|

시장보고서

상품코드

1906105

키네시오 테이프 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Kinesio Tape - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

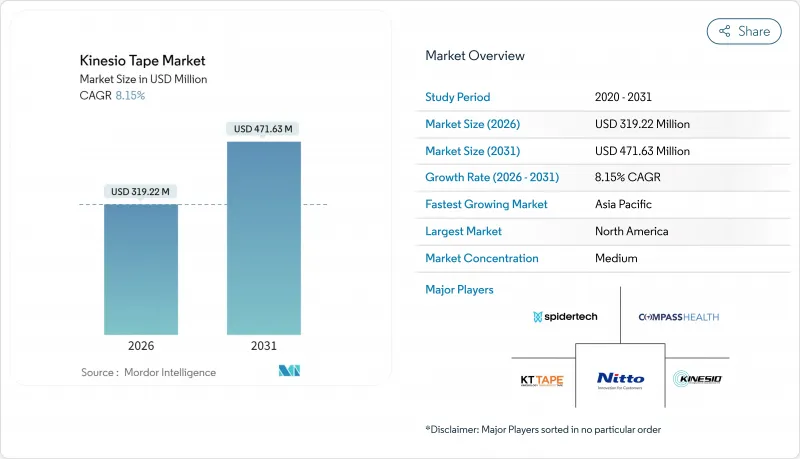

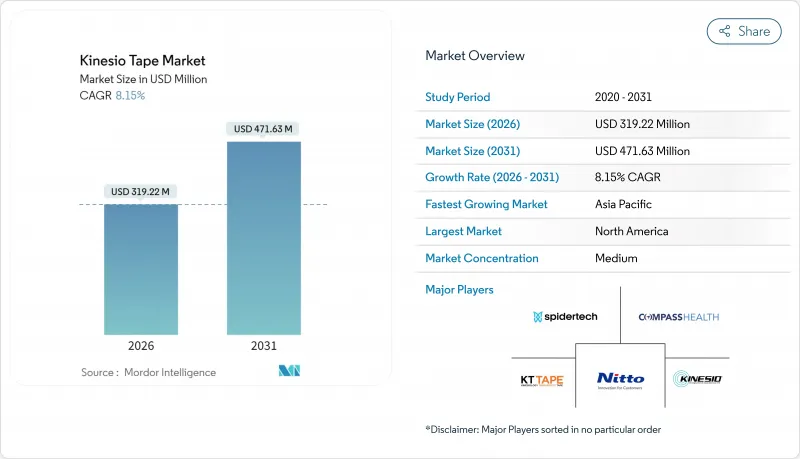

2026년 키네시오 테이프 시장의 규모는 3억 1,922만 달러로 추정되며, 2025년 2억 9,518만 달러에서 성장을 계속하고 있습니다.

2031년에는 4억 7,163만 달러에 달할 전망으로, 2026년부터 2031년에 걸쳐 CAGR 8.15%로 확대될 것으로 예측되고 있습니다.

치료 효과에 관한 지속적인 실증과 근골격계, 림프계, 신경계로의 응용 범위 확대가 임상 현장, 스포츠 분야, 재택 치료 환경에서의 수요를 견인하고 있습니다. 물리치료 클리닉이 수술 후 부종 관리를 위한 테이핑 절차를 표준화하는 가운데 기관용 구매는 견조하게 유지되고 있습니다. 한편, 소비자용 도입은 접근과 지식 습득을 간소화하는 전자상거래 채널을 통해 가속하고 있습니다. 북미는 확립된 스포츠의학 에코시스템을 배경으로 수익면에서 우위를 유지하고 있지만, 아시아태평양에서는 가처분 소득 증가와 외래 재활 능력의 확대에 따라 수량면에서 가장 급속한 성장을 기록하고 있습니다. 경쟁은 현재 재료과학과 트레이닝 서비스에 초점을 맞추고 있으며, 벤더는 내구성이 뛰어난 합성 소재와 올바른 부착법을 중시한 공인 시술자 프로그램을 통해 차별화를 도모하고 있습니다.

세계의 키네시오 테이프 시장의 동향 및 인사이트

스포츠 부상의 확산과 증가하는 운동 인구

스포츠 참여가 증가함에 따라 청소년부터 프로 선수에 이르기까지 근골격계 손상이 증가하여 키네시오 테이프 시장을 견인하고 있습니다. 육상 경기에서는 2014년부터 2023년에 걸쳐 12만 8,761건의 다리 손상이 기록되었고, 염좌와 좌상이 전체 사례의 거의 절반을 차지했습니다. 축구는 동기간 내에 84만 3,063건의 다리 손상이 발생하여 비제한적 회복 보조구에 대한 수요가 증가하고 있습니다. 2024년 파리올림픽에서의 높은 인지도로 인해 엘리트 선수의 테이핑이 일반화되고 소비자의 관심도 높아졌습니다.

물리치료 및 병원에서의 임상 도입

메타분석에 따르면, 테이핑은 인공 슬관절 전치환술 후 무릎 부종과 통증을 완화하고, 뇌졸중 후 삼킴 장애의 회복을 촉진하는 것으로 나타났으며, 병원이 종합적 재활 프로그램에 통합하는 움직임이 확산되고 있습니다. OSHA(미국노동안전보건국)가 2024년에 키네시오 테이프를 응급처치로 분류함으로써 직장환경에서 관리상의 장벽이 경감되었습니다. 손가락 손상에 대한 무작위화 비교 시험은 경성 스프린트와 비교하여 가동 영역과 편안함이 뛰어남을 입증하여 임상의의 신뢰를 더욱 강화했습니다. 이러한 지식은 지불자의 수용 범위를 넓혀 외래 네트워크 내에서 처방약 리스트로의 도입을 촉진하고 있습니다.

임상 효능에 대한 불확실한 증거

여러 메타 분석이 통증 완화 효과를 강조하는 반면 무릎 기능과 고유 수용 감각의 개선은 매우 미미하다고 지적하고 있으며, 지침위원회는 신중한 권장 사항을 발표했습니다. 연구자들은 위약 효과가 결과에 영향을 미칠 가능성을 주장하고, 검토자는 메커니즘을 명확하게 해명하기 위해 보다 대규모의 무작위화 시험 설계를 요구받고 있습니다.

부문 분석

롤형 제품은 임상의가 재단 길이와 신축성을 제어할 수 있는 이점으로 인해 2025년 시점에서 키네시오 테이프 시장의 46.28%의 점유율을 유지했습니다. 이 형태는 병원과 스포츠 프랜차이즈의 대량 구매 예산에 적합합니다. 그러나 복잡한 관절에 대한 해부학적 정확성을 요구하는 치료사와 오사용 방지 키트를 요구하는 소비자 수요가 증가함에 따라 프리쉐이핑 제품 시장은 CAGR 5.92%로 확대되고 있습니다. 주요 브랜드는 접착 경로를 설명하는 QR 코드 동영상이 포함된 키트를 제공하여 오사용에 대한 불만을 줄이고 있습니다. 프리컷 제품은 두 가지 요구를 모두 충족하고 경기 도중 신속성을 강조하는 운동 트레이너에 의해 뒷받침됩니다. 지속적인 제품 교육은 여전히 중요하며 부적절한 장력은 치료 효과를 저하시키기 때문에 대부분의 제품 출시 시 인증 과정이 병행되어야 합니다.

혁신의 초점은 근막의 활주를 모방하는 독특한 물결 모양 접착 패턴에 있습니다. 예를 들어 뮐러사의 타이푼 라인은 기존의 면 소재와 전단 응력을 분산시키는 정현파 모양의 접착제 융기를 융합시키고 있습니다. 비교 시험에서 주요 브랜드는 5일 후에 70%의 접착률을 유지했지만 저가 제품은 35%에 그쳤습니다. 이해관계자가 효과와 보험 환급을 연결하는 가운데, 입찰평가에서 검증의 영향력이 확대되고 있습니다.

2025년 시점의 키네시오 테이프 시장에서 통기성과 피부 자극이 낮은 면 소재가 63.05%의 점유율을 차지했습니다. 클리닉에서는 수술 후 장기 장착 시 선호되며 발한량이 적고 환자의 쾌적성이 최우선시되는 상황에서 도입되고 있습니다. 한편, 나일론 및 스판덱스 혼방 등의 합성 소재는 속건성과 흐트러짐 방지성 및 샤워나 격렬한 트레이닝 시의 탄성 유지를 이유로 CAGR 6.11%로 확대 중입니다. 수영 경기 연맹에서는 경기용 키트에 합성 테이프를 지정하는 움직임이 확산되어 수요 순환이 강화되고 있습니다. 천연섬유와 폴리에스테르를 혼합한 하이브리드 구조는 쾌적성과 내구성의 양립을 목표로 하고 있습니다. 실리콘 안감 유형은 저알레르기성이 비용보다 우선시되는 종양과 병동에서 도입이 진행되고 있습니다.

