 5.7.5.6 Rest of Asia-Pacific

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Atlas Copco AB

- 6.4.2 Ingersoll Rand Inc.

- 6.4.3 Kaeser Kompressoren SE

- 6.4.4 Sullair LLC (Hitachi Group)

- 6.4.5 Gardner Denver Holdings Inc.

- 6.4.6 Siemens Energy AG

- 6.4.7 Bauer Kompressoren GmbH

- 6.4.8 Doosan Portable Power

- 6.4.9 ELGi Equipments Ltd.

- 6.4.10 Quincy Compressor LLC

- 6.4.11 Fusheng Industrial Co. Ltd.

- 6.4.12 Kobe Steel Ltd.

- 6.4.13 Hanwha Power Systems

- 6.4.14 Boge Kompressoren Otto Boge GmbH & Co. KG

- 6.4.15 Aerzen Maschinenfabrik GmbH

- 6.4.16 CompAir (UK) Ltd.

- 6.4.17 Chicago Pneumatic

- 6.4.18 VMAC Global Technology Inc.

- 6.4.19 Shanghai Screw Compressor Co. Ltd.

- 6.4.20 Kobelco KNW (Industrial Air Compressors)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need