|

시장보고서

상품코드

1906081

중동 및 아프리카의 건설기계 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Middle East And Africa Construction Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

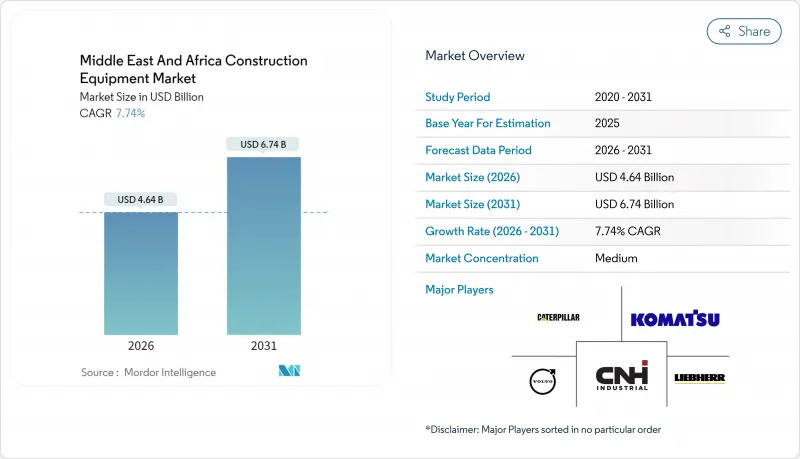

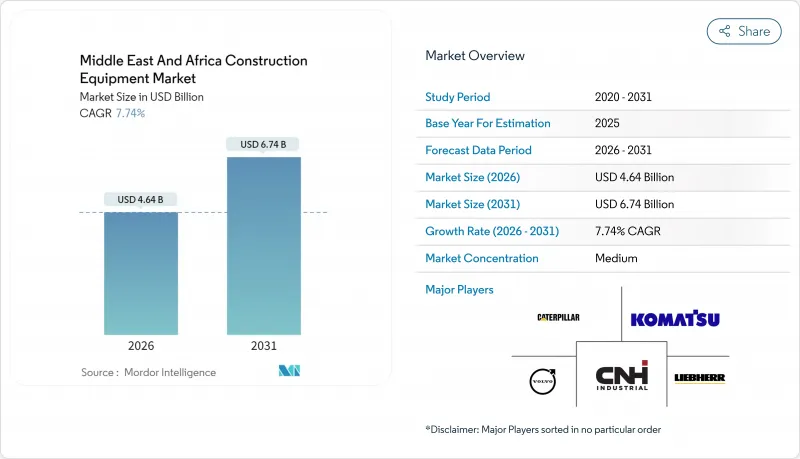

2026년 중동 및 아프리카의 건설기계 시장의 규모는 46억 4,000만 달러로 추정되고 있으며, 2025년 43억 1,000만 달러에서 성장하여, 2031년 67억 4,000만 달러에 이르고, 2026년부터 2031년까지는 CAGR 7.74%로 성장할 것으로 추정됩니다.

건설기계 시장은 걸프협력회의(GCC) 국가 전역에서 역대 최고인 2조 달러 규모의 인프라 정비 계획이 진행되고 있으며, 이 지역의 성장률은 세계 평균을 크게 웃돌고 있습니다. 사우디아라비아는 '비전 2030' 메가프로젝트를 통해 지출을 추진하고, 카타르는 월드컵 이후 투자로 기세를 유지하여 '내셔널 비전 2030'의 다양화 프로그램을 계속 실시했습니다. 견조한 계약자의 수주 잔여, 디지털에 의한 플릿 최적화로의 명확한 전환, 배터리용 광물의 채굴 활동 확대가 더하여 수요의 회복력을 강화하고 있습니다. 한편, 계약자는 신뢰성과 새로운 지속가능성 요구사항 간의 균형을 고려하고 있기 때문에 하이브리드 및 완전 전기기계의 채택이 가속화되었음에도 불구하고 디젤 구동 플릿이 우위를 유지하고 있습니다.