소재 선정은 치료자의 부담에도 영향을 미칩니다. 깨끗하게 벗겨지는 테이프는 재부착 시간을 단축하고, 외래 진료소에서는 이 지표를 추적하고 있습니다. ISO 10993에 따른 규제 조화는 투명한 생체적합성 데이터 제출을 공급업체에게 촉구하고 종합적인 시험 자금을 조달할 수 있는 대기업을 간접적으로 우대하는 결과를 낳고 있습니다.

지역별 분석

북미는 2025년 보험 적용 범위 내에서 치료되는 대학 스포츠 부상을 배경으로 키네시오 테이프 시장에서 41.76%의 점유율을 차지하여 매출을 견인했습니다. 미국 프로 리그는 대량 조달을 실시하고 2024년의 OSHA 재분류에 의해 직장 현장에서의 사용이 용이하게 되었습니다. 캐나다에서는 공공 물리치료 프로그램이 수술 후 부종에 대한 테이프 사용을 환급하기 때문에 유사한 동향이 나타나고 있습니다.

유럽은 증거 기반 실천을 지원하는 견조한 임상 조사 실적으로 이어집니다. 독일의 질병보험기금은 특정 정형외과 프로토콜에서 테이프 사용을 환급 대상으로 하고 프랑스에서는 에시티사가 2024년 11월에 현지 수요에 대응하는 운동 라인을 추가함으로써 제조 거점이 되었습니다. 영국에서는 물리치료사가 국민보건서비스(NHS) 지역 재활에 테이핑을 통합하고 있지만, 효과 검증은 보다 엄격합니다.

아시아태평양은 가장 빠르게 확대되는 지역으로, 2031년까지 연평균 복합 성장률(CAGR) 6.80%로 추이할 것으로 예측됩니다. 중국에서는 스포츠 참여율 상승과 정부 건강 증진 정책에 따라 외래 재활이 급성장하고 있습니다. 일본에서는 고령화에 따라 가동성 서포트로서 테이핑이 이용되고, 보험사는 림프부종의 적응증에 대해서 일부를 보상하고 있습니다. 인도와 동남아시아에서는 전자상거래 플랫폼이 물리치료용 액세서리와 지도 컨텐츠를 세트로 판매함으로써 소매주도의 성장이 나타나고 있습니다.

라틴아메리카에서는 중간 정도의 보급이 나타나고 있습니다. 브라질의 스포츠 의학 시장은 축구로 인한 부상으로 인해 혜택을 누리고 있으며, 멕시코 사립 병원에서는 전 십자인대 재건술 치료 과정에 테이핑을 추가했습니다. 중동 및 아프리카는 여전히 개발도상국이지만, 대규모 이벤트 관련 인프라와 연동한 사설 스포츠 클리닉에서 도입이 진행되고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 스포츠 부상의 유병률 및 운동 인구 증가

- 물리치료사 및 병원에 의한 임상 도입

- 전자상거래의 침투와 소비자용 직접 판매

- 원격 재활 키트의 통합

- 림프 부종 및 종양 재활에서의 새로운 치료 용도 전개

- 첨단 지속가능 저자극성 소재

- 억제요인

- 임상적 효능에 관한 증거 불충분

- 대체 서포트 기기 및 치료법과의 경쟁

- 과대 치료 효과 주장에 대한 규제 당국의 단속 강화

- 비용 구조에 영향을 미치는 면화 가격의 변동

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 롤

- 프리컷 스트립

- 프리쉐이핑

- 재료별

- 면

- 합성 섬유(폴리에스테르, 나일론)

- 하이브리드 및 기타

- 최종 사용자별

- 병원 및 클리닉

- 스포츠 팀 및 선수

- 재활 및 물리치료 센터

- 재택 치료 환경

- 용도별

- 근골격계의 통증 관리

- 스포츠 부상의 예방과 회복

- 수술 후 관리 및 림프 부종 관리

- 자세 교정

- 신경 질환 및 소아과 용도

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- KT Health LLC

- Kinesio Holding Corporation

- SpiderTech Inc.

- Nitto Denko Corporation

- Mueller Sports Medicine Inc.

- 3B Scientific GmbH

- Performance Health Holding Inc.

- DL Medical & Health Co. Ltd.

- Jaybird & Mais Inc.

- BSN medical GmbH(Essity)

- Sporttape Ltd

- Aupcon Medical Technology Co. Ltd

- TMAXTape Co. Ltd

- Cramer Products Inc.

- 3M Company

- Johnson & Johnson Consumer Inc.

- Ossur hf

제7장 시장 기회 및 미래 전망

CSM 26.01.28The kinesio tape market size in 2026 is estimated at USD 319.22 million, growing from 2025 value of USD 295.18 million with 2031 projections showing USD 471.63 million, growing at 8.15% CAGR over 2026-2031.

Continued evidence for therapeutic efficacy and a widening range of musculoskeletal, lymphatic, and neurological applications propel demand across clinical, athletic, and home-care settings. Institutional buying remains strong as physiotherapy clinics standardize taping protocols for post-operative edema control, while consumer adoption accelerates through e-commerce channels that simplify access and education. North America keeps its revenue lead on the back of entrenched sports medicine ecosystems, yet Asia-Pacific registers the fastest unit expansion as disposable incomes climb and outpatient rehabilitation capacity grows. Competition now turns on material science and training services, with vendors differentiating through longer-lasting synthetic blends and accredited practitioner programs that underscore correct application.

Global Kinesio Tape Market Trends and Insights

Sports Injury Prevalence & Rising Athlete Population

Escalating sports participation fuels the kinesio tape market as musculoskeletal injuries mount across youth and professional cohorts. Track-and-field logged 128,761 lower-extremity cases from 2014-2023, with sprains and strains making up nearly half the incidents. Soccer added 843,063 lower-extremity injuries in the same span, intensifying demand for non-restrictive recovery aids. High-visibility use during the 2024 Paris Games normalized taping on elite athletes and spurred consumer curiosity.

Clinical Adoption by Physiotherapists & Hospitals

Meta-analyses show taping can temper knee edema and pain after total knee arthroplasty while improving post-stroke dysphagia outcomes, nudging hospitals to integrate it into bundled rehabilitation programs. OSHA's 2024 guidance classifying kinesio tape as first-aid treatment reduced administrative hurdles in occupational settings. Randomized trials on finger injuries demonstrated superior range of motion and comfort versus rigid splints, further reinforcing clinician confidence. Such findings widen payer acceptance and strengthen formulary inclusion within outpatient networks.

Inconclusive Clinical Efficacy Evidence

Several meta-analyses underscore pain relief yet note negligible gains in knee function or proprioception, leading guideline committees to issue cautious recommendations. Scholars argue placebo components may influence outcomes, and reviewers call for larger randomized designs to delineate mechanisms conclusively.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Penetration & Direct-to-Consumer Sales

- Tele-rehabilitation Kit Integration

- Competition from Alternative Support Devices & Treatments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rolls maintained 46.28% kinesio tape market share in 2025 by offering clinicians control over cut length and stretch. The format aligns with bulk procurement budgets in hospitals and sports franchises. Pre-shaped designs, however, are rising at a 5.92% CAGR as therapists seek anatomical exactness for complex joints and as consumers demand error-proof kits. Top brands bundle QR-code videos that illustrate placement paths, reducing misuse complaints. Pre-cut strips straddle the two states, appealing to athletic trainers who value speed during games. Continuous product education remains vital: improper tension reduces therapeutic lift, underscoring why accredited courses accompany most launches.

Innovation centers on proprietary adhesive wave patterns claimed to mirror fascia glide. Mueller's Typhoon line, for example, marries conventional cotton with sinusoidal glue ridges said to dissipate shear stress. Comparative tests reported 70% adhesion retention after five days for leading brands versus 35% for economy offerings. As stakeholders link performance to reimbursement, verification labs gain influence in tender awards.

Cotton commanded 63.05% of the kinesio tape market size in 2025 owing to breathability and skin tolerance. Clinics favor it for longer post-surgical wear when perspiration is lower and patient comfort paramount. Yet synthetics such as nylon-spandex hybrids are scaling at 6.11% CAGR because they dry quickly, resist fray, and maintain elasticity through showers and intense training. Water-sports federations now specify synthetic tapes in competition kits, tightening demand loops. Hybrid constructions, weaving natural fibers with polyester, aim to merge comfort with longevity. Silicone-backed variants appear on oncology wards where hypoallergenic imperatives outweigh cost.

Material selection also influences therapist workload: tapes that peel cleanly reduce re-dressing time, a metric tracked by outpatient clinics. Regulatory harmonization via ISO 10993 steers suppliers toward transparent biocompatibility dossiers, indirectly favoring larger firms able to fund comprehensive testing.

The Kinesio Tape Market Report is Segmented by Product Type (Rolls, Pre-Cut Strips, Pre-Shaped Applications), Material (Cotton, Synthetic, Hybrid & Others), End User (Hospitals & Clinics, Sports Teams & Athletes, and More), Application (Musculoskeletal Pain Management, Sports Injury Prevention & Recovery, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led revenues with 41.76% kinesio tape market share in 2025 on the strength of collegiate sports injuries treated within insurance coverage frameworks. U.S. professional leagues procure large volumes, and OSHA reclassification in 2024 eased on-site workplace use. Canada mirrors trends through public physiotherapy programs that reimburse tape for post-surgical swelling.

Europe follows with robust clinical research output that feeds evidence-based practice. Germany's sickness funds reimburse tape for specific orthopedic protocols, while France became a manufacturing hub after Essity added an athletics-tape line in November 2024 to serve local demand. United Kingdom physiotherapists integrate taping into National Health Service community rehab, albeit with tighter evidence scrutiny.

Asia-Pacific is the fastest-expanding region, expected to clock a 6.80% CAGR to 2031. China's outpatient rehab boom aligns with rising sports participation and government fitness mandates. Japan's aging population uses tape for mobility support, and insurers partially cover lymphedema indications. India and Southeast Asia exhibit retail-led growth as e-commerce platforms bundle physiotherapy accessories with instructional content.

Latin America adopts moderately; Brazil's sports medicine market benefits from football injury prevalence, while private hospitals in Mexico add taping to ACL reconstruction pathways. The Middle East & Africa remain nascent but see uptake in private sports clinics linked to mega-event infrastructure.

- KT Health LLC

- Kinesio

- SpiderTech Inc.

- Nitto Denko

- Mueller Sports Medicine

- 3B Scientific

- Performance Health Holding Inc.

- DL Medical & Health Co. Ltd.

- Jaybird & Mais Inc.

- BSN medical GmbH (Essity)

- Sporttape Ltd

- Aupcon Medical Technology Co. Ltd

- TMAXTape Co. Ltd

- Cramer Products Inc.

- 3M

- Johnson & Johnson Consumer Inc.

- Ossur hf

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sports Injury Prevalence & Rising Athlete Population

- 4.2.2 Clinical Adoption By Physiotherapists & Hospitals

- 4.2.3 E-Commerce Penetration & Direct-To-Consumer Sales

- 4.2.4 Tele-Rehabilitation Kit Integration

- 4.2.5 Emerging Therapeutic Uses In Lymphedema & Oncology Rehab

- 4.2.6 Advanced Sustainable Hypoallergenic Materials

- 4.3 Market Restraints

- 4.3.1 Inconclusive Clinical Efficacy Evidence

- 4.3.2 Competition From Alternative Support Devices & Treatments

- 4.3.3 Regulatory Crackdown On Overstated Therapeutic Claims

- 4.3.4 Volatile Cotton Prices Affecting Cost Structure

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Rolls

- 5.1.2 Pre-cut Strips

- 5.1.3 Pre-shaped Applications

- 5.2 By Material

- 5.2.1 Cotton

- 5.2.2 Synthetic (Polyester, Nylon)

- 5.2.3 Hybrid & Others

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Sports Teams & Athletes

- 5.3.3 Rehabilitation & Physiotherapy Centers

- 5.3.4 Home-care Settings

- 5.4 By Application

- 5.4.1 Musculoskeletal Pain Management

- 5.4.2 Sports Injury Prevention & Recovery

- 5.4.3 Post-operative & Lymphedema Management

- 5.4.4 Posture Correction

- 5.4.5 Neurological & Pediatric Uses

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, and Recent Developments)

- 6.3.1 KT Health LLC

- 6.3.2 Kinesio Holding Corporation

- 6.3.3 SpiderTech Inc.

- 6.3.4 Nitto Denko Corporation

- 6.3.5 Mueller Sports Medicine Inc.

- 6.3.6 3B Scientific GmbH

- 6.3.7 Performance Health Holding Inc.

- 6.3.8 DL Medical & Health Co. Ltd.

- 6.3.9 Jaybird & Mais Inc.

- 6.3.10 BSN medical GmbH (Essity)

- 6.3.11 Sporttape Ltd

- 6.3.12 Aupcon Medical Technology Co. Ltd

- 6.3.13 TMAXTape Co. Ltd

- 6.3.14 Cramer Products Inc.

- 6.3.15 3M Company

- 6.3.16 Johnson & Johnson Consumer Inc.

- 6.3.17 Ossur hf

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment