|

시장보고서

상품코드

1906077

이형제 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Release Agents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

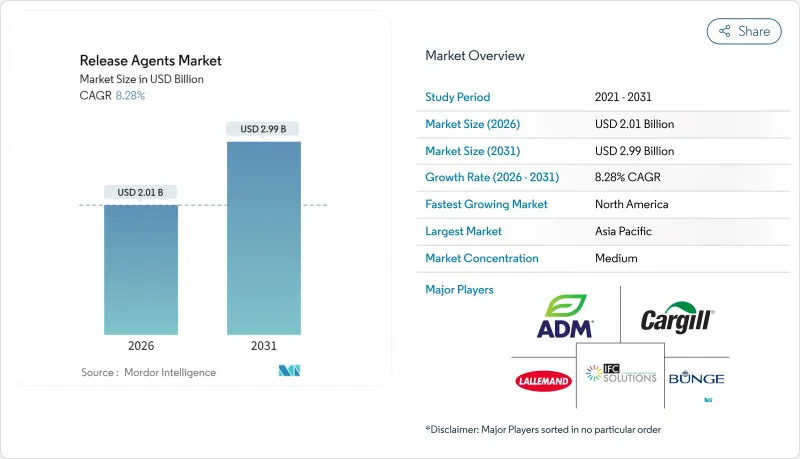

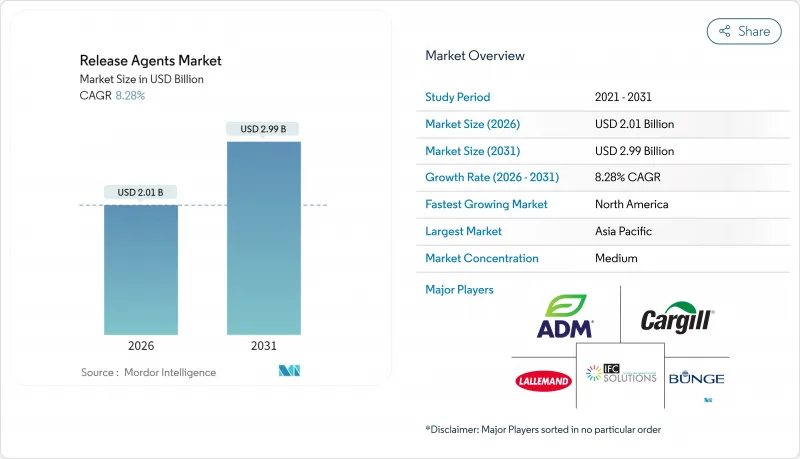

이형제 시장은 2025년에 18억 6,000만 달러로 평가되었고, 2026년 20억 1,000만 달러에서 2031년까지 29억 9,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 8.28%로 예상됩니다.

이러한 성장은 엄격한 식품 접촉 규제와 자동화 생산 요구사항 간의 균형을 맞추기 위한 제조업체의 노력을 반영합니다. NSF-H1 및 EU 1935/2004에 따른 배합제의 사용 증가와 저VOC 수성 스프레이 시스템의 도입은 베이커리, 육류 가공 공장, 과자 제조 라인, 냉동 디저트 시설에서의 첨단 이형제의 중요성을 돋보이게 합니다. 시장 확대는 신흥 경제국 중에서도 특히 아시아태평양의 인프라 투자에 의해 뒷받침됩니다. 이 지역에서는 유제품, 육류 및 편의점 사업의 성장이 특수 이형 기술에 관한 현지 전문 지식을 능가합니다. 각 회사는 지속가능성 목표와 소비자의 투명성 요구를 충족시키면서 효과적인 비점착 특성을 유지하기 위해 PFAS 프리 배합, 생분해성 왁스 에스테르, 식물성 오일에 주력하고 있습니다. 또한, 변동하는 상품 가격과 지역별 전환 테스트 요구사항이 공급업체의 통합을 촉진하고 있으며, 규제 준수와 신뢰할 수 있는 세계 공급망의 중요성이 강조되고 있습니다.

세계의 이형제 시장의 동향 및 인사이트

확대하는 식품 가공산업

세계 식품 가공산업의 확대는 베이커리제품, 과자, 유제품, 가공육제품의 생산 증가를 통해 이형제 시장의 성장을 견인하고 있습니다. 이형제는 대량 생산 공정에서 제품 품질 유지, 폐기물 최소화, 생산 라인 효율 확보에 필수적입니다. 영국의 빵 및 베이커리 제조 부문은 이러한 동향을 나타내며 기업 수에 있어서 식품 산업 최대의 하위 부문을 차지하고 있습니다. 영국국가통계국(ONS)의 보고에 의하면, 이 하위 부문에는 약 2,910개사가 있으며, 베이커리 관련 이형제에 대한 수요가 매우 높음을 나타내고 있습니다. 이 동향은 유럽, 북미, 아시아태평양에도 확산되고 있으며, 산업 식품 제조의 성장이 이형제 기술에 대한 수요를 뒷받침하고 있습니다. 업계의 성장과 포장 식품 또는 조리 식품에 대한 소비자 수요의 고조가 더하여 선진적인 이형제 배합의 도입이 진행되고 있습니다. 제조업체는 자동화 생산 시스템, 클린 라벨 요구사항 및 세계 가공업자에게 요구되는 지속가능성 기준을 충족하는 솔루션을 개발하고 있습니다.

비경화 식물성 기름의 선호

세계의 이형제 시장은 소비자의 건강 의식 증가와 규제 요건의 영향으로 비경화 식물성 기름의 도입 증가에 따라 변화하고 있습니다. 기존 경화유는 안정성과 기능성으로 이형제 배합에 널리 사용되었으나, 트랜스지방산이 심혈관질환, 비만, 대사장애 등 건강문제와 관련이 있다는 조사결과로 인해 세계적으로 규제 강화와 제품 재설계가 진행되고 있습니다. 캐나다 보건부가 부분경화유(PHO)의 대안으로 식물성 디아실글리세롤 오일을 승인한 사례는 새로운 지질 기술에 대한 규제 당국의 지지를 보여줍니다. 이 승인은 업계 전반에 걸쳐 대체 솔루션의 채택을 확대할 수 있습니다. 현재 제빵 및 제과, 가공육 업계의 식품 제조업체는 이형제 제품에 카놀라유, 해바라기유, 대두유, 유채유 등의 비경화 첨가유를 도입하고 있습니다. 이러한 대체품은 트랜스지방산과 관련된 건강 상의 우려 없이 클린 라벨화를 추진하면서 확실한 이형 효과와 장기 보존성 등 필수적인 기능 특성을 제공합니다.

원재료 가격의 변동성

상품 가격의 변동은 이익률에 대한 압박 요인이 되어, 배합의 복잡성과 비용 경쟁력의 양립을 위한 전략적 판단을 요구합니다. 노동통계국의 데이터에 따르면 식품가공용 원료비용은 2020-2024년 사이 23.6% 상승했습니다. 이러한 인플레이션 환경은 고품질의 원료를 필요로 하는 특수 이형제에 특히 큰 영향을 미치고 있으며, 가격 감응도가 높아 비용이 많이 드는 용도에서 시장 침투를 제한하고 있습니다. 공급망의 혼란은 변동의 영향을 강화하고 특정 원료 등급 및 공급원에 의존하는 이형제 제조업체에게 조달 상의 어려움을 가져오고 있습니다. 이러한 변동은 직접 재료비, 수송비, 에너지 투입량에 영향을 미치고, 헤지 능력이 없는 중소 공급업체에게 특히 심각한 복합 이익률 압박을 초래합니다. 선물 계약 전략은 가격 안정화와 장기적인 고객 관계 구축을 가능하게 하고 경쟁 우위를 제공하지만, 중소 경쟁사는 상품 가격의 급등 시 주기적인 이익률 축소에 노출됩니다.

부문 분석

2025년 시점에서 유화제는 시장 점유율의 38.05%를 차지하고 있었으며, 소수성 이형제와 물 기반 식품 시스템의 가교 역할로서 매우 중요한 역할을 담당하고 있음을 알 수 있습니다. 식품 가공에서의 광범위한 이용과 특히 모노글리세라이드, 디글리세라이드, 폴리글리세롤 에스테르, 레시틴 등의 배합은 다양한 제조 조건 하에서도 안정적인 효과를 보장합니다. 이러한 유화제는 제품의 안정성 유지, 식감 개선, 가공 식품의 종합적인 품질 향상에 필수적이며 업계에서 필수적인 존재입니다. 또한 다양한 가공 환경에 대한 적응성과 서로 다른 제조 조건에 대한 내성이 시장에서의 우위성을 더욱 확고하게 하고 있습니다.

왁스 및 왁스 에스테르는 2031년까지 8.84%라는 놀라운 CAGR을 나타낼 전망이며 따라서 주목할 만한 조성 부문입니다. 이 급성장은 주로 생분해성 배합과 PFAS 프리 대체품에서의 혁신에 의해 추진되고 있으며, 환경규제에의 적합성과 효과 간의 밸런스를 실현하고 있습니다. 지속가능성에 대한 관심 증가와 환경친화적인 솔루션에 대한 수요는 이러한 조성의 채택을 더욱 가속화하고 있습니다. 한편, 식물성 기름은 지속적인 수요를 누리고 있으며, 비경화 첨가 옵션에 대한 규제 당국의 권고가 이를 뒷받침하고 있습니다. 이는 더 건강하고 자연적인 성분을 요구하는 소비자의 선호도 증가와 일치합니다. 항산화제는 지질 기반 이형 시스템에서 보존 기간의 연장과 산패의 억제에 중요한 역할을 하며, 제품의 품질 유지 및 다양한 용도에서의 사용 기간 연장을 보장합니다. 또한, 항산화제를 이러한 시스템에 통합하면 제품의 수명을 연장할 뿐만 아니라 진화하는 소비자 및 업계의 기준을 충족하는 고품질의 안정적인 제형을 개발할 수 있습니다.

지역별 분석

2025년 북미는 시장 점유율의 34.10%를 차지하였습니다. 이는 첨단 식품가공 인프라와 최고 수준의 이형제 제형을 요구하는 엄격한 규제에 뒷받침된 결과입니다. 수년간 산업 식품 가공의 진보로 이 지역은 견고한 공급망과 깊은 전문 기술 지식을 보유하고 이형제 효과 기준의 일관된 적용을 보장하고 있습니다. 식품의 안전성과 품질을 중시하는 이 지역의 규제환경은 첨단 이형제의 도입을 더욱 촉진하고, 북미를 시장의 주도적 지역으로 자리매김하고 있습니다. 반면 아시아태평양은 성장 궤도에 있으며 2031년까지 연평균 복합 성장률(CAGR) 9.10%를 나타낼 전망입니다. 이 급성장은 주로 식품 가공에서의 산업화의 진전과 규제 기준의 변화에 의한 것으로, 모두 특수 이형제에 대한 수요를 확대시키고 있습니다. 이 지역에서 확대되는 중산층 인구와 가공 및 포장 식품에 대한 소비자 수요 증가도 효율적인 이형제 솔루션의 필요성 증가에 기여하고 있습니다.

유럽은 시장에서의 존재감이 크고 EU 규칙 1935/2004에 의해 규제되고 있습니다. 이 규제는 식품 접촉 재료에 대한 구체적인 요구사항을 규정하고 이형제의 선택에 영향을 미칩니다. 유럽의 환경보호 노력은 생분해성 및 식물 유래 이형제의 보급을 촉진하고 있습니다. 견고한 규제 프레임워크와 지속가능성에 초점을 맞춘 유럽은 이형제 제형에서 지속적인 혁신을 이끌어내는 중요한 시장으로 두드러지고 있습니다. 게다가 이 지역의 연구개발에 대한 강한 주력은 규제 요건과 소비자 요구에 부합하는 선진적인 솔루션의 창출을 촉진하여 세계 시장에서의 지위를 더욱 확고히 하고 있습니다.

식품가공의 산업화가 진전하는 가운데 남미, 중동, 아프리카는 유망한 시장으로 대두하고 있습니다. 그러나 시장 발전의 속도는 규제 프레임워크의 차이와 가공 인프라의 성숙도에 따라 불균일합니다. 이 지역에서는 식품 가공용 이형제의 도입이 현저하게 증가하고 있지만, 그 성장 속도는 각국의 산업 성숙도나 규제 상황에 크게 좌우되고 있습니다. 남미에서는 식품 가공시설의 근대화와 식품 안전기준의 향상에 대한 관심 증가가 수요를 견인하고 있습니다. 마찬가지로 중동 및 아프리카에서도 식품 가공산업에 대한 투자 증가와 규제 프레임워크의 단계적인 정비가 시장 확대의 기회를 창출하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 확대하는 식품 가공산업

- 비경화 식물성 기름의 선호도 증가

- NSF-H1 및 EU 1935/2004에 따른 식품 안전 추진

- 이형제 배합의 기술적 진보

- 비용 효율이 뛰어난 식물 유래 배합이 규제를 뒷받침

- 산업용 베이커리에서 용제의 VOC 저감을 실현하는 물 기반 분무 기술

- 억제요인

- 원재료 가격의 변동성

- 신흥 육류 가공 클러스터에서의 최종 사용자의 인지도 부족

- 엄격한 규제 기준

- 알레르겐 및 '프리 프롬' 제품의 제한

- 공급망 분석

- 규제와 기술 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁의 심각성

제5장 시장 규모 및 성장 예측

- 성분별

- 유화제

- 항산화제

- 식물성 기름

- 왁스 및 왁스 에스테르

- 기타

- 형태별

- 액체

- 고체

- 용도별

- 베이커리 및 과자

- 육류 및 육류 제품

- 유제품 및 냉동 디저트

- 기타 용도

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 스페인

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 가장 활발한 기업

- 시장 포지셔닝 분석

- 기업 프로파일

- Archer Daniels Midland(ADM)

- Cargill Inc.

- AAK AB

- Palsgaard A/S

- Dow Inc.

- IFC Solutions

- Lallemand Inc.

- Bunge Ltd.

- Masterol Foods Pty Ltd.

- Mallet & Company

- The Bakels Group

- Bundy Baking Solutions

- Avatar Corporation

- Chem-Trend(Lubrizol)

- Kerry Group plc

- PPG Silicones

- Henkel AG

- JAX Inc.

- ROCOL(ITW)

- Vegalene(R)/PLZ Corp.

제7장 시장 기회 및 미래 전망

CSM 26.01.21The release agents market was valued at USD 1.86 billion in 2025 and estimated to grow from USD 2.01 billion in 2026 to reach USD 2.99 billion by 2031, at a CAGR of 8.28% during the forecast period (2026-2031).

This growth reflects manufacturers' efforts to balance strict food-contact regulations with automated production requirements. The increased use of NSF-H1 and EU 1935/2004-compliant formulations, combined with the implementation of low-VOC water-based spray systems, highlights the importance of advanced release agents in bakeries, meat processing plants, confectionery production lines, and frozen-dessert facilities. The market expansion is supported by infrastructure investments in emerging economies, particularly in Asia-Pacific region, where the growth of dairy, meat, and convenience food operations exceeds local expertise in specialized release technologies. Companies are focusing on PFAS-free formulations, biodegradable wax esters, and plant-based oils to meet sustainability goals and consumer transparency demands while maintaining effective anti-stick properties. Additionally, fluctuating commodity prices and regional migration testing requirements are driving supplier consolidation, emphasizing the importance of regulatory compliance and reliable global supply chains.

Global Release Agents Market Trends and Insights

Expanding food processing industry

The global food processing industry's expansion drives the release agents market growth through increased production of bakery, confectionery, dairy, and processed meat products. Release agents are essential for maintaining product quality, minimizing waste, and ensuring production line efficiency in high-volume processing operations. The United Kingdom's bread and bakery manufacturing sector exemplifies this trend, representing the food industry's largest subsector by number of companies. The Office for National Statistics (UK) reports approximately 2,910 enterprises operating in this subsector, demonstrating substantial bakery-related demand for release agents. This pattern extends across Europe, North America, and Asia-Pacific, where industrial food manufacturing growth sustains the demand for release technologies. The combination of industry growth and increasing consumer demand for packaged and ready-to-eat foods drives the adoption of advanced release agent formulations. Manufacturers are developing solutions that align with automated production systems, clean-label requirements, and sustainability standards required by global processors.

Preference for non-hydrogenated vegetable oils

The global release agents market is transforming due to the increasing adoption of non-hydrogenated vegetable oils, influenced by growing consumer health consciousness and regulatory requirements. While hydrogenated oils were previously common in release agent formulations due to their stability and functionality, research linking trans fats to health issues such as cardiovascular disease, obesity, and metabolic disorders has led to global regulatory restrictions and product reformulations. Health Canada's endorsement of vegetable diacylglycerol oil as an alternative to partially hydrogenated oils (PHOs) demonstrates regulatory support for new lipid technologies. This approval may increase the adoption of alternative solutions across the industry. Food manufacturers in the bakery, confectionery, and processed meat industries are now implementing non-hydrogenated oils, including canola, sunflower, soybean, and rapeseed oils, in their release agent products. These alternatives provide essential functional properties such as reliable release performance and longer shelf life while supporting clean-label initiatives without the health concerns linked to trans fats.

Raw-material price volatility

Commodity price fluctuations create margin pressure, forcing strategic decisions between formulation complexity and cost competitiveness. Food processing ingredient costs increased by 23.6% between 2020-2024, according to Bureau of Labor Statistics data. The inflationary environment significantly affects specialty release agents that require premium raw materials, as price sensitivity restricts their market penetration in cost-conscious applications. Supply chain disruptions intensify volatility effects, creating procurement challenges for release agent manufacturers who depend on specific raw material grades or sources. The volatility impacts direct material costs, transportation, and energy inputs, creating compound margin pressure that particularly affects smaller suppliers without hedging capabilities. Forward contracting strategies provide competitive advantages by enabling price stability and supporting long-term customer relationships, while smaller competitors experience periodic margin compression during commodity price spikes.

Other drivers and restraints analyzed in the detailed report include:

- Food safety push for NSF-H1 and EU 1935/2004-compliant release agents

- Technological advancements in release agent formulations

- Stringent regulatory standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, emulsifiers command a 38.05% share of the market, underscoring their pivotal role in bridging the gap between hydrophobic release agents and water-based food systems. Their widespread use in food processing, particularly with formulations like mono- and diglycerides, polyglycerol esters, and lecithin, ensures consistent results across diverse manufacturing conditions. These emulsifiers are critical in maintaining product stability, improving texture, and enhancing the overall quality of processed foods, making them indispensable in the industry. Additionally, their ability to adapt to various processing environments and withstand different manufacturing conditions further solidifies their dominance in the market.

Wax and wax esters are the composition segment to watch, boasting an impressive 8.84% CAGR through 2031. This surge is largely fueled by innovations in biodegradable formulations and PFAS-free alternatives, striking a balance between environmental compliance and performance. The growing emphasis on sustainability and the need for eco-friendly solutions have further accelerated the adoption of these compositions. Meanwhile, vegetable oils enjoy sustained demand, bolstered by regulatory endorsements for non-hydrogenated options, which align with the increasing consumer preference for healthier and more natural ingredients. Antioxidants play a crucial role, enhancing shelf life and curbing rancidity in lipid-based release systems, thereby ensuring product integrity and extending usability in various applications. Furthermore, the integration of antioxidants into these systems not only improves product longevity but also supports the development of high-quality, stable formulations that meet evolving consumer and industry standards.

The Release Agents Market Report Segments the Industry by Composition (Emulsifiers, Antioxidants, Vegetable Oils, Wax and Wax Esters, Others), by Form (Liquid, Solid), by Application (Bakery and Confectionery, Meat and Meat Products, More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, North America commands a 34.10% share of the market, bolstered by its sophisticated food processing infrastructure and stringent regulations that demand top-tier release agent formulations. Years of advancement in industrial food processing have equipped the region with robust supply chains and deep technical expertise, ensuring the consistent application of release agent performance standards. The region's regulatory environment, which emphasizes food safety and quality, further drives the adoption of advanced release agents, making North America a dominant player in the market. Meanwhile, the Asia-Pacific region is on a growth trajectory, boasting a 9.10% CAGR through 2031. This surge is largely due to heightened industrialization in food processing and shifting regulatory standards, both of which amplify the demand for specialized release agents. The region's expanding middle-class population and increasing consumer demand for processed and packaged foods also contribute to the growing need for efficient release agent solutions.

Europe, with its significant market presence, is guided by EU Regulation 1935/2004. This regulation delineates specific requirements for food contact materials, influencing the selection of release agents. Europe's dedication to environmental stewardship has spurred the rise of biodegradable and plant-based release agents. Coupled with a robust regulatory framework and a sustainability focus, Europe stands out as a pivotal market, driving continuous innovation in release agent formulations. Additionally, the region's strong emphasis on research and development fosters the creation of advanced solutions that align with both regulatory and consumer demands, further solidifying its position in the global market.

As food processing industrialization gains momentum, South America and the Middle East, and Africa emerge as promising markets. Yet, the pace of market development is uneven, shaped by the nuances of regulatory frameworks and the maturity of processing infrastructure. While there's a noticeable uptick in the adoption of release agents for food processing in these regions, the speed of this growth is heavily influenced by each country's industrial maturity and regulatory landscape. In South America, the growing focus on modernizing food processing facilities and improving food safety standards is driving demand. Similarly, in the Middle East and Africa, increasing investments in food processing industries and the gradual establishment of regulatory frameworks are creating opportunities for market expansion.

- Archer Daniels Midland (ADM)

- Cargill Inc.

- AAK AB

- Palsgaard A/S

- Dow Inc.

- IFC Solutions

- Lallemand Inc.

- Bunge Ltd.

- Masterol Foods Pty Ltd.

- Mallet & Company

- The Bakels Group

- Bundy Baking Solutions

- Avatar Corporation

- Chem-Trend (Lubrizol)

- Kerry Group plc

- PPG Silicones

- Henkel AG

- JAX Inc.

- ROCOL (ITW)

- Vegalene(R) / PLZ Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and market definition

- 1.2 Scope of the study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding food processing industry

- 4.2.2 Preference for non-hydrogenated vegetable oils

- 4.2.3 Food safety push for NSF-H1 and EU 1935/2004-compliant release agents

- 4.2.4 Technological advancements in release agent formulations

- 4.2.5 Cost-effective plant-based formulations are gaining regulatory tailwinds

- 4.2.6 Water-based spray technologies cutting solvent VOCs in industrial bakeries

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility

- 4.3.2 Low end-user awareness in emerging meat-processing clusters

- 4.3.3 Stringent Regulatory Standards

- 4.3.4 Allergen and "free-from" limitations

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porters Five Force Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry Source

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Composition

- 5.1.1 Emulsifiers

- 5.1.2 Antioxidants

- 5.1.3 Vegetable Oils

- 5.1.4 Wax and Wax Esters

- 5.1.5 Others

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Solid

- 5.3 By Application

- 5.3.1 Bakery and Confectionery

- 5.3.2 Meat and Meat Products

- 5.3.3 Dairy and Frozen Desserts

- 5.3.4 Other Applications

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Active Companies

- 6.2 Market Positioning Analysis

- 6.3 Company Profiles

- 6.3.1 Archer Daniels Midland (ADM)

- 6.3.2 Cargill Inc.

- 6.3.3 AAK AB

- 6.3.4 Palsgaard A/S

- 6.3.5 Dow Inc.

- 6.3.6 IFC Solutions

- 6.3.7 Lallemand Inc.

- 6.3.8 Bunge Ltd.

- 6.3.9 Masterol Foods Pty Ltd.

- 6.3.10 Mallet & Company

- 6.3.11 The Bakels Group

- 6.3.12 Bundy Baking Solutions

- 6.3.13 Avatar Corporation

- 6.3.14 Chem-Trend (Lubrizol)

- 6.3.15 Kerry Group plc

- 6.3.16 PPG Silicones

- 6.3.17 Henkel AG

- 6.3.18 JAX Inc.

- 6.3.19 ROCOL (ITW)

- 6.3.20 Vegalene(R) / PLZ Corp.