|

시장보고서

상품코드

1906097

치질 치료 기기 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Hemorrhoid Treatment Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

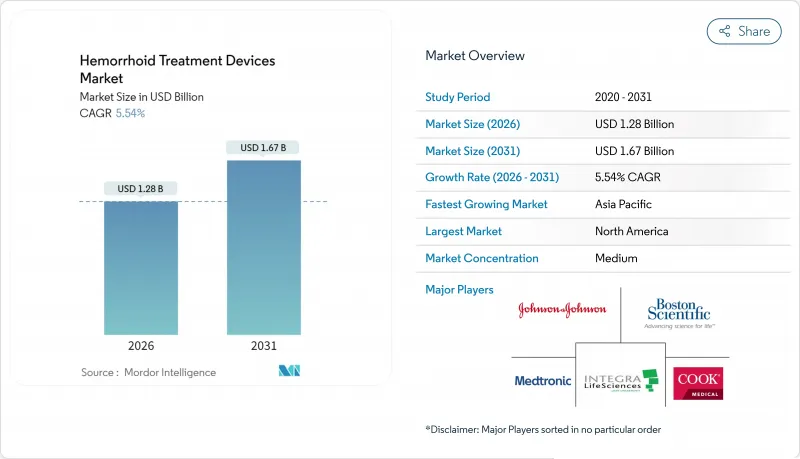

2026년 치질 치료 기기 시장 규모는 12억 8,000만 달러로 평가되었고, 2025년 12억 1,000만 달러에서 성장했으며, 2031년에는 16억 7,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 5.54%를 나타낼 전망입니다.

인구 고령화, 외래 진료로의 글로벌 전환, 회복 기간 단축 및 전체 치료 비용 절감을 가능케 하는 최소 침습 기술의 급속한 도입이 성장을 주도하고 있습니다. 인공지능(AI) 유도 내시경, 도플러 유도 결찰술, 레이저 치핵 성형술은 치료 옵션을 확대하여 의사가 조기에 개입하고 수술 후 통증을 줄이며 장기적 결과를 개선할 수 있게 합니다. 의료 보험사들이 외래 시술에 대한 보상을 확대함에 따라, 의료 제공자들은 안전성이나 효능을 저하시키지 않으면서도 표준화된 대량 치료를 더 낮은 비용으로 제공할 수 있는 외래 수술 센터를 우선적으로 활용하고 있습니다. 한편, 기존 제조사들은 감염 관리 정책 및 환경 지침에 부합하는 기술 차별화, 지속 가능성, 일회용 설계에 주력하고 있습니다.

세계의 치질 치료 기기 시장 동향 및 인사이트

증상을 동반한 치질의 유병률 상승

2024년 기준 약 1,000만 명의 미국인이 증상성 치핵으로 고통받았으며, 이는 성인 인구의 약 5%에 해당합니다. 50세 이후 발병률이 급격히 증가하여 인구 고령화에 따라 지속적인 환자 풀이 확보됩니다. 특히 첨단 치료가 용이한 도시 지역에서 좌식 업무 패턴, 고지방 식단, 증가하는 비만이 증상 심각도를 가중시킵니다. 신흥 경제국들도 고령화되고 유사한 생활 방식을 채택함에 따라, 해당 지역의 역학 곡선은 선진 시장과 유사한 추이를 보일 것으로 예상됩니다. 이러한 요소들이 종합적으로 작용하여 광범위하고 예측 가능한 수요 기반을 형성하며, 치질 치료 기기 시장의 지속적인 확장을 뒷받침합니다.

최소 침습적 외래 시술 선호도

환자와 보험사 모두 회복 기간을 단축하고 입원을 피할 수 있는 시술을 선호합니다. 메디케어는 주요 치질 결찰술 코드에 대해 보험 적용을 제공하여, 의료 제공자에게 외래 치료가 재정적으로 매력적인 선택이 되도록 합니다. 2024년 사례 연구에서 레이저 치핵 성형술 환자들은 4일차까지 통증이나 출혈이 없었으며, 이는 개방 수술 대비 빠른 회복을 보여줍니다. 전문 인력과 고효율 워크플로우를 결합한 외래 수술 센터가 점유율을 확대하고 있습니다. 이러한 추세들은 종합적으로 입원 환경에서 벗어나도록 가속화하며 첨단 기기에 대한 꾸준한 수요를 강화합니다.

개발도상국 시장의 제한된 보험 적용

많은 신흥 경제국에서 보험 예산은 전염병 및 모성 건강을 우선시하므로 치질 치료는 종종 자비 부담으로 이루어집니다. 도플러 유도 시스템이나 레이저 시스템의 높은 가격은 저소득층 환자에게 접근 불가능하게 하여, 부유한 도시 주민들은 첨단 치료를 받는 반면 농촌 인구는 보수적 관리에 의존하는 이중 시장 구조를 초래합니다. 이러한 격차는 전체 설치 기반 성장 둔화, 의료진 교육 도입 지연, 치질 치료 기기 시장의 장기 CAGR(연평균 성장률) 억제 요인으로 작용합니다.

부문 분석

고무 밴드 결찰기는 수십 년간의 임상적 친숙도, 낮은 단위 비용 및 최소한의 자본 요건을 반영하여 2025년 치질 치료 기기 시장 점유율의 41.98%를 차지하며 선두를 유지했습니다. 그러나 도플러 유도 결찰 시스템은 재발을 억제하는 실시간 혈관 위치 확인 기술로 외과의들이 전환함에 따라 2031년까지 연평균 6.28%의 성장률을 기록하며 더 빠른 성장 궤도에 있습니다. THD Revolution 플랫폼은 통합 영상, 직관적인 제어, 무균 최적화 액세서리를 통해 이러한 변화를 대표합니다. 적외선 응고기와 경화 요법 주사기는 조직 보존이 최우선인 1-2기 질환에 여전히 적합합니다. 양극성 프로브는 특정 환자군을 대상으로 표적 열 에너지를 공급하는 반면, 냉동치료 기기는 일회용 제품이 여전히 비용 부담이 큰 지역에서 틈새 시장을 찾고 있습니다. 지속가능성 규제가 강화됨에 따라 제조사들은 감염 관리와 환경 영향 사이의 균형을 맞추는 바이오폴리머 하우징과 일회용 키트를 모색 중입니다. 이러한 설계 혁신은 입문형 결찰기의 가치 제안을 유지하면서 해당 카테고리를 고마진 영역으로 이끌 것으로 기대됩니다.

치질 치료 기기 시장은 제품 유형(밴드 결찰기, 양극성 프로브, 레이저 프로브, 냉동치료 기기, 적외선 응고기, 경화 요법 주사기 등) 및 지역(북미, 유럽, 아시아태평양, 중동, 아프리카, 남미)으로 구분됩니다. 위 부문 시장 규모는(백만 달러)로 제공됩니다.

지역별 분석

북미는 2025년 기준 41.86%의 매출 점유율로 선두를 차지했으며, 이는 CPT 코드 46221, 46945, 46946에 대한 메디케어 적용(시술당 평균 400달러 지급)에 힘입은 결과입니다. 강력한 병원 인프라, 고해상도 내시경의 광범위한 보급, 그리고 Class II 결찰기에 대한 FDA 신속 승인 절차는 해당 지역의 우위를 뒷받침합니다.

아시아태평양 지역은 2031년까지 연평균 6.12% 성장률(CAGR)을 기록하며 가장 빠르게 성장하는 지역입니다. 중국은 2024년 의료기기 등록 체계를 간소화하여 평균 심사 주기를 단축하고 시판 후 감시를 강화함으로써 국내외 투자를 동시에 촉진했습니다. 인도의 마케팅 행위 규정은 홍보 기준을 공식화하여 엄격한 준수를 유지하는 다국적 제조사에 유리하게 작용했습니다. 올림푸스는 북미에서 전년 대비 32% 성장률을 기록했으며, 아시아에서 치료용 내시경 수요가 강세를 보인다고 보고하여 위장관 플랫폼의 지역 간 이전 가능성을 확인했습니다. 도시화되는 인구, 증가하는 가처분 소득, 높아진 건강 의식이 결합되어 고급 치질 치료 시술에 대한 지속적인 성장 동력을 창출하고 있습니다.

유럽은 성숙하면서도 탄력적인 시장을 보여줍니다. 엄격한 감염 관리 의무와 환경 지침은 일회용 기기 채택을 촉진하여 제조업체들이 재활용 가능한 생분해성 고분자로 결찰기를 재설계하도록 유도합니다. 보험 적용 구조는 다양하지만, 대부분의 국가 보험사는 현재 고등급 질환에 대한 도플러 유도 시술을 보장하여 꾸준한 교체 주기를 뒷받침합니다. 남미와 중동, 아프리카는 여전히 신흥 시장입니다. 제한된 보험 적용과 훈련된 항문병 전문의 부족으로 주요 도시 외 지역의 보급률은 낮지만, 고용주 지원 보험과 공공 부문 인프라 프로젝트의 증가로 기기 기반 치료 접근성이 점차 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 증상을 동반하는 치질의 유병률 상승

- 최소 침습적 외래 시술 선호도

- 기술 발전(예 : 도플러 가이드 하결결술)

- 아시아태평양 지역 의료비 지출 증가

- 일회용 결찰기(감염 관리)에 대한 규제 강화의 움직임

- 조기 개입을 가능케 하는 AI 유도 내시경

- 시장 성장 억제요인

- 개발도상국 시장의 제한된 보험 적용

- OTC 외용 제품에 의한 기기 도입의 지연

- 농촌 지역의 대장항문외과 의사 부족

- 일회용 플라스틱에 대한 지속가능성 압력

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(금액)

- 제품 유형별

- 고무 밴드 결찰기

- 적외선 응고기

- 경화 요법 주사기

- 양극성 프로브

- 냉동치료 기기

- 도플러 유도 결찰 시스템

- 시술 환경별

- 내시경 결찰술

- 비내시경 처리

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 전문 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Boston Scientific

- Medtronic

- Johnson & Johnson(Ethicon)

- Cook Medical

- Olympus Corporation

- Teleflex Incorporated

- ConMed Corporation

- CooperSurgical(Wallace)

- AMI Agency for Medical Innovations

- Lohmann & Rauscher

- Sklar Surgical Instruments

- Sterylab

- Privi Medical

- The Cooper Companies Inc

- Integra LifeSciences

- Smith & Nephew plc

- Hologic, Inc

제7장 시장 기회와 장래의 전망

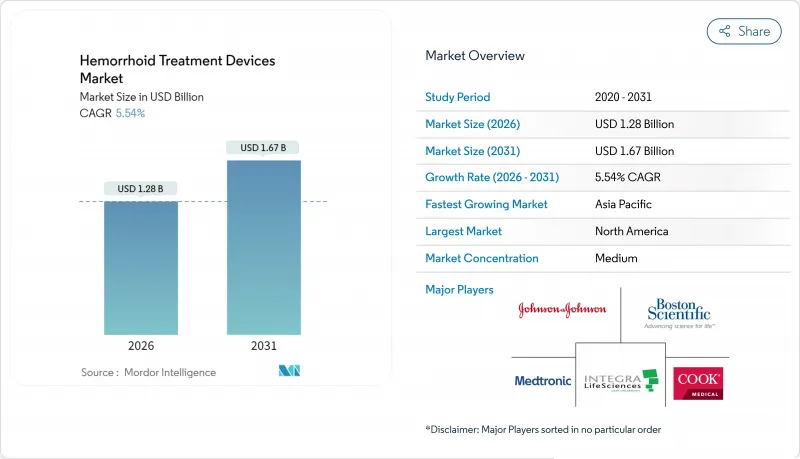

HBR 26.02.04The hemorrhoid treatment devices market size in 2026 is estimated at USD 1.28 billion, growing from 2025 value of USD 1.21 billion with 2031 projections showing USD 1.67 billion, growing at 5.54% CAGR over 2026-2031.

Growth is fueled by aging populations, a global shift toward outpatient care, and the rapid adoption of minimally invasive technologies that shorten recovery times and lower overall treatment costs. AI-guided endoscopy, Doppler-guided ligation, and laser hemorrhoidoplasty are widening the therapeutic toolbox, allowing physicians to intervene earlier, reduce postoperative pain, and improve long-term outcomes. Healthcare payers are increasingly reimbursing outpatient procedures, so providers are prioritizing ambulatory surgical centers that can deliver standardized, high-volume treatments at a lower cost without compromising safety or efficacy. Meanwhile, established manufacturers are focusing on technology differentiation, sustainability, and single-use designs that align with infection-control policies and environmental directives.

Global Hemorrhoid Treatment Devices Market Trends and Insights

Rising Prevalence of Symptomatic Hemorrhoids

Nearly 10 million Americans were affected by symptomatic hemorrhoids in 2024, representing about 5% of the adult population. The incidence rate rises sharply after age 50, ensuring a sustained patient pool as the population ages demographically. Sedentary work patterns, high-fat diets, and increasing obesity intensify symptom severity, especially in urban centers where advanced treatment is readily accessible. As emerging economies age and adopt similar lifestyles, epidemiological curves in those regions are expected to track those of developed markets. Together, these factors underpin a broad and predictable demand base that supports continued expansion of the hemorrhoid treatment devices market

Preference for Minimally Invasive Outpatient Procedures

Patients and payers alike prefer procedures that shorten recovery and avoid overnight admission. Medicare reimburses key hemorrhoid ligation codes, making outpatient treatment financially attractive for providers. Laser hemorrhoidoplasty patients in a 2024 case series reported no pain or bleeding by day 4, highlighting a faster convalescence compared to open surgery. Ambulatory surgical centers, which combine specialized staff with high-throughput workflows, are capturing a growing share of the volume. Collectively, these trends accelerate migration away from inpatient settings and reinforce steady demand for advanced devices.

Limited Reimbursement in Developing Markets

In many emerging economies, insurance budgets prioritize communicable diseases and maternal health, so hemorrhoid interventions are often paid out-of-pocket. The high ticket price of Doppler-guided or laser systems places them out of reach for lower-income patients, leading to a two-tiered market where affluent urban citizens access advanced care while rural populations rely on conservative management. This gap dampens overall installed-base growth, slows training uptake among clinicians, and tempers the long-run CAGR of the hemorrhoid treatment devices market.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances

- Healthcare Expenditure Growth in Asia-Pacific

- OTC Topical Products Delaying Device Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rubber band ligators remained the leader, accounting for 41.98% of the 2025 hemorrhoid treatment devices market share, reflecting decades of clinical familiarity, low unit costs, and minimal capital requirements. Doppler-guided ligation systems, however, are on a faster growth trajectory, posting a 6.28% CAGR to 2031 as surgeons migrate to real-time vessel localization, which curbs recurrence. The THD Revolution platform exemplifies this shift with integrated imaging, intuitive controls, and sterility-optimized accessories. Infrared coagulators and sclerotherapy injectors maintain relevance for grades I and II disease, where tissue sparing is paramount. Bipolar probes supply targeted thermal energy for select patient groups, whereas cryotherapy devices find niche application in districts where disposables remain cost-prohibitive. As sustainability regulations tighten, producers are exploring biopolymer housings and single-use kits that strike a balance between infection control and environmental impact. Such design innovations are expected to preserve the value proposition of entry-level ligators while nudging the category into higher-margin territory.

The Hemorrhoid Treatment Devices Market is Segmented by Product Type (Band Ligators, Bipolar Probes, Laser Probes, Cryotherapy Devices, Infrared Coagulators, Sclerotherapy Injectors, and Others), and Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Value is Provided in (USD Million) for the Above Segments.

Geography Analysis

North America held the leading 41.86% revenue share in 2025, supported by Medicare coverage for CPT codes 46221, 46945, and 46946, which pay providers an average of USD 400 per procedure. Strong hospital infrastructure, widespread availability of high-definition endoscopes, and expedited FDA pathways for Class II ligators underpin the region's dominance.

The Asia-Pacific region is the fastest-growing geography, with a 6.12% CAGR forecasted to 2031. China streamlined its device registration framework in 2024, reducing average review cycles and enhancing post-market surveillance, which in turn boosts both foreign and domestic investment. India's marketing conduct code formalized promotional standards, rewarding multinational producers that maintain rigorous compliance. Olympus recorded 32% year-over-year gains in North America, while reporting strong therapeutic endoscopy demand in Asia, confirming the cross-regional transferability of GI platforms. Urbanizing populations, rising disposable income, and heightened health awareness combine to create sustained momentum for advanced hemorrhoid interventions.

Europe represents a mature yet resilient market. Strict infection-control mandates and environmental directives encourage single-use device adoption, pushing manufacturers to redesign ligators with recyclable bio-polymers. Reimbursement structures vary, yet most national payers now cover Doppler-guided procedures for higher-grade disease, underpinning steady replacement cycles. South America and the Middle East & Africa remain emerging segments: limited reimbursement and fewer trained proctologists cap uptake outside major cities, although rising employer-sponsored insurance and public-sector infrastructure projects are gradually widening access to device-based care.

- Boston Scientific

- Medtronic

- Johnson & Johnson

- Cook Group

- Olympus

- Teleflex

- Conmed

- CooperSurgical (Wallace)

- A.M.I. Agency for Medical Innovations

- Lohmann & Rauscher

- Sklar Surgical Instruments

- Sterylab

- Privi Medical

- The Cooper Companies

- Integra LifeSciences

- Smiths Group

- Hologic

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of symptomatic hemorrhoids

- 4.2.2 Preference for minimally-invasive outpatient procedures

- 4.2.3 Technological advances (e.g., Doppler-guided ligation)

- 4.2.4 Healthcare expenditure growth in Asia-Pacific

- 4.2.5 Regulatory push for single-use ligators (infection control)

- 4.2.6 AI-guided endoscopy enabling earlier intervention

- 4.3 Market Restraints

- 4.3.1 Limited reimbursement in developing markets

- 4.3.2 OTC topical products delaying device adoption

- 4.3.3 Shortage of colorectal surgeons in rural settings

- 4.3.4 Sustainability pressure on disposable plastics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, 2024-2030)

- 5.1 By Product Type

- 5.1.1 Rubber Band Ligators

- 5.1.2 Infrared Coagulators

- 5.1.3 Sclerotherapy Injectors

- 5.1.4 Bipolar Probes

- 5.1.5 Cryotherapy Devices

- 5.1.6 Doppler-Guided Ligation Systems

- 5.2 By Procedure Setting

- 5.2.1 Endoscopic Ligations

- 5.2.2 Non-Endoscopic (Outpatient) Procedures

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Boston Scientific

- 6.3.2 Medtronic

- 6.3.3 Johnson & Johnson (Ethicon)

- 6.3.4 Cook Medical

- 6.3.5 Olympus Corporation

- 6.3.6 Teleflex Incorporated

- 6.3.7 ConMed Corporation

- 6.3.8 CooperSurgical (Wallace)

- 6.3.9 A.M.I. Agency for Medical Innovations

- 6.3.10 Lohmann & Rauscher

- 6.3.11 Sklar Surgical Instruments

- 6.3.12 Sterylab

- 6.3.13 Privi Medical

- 6.3.14 The Cooper Companies Inc

- 6.3.15 Integra LifeSciences

- 6.3.16 Smith & Nephew plc

- 6.3.17 Hologic, Inc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment