|

시장보고서

상품코드

1906103

대용량 비경구 의약품(LVP) 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Large Volume Parenteral (LVP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

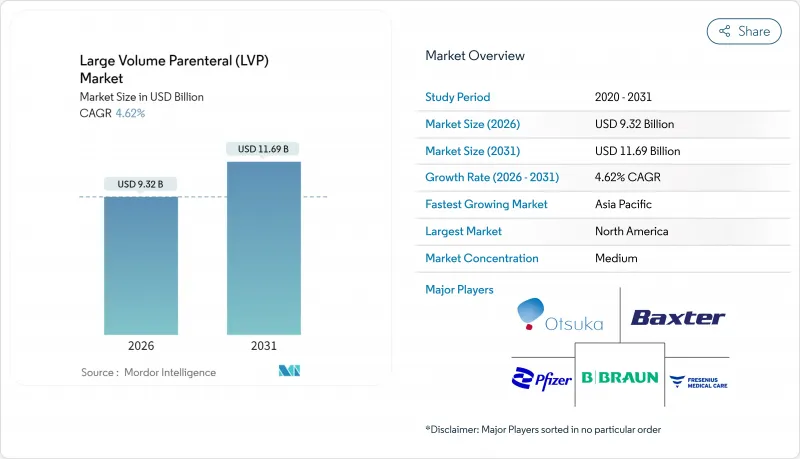

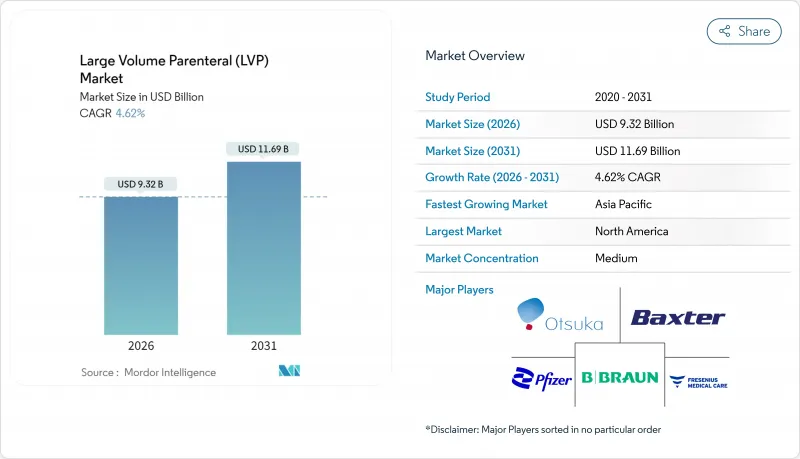

2026년 대용량 비경구 의약품(LVP) 시장의 규모는 93억 2,000만 달러로 추정되며, 2025년 89억 1,000만 달러에서 성장할 것으로 예상됩니다.

2031년까지는 116억 9,000만 달러에 달하고, 2026년부터 2031년에 걸쳐 CAGR 4.62%로 확대될 전망입니다.

수술 건수 증가, 만성 질환의 부담 확대, 무균 처리 자동화의 보급 확대가 함께 안정된 성장 궤도를 뒷받침하고 있습니다. 또한 병원 밖에서의 점적요법을 가능하게 하는 재택 주입 프로그램에 대한 수요 증가도 기여하고 있으며, 또한 BFS(블로우-충전-밀봉) 기술의 규제면에서의 도입이 진행됨으로써 생산 능력의 확대가 가속화되고 있습니다. 고분자 백과 의약품 등급의 물 인프라에 대한 공급망 투자는 유리 바이알 공급 부족 현상이 계속되는 가운데 제조 탄력성(회복력)을 지속적으로 향상시키고 있습니다. 경쟁 전략은 규모 확대, 수직 통합, 기술 업그레이드에 초점을 맞추고 있으며, 대용량 비경구 의약품(LVP) 시장은 구조적으로는 완만하지만 꾸준히 진화하는 환경을 나타내고 있습니다.

세계의 대용량 비경구 의약품(LVP) 시장의 동향 및 인사이트

세계적인 수술 건수 증가

2024년에는 선택적 수술 건수가 빠르게 회복되었고, 팬데믹 동안 누적된 수술을 병원이 진행하면서, 2019년 기준치를 12% 웃돌았습니다. 각 수술에서는 보통 2-4리터의 정맥내 수액이 소비되기 때문에 대용량 비경구 의약품(LVP) 시장에 대한 총 수요가 증가하고 있습니다. 로봇 수술의 도입 확대(2024년에는 18% 증가)는 수술 시간을 연장하고, 수술 기간의 수액 수요를 증가시킵니다. 노인 환자층 증가가 이 경향을 더욱 강화하고 있으며, 65세 이상의 환자는 혈행동태의 안정화를 위해 추가적인 주입액을 필요로 하는 경우가 많습니다.

만성 질환의 유병률 증가와 수액 요법의 도입 확대

만성 신장병은 8억 5,000만 명에 영향을 미치고, 투석 프로토콜만으로 28억 달러 규모의 주입 시장을 형성하고 있습니다. 심부전은 2024년에 세계에서 6,400만 증례에 달하였고, 이는 특수 전해질 용액에 대한 수요를 촉진하고 있습니다. 미국 질병 예방관리센터(CDC)의 기록에 따르면 당뇨병 관련 정맥내 요법을 필요로 하는 입원은 23% 증가하였으며, 전형적인 당뇨병성 케톤산증의 치료에는 1회당 6-8리터의 주입이 필요합니다.

복잡한 제제 설계와 추출물 및 용출물 규제에 대한 대응 과제

2024년에 발표된 FDA 및 USP 갱신 지침에서는 용기 밀봉 시스템에 대한 철저한 분석 시험을 의무화하고 검증 기간이 최대 24개월로 연장되었으며 제품당 280만 달러의 컴플라이언스 비용이 추가되었습니다. 추출물을 0.15μg/일 단위로 정량화하는 요건은 중소기업의 부담을 증대시켜 제품 도입을 늦추고 대용량 비경구 의약품(LVP) 시장의 성장을 억제하고 있습니다.

부문 분석

2,000mL 초과 부문은 24-48시간 지속 투여를 필요로 하는 종양학 및 집중치료 프로토콜에 뒷받침되어 2031년까지 연평균 복합 성장률(CAGR) 9.08%로 추이할 전망입니다. 제조 기술의 진보로 2024년 이후 이러한 초대용량 용기의 생산 비용은 18% 절감되었습니다. 한편, 500-1,000mL 부문은 중형 포맷을 규정하는 표준화된 수술 및 응급 가이드라인에 의해 2025년에 대용량 비경구 의약품(LVP) 시장의 39.12%의 점유율을 유지했습니다. 규제 당국은 라인 변경을 최소화하기 위해 대형 유닛을 권장하며, 이는 성장을 더욱 뒷받침합니다. 소용량 부문은 소아과 및 외래 환자의 요구에 부응하며, 대용량 비경구 의약품(LVP) 시장에서 최종 용도 프로파일의 다양화를 통해 종합적인 탄력성을 강화하고 있습니다.

치료용 주사제는 안전한 주입을 위해 다량의 희석을 필요로 하는 항생제, 화학요법제, 특수제를 포함하여 2025년 수익의 45.10%를 차지하면서 시장을 독점했습니다. 그러나 영양제제는 HPN(완전경장영양)의 적용범위 확대와 장기보존 안정성을 배경으로 CAGR 9.88%로 급성장하고 있습니다. 환자 고유의 대사 프로파일에 맞춘 맞춤 아미노산 및 지질 배합이 실현되어, 대용량 비경구 의약품(LVP) 시장에서의 수량 할인을 상쇄하는 프리미엄 가격대를 뒷받침하고 있습니다.

지역별 분석

북미는 2025년 매출액의 35.25%를 차지하였으며, 높은 처치건수, 선진적인 환급제도, 확립된 규제경로가 성장 기반이 되고 있습니다. 시장의 선도기업은 도시 및 지방 시설 모두에 대한 적시 배송을 보장하는 밀접한 유통 네트워크를 활용하고 있습니다. 견고한 보험 적용 범위는 대용량 비경구 의약품(LVP) 시장에서 가격 압력을 완화합니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 8.63%로 가장 빠르게 성장할 전망입니다. 인도는 생산연동형 장려제도로 무균주사제 시설에 20억 달러 이상이 투입되어 국내 생산량이 25% 증가했습니다. 중국은 2024년 승인 기간을 40% 단축하여 국내 기업이 국내 시장과 수출 채널 모두에서 점유율을 확보하도록 지원했습니다. 일본과 한국은 고령화가 수요를 더욱 확대하고 있습니다.

유럽은 엄격하면서도 조화를 이룬 EMA 기준에 따라 다국간 등록이 효율화되어 여전히 큰 존재감을 유지하고 있습니다. 지속가능성에 대한 요구는 병원에서 재활용가능한 폴리머 백 도입을 촉진하고, 유럽 공급업체는 친환경 포장의 조기 도입자로서 우위를 얻고 있습니다. 독일은 하이브리드 BFS 라인의 도입을 주도하여 유럽의 대용량 비경구 의약품(LVP) 시장의 경쟁력을 강화하고 있습니다.

라틴아메리카, 중동, 아프리카의 신흥 지역에서는 시장의 규모는 작지만 두 자릿수의 수량 성장이 보고되었습니다. 인프라 정비, 기증자 자금에 의한 보건 프로그램, 단계적인 규제 근대화가 촉진요인이나 공급 체인의 과제는 여전히 남아 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 세계적인 외과 수술 건수 증가

- 만성 질환의 유병률 증가와 주입 요법의 도입 확대

- 재택 점적 요법 및 경장 영양 프로그램의 확대

- BFS(블로우-충전-밀봉) 및 기타 무균 자동화 기술의 도입

- 대용량 웨어러블 및 피하 주사기로의 이행에 의한 병원 내 체류시간 단축

- 주사용수(WFI) 및 즉시 사용 멀티 챔버 백에 대한 공급 체인 투자

- 억제요인

- 복잡한 제제 설계와 추출물 및 용출물(E&L) 규제 대응 과제

- 대규모 병원 입찰에서의 가격 압력과 환급 상한

- 유리 포장 부족과 재료 리콜 위험

- 일부 생물학적 제제에 대한 정맥내 투여에서 피하 투여로의 전환 경향으로 LVP 수요 감소

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 수량별

- 100-250 mL

- 250-500 mL

- 500-1,000 mL

- 1,000-2,000 mL

- 2,000 mL 초과

- 용도별

- 치료용 주사제

- 체엑 균형용 주사제

- 영양 보급 및 비경구 영양 주사제

- 포장 유형별

- 유리병

- 연질 백(PVC, 비PVC)

- 제조 기술별

- 기존 무균 충전 및 마감

- BFS(블로우-충전-밀봉)

- 최종 사용자별

- 병원

- 재택치료 및 대체 시설에서의 점적 요법

- 외래수술센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Amanta Healthcare

- B. Braun SE

- BAG Healthcare GmbH

- Baxter International

- Becton Dickinson & Co.

- Eurofarma

- Fresenius Kabi AG

- Grifols SA

- ICU Medical Inc.

- JW Life Science

- Kelun Pharma

- Otsuka Pharmaceutical Co.

- Pfizer Inc.

- Salius Pharma

- Taj Pharma

- Terumo Corp.

- Teva Pharmaceutical Industries

- Vifor Pharma Group

제7장 시장 기회 및 미래 전망

CSM 26.01.21The large volume parenteral market size in 2026 is estimated at USD 9.32 billion, growing from 2025 value of USD 8.91 billion with 2031 projections showing USD 11.69 billion, growing at 4.62% CAGR over 2026-2031.

Rising surgical case counts, an expanding chronic disease burden, and broader adoption of automated aseptic processing collectively underpin this stable trajectory. Demand also benefits from home-based infusion programs that shift IV therapy outside hospitals, while regulatory recognition of Blow-Fill-Seal (BFS) technology accelerates capacity expansion. Supply chain investments in polymer bags and pharmaceutical-grade water infrastructure continue to improve manufacturing resilience, even as glass vial shortages linger. Competitive strategies center on scale, vertical integration, and technology upgrades, indicating a structurally moderate but steadily evolving landscape for the large volume parenteral market.

Global Large Volume Parenteral (LVP) Market Trends and Insights

Rising Surgical Volumes Worldwide

Elective procedure throughput recovered sharply in 2024, exceeding 2019 baselines by 12% as hospitals addressed pandemic-era backlogs. Each surgical event typically consumes 2-4 L of IV fluids, increasing aggregate demand for the large volume parenteral market. Growing robotic surgery uptake-up 18% in 2024-extends operating times and thus elevates perioperative fluid requirements. An aging patient cohort intensifies this pattern because individuals over 65 often need additional volume for hemodynamic stability.

Growing Chronic Disease Prevalence & Fluid Replacement Therapy Adoption

Chronic kidney disease affects 850 million people, and dialysis protocols alone represent a USD 2.8 billion fluid segment. Heart failure reached 64 million global cases in 2024, spurring demand for specialized electrolyte solutions. The Centers for Disease Control and Prevention recorded a 23% rise in diabetes-related hospitalizations requiring IV therapy, where typical diabetic ketoacidosis care involves 6-8 L of fluids per episode.

Complex Formulation & Extractables-Leachables Compliance Challenges

FDA and USP updates released in 2024 force exhaustive analytical testing of container-closure systems, extending validation timelines to as long as 24 months and adding USD 2.8 million in compliance costs per product. Requirements to quantify extractables down to 0.15 µg/day strain smaller firms and slow product introductions, tempering the growth of the large volume parenteral market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Home-Based Infusion & Parenteral Nutrition Programs

- Adoption of BFS & Other Automated Aseptic Technologies

- Price Pressures & Reimbursement Caps in High-Volume Hospital Tenders

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The >2,000 mL category will post a 9.08% CAGR through 2031, buoyed by oncology and critical-care protocols that demand continuous delivery for 24-48 hours. Manufacturing advances have shaved 18% off production costs for these ultra-large containers since 2024. Meanwhile, the 500-1,000 mL range retained 39.12% large volume parenteral market share in 2025, due to standardized intra-operative and emergency guidelines that specify this mid-sized format. Regulatory bodies favor larger units to minimize line changes, further anchoring growth. Smaller segments serve pediatric and outpatient needs and collectively add resilience by diversifying end-use profiles in the large volume parenteral market.

Therapeutic injections dominated 2025 revenues at 45.10%, covering antibiotics, chemotherapy agents, and specialty drugs that require dilution in large volumes for safe infusion. Nutritious formulations, however, are accelerating at a 9.88% CAGR on the back of expanded HPN coverage and longer shelf-life stability. Customized amino-acid and lipid blends now match patient-specific metabolic profiles, supporting premium price points that offset volume discounts elsewhere in the large volume parenteral market.

The Large Volume Parenteral Market Report is Segmented by Volume (100 ML - 250 ML, 250 ML - 500 ML, and More), Application (Therapeutic Injections, and More), Type of Packaging (Bottles, and Flexible Bags), Manufacturing Technology (Traditional Aseptic Fill-Finish and Blow-Fill-Seal (BFS)), End User (Hospitals and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 35.25% of 2025 revenues, anchored by high procedure counts, advanced reimbursement systems, and established regulatory pathways. Market leaders leverage dense distribution networks that secure timely deliveries to urban and rural facilities alike. Robust insurance coverage also cushions price pressures in the large volume parenteral market.

Asia-Pacific is the fastest-growing territory at 8.63% CAGR through 2031. India's Production Linked Incentive scheme injected more than USD 2 billion into sterile injectable facilities, lifting domestic output 25%. China slashed approval timelines by 40% in 2024, enabling local firms to capture share in both domestic and export channels. Aging populations in Japan and South Korea further amplify demand.

Europe retains a sizable footprint owing to stringent but harmonized EMA standards that streamline multi-country registrations. Sustainability mandates push hospitals toward recyclable polymer bags, giving European suppliers an early-adopter advantage in green packaging. Germany leads adoption of hybrid BFS lines, reinforcing the competitive position of the European large volume parenteral market.

Emerging regions in Latin America, the Middle East, and Africa report double-digit unit growth, albeit from small bases. Infrastructure upgrades, donor-funded health programs, and gradual regulatory modernization provide incremental tailwinds, but supply chain gaps persist.

- Amanta Healthcare

- B. Braun

- BAG Healthcare GmbH

- Baxter

- Becton Dickinson & Co.

- Eurofarma

- Fresenius

- Grifols

- ICU Medical

- JW Life Science

- Kelun Pharma

- Otsuka Pharmaceutical Co.

- Pfizer

- Salius Pharma

- Taj Pharma

- Terumo Corp.

- Teva Pharmaceutical Industries

- Vifor Pharma Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Surgical Volumes Worldwide

- 4.2.2 Growing Chronic Disease Prevalence & Adoption of Fluid Replacement Therapies

- 4.2.3 Expansion of Home-Based Infusion & Parenteral Nutrition Programs

- 4.2.4 Adoption of Blow-Fill-Seal (BFS) & Other Automated Aseptic Technologies

- 4.2.5 Shift Toward Large-Volume Wearable/SC Injectors Reducing Hospital Time

- 4.2.6 Supply-Chain Investments In Water-For-Injection (WFI) & Ready-To-Use Multichamber Bags

- 4.3 Market Restraints

- 4.3.1 Complex Formulation & Extractables-Leachables (E&L) Compliance Challenges

- 4.3.2 Price Pressures & Reimbursement Caps in High-Volume Hospital Tenders

- 4.3.3 Glass-Packaging Shortages & Material Recall Risks

- 4.3.4 Emerging Shift of Some Biologics From IV to SC Reducing LVP Demand

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Volume

- 5.1.1 100 - 250 mL

- 5.1.2 250 - 500 mL

- 5.1.3 500 - 1,000 mL

- 5.1.4 1,000 - 2,000 mL

- 5.1.5 More Than 2,000 mL

- 5.2 By Application

- 5.2.1 Therapeutic Injections

- 5.2.2 Fluid-Balance Injections

- 5.2.3 Nutritious/Parenteral Nutrition Injections

- 5.3 By Type of Packaging

- 5.3.1 Bottles (Glass)

- 5.3.2 Flexible Bags (PVC, Non-PVC)

- 5.4 By Manufacturing Technology

- 5.4.1 Traditional Aseptic Fill-Finish

- 5.4.2 Blow-Fill-Seal (BFS)

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Home-Care & Alternate Site Infusion

- 5.5.3 Ambulatory Surgical Centers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Amanta Healthcare

- 6.3.2 B. Braun SE

- 6.3.3 BAG Healthcare GmbH

- 6.3.4 Baxter International

- 6.3.5 Becton Dickinson & Co.

- 6.3.6 Eurofarma

- 6.3.7 Fresenius Kabi AG

- 6.3.8 Grifols S.A.

- 6.3.9 ICU Medical Inc.

- 6.3.10 JW Life Science

- 6.3.11 Kelun Pharma

- 6.3.12 Otsuka Pharmaceutical Co.

- 6.3.13 Pfizer Inc.

- 6.3.14 Salius Pharma

- 6.3.15 Taj Pharma

- 6.3.16 Terumo Corp.

- 6.3.17 Teva Pharmaceutical Industries

- 6.3.18 Vifor Pharma Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment