|

시장보고서

상품코드

1906063

폴리실록산 코팅 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Polysiloxane Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

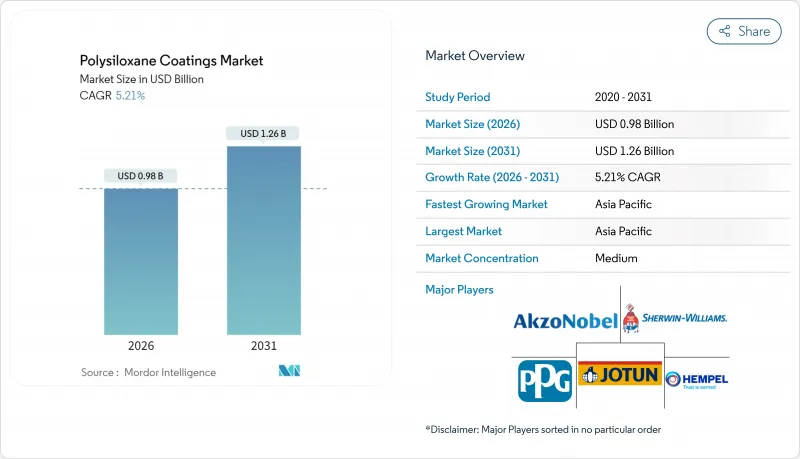

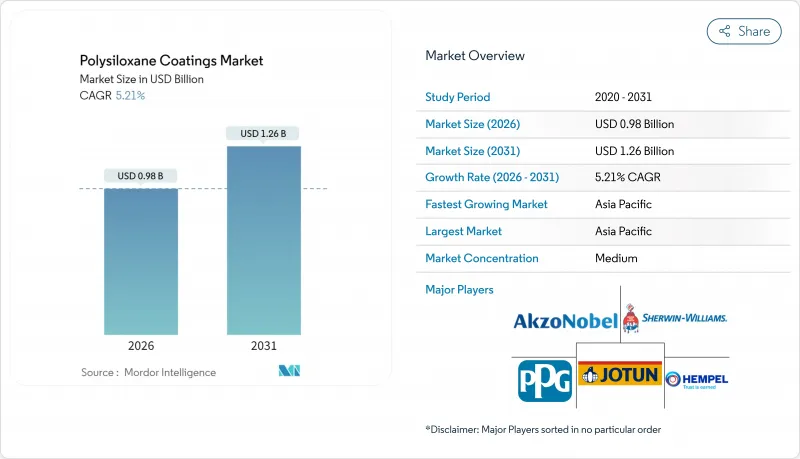

폴리실록산 코팅 시장은 2025년 9억 3,000만 달러에서 2026년 9억 8,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 5.21%로 성장을 지속하여 2031년까지 12억 6,000만 달러에 달할 것으로 예측됩니다.

가혹한 해양환경 및 에너지 분야에서 이러한 실리콘-유기 하이브리드 재료의 사양 증가, 신흥국의 인프라 투자 확대, 세계적인 VOC 규제 강화가 더하여 수요의 기세를 뒷받침하고 있습니다. 사양 설계 엔지니어는 폴리실록산 방식을 유지보수 사이클 연장, 수명 주기 비용 절감, 진화하는 건강 안전 기준 준수를 실현하는 효과적인 수단으로 파악하고 있으며, 이 인식은 프리미엄 가격 설정의 기반을 강화하고 있습니다. 주요 공급업체는 3코트 아연이 풍부한 에폭시 폴리우레탄 도장 체계를 대체하는 2코트 에폭시 폴리실록산 대체품을 강조하고 있어 숙련 도장공이 부족한 시대에 노동력 수요를 절감합니다. 한편, 초고고형분 유형은 엣지의 피복성을 손상시키지 않고 용제 방출을 저감합니다. 경쟁의 초점은 수지 혁신, 인수 주도 포트폴리오 구축, 반복 수주를 보장하는 지역 특화형 기술 서비스 프로그램으로 전환하고 있습니다.

세계의 폴리실록산 코팅 시장의 동향 및 인사이트

부식성 환경에서 해양 및 셰일 자산의 석유 및 가스 설비 투자 확대

세계 업스트림 사업자는 강재를 염화물, CO2, H2S의 고농도 환경에 노출시키는 심해 및 셰일 광구에 신규 자본을 투입하고 있습니다. 폴리실록산 기술은 2회 도포에 필요한 C5 보호를 실현해, 해마다 좁아지는 기상 조건의 범위 내에서 부체식 생산 플랫폼의 트리밍 시간을 단축합니다. 자산 소유자는 기존의 에폭시 도료에 비해 도막하 브리징이 적은 점도 높이 평가하고 있으며, 이는 비말 구역에서 고비용 보수 작업을 지연시키는 이점이 있습니다. 최근 인증된 방식에서는 염수 분무 시험으로 15,000시간 이상을 달성했으며, 3,000시간의 QUV 시험 후에도 광택 유지율 85% 이상을 유지하여 본 기술의 내구성을 입증하는 결과가 되었습니다. 따라서 해외 계약자는 수명 연장 프로그램의 일환으로 재킷, 갑판, 플레어 타워의 표준 유지보수 사양에 폴리실록산계 탑 코트를 통합하고 있습니다. 서비스 제공업체는 높은 도막 두께를 형성하는 능력으로 1회의 크로스 스프레이로 충분한 엣지 보호가 가능해 원격 해역에서의 노동력 부족에 의한 생산성 과제를 완화할 수 있다는 점을 강조하고 있습니다.

아시아 및 아프리카의 정부-민간 연계 메가프로젝트 파이프라인

중국, 인도 및 아프리카 국가의 정부는 습도 변화, 사막의 모래에 의한 마모, 자외선 노출을 견뎌야 하는 국경을 넘는 파이프라인 및 터미널 네트워크에 공동 출자를 실시했습니다. 폴리실록산 코팅은 -40°C에서 120°C의 온도 사이클에서도 밀착성과 유연성을 유지하기 때문에 지상부의 재도장에 수반하는 가동 정지의 필요성을 줄입니다. 설계, 조달 및 건설(EPC) 컨소시엄은 ISO 12944 C4 또는 C5 준수를 광범위하게 의무화하고 있으며, 폴리실록산 하이브리드 코팅은 적은 적용 횟수로 이 기준을 달성합니다. 현지 시공업자는 속건성에 의한 작업 효율의 향상을 도모할 있습니다. 이는 매일 수킬로미터 단위로 시공 구간이 이동하는 선형 프로젝트에서 중요한 요소입니다. BASF와 오리엔탈 유홍사와의 제휴에서 알 수 있듯이 공급업체는 지역 파트너십을 심화시키고 세계 수지 기술과 현지 품질 기준을 충족하는 현장 교육을 융합시키고 있습니다. 동아프리카 및 아세안 지역 가스 파이프라인 회랑에서의 선행 일정은 보호 분야를 위한 폴리실록산 판매의 다년에 걸친 원동력을 시사합니다.

숙련 도장공의 부족이 현장 시공 비용을 밀어 올립니다.

미국의 NACE 인증 스프레이 작업자의 평균 시급은 2025년에 50달러를 돌파하였고 계절적인 유지보수 피크 시에는 시간외 할증 임금이 더욱 상승합니다. 독일과 네덜란드에서도 비슷한 인재 부족 현상이 현저하고, 노인 노동자의 퇴직이 신규 참가자를 웃돌고 있습니다. 폴리실록산 코팅은 정확한 혼합 비율과 이슬점 관리를 필요로 하므로 노동력 부족의 영향이 더욱 증폭됩니다. 선박수리공장에서는 인건비에서만 전년 대비 15%의 입찰가 상승이 보고되었으며, 일부 선주는 재도장 사이클을 연기해야 합니다. 제조업체는 현장에서의 취급을 경감하는 1액형이나 프리믹스 키트로 대응하고 있지만, 이러한 제품은 수지 비용이 높아지는 경향이 있습니다. 도료 공급자나 업계 단체 주도의 연수 프로그램에 의해 신규 시공자 인증을 목표로 하고 있지만, 인력의 보충에는 수년을 필요로 하기 때문에 단기적인 수요 증가는 둔화할 전망입니다.

부문 분석

폴리실록산 코팅 시장에서 에폭시 폴리실록산 하이브리드가 가장 큰 점유율을 차지했으며 2025년 수익 점유율은 38.86%였습니다. 그 우위성은 에폭시의 프라이머 레벨 밀착성과 실리콘의 자외선 안정성이 융합하여 발생하였으며, 이들을 조합한 2코트 구조에 의해 ISO 12944 C5-M 기준을 충족할 수 있습니다. 실제 해상 재킷 시험에서는 15년이 넘는 유지보수 기간이 확인되었으며 노동력 부족 상황에서 총 소유 비용 절감 효과가 높아집니다. 이 때문에 최종 사용자는 가격 프리미엄을 허용 가능하다고 인식하고 플랫폼 업그레이드 및 해군 함정 업그레이드에 있어서 장기 계약의 기반이 되고 있습니다.

아크릴계 폴리실록산 하이브리드는 시장 규모는 작지만, 뛰어난 색유지성과 저황변성에 의해 5.62%라는 가장 높은 CAGR을 나타내고 있습니다. 크루즈 선박, 건축물 외관, 교량 프로젝트에서 수요가 증가하고 있습니다. 캘리포니아 및 유럽 경제 지역(EEA)에서 엄격한 휘발성 유기 화합물(VOC) 규정은 광택을 손상시키지 않고 용매 방출량을 줄이는 수성 아크릴계 실록산 분산액으로의 사양 변경을 더욱 촉진하고 있습니다. 폴리에스테르 변성 등급은 산과 알칼리에 노출되는 화학 플랜트용으로 틈새 시장을 개척하고 있으며, 에스테르 결합을 활용하여 내약품성을 높이고 있습니다. 불소화 폴리실록산 블렌드와 세라믹 충전 유형은 각각 극한 온도 환경의 유닛이나 그래피티에 노출되기 쉬운 교통 구조물을 대상으로 하고 있으며, 수지 화학자가 멀티코트 도장을 대체하는 다기능성을 추구하는 광범위한 동향을 뒷받침하고 있습니다. 실온 경화형 무유화제 실리콘 바인더에 관한 최근의 연구에서는 가수분해 스트레스의 저감이 입증되어 차세대 제품에서는 제로 VOC 특성과 고기계적 강도의 양립이 기대됩니다.

지역별 분석

아시아태평양은 2025년 폴리실록산 코팅 시장의 54.88%를 차지하였고 2026년부터 2031년에 걸쳐 6.55%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 이는 중국의 타의 추종을 불허하는 조선 규모와 한국의 LNG선 건조에서의 우위성에 의해 지원되고 있습니다. 베이징에서의 국산 해군 함정의 추진과 해상 풍력 발전 용량 260GW를 목표로 하는 제14차 5개년 계획에 의해 국내 수요가 더욱 높아지고 있습니다. 일본에서는 화물 유출 방지를 위해 실리콘 함량이 높은 탑 코트를 지정하는 고사양 화학제품 탱커와 FSRU 프로젝트가 공헌하고 있습니다. 인도의 사가르말라 항만 정비 계획과 ASEAN 지역 내의 모듈식 조선소 증가로 인해 지역 고객 기반이 확대되고 있습니다.

북미는 멕시코만의 부체식 생산 설비 업그레이드, 캐나다의 오일 샌드 모듈화, 교량 및 공항 등 연방 인프라 업그레이드 프로젝트에 의해 두 번째로 높은 점유율을 차지합니다. 미국 환경보호청(EPA)이 산업용 유지관리 도료의 휘발성 유기 화합물(VOC) 함유량을 275g/L 이하로 제한하는 방침을 내세우면서 자산 소유자는 초고고형분 폴리실록산 코팅으로의 이행을 진행하고 있습니다. 지역 전력 회사는 실리콘 골격이 산성 응축 사이클을 견딜 수 있기 때문에 배연 탈황 덕트에 이러한 하이브리드 제품을 채택하고 있습니다. USMCA(미국, 멕시코, 캐나다 협정) 하의 자유 무역 물류에 의해 수지 및 안료의 국경을 넘은 공급이 효율화되고, 멕시코 해안 EPC 거점용 고고형분 폴리실록산 제품의 리드 타임이 단축되고 있습니다.

유럽은 보다 안정적인 성장을 보이면서도 전략적으로 중요한 시장으로 남아 있습니다. 북해의 해체 공사와 해상 풍력 발전소의 업그레이드 공사가 유지관리용 도료 수요를 만들어내는 한편, 북유럽의 조선소에서는 저온 경화형 폴리실록산 베이스 코팅을 필요로 하는 내빙급 보급선이 건조되고 있습니다. EU에서의 시클로실록산 규제의 시행이 다가오는 가운데, 적합성이 있는 수성 분산액으로의 조기 전환이 진행되어, 이 지역은 차세대 배합의 시험장으로서의 역할을 담당하고 있습니다. 독일의 아우토반 교량 업그레이드 프로그램은 25년간의 부식 성능을 요구하며 에폭시 폴리실록산 2코트 방식은 2코트로 이 목표를 달성할 수 있습니다. 이를 통해 도로 폐쇄일수를 줄일 수 있습니다. 중동, 아프리카 및 남미는 장기적인 수요 거점으로 부상하고 있습니다. 브라질의 프리솔트층용 FPSO 백로그와 UAE의 항만 확장 프로젝트에서는 고온 염분 환경 하에서의 검사 사이클 연장에 대응하기 위해 폴리실록산 기술이 도입될 전망입니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 부식성 환경하의 해양 및 셰일 자산에서의 석유 및 가스 설비 투자 증가

- 아시아 및 아프리카에서의 정부-민간 연계 메가프로젝트 파이프라인

- 용제계에서 초고고형분 하이브리드로의 이행

- 모듈식 풍력 타워 제조 야드의 급증

- LNG 운반선대의 급속한 확대

- 억제요인

- 숙련 도장공의 부족에 의한 현장 시공 비용 상승

- 환형 실록산 제품에 대한 규제 당국의 감시

- 고온 사이클 하에서의 엣지 결함

- 불소 수지 탑 코트로부터의 경쟁 위협

- 밸류체인 분석

- Porter's Five Forces

- 공급자의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체 제품 및 서비스의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 수지 유형별

- 에폭시 폴리실록산 하이브리드

- 아크릴 폴리실록산 하이브리드

- 폴리에스테르 변성 폴리실록산

- 기타 수지 유형

- 최종 사용자 산업별

- 보호

- 석유 및 가스

- 전력

- 인프라

- 해양

- 기타 최종 사용자 산업

- 보호

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 스페인

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 및 순위 분석

- 기업 프로파일

- Akzo Nobel NV

- Asian Paints Ltd.

- Hempel A/S

- Jotun

- KISHO Corporation Co.,Ltd

- Metcon Coatings & Chemicals India Private Limited.

- NCP Coatings LLC

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Thomas Industrial Coatings

- Tianjin Jinhai Special Coatings & Decoration Co., Ltd.

- Tikkurila

- Tnemec

- Yung Chi Paint & Varnish MFG. CO.,LTD

제7장 시장 기회 및 미래 전망

CSM 26.01.28The Polysiloxane Coatings Market is expected to grow from USD 0.93 billion in 2025 to USD 0.98 billion in 2026 and is forecast to reach USD 1.26 billion by 2031 at 5.21% CAGR over 2026-2031.

The rising specification of these silicone-organic hybrids in harsh marine and energy settings, along with elevated infrastructure spending in emerging economies and tightening global VOC regulations, collectively underpin demand momentum. Specification engineers view polysiloxane systems as an effective path to extend maintenance cycles, cut life-cycle cost, and comply with evolving health and safety norms, an alignment that reinforces premium pricing power. Major suppliers highlight two-coat epoxy-polysiloxane alternatives that replace three-coat zinc-rich epoxy-polyurethane schemes, thereby reducing labor needs at a time of skilled painter scarcity. Meanwhile, ultra-high-solid variations reduce solvent release without sacrificing edge coverage. Competitive emphasis has therefore shifted to resin innovation, acquisition-led portfolio shaping, and region-specific technical service programs that secure repeat orders.

Global Polysiloxane Coatings Market Trends and Insights

Growing Oil and Gas CAPEX in Corrosive Offshore and Shale Assets

Global upstream operators are channeling new capital toward deep-water and shale prospects that expose steel to high concentrations of chloride, CO2, and H2S. Polysiloxane technology provides the required C5 protection in two coats, reducing trimming time on floating production platforms where weather windows narrow each year. Asset owners also cite lower under-film blistering versus conventional epoxies, a benefit that delays costly touch-ups in splash zones. Recent qualified systems have exceeded 15,000 hours of salt-spray testing while maintaining gloss retention above 85% after 3,000 hours of QUV, reinforcing the technology's durability credentials. Offshore contractors, therefore, embed polysiloxane topcoats in standard maintenance specifications for jackets, decks, and flare towers as part of life-extension programs. Service providers emphasize that high film-build capability enables adequate edge protection with one cross-spray pass, easing productivity hurdles created by labor shortages in remote basins.

Public-Private Megaproject Pipelines in Asia and Africa

Governments in China, India, and several African nations are co-funding cross-country pipelines and terminal networks that must withstand humidity swings, desert sand abrasion, and ultraviolet exposure. Polysiloxane systems retain adhesion and flexibility across -40°C to +120°C cycles, reducing the need for shutdowns to recoat above-ground sections. Engineering, procurement, and construction (EPC) consortia largely mandate ISO 12944 C4 or C5 compliance, a threshold that polysiloxane hybrids reach with fewer coats. Local applicators gain speed benefits from faster touch-dry times, a critical factor on linear projects where kilometer-long spreads move daily. Suppliers deepen regional partnerships-exemplified by BASF and Oriental Yuhong-to blend global resin expertise with on-site training that meets local quality standards. Forward schedules for gas pipeline corridors in East Africa and ASEAN suggest a multi-year tailwind for polysiloxane sales into protective segments.

Skilled-Painter Scarcity Inflating Field-Applied Costs

Average hourly wages for NACE-certified sprayers in the United States exceeded USD 50 in 2025, and overtime premiums escalate further during seasonal maintenance peaks. Similar shortages are also evident in Germany and the Netherlands, as an aging workforce retires faster than newcomers enter. Polysiloxane systems require accurate mix ratios and dew-point control, amplifying the impact of labor gaps. Ship-repair yards report bid prices up 15% year-on-year on labor alone, pushing some owners to postpone repaint cycles. Manufacturers counter with single-component or pre-blended kits that reduce on-site handling, but these variants often carry a higher resin cost. Training initiatives led by coating suppliers and trade associations aim to certify new applicators; however, the pipeline will take years to refill, which will mute near-term volume growth.

Other drivers and restraints analyzed in the detailed report include:

- Transition from Solvent-Borne to Ultra-High-Solid Hybrids

- Rapid Expansion of LNG Carrier Fleet

- Regulatory Scrutiny on Cyclic Siloxane By-Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy-polysiloxane hybrids accounted for the largest share of the polysiloxane coatings market, with a revenue share of 38.86% in 2025. Their dominance stems from the union of epoxy's primer-level adhesion with silicone's UV stability, which together allow a two-layer build to meet ISO 12944 C5-M performance. Field studies on offshore jackets confirm maintenance intervals above 15 years, a result that amplifies total cost-of-ownership savings when labor is scarce. End-users thus perceive price premiums as acceptable, anchoring long-term contracts for platform upgrades and naval refits.

Acrylic-polysiloxane hybrids, although having a smaller base, boast the quickest 5.62% CAGR due to their superior color retention and low yellowing, which appeal to cruise vessels, architectural facades, and bridge girder projects. Strict VOC limits in California and the European Economic Area further steer specifiers toward water-based acrylic-siloxane dispersions that release fewer solvents without sacrificing gloss. Polyester-modified grades carve a niche in chemical plants exposed to acids and alkalis, leveraging ester linkages to boost chemical resistance. Fluorinated polysiloxane blends and ceramic-filled variants target extreme-temperature units and graffiti-prone transit structures, respectively, underscoring a broader trend: resin chemists seek multi-attribute performance to replace multi-coat stacks. Recent lab work on room-temperature-curing emulsifier-free silicone binders reduces hydrolytic stress, suggesting next-generation offerings will merge zero-VOC status with higher mechanical strength.

The Polysiloxane Coatings Market Report is Segmented by Resin Type (Epoxy-Polysiloxane Hybrids, Acrylic-Polysiloxane Hybrids, Polyester-Modified Polysiloxane, and Other Resin Types), End-User Industry (Protective, Marine, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured a 54.88% share of the polysiloxane coatings market in 2025 and is set to log a 6.55% CAGR from 2026-2031, anchored by China's unrivaled shipbuilding scale and South Korea's dominance in LNG vessel construction. Beijing's push for locally built naval ships and the country's 14th Five-Year Plan, which targets 260 GW of offshore wind capacity, intensifies domestic demand for these products. Japan contributes through high-spec chemical carriers and FSRU projects that specify silicone-rich topcoats to resist cargo spillage. India's Sagarmala port upgrade and the growth of modular fabrication yards across ASEAN widen the regional customer pool.

North America holds the second-largest share, driven by the Gulf of Mexico's floating production unit refurbishment, the modularization of Canadian oil sands, and federal infrastructure renewal projects across bridges and airports. The US EPA's aim to clamp VOCs below 275 g/L in industrial maintenance coatings steers asset owners toward ultra-high-solid polysiloxane systems. Regional power-utilities adopt these hybrids for flue-gas desulfurization ducting because silicone backbones withstand acidic condensation cycles. Free-trade logistics under USMCA streamline cross-border resin and pigment supply, lowering lead times for high-build polysiloxane shipments into Mexican offshore EPC hubs.

Europe shows steadier growth yet stays strategically important. North Sea decommissioning and wind-farm repowering generate maintenance coatings work, while Nordic yards fabricate ice-class supply vessels requiring low-temperature cure polysiloxane primers. The upcoming EU cyclic-siloxane restriction drives early conversion to compliant water-based dispersions, making the region a test bed for next-generation formulations. Germany's autobahn bridge renewal program specifies 25-year anti-corrosion performance, a target that epoxy-polysiloxane duplex systems can meet in two layers, thereby curbing lane-closure days. Middle East & Africa and South America emerge as long-term demand centers. Brazil's pre-salt FPSO backlog and UAE's port expansions are likely to adopt polysiloxane technology to meet extended inspection cycles in hot saline environments.

- Akzo Nobel N.V.

- Asian Paints Ltd.

- Hempel A/S

- Jotun

- KISHO Corporation Co.,Ltd

- Metcon Coatings & Chemicals India Private Limited.

- NCP Coatings LLC

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Thomas Industrial Coatings

- Tianjin Jinhai Special Coatings & Decoration Co., Ltd.

- Tikkurila

- Tnemec

- Yung Chi Paint & Varnish MFG. CO.,LTD

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing oil and gas CAPEX in corrosive offshore and shale asset

- 4.2.2 Public-private megaproject pipelines in Asia and Africa

- 4.2.3 Transition from solvent-borne to ultra-high-solid hybrids

- 4.2.4 Surge of modular wind-tower fabrication yards

- 4.2.5 Rapid expansion of LNG carrier fleet

- 4.3 Market Restraints

- 4.3.1 Skilled-painter scarcity inflating field-applied costs

- 4.3.2 Regulatory scrutiny on cyclic siloxane by-products

- 4.3.3 Edge-defect failures under high-temperature cycling

- 4.3.4 Competitive threat from fluoropolymer top-coats

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products & Services

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy-Polysiloxane Hybrids

- 5.1.2 Acrylic-Polysiloxane Hybrids

- 5.1.3 Polyester-Modified Polysiloxane

- 5.1.4 Other Resin Types

- 5.2 By End-user Industry

- 5.2.1 Protective

- 5.2.1.1 Oil and Gas

- 5.2.1.2 Power

- 5.2.1.3 Infrastructure

- 5.2.2 Marine

- 5.2.3 Other End-user Industries

- 5.2.1 Protective

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Asian Paints Ltd.

- 6.4.3 Hempel A/S

- 6.4.4 Jotun

- 6.4.5 KISHO Corporation Co.,Ltd

- 6.4.6 Metcon Coatings & Chemicals India Private Limited.

- 6.4.7 NCP Coatings LLC

- 6.4.8 PPG Industries, Inc.

- 6.4.9 The Sherwin-Williams Company

- 6.4.10 Thomas Industrial Coatings

- 6.4.11 Tianjin Jinhai Special Coatings & Decoration Co., Ltd.

- 6.4.12 Tikkurila

- 6.4.13 Tnemec

- 6.4.14 Yung Chi Paint & Varnish MFG. CO.,LTD

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-need Assessment