중동 및 아프리카의 건설기계 시장의 동향 및 분석

GCC 메가프로젝트 계획이 설비 수요 가속화

사우디아라비아의 비전 2030 계획은 인프라 정비에 1조 달러를 할당하고 있으며, 이는 타워 크레인이 필요한 NEOM 개발 프로젝트도 포함합니다. 이에 따라 볼프크란사와 자밀 그룹은 중동 최초의 타워 크레인 제조 시설을 설립했습니다. 아랍에미리트(UAE)에서는 6,500억 달러를 넘는 진행 또는 수주 프로젝트가 기세를 뒷받침하며, 카타르에서는 250억 달러의 국가 철도 계획이 건설 작업을 유지하고 있습니다. NEOM이 삼성 C&T와 체결한 13억 사우디아라비아 리얄 규모의 로봇 계약과 같은 합작사업은 철근 수작업을 80% 줄이는 한편, 자동화 설비 수요를 더욱 높이고 있습니다. 장기적인 전망과 정부 자금으로 인해 건설기계 시장은 세계 경기 감속의 영향을 받기 어려우며 OEM 제조업체와 딜러의 주문은 안정적입니다.

지역 전체적으로 소유에서 렌탈 모델로 전환

건설업자는 2020년 이후 20% 상승한 설비 구입 가격에 대처하기 위해 렌탈 모델로 전환을 진행하고 있습니다. 유나이티드 렌탈사는 중동 고객이 텔레매틱스 서비스 운영자 교육을 포함한 단기 계약을 확대함으로써 2024년 수익 증가를 보고했습니다. 허크 렌탈사도 같은 종합적 서비스로 2025년 지역 성장을 달성했습니다. 사우디아라비아의 렌탈 시장은 고금리 환경 하에서의 현금 흐름 최적화를 배경으로 두 자릿대의 CAGR로 성장을 지속하고 있습니다. 이 모델은 설비 가동률의 향상에 기여하고 거액의 초기 투자 없이 차세대 전기식 굴착기에 대한 접근을 가능하게 하여 건설기계 시장을 주도하는 지속가능성 목표와 부합하고 있습니다.

원유 가격의 변동성은 자본 투자 판단을 앞당깁니다.

원유 가격의 급등으로 계약자들은 코스트 플러스 방식의 재협상과 자금조달 제약을 예상하고 따라서 임의의 플릿 예산을 축소시킵니다. 해양 부문은 2020년에 설비투자를 대폭 삭감하여 특수 크레인과 파이프 레이어가 필요한 플랫폼 확장을 연기했습니다. 나이지리아는 그 영향의 크기를 나타내는 지역입니다. 브렌트 원유 가격이 상승하면 건축자재 비용이 급등하고 GDP 성장에도 불구하고 대출 계약과 신규 설비 주문의 축소를 초래합니다. 그러나 GCC 국가의 다양화된 경제는 조달 일정을 안정시키는 정부 보증의 유틸리티로 변동을 완화하고 건설기계 시장의 하향 위험을 억제하고 있습니다.

부문 분석

굴착기는 2025년 시점에서 중동 및 아프리카의 건설기계 시장의 35.75%를 차지하였으며, 공공 메가프로젝트, 광업, 주택 개발에서의 핵심적인 역할을 부각하고 있습니다. 굴착기와 관련된 건설기계 시장의 규모는 카타르의 국가철도계획에서의 대규모 굴착 수요와 이집트 시멘트 공장에서의 석회암 표토 제거 수요에 따라 2031년까지 연평균 복합 성장률(CAGR) 7.79%로 확대될 전망입니다. 자동 구배 제어 장치와 고소 해체 붐을 갖춘 굴착기는 작업 효율을 5분의 1 향상시켜 주요 건설 회사의 반복 주문을 촉진합니다.

수요는 또한 콩고 민주 공화국의 배터리 광물 채굴을 반영하고 있으며, 심광 코발트 광산은 강화 하부를 갖춘 90톤급 유닛이 필요합니다. 엄격한 건설 안전 기준으로 360도 카메라와 텔레매틱스를 탑재한 굴착기에 대한 선호가 높아지고 있어 가동률을 5분의 1 개선할 수 있게 되었습니다. 휠 로더와 크롤러 크레인과 같은 보완 카테고리는 골재 이송과 고층 리프트를 지원하지만, 성장 기세에서는 굴착기에 뒤처져 있습니다. 사우디아라비아에서는 모듈식 주택 공장 내에서 텔레스코픽 핸들러의 수요가 확대되고, 백호 로더는 복합 교통 도시 도로에서의 유틸리티용 굴착에 활용되고 있습니다.

2025년 중동 및 아프리카의 건설기계 시장에서는 디젤 및 내연기관(ICE) 모델이 72.63%를 차지하였으며 이는 사막지역과 아프리카의 오프그리드 현장에서 기존의 파워트레인에 대한 지속적인 의존을 뒷받침하고 있습니다. 고온 내성 엔진과 다단식 필터를 조합하여 50°C의 환경에서도 가동 시간을 확보합니다. 그러나 GCC(걸프협력회의)의 탈탄소화 정책에 의해 스코프 1 배출량 저감 목표가 추진되는 가운데 전기식 및 하이브리드식 기종은 CAGR 7.75%로 확대되고 있습니다.

캐터필러의 320 Electric 굴착기는 1회 충전으로 8시간의 가동을 실현하고 플릿 텔레매틱스 대시보드에 직접 연결할 수 있으므로 혼합 동력 플릿 내에서의 도입이 용이합니다. 두바이의 도시 지하철 터널 공사에서는 제로 에미션 장비의 지정이 증가하고 있으며, 광산 사업자도 지하에서의 환기 비용 절감을 활용하고 있습니다. 열에 의한 배터리의 열화나 충전 인프라의 부족이라는 과제가 도시 이외에서의 보급을 늦추고 있지만, 렌탈 기업은 이동식 충전기를 설비 서비스 패키지에 포함시켜 도입을 가속화하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- GCC 메가프로젝트의 파이프라인이 설비 수요를 가속화

- 지역 전반적인 소유 모델에서 렌탈 모델로의 이행

- 아프리카 전역의 급속한 도시 주택 건설 프로그램

- 현지 조달 규제가 OEM과 현지 합작의 조립 라인을 추진

- 원격 사막지역에서의 차량군 최적화를 위한 서비스형 텔레매틱스

- 배터리용 광물 채굴(리튬, 망간)에 필요한 대형 로더

- 억제요인

- 원유 가격의 순환성이 설비 투자 결정을 앞당김

- 정치 및 안보상의 핫스팟이 프로젝트 실행을 억제

- 항만의 혼잡에 의한 중요 예비 부품의 유통 지연

- 차세대 전기기계 기술자의 부족

- 가치 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측(금액, 달러)

- 기계 유형별

- 굴착기

- 휠 로더

- 크롤러 크레인

- 텔레스코픽 핸들러

- 백호 로더

- 스키드 스티어 로더 및 컴팩트 트랙 로더

- 모터 그레이더

- 불도저 및 도저

- 아스팔트 포장기 및 로드 롤러

- 굴절식 덤프 트럭

- 트렌처 및 기타

- 드라이브 유형별

- 디젤 및 내연기관

- 전기식 및 하이브리드식

- 유압식

- 출력별

- 100마력 이하

- 101-200 마력

- 201-400 마력

- 400마력 초과

- 용도별

- 인프라 및 수송

- 석유 및 가스

- 광업 및 채석업

- 상업 빌딩

- 주택

- 공업 및 제조

- 최종 사용자별

- 계약자

- 시설 렌탈 회사

- 정부 및 지자체

- 광업회사

- 국가별

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 오만

- 쿠웨이트

- 바레인

- 남아프리카

- 기타 중동 및 아프리카

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Caterpillar Inc.

- Komatsu Ltd.

- Volvo AB

- Hitachi Construction Machinery

- Liebherr Group

- CNH Industrial(Case CE)

- JCB Ltd.

- Doosan Corporation

- Kobelco Construction Machinery

- Tadano Ltd.

- Manitowoc Company Inc.

- Sumitomo Construction Machinery

- Mitsubishi Corporation

- XCMG

- SANY Heavy Industry

- Hyundai Genuine

- Deere & Company(Wirtgen)

- Bobcat Company

- Zoomlion Heavy Industry

- Terex Corporation

제7장 시장 기회 및 미래 전망

CSM 26.01.28The Middle East And Africa Construction Equipment Market size in 2026 is estimated at USD 4.64 billion, growing from 2025 value of USD 4.31 billion with 2031 projections showing USD 6.74 billion, growing at 7.74% CAGR over 2026-2031.

The construction equipment market benefits from an unprecedented USD 2 trillion infrastructure pipeline across the Gulf Cooperation Council (GCC), positioning regional growth far ahead of the global average. Saudi Arabia drives spending through Vision 2030 mega-projects, while Qatar sustains momentum with post-World-Cup investments and continues to implement National Vision 2030 diversification programs. Robust contractor backlogs, a clear pivot toward digital fleet optimization, and expanding mining activity for battery minerals collectively reinforce demand resilience. Meanwhile, the diesel-powered fleet maintains dominance despite accelerating adoption of hybrid and fully electric machines as contractors balance reliability with emerging sustainability requirements.

Middle East And Africa Construction Equipment Market Trends and Insights

GCC Mega-Projects Pipeline Accelerates Equipment Demand

Saudi Arabia's Vision 2030 agenda earmarks USD 1 trillion for infrastructure, including NEOM development that requires tower cranes, prompting Wolffkran and Zamil Group to establish the region's first tower-crane manufacturing facility. The UAE supports momentum with more than USD 650 billion in active or awarded projects, while Qatar's USD 25 billion National Rail Scheme sustains construction work. Joint ventures such as NEOM's SAR 1.3 billion robotics deal with Samsung C&T cut manual rebar labor by 80% yet intensify demand for automated equipment fleets. Long-term visibility and sovereign funding insulate the construction equipment market from global slowdowns, ensuring steady machine order books for OEMs and dealers.

Region-Wide Shift From Ownership To Rental Models

Contractors are pivoting toward rental to combat the two-fifth surge in equipment purchase prices since 2020. United Rentals reported a revenue uptick in 2024 as Middle East customers expand short-term contracts covering telematics, service, and operator training. Herc Rentals projects regional growth in 2025 on similar bundled offerings. Saudi Arabia's rental niche is tracking a double-digit CAGR, driven by cash-flow optimization during a high-interest environment. The model improves fleet utilization and opens access to next-generation electric excavators without large upfront capital, keeping the construction equipment market aligned with evolving sustainability targets.

Oil-Price Cyclicality Defers Capex Decisions

Sharp upward shifts in crude prices reduce discretionary fleet budgets because contractors anticipate cost-plus contract renegotiations and financing constraints. The offshore sector slashed in CAPEX in 2020, postponing platform expansions that otherwise require specialized cranes and pipelayers. Nigeria showcases the sensitivity: construction input costs spike when Brent exceeds tightening lending and dampening new equipment orders despite GDP growth. Nonetheless, diversified GCC economies cushion volatility via sovereign-backed public works that hold procurement schedules steady, limiting downside risk for the construction equipment market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Urban Housing Programmes Across Africa

- Local-Content Rules Driving Oem-Local Jv Assembly Lines

- Political & Security Hotspots Curb Project Execution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Excavators accounted for 35.75% of Middle East and Africa construction equipment market in 2025, underscoring their pivotal role across public mega-projects, mining, and housing developments. The construction equipment market size attached to excavators is on track to rise at a 7.79% CAGR through 2031 in response to heavy trenching needs on Qatar's National Rail Scheme and limestone overburden removal at Egyptian cement sites. Excavators equipped with grade-control automatics and high-reach demolition booms deliver one-fifth efficiency gains, prompting repeat orders from Tier 1 contractors.

Demand also reflects battery-mineral extraction in the DRC, where deep-pit cobalt mines require 90-ton units with reinforced undercarriages. Stringent construction safety codes boost preference for excavators with 360-degree cameras and telematics, enabling one-fifth utilization improvements. Complementary categories including wheel loaders and crawler cranes, support aggregate transfer and high-rise lifts yet trail excavators in growth momentum. Telescopic handlers grow within modular housing plants in Saudi Arabia, while backhoe loaders supply utility trenching across mixed-traffic urban roads.

Diesel and ICE models represented 72.63% of Middle East and Africa construction equipment market in 2025, validating continued reliance on conventional powertrains in desert and off-grid African sites. High thermal-tolerance engines paired with multi-stage filtration safeguard uptime against 50 °C ambient conditions. Nevertheless, the electric and hybrid cohort is advancing at a 7.75% CAGR as GCC decarbonization policies push clients toward lower Scope 1 emissions targets.

Caterpillar's 320 Electric excavator delivers an eight-hour shift on a single charge and slots directly into fleet telematics dashboards, simplifying adoption within mixed-power fleets. Urban metro tunneling in Dubai increasingly specifies zero-tailpipe machines, while mining operators exploit reduced ventilation costs underground. Persistent constraints-battery degradation under heat and limited charging infrastructure-slow penetration outside metropolitan hubs, yet rental firms accelerate exposure by bundling mobile chargers into equipment-as-a-service packages.

The Middle East and Africa Construction Equipment Market Report is Segmented by Machinery Type (Excavators, Wheel Loaders, and More), Drive Type (Diesel/ICE and More), Power Output (Less Than or Equal To 100 HP and More), Application (Infrastructure & Transport, Oil & Gas, and More), End-User (Contractors, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Caterpillar Inc.

- Komatsu Ltd.

- Volvo AB

- Hitachi Construction Machinery

- Liebherr Group

- CNH Industrial (Case CE)

- JCB Ltd.

- Doosan Corporation

- Kobelco Construction Machinery

- Tadano Ltd.

- Manitowoc Company Inc.

- Sumitomo Construction Machinery

- Mitsubishi Corporation

- XCMG

- SANY Heavy Industry

- Hyundai Genuine

- Deere & Company (Wirtgen)

- Bobcat Company

- Zoomlion Heavy Industry

- Terex Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 GCC Mega-Projects Pipeline Accelerates Equipment Demand

- 4.2.2 Region-Wide Shift From Ownership To Rental Models

- 4.2.3 Rapid Urban Housing Programmes Across Africa

- 4.2.4 Local-Content Rules Driving Oem-Local Jv Assembly Lines

- 4.2.5 Telematics-As-A-Service For Remote Desert Fleet Optimisation

- 4.2.6 Battery-Mineral Mining (Lithium, Manganese) Needs Heavy Loaders

- 4.3 Market Restraints

- 4.3.1 Oil-Price Cyclicality Defers Capex Decisions

- 4.3.2 Political & Security Hotspots Curb Project Execution

- 4.3.3 Port Congestion Delays Critical Spare-Parts Flow

- 4.3.4 Shortage Of Technicians For Next-Gen Electric Machines

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Machinery Type

- 5.1.1 Excavators

- 5.1.2 Wheel Loaders

- 5.1.3 Crawler Cranes

- 5.1.4 Telescopic Handlers

- 5.1.5 Backhoe Loaders

- 5.1.6 Skid-Steer & Compact Track Loaders

- 5.1.7 Motor Graders

- 5.1.8 Bulldozers & Dozers

- 5.1.9 Asphalt Pavers & Road Rollers

- 5.1.10 Articulated Dump Trucks

- 5.1.11 Trenchers & Misc.

- 5.2 By Drive Type

- 5.2.1 Diesel / ICE

- 5.2.2 Electric & Hybrid

- 5.2.3 Hydraulic

- 5.3 By Power Output

- 5.3.1 Less than or equal to 100 HP

- 5.3.2 101-200 HP

- 5.3.3 201-400 HP

- 5.3.4 More than 400 HP

- 5.4 By Application

- 5.4.1 Infrastructure & Transport

- 5.4.2 Oil & Gas

- 5.4.3 Mining & Quarrying

- 5.4.4 Commercial Buildings

- 5.4.5 Residential

- 5.4.6 Industrial / Manufacturing

- 5.5 By End-User

- 5.5.1 Contractors

- 5.5.2 Equipment Rental Companies

- 5.5.3 Government & Municipalities

- 5.5.4 Mining Firms

- 5.6 By Country

- 5.6.1 Saudi Arabia

- 5.6.2 United Arab Emirates

- 5.6.3 Qatar

- 5.6.4 Oman

- 5.6.5 Kuwait

- 5.6.6 Bahrain

- 5.6.7 South Africa

- 5.6.8 Rest of Middle East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Komatsu Ltd.

- 6.4.3 Volvo AB

- 6.4.4 Hitachi Construction Machinery

- 6.4.5 Liebherr Group

- 6.4.6 CNH Industrial (Case CE)

- 6.4.7 JCB Ltd.

- 6.4.8 Doosan Corporation

- 6.4.9 Kobelco Construction Machinery

- 6.4.10 Tadano Ltd.

- 6.4.11 Manitowoc Company Inc.

- 6.4.12 Sumitomo Construction Machinery

- 6.4.13 Mitsubishi Corporation

- 6.4.14 XCMG

- 6.4.15 SANY Heavy Industry

- 6.4.16 Hyundai Genuine

- 6.4.17 Deere & Company (Wirtgen)

- 6.4.18 Bobcat Company

- 6.4.19 Zoomlion Heavy Industry

- 6.4.20 Terex Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment