|

시장보고서

상품코드

1906121

압출 폴리스티렌 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Extruded Polystyrene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

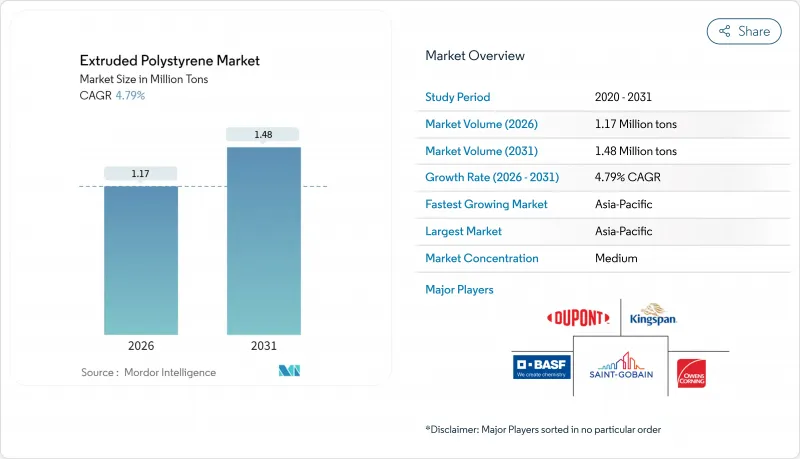

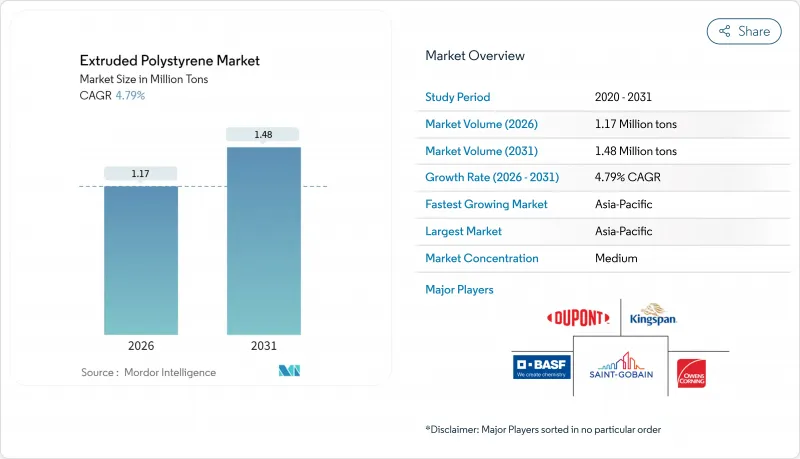

압출 폴리스티렌 시장은 2025년 112만 톤으로 평가되었으며, 2026년 117만 톤에서 2031년까지 148만 톤에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 4.79%로 전망됩니다.

이러한 성장은 대체 발포체 대비 우수한 내열성과 내습성을 제공하는 재료의 독립 기포 구조에 의해 뒷받침됩니다. 수량 증가는 세계 건설 활동의 가속화, 에너지 효율 규제 강화, 오래된 건축물의 개보수 수요 증가와 관련이 있습니다. 또, 옥상 설비를 지원하는 압축 강도 및 장기적인 에너지 손실을 줄이는 치수 안정성 등의 제품 특성도 경쟁 우위성의 요인입니다. 또한, 지구온난화계수가 낮은 발포제에 대한 전략적 주력은 기후규제의 강화 하에서도 장기적인 수요의 지속성을 강화할 전망입니다.

세계의 압출 폴리스티렌 시장의 동향 및 인사이트

에너지 절약 건축물에 대한 수요 증가

정부 및 유틸리티자의 인센티브로 고단열성능(고R-밸류)의 단열재에 대한 투자회수 효과가 확대되고 건축가는 벽과 지붕 및 기반에 압출 폴리스티렌 보드를 도입하는 경향이 강해지고 있습니다. 국제 에너지 절약 기준(IECC)에서 요구하는 연속 단열재는 열교를 최소화해야 하는 상업 건축물의 외피로의 도입을 촉진하고 있습니다. 건물 소유자는 초기 비용을 건물의 수명 내내 신뢰할 수 있는 에어컨 시설(HVAC)의 절약 효과와 연결합니다. 대량의 물이나 수증기 확산에 대한 내성에 의해 습윤 기후 하에서도 시공 후의 단열 성능이 유지됩니다. LEED v4 등의 인증 제도는 건물 전체의 에너지 성능을 소재 선정과 연결함으로써 장기적인 수요를 지원하고 있습니다. 에너지망의 탈탄소화가 진행되고 있는 가운데, 단열재는 여전히 주요한 저비용 효율화 대책이며, 보다 대규모의 개보수 범위를 촉진하고 있습니다.

급속한 도시화와 인프라 확장

아시아태평양의 도시 인구는 매년 수백만 명 가량 증가를 지속하여 고층 주택, 대규모 교통 거점, 상업 지구의 건설을 촉진하고 있으며, 이들은 견고한 외피 단열재를 요구합니다. 중국과 인도의 인프라 계획이 지역 소비를 지원하는 반면 동남아시아의 스마트 시티 프로젝트는 압출 폴리스티렌 시장 진출기업의 설계 도입 사례를 증가시키고 있습니다. 중산층 소비자가 요구하는 열적 쾌적성에 의해 건축 기준의 책정자는 최저 단열 성능치(R-밸류)의 향상을 추진하고 있습니다. 인도네시아와 필리핀의 공공 주택 계획에서는 기존에는 고급 프로젝트에만 적용된 단열 지침이 채택되었습니다. 이러한 장기적인 동향으로 인해 압출 폴리스티렌 시장은 급속한 건설 붐이 일어나는 지방 도시로 확대되고 있습니다.

친환경 단열재 대체품의 점유율 확대

라이프사이클 영향을 기준으로 하는 그린 빌딩 프로젝트에서는 목재 섬유판과 재생 셀룰로오스 단열재가 사양서에 채택되었습니다. 유럽의 플라스틱 폐기물 규제 강화는 바이오 솔루션 수요를 뒷받침하고 일부 건축가는 화석 유래 제품을 기피하고 있습니다. 순환형 경제 정책은 재활용을 촉진하고 재활용성이 입증된 단열 시스템을 유리하게 만듭니다. 이러한 변화는 여전히 고급 부문에 집중되어 있지만 생산 규모가 확대됨에 따라 비용 곡선이 개선되고 있습니다. 압출 폴리스티렌 공급업체는 환경 인증을 강화하기 위해 회수 프로그램 및 바이오 발포제에 대한 투자로 대응하고 있습니다.

부문 분석

2025년 압출 폴리스티렌 시장 점유율의 61.50%를 보드가 차지하였으며 구조적 강도와 보행성이 중요한 지붕과 벽 및 기초 구조에서의 범용성을 뒷받침하고 있습니다. 건축업자가 내압 강도와 밀폐 셀 구조에 의한 내습성을 중시하는 경향이 강해지는 가운데, 보드 부문의 압축 폴리스티렌 시장 내 규모는 계속 확대되고 있습니다. 한편, 패널은 현장 작업을 효율화하는 조립식 건축에 대한 적합성을 배경으로 2031년까지 연평균 복합 성장률(CAGR) 4.86%로 성장할 것으로 전망되고 있습니다.

블록은 두께 요구사항이 기존 보드의 한계를 초과하는 둘레 기초 공사 및 지하 방수에서 여전히 틈새 애플리케이션입니다. 파이프 섹션은 기계실 및 공정 산업의 단열재로 활용되며 콜드체인 확장과 관련된 새로운 기회를 제공합니다. 제품 혁신은 현재 밀착성을 높이는 엣지 프로파일과 다층 지붕 시스템의 접착력을 향상시키는 표면 텍스처에 초점을 맞추었습니다.

압출 폴리스티렌 보고서는 제품 유형(보드, 패널, 블록, 파이프 섹션), 용도(지붕 단열재, 벽 단열재 등), 최종 사용자 산업(주택, 상업, 인프라), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년에 세계 시장의 44.20%를 차지하였고 견조한 도시화, 인프라 대규모 프로젝트, 정부 주택 정책을 배경으로 2031년까지 연평균 복합 성장률(CAGR) 4.93%로 추이할 것으로 예측됩니다. 중국의 '일대일로' 구상은 참여국에 파급 수요를 만들어 내고, 인도의 '스마트 시티 구상'은 단열 사양을 높이는 에너지 절약 기준을 포함하고 있습니다.

북미에서는 캐나다와 미국에서의 건축 기준의 개정에 의해 신축 건물에 대한 지붕 및 벽의 단열 성능(R-밸류) 향상 의무화가 진행되고 있습니다. 외피 개선을 대상으로 한 유틸리티의 리베이트 프로그램 확충에 수반하여 개보수 활동이 활발해지고 있습니다. 전자상거래에 의한 식품 택배의 보급이 냉장창고 건설을 가속시켜 산업용 부동산에서의 제품 수요를 뒷받침하고 있습니다. 본 지역의 압출 폴리스티렌 시장은 스티렌 가격 변동에 대응할 수 있는 수직 통합형 제조업체를 중심으로 통합이 진행되고 있습니다.

유럽에서는 건설량 증가가 둔화되고 있지만, 엄격한 에너지 성능 규제와 대규모 개보수 프로젝트에 대한 공적 자금 지원에 의해 여전히 큰 기반을 유지하고 있습니다. 대체 단열재의 도입이 점진적으로 점유율을 압박하는 한편, 압출 폴리스티렌은 내수성 특성으로 지하 구조물이나 역구배 지붕 용도로는 여전히 주류입니다. 제조업체 각사는 지역의 재활용 의무에 준거한 순환형 경제의 회수 프로그램을 운영하고 있으며 이에 의해 지속가능성을 중시하는 건설업자가 사양을 우선시하도록 하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 에너지 절약 건축물에 대한 수요 증가

- 급속한 도시화와 인프라 확장

- 단열재를 의무화하는 엄격한 건축 기준

- 생물제제 및 온라인 식료품용 콜드체인 창고에 대한 수요 급증

- 오프사이트 및 모듈 건축 시스템의 보급

- 억제요인

- 친환경 단열재 대체품의 점유율 확대

- 원료(스티렌) 가격의 변동성

- 키갈리 협정에 근거한 HFC 발포제 규제

- 밸류체인 분석

- Porter's Five Forces

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 보드

- 패널

- 블록

- 파이프 섹션

- 용도별

- 지붕 단열재

- 벽 단열재

- 기타(바닥, 지하실, 중공, 둘레)

- 최종 사용자 업계별

- 주택

- 상업

- 인프라

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 순위 분석

- 기업 프로파일

- Austrotherm

- BASF

- DuPont

- Emirates Extruded Polystyrene LLC

- JACKON Insulation GmbH

- Kingspan Group

- Knauf Insulation

- Owens Corning

- Polyfoam XPS

- Saint-Gobain

- Soprema Group

- Supreme Petrochem Ltd.

- Synthos

- TECHNONICOL

- URSA

제7장 시장 기회 및 미래 전망

CSM 26.01.28The Extruded Polystyrene Market was valued at 1.12 million tons in 2025 and estimated to grow from 1.17 million tons in 2026 to reach 1.48 million tons by 2031, at a CAGR of 4.79% during the forecast period (2026-2031).

This growth rests on the material's closed-cell structure, which delivers superior thermal resistance and moisture tolerance compared with alternative foams. Volume gains track the acceleration of global construction activity, the hardening of energy-efficiency mandates, and mounting renovation demand in mature building stocks. Competitive advantages also stem from the product's compressive strength, which supports rooftop equipment, and from its dimensional stability, which reduces long-term energy loss. Strategic focus on low-global-warming-potential blowing agents further reinforces long-range demand resilience under tightening climate regulations.

Global Extruded Polystyrene Market Trends and Insights

Growing Demand for Energy-Efficient Buildings

Government and utility incentives amplify the payback of high-R-value insulation, steering architects toward extruded polystyrene boards for walls, roofs, and foundations. Continuous insulation requirements in the International Energy Conservation Code elevate adoption in commercial envelopes where thermal bridging must be minimized. Building owners associate the material's higher upfront cost with reliable HVAC savings over building life. Resilience to bulk water and vapor diffusion protects installed R-value in humid climates. Certification schemes such as LEED v4 link whole-building energy performance to material selection, sustaining long-term demand. As energy grids decarbonize, insulation remains a primary low-cost efficiency measure, encouraging deeper retrofit scopes.

Rapid Urbanization and Infrastructure Expansion

Asia-Pacific's urban population adds millions of residents each year, driving high-rise housing, mass-transit stations, and commercial districts that specify robust envelope insulation. China's and India's infrastructure programs anchor regional consumption, while Southeast Asian smart-city projects multiply design wins for extruded polystyrene market participants. Middle-class consumer expectations for thermal comfort encourage code writers to raise minimum R-values. Public housing schemes in Indonesia and the Philippines adopt insulation guidelines that previously applied only to premium projects. These secular forces extend the extruded polystyrene market footprint into second-tier cities that are experiencing rapid construction booms.

Eco-Friendly Insulation Substitutes Gaining Share

Wood-fiber boards and recycled cellulose insulation win specifications in green building projects that benchmark lifecycle impacts. European regulatory pressure on plastic waste bolsters demand for bio-based solutions, nudging some architects away from fossil-derived foams. Circular-economy policies promote material reuse, which favors insulation systems with demonstrated recyclability. These shifts are still concentrated in premium segments, yet cost curves are improving as production scales. Extruded polystyrene suppliers counteract by investing in take-back programs and bio-sourced blowing agents to shore up environmental credentials.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Building Codes Mandating Thermal Insulation

- Cold-Chain Warehousing Boom for Biologics and E-Grocery

- Kigali-Driven HFC Blowing-Agent Restrictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Boards accounted for 61.50% of the extruded polystyrene market share in 2025, underscoring their versatility across roofs, walls, and foundations, where structural integrity and walkability are critical. The extruded polystyrene market size tied to boards continues to rise as builders prioritize compressive strength and closed-cell moisture resistance in exposed conditions. Panels, meanwhile, are projected to register a 4.86% CAGR to 2031, benefiting from their suitability for prefabricated assemblies that streamline onsite labor.

Blocks remain a niche for perimeter foundations and below-grade waterproofing where thickness needs exceed conventional board limits. Pipe sections serve mechanical room and process-industry insulation, capturing emerging opportunities in cold-chain expansion. Product innovation now centers on edge profiles that promote tight interlocks and on surface textures that improve adhesion in multi-layer roof systems.

The Extruded Polystyrene Report is Segmented by Product Type (Boards, Panels, Blocks, and Pipe Sections), Application (Roof Insulation, Wall Insulation, and Others), End-User Industry (Residential, Commercial, and Infrastructure), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa, ). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific held 44.20% of global volume in 2025, and the region is projected to log a 4.93% CAGR through 2031 on the back of robust urbanization, infrastructure megaprojects, and government housing programs. China's Belt and Road Initiative generates spill-over demand in participating nations, while India's Smart Cities Mission embeds energy-efficiency standards that elevate insulation specifications.

North America is buoyed with code updates in Canada and the United States mandating higher R-values for roofs and walls in new builds. Renovation activity picks up as utilities expand rebate programs targeting envelope improvements. Cold-storage construction accelerates due to strong e-grocery adoption, reinforcing product pull-through in industrial real estate. The extruded polystyrene market in this region remains consolidated around vertically integrated producers able to navigate styrene price swings.

Europe maintains a sizable base despite slower construction volume growth, supported by strict energy-performance legislation and public funding for deep-renovation projects. Adoption of alternative insulation materials exerts gradual share pressure; however, extruded polystyrene still dominates below-grade and inverted-roof applications because of its water-resistance profile. Manufacturers operate circular-economy take-back programs to align with regional recycling mandates, which helps preserve specification preference among sustainability-conscious builders.

- Austrotherm

- BASF

- DuPont

- Emirates Extruded Polystyrene L.L.C.

- JACKON Insulation GmbH

- Kingspan Group

- Knauf Insulation

- Owens Corning

- Polyfoam XPS

- Saint-Gobain

- Soprema Group

- Supreme Petrochem Ltd.

- Synthos

- TECHNONICOL

- URSA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for energy-efficient buildings

- 4.2.2 Rapid urbanization and infrastructure expansion

- 4.2.3 Stringent building codes mandating thermal insulation

- 4.2.4 Cold-chain warehousing boom for biologics and e-grocery

- 4.2.5 Uptake of off-site modular construction systems

- 4.3 Market Restraints

- 4.3.1 Eco-friendly insulation substitutes gaining share

- 4.3.2 Raw-material (styrene) price volatility

- 4.3.3 Kigali-driven HFC blowing-agent restrictions

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Boards

- 5.1.2 Panels

- 5.1.3 Blocks

- 5.1.4 Pipe Sections

- 5.2 By Application

- 5.2.1 Roof Insulation

- 5.2.2 Wall Insulation

- 5.2.3 Others (Floor, Basement, Cavity and Perimeter)

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastruture

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Austrotherm

- 6.4.2 BASF

- 6.4.3 DuPont

- 6.4.4 Emirates Extruded Polystyrene L.L.C.

- 6.4.5 JACKON Insulation GmbH

- 6.4.6 Kingspan Group

- 6.4.7 Knauf Insulation

- 6.4.8 Owens Corning

- 6.4.9 Polyfoam XPS

- 6.4.10 Saint-Gobain

- 6.4.11 Soprema Group

- 6.4.12 Supreme Petrochem Ltd.

- 6.4.13 Synthos

- 6.4.14 TECHNONICOL

- 6.4.15 URSA

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Innovations in Extruded Polystyrene Manufacturing