|

시장보고서

상품코드

1906142

폴리머 코팅 직물 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Polymer Coated Fabric - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

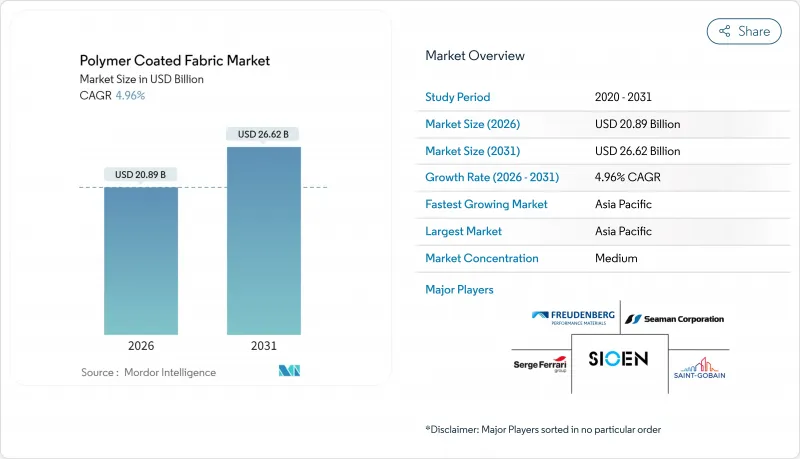

폴리머 코팅 직물 시장의 규모는 2026년에는 208억 9,000만 달러로 추정되며, 2025년 199억 달러에서 성장할 전망입니다.

2031년에는 266억 2,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 4.96%로 성장할 것으로 전망됩니다.

이 전망은 탈탄소화 목표를 달성하면서 보다 엄격한 화학물질 규정을 준수하는 경량 고성능 소재에 대한 지속적인 투자를 반영합니다. 운송 장비의 인테리어, 보호복, 기후 변화에 강한 건축 분야의 수요 집계로 폴리머 코팅 직물 시장은 꾸준한 성장 궤도를 유지하고 있습니다. 제조업체 각사는 내구성과 재활용성을 융합한 코팅 기술을 구사해, 최종 사용자가 라이프사이클 비용과 공개 의무를 충족시키도록 하고 있습니다. 경쟁의 치열성은 중간 정도이지만 전략적 인수, 지역별 생산 능력 확대, PFAS 프리 혁신으로 제품 라인 간의 차별화가 선명해지고 있습니다.

세계의 폴리머 코팅 직물 시장의 동향 및 인사이트

태양광 발전용 플렉서블 백시트 원단에 대한 투자

태양광 자원이 풍부한 경제권에서는 곡면 구조와 경량 구조에 적합한 직물 기반의 태양광 발전이 추진되고 있습니다. PTFE 코팅 유리 섬유 기재는 내후성을 제공해 플렉서블 모듈의 20-25년의 가동 수명을 실현합니다. 이에 의해 건축물 통합형 태양광 외관으로의 도입이 가속하고 있습니다. 중국에서는 섬유산업과 태양광발전의 시너지 효과가 상업규모를 지원하고 EU에서는 건축가가 넷 제로 건축기준을 충족하는 경량 태양막을 지정하고 있습니다.

가볍고 지속 가능한 내장재에 대한 수요 증가

자동차 및 항공우주 OEM 제조업체는 무거운 기재를 폴리머 코팅 직물로 대체함으로써 15-20%의 경량화를 실현하여 직접적인 연비 향상을 도모합니다. 콘티넨탈 AG는 쌀겨 실리카와 천연 고무를 코팅 직물 제품군에 통합하여 재생 가능 필러가 비용 증가 없이 내구성 사양을 충족하는 방법을 실증하고 있습니다.

공급망의 지역화가 국제 무역의 흐름을 변화

지정학적 긴장이 높아지는 가운데 지역 분산형 생산이 촉진되고 대륙을 가로지르는 중복 코팅 라인에 대한 자본 수요가 증가하여 규모의 경제 효과가 축소되고 있습니다. 미국 구매자는 관세 위험을 줄이기 위해 조달 대상을 인도와 동남아시아로 다양화하고 있습니다.

부문 분석

폴리염화비닐(PVC)은 2025년 시점에서 폴리머 코팅 직물 시장의 41.55%를 차지했으며 이는 확고한 비용면 및 가공면의 우위성을 반영하고 있습니다. 그러나, 폴리우레탄은 프탈산에스테르 규제나 재활용 의무에 대한 대응이 진행되는 컨버터에 의해 2031년까지 연평균 복합 성장률(CAGR) 5.88%의 성장이 전망됩니다. 루브리졸사의 ESTANE RNW TPU는 내마모성을 유지하면서 탄소 실적을 59% 저감해 환경친화적인 화학 기술이 틈새에서 주류로 이행하는 실례를 나타내고 있습니다.

실리콘과 폴리에틸렌은 극한 온도 환경과 화학적으로 불활성인 용도에서 전문적인 역할을 유지하는 반면, 바이오 하이브리드 소재는 소비자용 전자기기의 케이스와 고급 액세서리 분야에서 존재감을 높이고 있습니다. 기술 로드맵에 따르면, 주요 공급업체는 코팅 기술 혁신과 기판 디자인을 결합합니다. 프로이덴베르크의 정밀 필라멘트 스펀본드는 얇고 가벼운 멤브레인을 제공하여 용매 흡수량을 줄이고 코팅 라인의 생산성을 향상시킵니다. 이 통합 접근법은 성능 향상이 중합체의 진보와 직물 구조 모두에서 발생함을 보여줍니다.

폴리머 코팅 직물 시장의 보고서는 제품 유형(PVC(폴리염화비닐), 폴리우레탄(PU), 폴리에틸렌 등), 용도(수송 기기, 산업 기기 커버, 지붕 및 차양, 보호복, 가구, 스포츠 및 레저 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분석되고 있습니다. 시장 예측은 금액 기준(달러)으로 제시됩니다.

지역별 분석

아시아태평양은 2025년에 폴리머 코팅 직물 시장의 46.10%를 차지하였고 2031년까지 연평균 복합 성장률(CAGR) 5.72%를 보일 것으로 예측됩니다. 인도의 섬유 산업 진흥 계획(Textile Mission)은 2025년도 예산 6억 2,900만 달러의 지원을 받아 테크니컬 텍스타일의 연구 개발 및 파일럿 코팅 시설에 대해 자금을 할당하고 있습니다. 지하철에서 홍수에 대비한 지붕재에 이르는 공공 인프라 사업으로 생산 능력은 지속적인 코팅 직물 수요로 전환됩니다.

북미에서는 항공우주 및 의료기기 제조업체가 저VOC 및 PFAS 프리 소재를 요구하는 기술 주도형 틈새 시장이 확립되고 있습니다. 전기자동차 생산의 국내 회귀에 의해 시트 천이나 배터리 팩 커버의 현지 조달이 증가하고 있습니다. 트렐레보르사의 러더퍼드 카운티 프로젝트(LEED 인증 취득 예정)에서 나타나듯이 탄소 중립 운영을 목적으로 하는 미국 그린필드 공장에 대해 공급업체의 투자가 진행 중입니다.

유럽은 규제 주도 시장이며, 산업 배출 지침에 따른 무용제 및 수성 코팅이 성장하고 있습니다. OEM 제조업체가 재료의 완전 공개를 중시하는 경향은 인증 취득 공급업체의 우수하고 컴플라이언스를 준수하는 제품에 대해 가격 내성을 창출하고 있습니다. 중동 및 아프리카는 규모가 작지만, 걸프 지역의 기후 변화에 강한 건설 수요와 남아프리카의 산업 다각화를 배경으로 평균을 웃도는 성장을 나타내고 있습니다. 국내 코팅 라인이 한정되어 있기 때문에 지역 서비스 거점에 투자하지 않는 기존 기업에는 아웃소싱 기회가 존재합니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 경량이며 지속 가능한 내장재에 대한 수요 증가

- 아시아태평양에서 제조업계의 보호복 기준 강화

- 기후 변화에 강한 인프라용 건축용 장력 구조물의 급증

- 의료용 가구에서의 항균 코팅 도입

- 플렉서블 PV 백시트 소재에 대한 투자

- 억제요인

- 원유 폴리머 가격의 변동성

- PVC 및 프탈산에스테르류에 대한 환경 규제

- 공급망의 지역화가 세계 무역의 흐름을 저해

- 밸류체인 분석

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 폴리염화비닐(PVC)

- PU(폴리우레탄)

- 폴리에틸렌

- 실리콘

- 기타

- 용도별

- 운송

- 산업용 기기 커버

- 지붕재 및 차양

- 보호복

- 가구

- 스포츠 및 레저

- 기타

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 순위 분석

- 기업 프로파일

- Continental AG

- Cooley Group

- Freudenberg Performance Materials Holding GmbH

- Heytex Gruppe

- OMNOVA North America Inc.

- Saint-Gobain

- Seaman Corporation

- Serge Ferrari Group

- Sioen Industries NV

- SPRADLING INTERNATIONAL GmbH

- SRF Limited

- Trelleborg AB

제7장 시장 기회 및 미래 전망

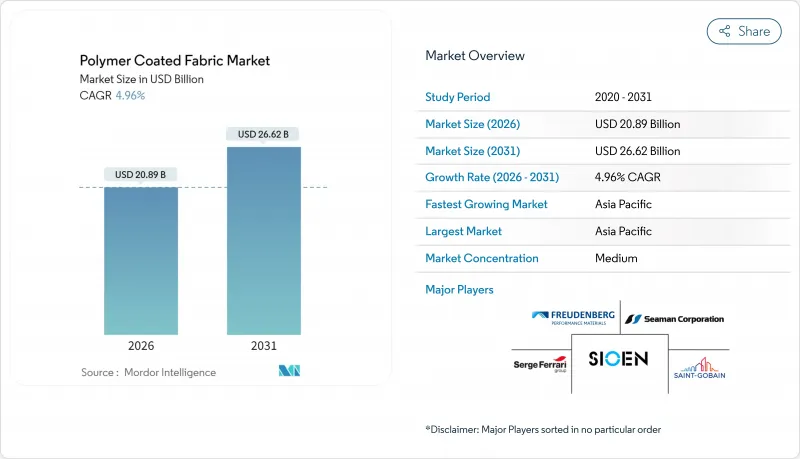

CSM 26.01.28Polymer Coated Fabric Market size in 2026 is estimated at USD 20.89 billion, growing from 2025 value of USD 19.90 billion with 2031 projections showing USD 26.62 billion, growing at 4.96% CAGR over 2026-2031.

The outlook mirrors sustained investments in lightweight, high-performance materials that meet decarbonization targets while complying with more stringent chemical regulations. Demand consolidation in transportation interiors, protective clothing, and climate-resilient construction keeps the polymer coated fabric market on a steady growth track. Producers leverage coating chemistries that fuse durability with recyclability, allowing end-users to meet lifecycle cost and disclosure mandates. Competitive intensity remains moderate, yet strategic acquisitions, regional capacity expansion, and PFAS-free innovation sharpen differentiation across product lines.

Global Polymer Coated Fabric Market Trends and Insights

Investments in Flexible Photovoltaic Back-Sheet Fabrics

Solar-rich economies champion fabric-based photovoltaics that conform to curved or lightweight structures. PTFE-coated glass fiber substrates deliver weather tolerance and enable 20-25-year operating life of flexible modules, accelerating adoption in building-integrated solar facades. Chinese textile-solar synergies underpin commercial scale, while EU architects specify low-mass solar membranes to meet net-zero building codes.

Increasing Demand for Lightweight, Sustainable Interior Materials

Automotive and aerospace OEMs see 15-20% weight savings when polymer coated fabrics replace heavier substrates, translating directly to fuel efficiency gains. Continental AG integrates rice-husk silica and natural rubber into its coated fabric range, demonstrating how renewable fillers meet durability specifications without cost penalties.

Supply-Chain Localization Disrupting Global Trade Flows

Geopolitical tensions spur regionalized production, raising capital needs for duplicate coating lines across continents and compressing economies of scale. U.S. buyers diversify sourcing toward India and Southeast Asia to mitigate tariff exposure.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Protective-Clothing Standards Across APAC Manufacturing

- Adoption of Antimicrobial Coatings in Healthcare Furnishings

- Environmental Scrutiny of PVC and Phthalates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PVC held 41.55% polymer-coated fabric market share in 2025, reflecting entrenched cost and processing advantages. Polyurethane, however, is projected to post a 5.88% CAGR to 2031 as converters adapt to phthalate restrictions and recyclability mandates. Lubrizol's ESTANE RNW TPU offers a 59% lower carbon footprint while maintaining abrasion resistance, illustrating how greener chemistries transition from niche to mainstream.

Silicone and polyethylene retain specialized roles in extreme-temperature or chemically inert uses, whereas bio-based hybrids gain traction in consumer electronics casings and luxury accessories. Technological roadmaps reveal that leading suppliers pair coating innovation with substrate engineering. Freudenberg's fine-filament spunbond supports thinner, lighter membranes, lowering solvent uptake and boosting coating line throughput. This integrated approach underscores how performance gains derive from both polymer advances and fabric architecture.

The Polymer Coated Fabric Report is Segmented by Product Type (PVC (Polyvinyl Chloride), Polyurethane (PU), Polyethylene, and Others), Application (Transportation, Industrial Equipment Covers, Roofing and Awning, Protective Clothing, Furniture, Sports and Leisure, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 46.10% polymer-coated fabric market share in 2025 and is projected to register a 5.72% CAGR through 2031. India's Textile Mission, backed by USD 629 million in 2025 budget allocations, earmarks funds for technical-textile research and development and pilot coating facilities. Public infrastructure programs, from metro rail to flood-resilient roofing, convert this capacity into sustained coated fabric off-take.

North America secures a technology-driven niche where aerospace and medical OEMs demand low-VOC, PFAS-free materials. Reshoring of electric-vehicle production amplifies local sourcing for seat fabrics and battery-pack covers. The polymer-coated fabric market sees suppliers investing in U.S. greenfield plants built for carbon-neutral operation, as evidenced by Trelleborg's Rutherford County project, slated for LEED certification

Europe remains a regulation-led market incubating solvent-free, waterborne coatings aligned with the Industrial Emissions Directive. OEM preference for full material disclosure favors certified suppliers, creating price resilience for high-compliance products. Middle East and Africa, though smaller, post above-average growth on the back of climate-resilient construction in the Gulf and industrial diversification in South Africa. Limited domestic coating lines present outsourcing opportunities for incumbents willing to invest in regional service hubs.

- Continental AG

- Cooley Group

- Freudenberg Performance Materials Holding GmbH

- Heytex Gruppe

- OMNOVA North America Inc.

- Saint-Gobain

- Seaman Corporation

- Serge Ferrari Group

- Sioen Industries NV

- SPRADLING INTERNATIONAL GmbH

- SRF Limited

- Trelleborg AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Lightweight, Sustainable Interior Materials

- 4.2.2 Growth in Protective-Clothing Standards Across APAC Manufacturing

- 4.2.3 Surge in Architectural Tensile Structures for Climate-Resilient Infrastructure

- 4.2.4 Adoption of Antimicrobial Coatings in Healthcare Furnishings

- 4.2.5 Investments in Flexible PV Back-Sheet Fabrics

- 4.3 Market Restraints

- 4.3.1 Volatility of Crude-Derived Polymer Prices

- 4.3.2 Environmental Scrutiny of PVC and Phthalates

- 4.3.3 Supply-Chain Localization Disrupting Global Trade Flows

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 PVC (Polyvinyl Chloride)

- 5.1.2 PU (Polyurethane)

- 5.1.3 Polyethylene

- 5.1.4 Silicone

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Transportation

- 5.2.2 Industrial Equipment Covers

- 5.2.3 Roofing and Awning

- 5.2.4 Protective Clothing

- 5.2.5 Furniture

- 5.2.6 Sports and Leisure

- 5.2.7 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Cooley Group

- 6.4.3 Freudenberg Performance Materials Holding GmbH

- 6.4.4 Heytex Gruppe

- 6.4.5 OMNOVA North America Inc.

- 6.4.6 Saint-Gobain

- 6.4.7 Seaman Corporation

- 6.4.8 Serge Ferrari Group

- 6.4.9 Sioen Industries NV

- 6.4.10 SPRADLING INTERNATIONAL GmbH

- 6.4.11 SRF Limited

- 6.4.12 Trelleborg AB

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment