|

시장보고서

상품코드

1906133

폴리트리메틸렌 테레프탈레이트 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Polytrimethylene Terephthalate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

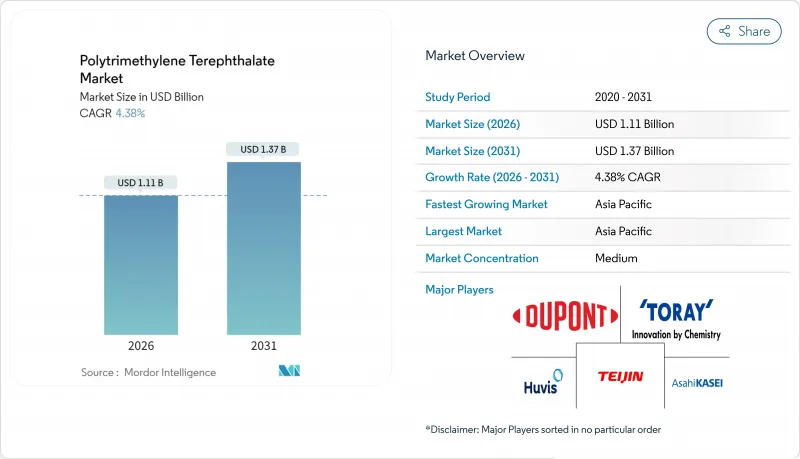

폴리트리메틸렌 테레프탈레이트 시장은 2025년 10억 6,000만 달러로 평가되었고, 2026년 11억 1,000만 달러로 평가되었고, 2031년까지 13억 7,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 4.38%를 나타낼 전망입니다.

이 완만한 성장세는 폴리머가 일반 PET와 고급 엔지니어링 플라스틱을 연결하는 능력에서 비롯되며, 95% 이상의 탄성 회복력, 선명한 염료 흡수력, 내재된 얼룩 방지 기능을 제공합니다. 편안한 신축성 의류에 대한 수요 증가, 카펫 생산량 확대, 지속가능성 요구 강화는 아시아태평양, 북미, 유럽 지역에서 꾸준한 물량 증가를 지속적으로 뒷받침하고 있습니다. 지속적인 역풍으로는 PET 대비 20-30% 높은 생산 비용, 1,3-프로판디올 원료 가격 변동성, 화학 재활용 공정 확장에 나서는 PET 및 PBT 생산업체들의 공고한 경쟁 등이 있습니다. 그럼에도 2025년 1월부터 시행되는 섬유용 PFAS 코팅 금지 조치는 PTT의 내재적 얼룩 방지 기능을 상업적으로 더욱 매력적으로 만들어 가치 제안을 높입니다.

세계의 폴리트리메틸렌 테레프탈레이트 시장 동향 및 인사이트

신축성과 편안함을 결합한 섬유에 대한 섬유 수요 증가

세계의 액티브웨어 및 애슬레저 브랜드들은 PTT 섬유가 일반 폴리에스터보다 신축 후 원래 길이로 복원되는 신뢰성이 높아 의류의 수명과 착용감을 연장하기 때문에 PTT를 지정하고 있습니다. 아시아 직물 공장들은 PTT와 스판덱스를 혼합하기 위한 전용 라인을 확장 중이며, 중국의 주요 공장들은 고탄성 니트 직물에 대해 두 자릿수 주문 증가율을 보고하고 있습니다. Teijin Frontier의 다기능 폴리에스터 직물 라인은 PTT가 편안함을 저해하지 않으면서 자외선 차단 및 통기성 마감 처리와 어떻게 결합될 수 있는지 보여줍니다. 소매업체들이 마진이 높은 기능성 의류로 상품 구성을 전환함에 따라 가격에 민감한 부문에서도 채택이 가속화되고 있습니다.

바이오 기반 및 재활용 가능한 폴리에스터를 향한 지속가능성 추진

PTT는 1,3-프로판디올 성분이 옥수수 포도당에서 유래될 경우 31%의 바이오 함량을 달성할 수 있으며, 이는 듀폰이 2015년부터 이미 상용화한 방식입니다. EU와 미국의 범주 3 배출량에 대한 정책적 압박으로 의류 그룹들은 15-20%의 프리미엄에도 불구하고 바이오 기반 등급에 대한 다년간 구매 계약을 체결하고 있습니다. 노바 연구소(nova-Institut)는 2023년 바이오 폴리머 생산 능력을 440만 톤으로 추정했으며, 연간 17% 성장할 것으로 전망했습니다. PTT는 이 중 상업화된 아로마틱 폴리에스터 중 하나입니다. 화학 재활용업체들은 현재 PET와 PTT를 함께 처리하는 효소 분해 중합 분해 기술을 시험 중이며, 이는 복잡한 분류 과정 없이 순환 경제 옵션을 열어줍니다.

높은 생산 비용

생물학적 1,3-프로판디올은 석유화학 유래 에틸렌글리콜보다 여전히 25-30% 비싸며, 특히 대중 시장 티셔츠 및 포장재 분야에서 PET 소재와의 비용 경쟁력을 저해합니다. 제한된 공장 규모(연간 20만 톤을 초과하지 않음)로 인해 고정 비용 분산이 제한됩니다. 2024년까지 아시아 올레핀 마진이 축소되면서 특수 폴리머 경제성이 더욱 압박받고 있습니다. 이에 PTT 공급업체들은 마진 방위를 위해 고성능 스포츠웨어, 카펫, 엔지니어링 컴파운딩과 같은 프리미엄 틈새 시장을 공략하고 있습니다.

부문 분석

석유 기반 등급은 2025년 폴리트라이메틸렌 테레프탈레이트 시장에서 66.05%의 점유율을 유지하며 확고한 공급망과 상대적 비용 우위를 반영했습니다. 그러나 브랜드 소유자들이 2030년까지 폴리에스터의 재생 가능 함량을 25-50%로 확대하기로 약속함에 따라 바이오 기반 생산량은 연평균 5.29% 성장률(CAGR)로 확대되고 있습니다. 이러한 변화로 인해 바이오 등급 폴리트리메틸렌 테레프탈레이트 시장 규모는 전체 산업 수요보다 가파른 성장 곡선을 유지하고 있습니다. 발효 공정 개선으로 2023년 이후 바이오-PDO 단위 비용이 12% 감소했으며, 글리세롤의 부가적 활용으로 순 원료 비용이 낮아졌습니다. 이 부문 매출 증가는 탄소 집약도 공개 규정이 친환경 프리미엄 제품의 경제적 수익률을 높이는 EU와 미국에서 가장 두드러집니다.

효소 재활용 설비에 대한 병행 투자를 통해 재활용 및 바이오 기반 PTT를 혼합하면서도 실의 인장 강도를 저하시키지 않는 하이브리드 펠릿 생산이 가능해졌습니다. 생산사들은 시장 신호에 따라 바이오 원료 비중을 유연하게 조정할 수 있어 옥수수 가격 변동 위험을 헤지하는 방안으로 이 경로를 보고 있습니다. 2028년까지 연간 생산량이 40만 톤에 도달하면, 이해관계자들은 운영 규모 확대를 통해 석유계 PTT와의 가격 격차를 좁혀 폴리트리메틸렌 테레프탈레이트 시장의 장기적 지속가능성 논리를 강화할 것으로 기대합니다.

지역별 분석

아시아태평양은 2025년에 폴리트리메틸렌 테레프탈레이트 시장 수익의 60.20%를 차지하며, 중국의 거대한 실방적 기반과 지역 내 트라이 엑스터 카펫 라인의 급속한 보급에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 5.21%로 추이할 것으로 예측되고 있습니다. 2024년 장쑤성에서 가동을 시작한 중국 석유화공(시노펙)의 300만 톤 PTA 플랜트는 업스트림 부문의 견고한 기반이 지속되고 있음을 나타내며 통합형 PTT 제조업체에 대한 테레프탈산의 안정적인 공급을 보장합니다. 일본의 섬유 제조업체는 초극세 필라멘트용 정밀 방사 기술을 중시하는 한편, 한국의 수지 공급자는 바이오 원료의 통합을 추진해, 지역의 리더십을 지지하고 있습니다.

북미는 여전히 두 번째 생산 기지이며 듀폰의 트라이 엑스터 카펫의 실적과 주택 소유자의 PFAS 프리로 손질이 용이한 바닥재로의 이행이 기반이 되고 있습니다. 미국의 바닥재 제조업체는 PTT 벌크 연속 장섬유 전용 압출 설비를 신설해, 유통 체인에서는 반려동물 사육 가구에 소구하는 성능 보증 프로그램 하에서 해당 섬유를 판매하고 있습니다.

유럽은 정책 주도적 수요 증가를 반영하며, 에코디자인 지침과 생산자 책임 확대 제도가 저탄소 소재 수요를 높이고 있습니다. 독일과 스칸디나비아의 브랜드들은 과학 기반 목표(SBT) 달성을 위해 바이오 PTT 직물을 지정하고 있으며, 이탈리아의 가공업체들은 럭셔리 패션 하우스를 위해 재생 PTT와 신규 바이오 소재를 혼합하고 있습니다.

남미와 중동 및 아프리카는 아직 초기 도입 단계이지만, 브라질과 이집트의 섬유 수출 증가 추세는 현지 방적업체들이 공급 계약을 체결하면 잠재적 성장 가능성이 있음을 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신축성 및 편안함을 위한 섬유에 대한 의류 수요 증가

- 바이오 기반 및 재활용 가능한 폴리에스터로의 지속가능성 추진

- 트라이엑스타(Triexta)를 활용한 카펫/바닥재 응용 분야 확대

- 프로토타이핑용 3D 프린팅 필라멘트의 폴리트리메틸 렌테레프탈레이트(PTT)의 채택 상황

- 전기자동차용 경량 복합재료 부품에의 응용

- 시장 성장 억제요인

- 높은 생산 비용

- 폴리에틸렌테레프탈레이트(PET) 및 폴리부틸렌테레프탈레이트(PBT) 기존 제조업체와의 경쟁

- 원료 공급의 변동성

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 소스별

- 석유 기반 폴리트리메틸렌 테레프탈레이트(PTT)

- 바이오 기반 폴리트리메틸렌 테레프탈레이트(PTT)

- 용도별

- 의류

- 가정용 섬유 제품

- 산업용 섬유

- 기타 용도(자동차 내장 부품 등)

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Asahi Kasei Corporation

- DuPont

- Huvis

- RTP Company

- Shell plc

- Shenghong Holding Group Co., Ltd.

- Technip Energies NV

- Teijin Limited

- TORAY INDUSTRIES, INC.

- Xianglu Tenglong Group

제7장 시장 기회와 장래의 전망

HBR 26.01.26The Polytrimethylene Terephthalate Market was valued at USD 1.06 billion in 2025 and estimated to grow from USD 1.11 billion in 2026 to reach USD 1.37 billion by 2031, at a CAGR of 4.38% during the forecast period (2026-2031).

This moderate pace comes from the polymer's ability to bridge commodity PET and higher-end engineering plastics, offering elastic recovery above 95%, vivid dye uptake, and inherent stain resistance. Rising demand for comfort-stretch apparel, expanding carpet output, and mounting sustainability mandates continue to underpin steady volume gains in Asia-Pacific, North America, and Europe. Persistent headwinds include 20-30% higher production costs versus PET, feedstock price volatility for 1,3-propanediol, and entrenched competition from PET and PBT producers who are scaling up chemical-recycling routes. Nonetheless, the shift away from PFAS coatings in textiles effective January 2025 lifts the value proposition of PTT by making its built-in stain repellence more commercially attractive.

Global Polytrimethylene Terephthalate Market Trends and Insights

Rising Textile Demand for Stretch-Comfort Fibres

Global activewear and athleisure brands are specifying PTT because the fibre recovers its original length after stretching more reliably than standard polyester, extending garment life and fit. Asian fabric mills are scaling dedicated lines to blend PTT with spandex, and leading mills in China are quoting double-digit order growth for high-elastic knit fabrics. Teijin Frontier's multifunctional polyester fabric range illustrates how PTT can be paired with UV protection and breathability finishes without compromising comfort. As retailers shift merchandising toward higher-margin performance clothing, adoption accelerates even in price-sensitive segments.

Sustainability Push Toward Bio-Based and Recyclable Polyester

PTT can reach 31% bio-content when its 1,3-propanediol component is derived from corn glucose, an approach already commercialised by DuPont since 2015. Policy pressure in the EU and US on Scope 3 emissions is prompting apparel groups to sign multiyear offtake agreements for bio-based grades despite premiums of 15-20%. The nova-Institut estimated bio-polymer capacity at 4.4 million t in 2023, growing 17% annually, with PTT one of the few commercial aromatic polyesters in the mix. Chemical recyclers are now trialling enzymatic depolymerisation that processes PET and PTT together, opening circularity options while avoiding complex sorting.

High Production Costs

Biological 1,3-propanediol remains 25-30% dearer than petrochemically derived ethylene glycol, hampering cost parity with PET fabrics, particularly in mass-market T-shirts and packaging. Limited plant scales-none exceeding 200 ktpa-restrict fixed-cost dilution. Asian olefin margins tightened through 2024, further squeezing specialty polymer economics. PTT suppliers therefore target premium niches such as performance sportswear, carpets, and engineering compounding to defend margins.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Carpet/Flooring Applications Using Triexta

- Polytrimethylene Terephthalate Adoption in 3D Printing Filaments for Prototyping

- Competition from PET and PBT Incumbents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Petro-based grades retained a 66.05% position within the Polytrimethylene Terephthalate market in 2025, reflecting entrenched supply chains and relative cost advantages. Yet bio-based output is expanding at a 5.29% CAGR as brand owners commit to 25-50% renewable content in polyester by 2030. This shift keeps the Polytrimethylene Terephthalate market size for bio grades on a steeper curve than overall industry demand. Fermentation improvements have trimmed unit costs for bio-PDO by 12% since 2023, while side-stream valorisation of glycerol lowers net feedstock expenses. The segment's revenue gains are strongest in the EU and US, where carbon-intensity disclosure rules raise the economic return on green-premium products.

Parallel investments in enzymatic recycling plants enable hybrid pellets that blend recycled and bio-based PTT without compromising yarn tenacity. Producers see the route as a hedge against corn-price swings because bio-feedstock share can flex depending on market signals. Once capacity reaches 400 kt annually by 2028, stakeholders expect operating scale to narrow the price gap with petro-PTT, reinforcing the long-term sustainability narrative of the Polytrimethylene Terephthalate market.

The Polytrimethylene Terephthalate Market Report is Segmented by Source (Petro-Based PTT and Bio-Based PTT), Application (Apparel, Household Textiles, Industrial Fabrics, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured 60.20% of Polytrimethylene Terephthalate market revenue in 2025 and is projected to register a 5.21% CAGR to 2031, propelled by China's vast yarn spinning base and the rapid adoption of Triexta carpet lines in the region. Sinopec's 3 million t PTA plant commissioned in Jiangsu during 2024 signals ongoing upstream strength, ensuring reliable terephthalic acid flows to integrated PTT producers. Japanese fibre makers emphasise precision spinning for ultra-microfilaments, while South Korean resin suppliers push bio-feedstock integration, supporting regional leadership.

North America remains the second-largest cluster, underpinned by DuPont's legacy in Triexta carpets and the migration of residential homeowners toward PFAS-free, easy-clean flooring. US floor-covering mills have installed new extrusion capacity dedicated to PTT bulk-continuous-filament yarns, and distribution chains now market the fibre under performance warranty programmes that resonate with pet-owning households.

Europe reflects a policy-driven pull, with eco-design directives and extended-producer-responsibility schemes elevating demand for low-carbon materials. Brands in Germany and Scandinavia specify bio-PTT fabrics to meet Science-Based Targets, and converters in Italy blend recycled PTT with virgin bio content for luxury fashion houses.

South America and the Middle East and Africa remain early-stage adopters, yet rising textile exports from Brazil and Egypt suggest latent potential once local yarn spinners establish supply agreements.

- Asahi Kasei Corporation

- DuPont

- Huvis

- RTP Company

- Shell plc

- Shenghong Holding Group Co., Ltd.

- Technip Energies N.V.

- Teijin Limited

- TORAY INDUSTRIES, INC.

- Xianglu Tenglong Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Textile Demand for Stretch-Comfort Fibres

- 4.2.2 Sustainability Push Toward Bio-Based and Recyclable Polyester

- 4.2.3 Expansion of Carpet/Flooring Applications using Triexta

- 4.2.4 Polytrimethylene Terephthalate (PTT) Adoption in 3-D-Printing Filaments for Prototyping

- 4.2.5 Use in EV Lightweight Composite Components

- 4.3 Market Restraints

- 4.3.1 High Production Costs

- 4.3.2 Competition from Polyethylene Terephthalate (PET) And Polybutylene Terephthalate (PBT) Incumbents

- 4.3.3 Feed-Stock Supply Volatility

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Source

- 5.1.1 Petro-based Polytrimethylene Terephthalate (PTT)

- 5.1.2 Bio-based Polytrimethylene Terephthalate (PTT)

- 5.2 By Application

- 5.2.1 Apparel

- 5.2.2 Household Textiles

- 5.2.3 Industrial Fabrics

- 5.2.4 Other Applications (Automotive Interior Parts, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Asahi Kasei Corporation

- 6.4.2 DuPont

- 6.4.3 Huvis

- 6.4.4 RTP Company

- 6.4.5 Shell plc

- 6.4.6 Shenghong Holding Group Co., Ltd.

- 6.4.7 Technip Energies N.V.

- 6.4.8 Teijin Limited

- 6.4.9 TORAY INDUSTRIES, INC.

- 6.4.10 Xianglu Tenglong Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment