|

시장보고서

상품코드

1906101

근전도(EMG) 기기 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Electromyography Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

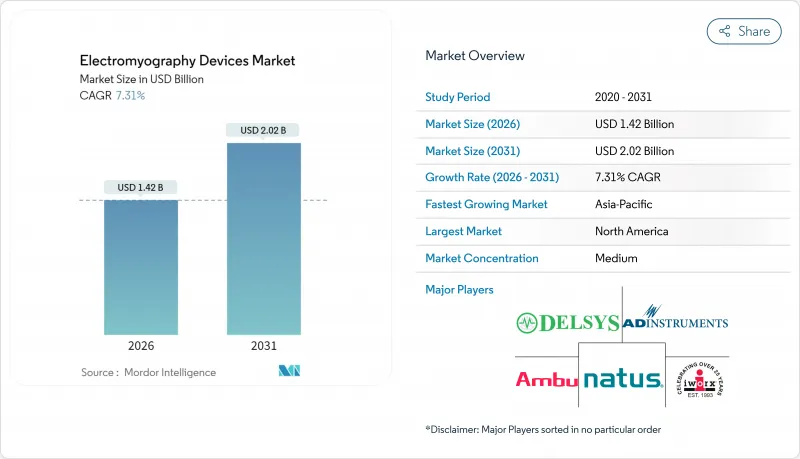

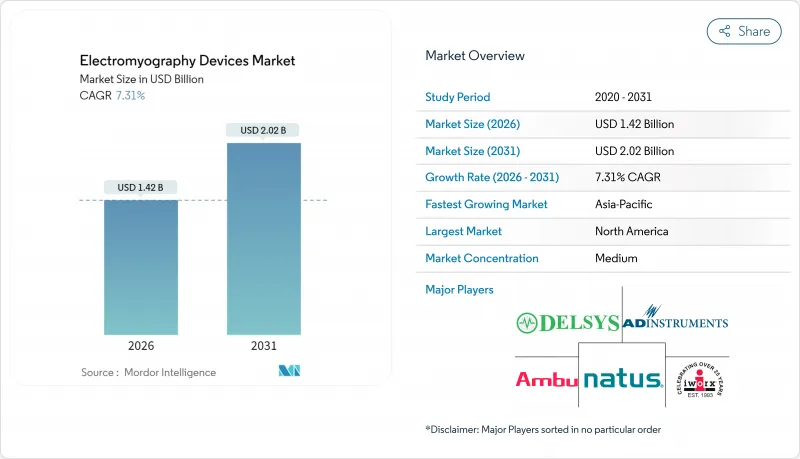

근전도 기기 시장의 규모는 2026년에는 14억 2,000만 달러로 추정되고 있으며, 2025년 13억 2,000만 달러에서 성장할 것으로 예상됩니다.

2031년까지 20억 2,000만 달러에 달하고, 2026년부터 2031년에 걸쳐 CAGR 7.31%로 확대할 것으로 전망되고 있습니다.

고령화, 임상 응용 범위의 확대, 웨어러블 기술 및 AI 탑재 시스템에서의 기술 진보가 함께 성장을 견인하고 있습니다. 신경근 질환의 유병률 상승이 진단 수요를 뒷받침하는 한편, 소형화 센서와 클라우드 해석 기술에 의해 병원 내 뿐만 아니라 재활, 스포츠 의학, 재택 모니터링 등으로 응용 범위가 넓어지고 있습니다. 선진기기의 규제 승인이 혁신 사이클을 단축하고 일회용 전극의 도입이 감염 위험을 줄임으로써 의료 제공업체의 도입 촉진에 기여하고 있습니다. 경쟁 전략은 예측적 지식과 원활한 워크플로를 제공하는 통합 하드웨어-소프트웨어 플랫폼에 집중되어 있으며, 근전도 검사를 정밀 신경근육 관리의 중심에 두고 있습니다.

세계의 근전도 기기 시장의 동향 및 인사이트

신경근 질환 증가 경향과 인구 고령화

평균 수명이 연장됨에 따라 근위축성 측색경화증과 중증 근무력증 등의 질병 발생률이 상승하여 1차 의료와 노년 의료 현장에서 진단 건수가 증가하고 있습니다. 근전도 검사는 신경근 장애의 확인에 화상 진단을 대체하는 비용 대비 효과가 높은 옵션이며, 장기적인 장애 비용 관리를 위해 검사 비용의 환급을 인정하는 지불 기관이 증가하고 있습니다. 경기 순환에 좌우되지 않는 안정적인 수요는 장비 공급업체의 수익을 안정시키는 한편, 1차 의료 의사가 진료 현장에서 근전도 검사 솔루션을 도입하도록 촉구하고 도입 경로를 단축하여 치료 개입을 가속화하고 있습니다.

휴대용 웨어러블 근전도 기기의 기술적 진보

소형화된 전자기기와 무선 연결 기술에 의해 50그램 미만의 기기로 임상 레벨의 정밀도를 실현할 수 있게 되면서 일상 활동 중 연속적인 모니터링이 가능해졌습니다. 48시간을 넘는 배터리 지속시간에 의해 충전 제약이 해소되면서 내장 머신러닝 필터가 아티팩트를 제거하여 전문가의 모니터링 부담을 줄이고 있습니다. 이러한 기능은 의료 신뢰성을 손상시키지 않고 EMG를 소비자 웰빙 및 스포츠 퍼포먼스 분야로 확대하고 있습니다. 이 변화는 시간 경과에 따른 근육 데이터를 분석하는 관련 소프트웨어의 정기 구독을 통한 지속적인 수익 창출을 촉진합니다.

근전도 시스템의 높은 자본 비용 및 유지비

종합적인 플랫폼은 5만-20만 달러의 비용이 들고, 구입 가격의 약 12%에 상당하는 연간 보수 계약이 요구됩니다. 소규모 시설에서는 환급액이 총소유비용을 커버할 수 없는 경우 투자 정당화가 어렵습니다. 차폐실, 절연 트랜스, 주기적인 교정 등 인프라 정비의 추가 부담도 더해집니다. 그 결과, EMG의 대응 능력은 3차 의료기관에 집중되어 대도시권 외의 환자의 접근이 제한되고 있습니다.

부문 분석

2025년 시점에서 표면전극장치는 근전도 기기 시장의 45.62%를 차지하였으며 이는 일상적인 신경근 평가에서의 다용도성의 크기를 나타내고 있습니다. 확립된 프로토콜에 대한 신뢰와 간편한 환급제도에 의해 표면전극장치 시장의 규모는 확대를 계속하고 있습니다. 한편, 웨어러블 시스템은 지속적인 활동 기반 데이터를 제공하고 재활 및 운동 능력 향상 프로그램을 충실화하여 7.95%라는 가장 높은 CAGR을 기록하고 있습니다.

심부근 평가에는 침근전도가 여전히 필수적이며, 저침습 모달리티의 성장에도 불구하고 안정적인 수요를 유지하고 있습니다. 고밀도 어레이는 한때 학술기관으로 제한되었지만, 현재는 복잡한 운동 장애를 분석하는 전문 클리닉의 관심을 끌고 있습니다. FDA의 Glide 표면전극시스템 승인은 신호 품질을 향상시키는 환자 친화적인 설계에 대한 규제 당국의 지원을 보여주는 좋은 예입니다. 소모품이 지속적인 수익을 견인하며 일회용 건식 전극은 교차 감염 위험을 줄이고 물리치료 센터의 업무 효율성을 실현합니다. 감염 관리 연구에 따르면 패혈증 치료 비용은 환자 1인당 33,718달러에 이를 수 있으며 일회용 솔루션은 경제적으로도 합리적입니다. 외래 환자 수가 증가함에 따라 전극 출하량은 공급자 수익의 기초로서 중요성을 높일 것입니다.

독립형 구성은 2025년에 근전도 기기 시장 점유율의 38.25%를 차지하였고 동시에 8.22%의 연평균 복합 성장률(CAGR)을 기록했습니다. 이는 최적화된 신호 품질과 직관적인 워크플로를 제공하는 전용 시스템을 임상의가 선호하는 경향을 반영합니다. 통합형 EMG/EEG 플랫폼은 뇌와 근육의 동시 데이터가 진단에 도움이 되는 간질 및 수면 클리닉에서 틈새 용도를 발견하고 있지만, 설계상의 타협에 의해 둘 중 하나의 모달리티의 심도가 제한될 가능성이 있습니다. FDA Class II 의료기기의 승인과정은 또한 단일기능기기의 승인을 단순화하는 집중 검증을 뒷받침합니다. 병원에서는 독립형 장치에 내장된 전용 해석 소프트웨어와 설정 시간 단축으로 검사 사이클이 단축되어 일일 처리 능력이 향상됩니다.

지역별 분석

북미는 27.95% 시장 점유율을 차지하였고, 전문의 네트워크가 밀집하여 진단용 근전도 검사에 대한 지불자 지원이 갖추어져 있습니다. 민간 보험은 표준 검사를 환급하지만 일부 스포츠 관련 표면 검사를 연구 단계로 분류하기 때문에 부문 확대가 억제됩니다. FDA의 승인 경로는 장비의 업그레이드 사이클을 가속화하지만, 지방 지역에서 신경생리학자의 부족이 계속되어 도시 지역 이외의 보급을 늦추고 있습니다.

아시아태평양은 공중 보건 예산의 중점 배분과 진단 능력에 대한 민간 투자로 9.12%라는 가장 높은 CAGR을 기록하고 있습니다. 중국은 3차 의료병원을 확대하는 동시에 수입 의존도를 억제하기 위해 국내 의료기기 제조를 촉진하고 있습니다. 일본은 고령화가 진행됨에 따라 근전도 검사 건수가 증가하고, 고정밀 검사가 국가 환급 대상 리스트에 포함되고 있습니다. 인도의 중견 병원에서는 부유층 시장에서 선호되는 고급 기능이 필요하지 않으며 최소한의 성능을 제공하는 비용 효율적인 시스템이 필요합니다. 현지 조립과 유연한 자금 조달로 공급업체의 경쟁력이 높아지고 있습니다.

유럽에서는 통일된 의료기기규정(MDR) 인증을 통해 크로스보더 유통이 단순화되어 안정적인 성장을 유지하고 있습니다. 일반 데이터 보호 규정(GDPR, EU 개인정보보호규정)에 대한 대응은 엄격한 데이터 보안 관리를 요구하며, 공급업체는 암호화, 사용자 동의, 지역별 호스팅 옵션의 통합을 추진하고 있습니다. 신경학 서비스가 성숙한 독일, 프랑스, 영국이 도입을 주도하는 한편, 동유럽에서는 EU 구조 기금에 의한 의료 근대화에 따라 단계적인 보급이 진행되고 있습니다. 남미 및 중동 및 아프리카에서는 정부와 병원의 연계를 통한 이동식 근전도 검사실의 전개가 의료 과소 지역에 새로운 판매 채널을 개척하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 신경근질환의 유병률 상승과 인구 고령화

- 휴대형 및 웨어러블 EMG 기기의 기술적 진보

- 수술 중 신경 모니터링의 보급 확대

- 예측 진단을 위한 AI 탑재 실시간 근전도 해석

- 물리치료 클리닉용 저비용 일회용 건식 전극의 급증

- 억제요인

- 근전도 시스템의 높은 자본 비용 및 유지 관리 비용

- 숙련된 신경생리학자 및 기술자의 부족

- 클라우드 기반 EMG 플랫폼에 대한 데이터 프라이버시 우려

- 스포츠 의학에서의 근전도 검사 보험 적용 범위 제한

- 가치 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 표면 근전도 기기

- 침근전도 기기

- 웨어러블 및 휴대용 근전도 시스템

- 고밀도 근전도 시스템

- 근전도 전극 및 부속품

- 모달리티별

- 독립형 근전도 시스템

- 통합형 근전도 및 뇌파 시스템

- 용도별

- 신경근 질환의 진단

- 통증 관리 및 재활

- 정형외과 및 스포츠의학

- 수술 중 모니터링

- 연구 및 학술

- 최종 사용자별

- 병원

- 전문 클리닉

- 외래수술센터(ASC)

- 스포츠 재활센터

- 학술기관 및 연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Cadwell Industries Inc.

- Cometa Systems srl

- Compumedics Ltd.

- G.Tec Medical Engineering GmbH

- Inomed Medizintechnik GmbH

- Medtronic plc

- Natus Medical Incorporated

- NeuroMetrix, Inc.

- Neurosoft LLC

- Nihon Kohden Corporation

- Noraxon USA, Inc.

- OT Bioelettronica Srl

- Plexon Inc.

- TMSi(Artinis Medical Systems BV)

- Delsys

제7장 시장 기회 및 미래 전망

CSM 26.01.28Electromyography devices market size in 2026 is estimated at USD 1.42 billion, growing from 2025 value of USD 1.32 billion with 2031 projections showing USD 2.02 billion, growing at 7.31% CAGR over 2026-2031.

Demographic aging, broader clinical applications, and technological advances in wearable and AI-enabled systems collectively fuel this expansion. Rising neuromuscular disease prevalence sustains diagnostic demand, while miniaturized sensors and cloud analytics broaden use beyond hospital walls into rehabilitation, sports medicine, and home monitoring. Regulatory clearances for advanced devices shorten innovation cycles, and single-use electrode adoption mitigates infection risk, supporting provider uptake. Competitive strategies concentrate on integrated hardware-software platforms that deliver predictive insights and seamless workflows, positioning electromyography at the center of precision neuromuscular care.

Global Electromyography Devices Market Trends and Insights

Rising Prevalence of Neuromuscular Disorders and Aging Population

Rising life expectancy elevates the incidence of conditions such as amyotrophic lateral sclerosis and myasthenia gravis, raising diagnostic volumes across primary care and geriatric settings. EMG offers a cost-effective alternative to imaging for confirming neuromuscular impairment, and payers increasingly reimburse testing to manage long-term disability costs. Consistent demand, irrespective of economic cycles, stabilizes revenue for device suppliers while encouraging primary-care physicians to adopt point-of-care EMG solutions that shorten referral pathways and speed therapeutic intervention.

Technological Advances in Portable and Wearable EMG Devices

Miniaturized electronics and wireless connectivity now deliver clinical-grade accuracy in devices under 50 grams, enabling continuous monitoring during daily activity. Battery life exceeding 48 hours eliminates charging constraints, and on-board machine-learning filters remove artifacts, reducing specialist oversight. These features expand EMG into consumer wellness and sports performance arenas without compromising medical reliability. The shift also stimulates recurring revenue through companion software subscriptions that analyze longitudinal muscle data.

High Capital and Maintenance Cost of EMG Systems

Comprehensive platforms cost USD 50,000-USD 200,000 and demand annual service contracts near 12% of purchase price. Smaller facilities struggle to justify investment when reimbursement fails to cover total ownership costs. Infrastructure upgrades-shielded rooms, isolation transformers, and regular calibration-add to the burden. Consequently, EMG capacity clusters in tertiary hospitals, limiting access for patients outside metropolitan hubs.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Intra-operative Neuromonitoring

- AI-Enabled Real-Time EMG Analytics for Predictive Diagnostics

- Shortage of Trained Neurophysiologists and Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface devices accounted for a 45.62% electromyography devices market share in 2025, underscoring their versatility across routine neuromuscular evaluations. The electromyography devices market size for surface devices continues to rise as clinicians trust established protocols and reimbursement is straightforward. Wearable systems, however, post the fastest 7.95% CAGR by delivering continuous, activity-based data that enrich rehabilitation and athletic performance programs.

Needle EMG remains indispensable for deep-muscle assessment, sustaining stable demand even as less invasive modalities grow. High-density arrays, once confined to academia, now attract specialty clinics analyzing complex movement disorders. FDA clearance of the Glide surface electrode system exemplifies regulatory endorsement of patient-friendly designs that enhance signal quality. Consumables drive recurring revenue: single-use dry electrodes reduce cross-infection risk and streamline workflow for physiotherapy centers. Infection-control studies report potential sepsis treatment costs of USD 33,718 per affected patient, making disposable solutions financially prudent. As outpatient volumes climb, electrode shipments will increasingly anchor supplier revenue.

Standalone configurations captured 38.25% of electromyography devices market share in 2025 and simultaneously posted an 8.22% CAGR, reflecting clinician preference for purpose-built systems offering optimized signal quality and intuitive workflows. Integrated EMG/EEG platforms find niche use in epilepsy and sleep clinics where simultaneous brain-muscle data inform diagnosis, yet design compromises can limit depth in either modality. FDA Class II device pathways also favor focused validation, simplifying approvals for single-purpose equipment. Hospitals value the reduced setup time and dedicated analysis software embedded in standalone units, which shortens exam cycles and increases daily throughput.

The Electromyography Devices Market Report is Segmented by Product Type (Surface EMG Devices, Needle EMG Devices, and More), Modality (Stand-Alone EMG Systems, Integrated EMG/EEG Systems), Application (Neuromuscular Disorder Diagnosis, Pain Management & Rehabilitation, and More), End User (Hospitals, Specialty Clinics, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America combines 27.95% market share with a dense specialist network and payer support for diagnostic EMG procedures. Commercial insurers reimburse standard tests, yet classify some sports-related surface studies as investigational, tempering segment expansion. FDA pathways expedite device upgrade cycles, but rural shortages of neurophysiologists persist, slowing penetration beyond urban centers.

Asia-Pacific registers the fastest 9.12% CAGR through targeted public-health budgets and private investment in diagnostic capability. China expands tertiary-care hospitals while encouraging domestic device manufacturing to curb import reliance. Japan's advanced aging boosts electromyography volumes, and national reimbursement lists endorse high-precision testing. India's mid-tier hospitals demand cost-efficient systems that deliver acceptable performance without the premium features favored in wealthier markets. Local assembly and flexible financing help suppliers compete.

Europe maintains consistent growth under unified MDR certification that simplifies cross-border distribution. GDPR compliance imposes rigorous data-security controls, prompting vendors to embed encryption, user consent, and regional hosting options. Germany, France, and the United Kingdom lead uptake due to mature neurology services, while Eastern Europe sees gradual adoption as EU structural funds modernize healthcare. South America and Middle East/Africa open new sales channels as government-hospital partnerships deploy mobile EMG labs to underserved communities.

- Abbott Laboratories

- Cadwell

- Cometa Systems srl

- Compumedics Ltd.

- G.Tec Medical Engineering GmbH

- Inomed Medizintechnik

- Medtronic

- Natus Medical

- NeuroMetrix

- Neurosoft LLC

- Nihon Kohden

- Noraxon USA, Inc.

- OT Bioelettronica Srl

- Plexon Inc.

- TMSi (Artinis Medical Systems BV)

- Delsys

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of neuromuscular disorders and ageing population

- 4.2.2 Technological advances in portable & wearable EMG devices

- 4.2.3 Growing adoption of intra-operative neuromonitoring

- 4.2.4 AI-enabled real-time EMG analytics for predictive diagnostics

- 4.2.5 Surge in low-cost single-use dry electrodes for physiotherapy clinics

- 4.3 Market Restraints

- 4.3.1 High capital & maintenance cost of EMG systems

- 4.3.2 Shortage of trained neurophysiologists & technicians

- 4.3.3 Data-privacy concerns around cloud-based EMG platforms

- 4.3.4 Limited reimbursement for sports-medicine EMG assessments

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Surface EMG Devices

- 5.1.2 Needle EMG Devices

- 5.1.3 Wearable / Portable EMG Systems

- 5.1.4 High-Density EMG Systems

- 5.1.5 EMG Electrodes & Accessories

- 5.2 By Modality

- 5.2.1 Stand-alone EMG Systems

- 5.2.2 Integrated EMG/EEG Systems

- 5.3 By Application

- 5.3.1 Neuromuscular Disorder Diagnosis

- 5.3.2 Pain Management & Rehabilitation

- 5.3.3 Orthopedics & Sports Medicine

- 5.3.4 Intraoperative Monitoring

- 5.3.5 Research & Academia

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Specialty Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Sports Rehabilitation Centers

- 5.4.5 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Cadwell Industries Inc.

- 6.3.3 Cometa Systems srl

- 6.3.4 Compumedics Ltd.

- 6.3.5 G.Tec Medical Engineering GmbH

- 6.3.6 Inomed Medizintechnik GmbH

- 6.3.7 Medtronic plc

- 6.3.8 Natus Medical Incorporated

- 6.3.9 NeuroMetrix, Inc.

- 6.3.10 Neurosoft LLC

- 6.3.11 Nihon Kohden Corporation

- 6.3.12 Noraxon USA, Inc.

- 6.3.13 OT Bioelettronica Srl

- 6.3.14 Plexon Inc.

- 6.3.15 TMSi (Artinis Medical Systems BV)

- 6.3.16 Delsys

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment