|

시장보고서

상품코드

1906144

중동 및 아프리카의 바이오 비료 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Middle East And Africa Biofertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

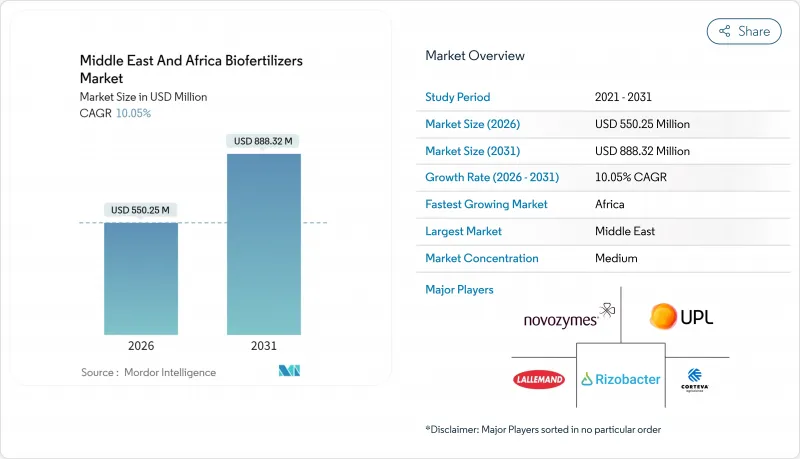

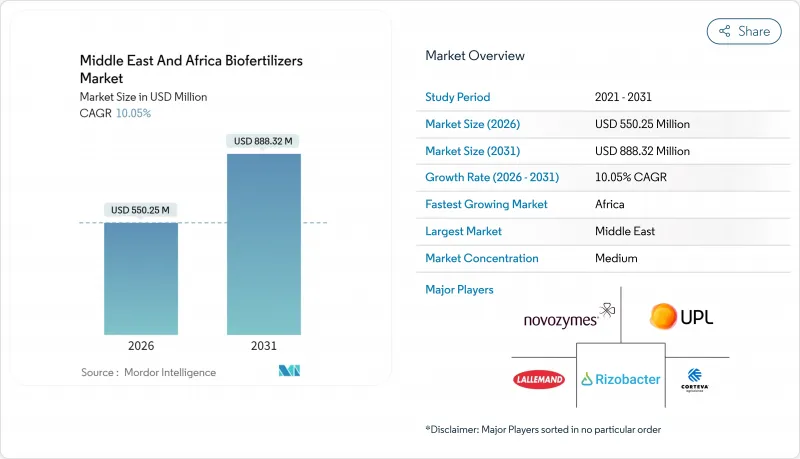

중동 및 아프리카의 바이오 비료 시장은 2025년 5억 달러로 평가되었으며, 2026년 5억 5,025만 달러에서 2031년까지 8억 8,832만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 10.05%로 전망됩니다.

이러한 성장의 기세는 물 부족, 토양염류화, 합성자재 가격의 변동 등 지역 특유의 과제에 의해 발생하고 있으며, 이들이 생물 유래 선택지로의 이행을 가속화하고 있습니다. 사우디아라비아의 '비전 2030', 남아프리카의 생물소재에 대한 규제 신속화 프로그램, 아프리카 연합의 비료 자급률 향상 계획 등의 정부 시책은 규제 장벽 감소와 생물소재에 대한 보조금 제공을 통해 바이오비료 도입을 뒷받침하고 있습니다. 다국적 공급업체는 현지 생산과 목표를 좁힌 파트너십을 통해 존재감을 높이는 한편, 지역의 혁신자는 가혹한 농업 기후 조건에 적합한 미생물주를 개발함으로써 틈새 시장을 확보하고 있습니다. 이러한 요인들이 더하여 중동 및 아프리카의 바이오 비료 시장은 기후 스마트 농업의 목표에 따른 정책 지원에 의한 견조한 확대가 예상됩니다.

중동 및 아프리카의 바이오 비료 시장의 동향 및 인사이트

유기농 인증 농지의 확대

중동 및 아프리카 주요 시장의 유기농 인증 농지 면적은 2019년부터 2024년에 걸쳐 확대되었으며 이집트, 케냐, 남아프리카가 도입률을 견인하고 있습니다. 유기농 인증 기준이 합성재료보다 생물소재의 사용을 의무화하기 때문에 이 성장궤도는 바이오 비료의 수요를 가속화하고 있습니다. 케냐의 유기농 농업 부문은 현재 16만 5천 헥타르 이상으로 확대되고 있으며, 수출시장의 프리미엄 가격과 '국가유기농농업정책'을 통한 정부지원이 원동력이 되고 있습니다. 이 확장은 특히 유기농 생산 시스템의 복잡한 영양 요구에 대응하는 다균주 배합 제품을 제공하는 바이오 비료 공급자에게 독점 시장을 창출하고 있습니다. 모로코의 '그린 모로코 계획'은 유기농 전환 지원에 많은 자원을 할당하고, 생물소재를 우대하는 규제 프레임워크을 구축하여, 품질 인증 경로를 확립하고 있습니다.

보조금과 유기농 소재 우대 정책

지역 전체의 정부 보조금 제도는 생물소재를 점점 우대하고 있으며, 모로코의 유기농 소재 보조금 프로그램은 보조대상 외 합성소재에 비해 농가의 도입비용을 25% 절감하고 있습니다. 사우디아라비아의 환경수자원농업부는 비전 2030의 지속가능성 목표에 따라 생물학적 영양 관리 시스템을 도입하는 온실 경영자에 대한 맞춤형 지원을 실시했습니다. 이러한 정책 전환은 생물소재가 식량 안보 목표를 지원하는 동시에 수입 의존도를 줄이는 전략적 인식을 반영합니다. 아랍에미리트(UAE)의 '국가 식량 안보 전략 2051'은 제어 환경 농업용 미생물 접종제를 포함한 현지 생산 기술을 명시적으로 우선합니다. 남아프리카의 '비료, 사료, 농업용 약제 및 축산용 약제법'에 근거한 규제 프레임워크는 바이오 비료의 등록에 대한 명확한 경로를 나타내고 있지만, 제품 등록료 3,500랜드(202.30달러)로부터 업그레이드료 1,800랜드(104.06달러)에 이르는 비용이 발생합니다.

보조금이 제공되는 합성 비료의 우위

나이지리아, 이집트 및 기타 주요 농업 경제 국가의 국가 비료 보조금 제도는 가격에 민감한 시장 부문에서 합성 소재에 구조적 우위를 부여하고 생물학적 대체품이 시장에서 밀려나는 요인이 되고 있습니다. 나이지리아의 비료 보조금 제도는 식량 안보 목적을 지원하는 한편, 수입 합성 제품에 인위적인 가격 우위성을 유지하게 하여, 의도치 않게 바이오 비료의 도입을 제한하고 있습니다. 이집트의 보조금 프레임워크도 기존의 투입소재를 우대하지만 최근의 정책 논의에서는 미래의 보조금 제도에 생물학적 제품을 도입할 가능성이 시사되고 있습니다. 이러한 제도는 시장 왜곡을 일으키고, 바이오 비료 공급업체는 비용 경쟁력이 아니라 성능 차별화로 경쟁할 수밖에 없습니다. 보조금 제도 유지의 재정부담은 농업생산성을 지지하면서 예산압력을 경감하는 비용효과적인 대체수단을 정부가 모색하는 가운데 미래에 생물학적 투입소재의 기회 창출로 이어질 수 있습니다.

부문 분석

근류균 기반의 바이오 비료는 2025년에 35.85% 시장 점유율을 차지하고 있으며, 식량 안보와 토양 비옥도 관리의 양면에서 이 지역의 콩류 재배의 중요성을 반영하고 있습니다. 이러한 이점은 확립된 농학적 지식과 입증된 질소 고정 효과로 인해 비용 의식이 높은 농가층에 의해 뒷받침됩니다. 다국적 기업과 지역 연구소 간의 기술 이전 계약은 듀얼 브랜딩을 촉진하고 첨단 협동 조합 간의 신뢰 강화에 기여합니다. 근류균의 사용과 보전 농업 기술을 결합한 교육 모듈은 반복 판매의 기반을 더욱 강화합니다.

균근 제품은 고부가가치 온실 재배와 가뭄 다발 지역에서 농업 시스템으로의 도입이 추진력이 되어, 2031년까지 연평균 복합 성장률(CAGR) 12.75%로 가장 급속하게 성장할 것으로 예상되는 부문입니다. 이러한 환경에서 영양 흡수의 향상은 측정 가능한 수율 향상을 가져옵니다. 지역 전체의 연구 활동은 현지 토양 조건과 기후 스트레스에 적응한 재래 미생물주에 초점을 맞추는 경향이 강해지고 있으며, 현지 조달 제품의 시장 수용이 진행됨에 따라 경쟁 구도의 재편이 예상됩니다. 균주 선별과 지역 적응에 투자하는 기업은 범용적인 국제 제제를 통해 시장 점유율을 획득하는 입장에 있습니다.

담체 강화형 바이오 비료는 2025년에 56.80% 시장 점유율을 유지한 것으로 나타났습니다. 이는 소규모 농가 시스템의 기존 적용 관행과의 호환성과 비용 효율성을 반영한 것입니다. 이러한 제제는 갈탄이나 목탄 등 현지에서 입수할 수 있는 담체를 이용함으로써 생산 비용을 절감하고 지역 공급망을 지원하고 있습니다. 기술 세분화는 비용에 중점을 둔 소규모 농부용 용도와 성능 중심의 상업적 운영 사이의 광범위한 시장 양극화를 반영합니다. 고온 조건 하에서도 생존성을 유지하는 기후 적응형 제제를 개발하는 기업은 시장의 성숙화와 품질 기준의 엄격화에 따라 상대적으로 큰 가치를 획득할 가능성이 높습니다.

액체 바이오 비료는 2031년까지 15.1%의 연평균 복합 성장률(CAGR)로 성장할 가장 빠른 기술 부문으로 떠오르고 있으며, 주로 GCC 국가에서 온실 재배에서의 도입과 정밀 농업 용도가 견인하고 있습니다. 액체 부문은 미생물의 생존율이 높고 시비 관개 시스템과의 통합이 용이하다는 장점이 있지만, 콜드체인 요구사항은 인프라가 제한된 시장에서의 보급을 제한하고 있습니다.

중동 및 아프리카의 바이오 비료 시장은 미생물 유형별(근류균, 질소 고정균 등), 기술 유형별(담체 강화형 바이오 비료, 액체 바이오 비료 등), 용도별(토양 개량 등), 작물 유형별(곡류 등), 지역별(아프리카, 중동)으로 분류됩니다. 시장 예측은 금액, 달러 및 수량(메트릭)으로 제공됩니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 유기농 인증 농지의 확대

- 보조금 및 유기농 소재 도입 촉진 정책

- 합성 비료 가격의 변동성

- 걸프 지역 토양의 염해 완화 프로그램

- 첨단 온실 붐

- 토양 미생물총 프로젝트용 탄소배출권 파일럿 사업

- 억제요인

- 보조금을 동반하는 합성 비료의 지배적 지위

- 농가의 인지도가 낮고 보급 네트워크가 취약함

- 규제의 틈으로 인해 발생하는 모조품 및 저품질 접종제

- 액체 제제에 대한 콜드체인 물류의 과제

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측(금액 및 수량)

- 미생물 유형별

- 근류균

- 아조토박터

- 아조스피릴룸

- 인산 용해성 세균

- 균근

- 기타 미생물

- 기술 유형별

- 담체 강화형 바이오 비료

- 액체 바이오 비료

- 캡슐화 및 비드 기술

- 기타 기술

- 용도별

- 토양 처리

- 종자 처리

- 엽면 살포 및 근부 침지

- 기타 용도

- 작물 유형별

- 곡물

- 콩류

- 상업 작물

- 과수 및 채소

- 기타 작물

- 지역별

- 아프리카

- 남아프리카

- 케냐

- 우간다

- 탄자니아

- 나이지리아

- 기타 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 이집트

- 카타르

- 기타 중동

- 아프리카

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Novozymes A/S

- UPL Limited

- Lallemand Inc

- Corteva, Inc.

- Rizobacter Argentina SA

- FMC Corporation

- Koppert BV

- IPL Biologicals Limited

- Groundwork BioAg Ltd.

- Biobest Group NV

- Biomax Technologies Pte. Ltd.

- Mapleton Agri Biotec Pty Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

제7장 시장 기회 및 미래 전망

CSM 26.01.28The Middle East and Africa biofertilizers market was valued at USD 500 million in 2025 and estimated to grow from USD 550.25 million in 2026 to reach USD 888.32 million by 2031, at a CAGR of 10.05% during the forecast period (2026-2031).

Momentum stems from region-specific pressures including water scarcity, soil salinity, and synthetic input price volatility, which are accelerating the shift toward biologically based options. Government programs such as Saudi Arabia's Vision 2030, South Africa's regulatory fast-track for biologicals, and the African Union's fertilizer self-sufficiency agenda reinforce adoption by lowering regulatory hurdles and subsidizing biological inputs. Multinational suppliers deepen their presence through local manufacturing and targeted partnerships, while regional innovators secure niches by tailoring microbial strains to harsh agro-climatic conditions. Collectively, these forces position the Middle East and Africa biofertilizers market for robust, policy-backed expansion that aligns with climate-smart agriculture goals.

Middle East And Africa Biofertilizers Market Trends and Insights

Expansion of Organic-Certified Farmland

Certified organic acreage across key Middle East & Africa markets expanded between 2019-2024, with Egypt, Kenya, and South Africa leading adoption rates. This growth trajectory accelerates biofertilizer demand as organic certification standards mandate biological inputs over synthetic alternatives. Kenya's organic sector now encompasses over 165,000 hectares, driven by export market premiums and government support through the National Organic Agriculture Policy. The expansion creates a captive market for biofertilizer suppliers, particularly those offering multi-strain formulations that address the complex nutrient needs of organic production systems. Morocco's Green Morocco Plan has allocated significant resources to organic transition support, creating regulatory frameworks that favor biological inputs and establish quality certification pathways.

Subsidies and Favorable Organic-Input Policies

Government subsidy schemes across the region increasingly favor biological inputs, with Morocco's organic-input subsidy program reducing farmer adoption costs by 25% compared to unsubsidized synthetic alternatives. Saudi Arabia's Ministry of Environment, Water, and Agriculture has implemented targeted support for greenhouse operators adopting biological nutrient management systems, aligning with Vision 2030 sustainability objectives. These policy shifts reflect strategic recognition that biological inputs support food security goals while reducing import dependency. The UAE's National Food Security Strategy 2051 explicitly prioritizes local production technologies, including microbial inoculants for controlled environment agriculture. South Africa's regulatory framework under the Fertilizers, Farm Feeds, Agricultural Remedies and Stock Remedies Act provides clear pathways for biofertilizer registration, though fees ranging from R 3,500 (USD 202.30) for product registration to R 1,800 (USD 104.06) for renewals create cost barriers for smaller manufacturers .

Dominance of Subsidized Synthetic Fertilizers

National fertilizer subsidy programs in Nigeria, Egypt, and other major agricultural economies create structural advantages for synthetic inputs that crowd out biological alternatives in price-sensitive market segments. Nigeria's fertilizer subsidy program, while supporting food security objectives, inadvertently limits biofertilizer adoption by maintaining artificial price advantages for imported synthetic products. Egypt's subsidy framework similarly favors conventional inputs, though recent policy discussions indicate potential inclusion of biological products in future subsidy schemes. These programs create market distortions that require biofertilizer suppliers to compete on performance differentiation rather than cost parity. The fiscal burden of maintaining subsidy programs may create future opportunities for biological inputs as governments seek cost-effective alternatives that support agricultural productivity while reducing budget pressures.

Other drivers and restraints analyzed in the detailed report include:

- Synthetic-Fertilizer Price Volatility

- High-Tech Greenhouse Boom

- Low Farmer Awareness and Weak Extension Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rhizobium-based biofertilizers command 35.85% market share in 2025, reflecting the region's substantial legume cultivation for both food security and soil fertility management. This dominance stems from well-established agronomic understanding and proven nitrogen fixation benefits that resonate with cost-conscious farmers.Technology transfer agreements between multinationals and regional labs promote dual branding, enhancing trust among progressive cooperatives. Training modules that bundle Rhizobium use with conservation agriculture practices further anchor repeat sales.

Mycorrhizal products represent the fastest-growing segment at 12.75% CAGR through 2031, driven by adoption in high-value greenhouse operations and drought-prone farming systems where enhanced nutrient uptake provides measurable yield advantages. Research initiatives across the region increasingly focus on indigenous microbial strains adapted to local soil conditions and climatic stresses, potentially reshaping competitive dynamics as locally sourced products gain market acceptance. Companies investing in strain selection and regional adaptation are positioned to capture market share from generic international formulations.

Carrier-enriched biofertilizers maintain 56.80% market share in 2025, reflecting their cost-effectiveness and compatibility with existing farmer application practices across smallholder systems. These formulations utilize locally available carriers such as lignite and charcoal, reducing production costs and supporting regional supply chains. The technology segmentation reflects broader market bifurcation between cost-focused smallholder applications and performance-oriented commercial operations. Companies developing climate-adapted formulations that maintain viability under high-temperature conditions are likely to capture disproportionate value as the market matures and quality standards tighten.

Liquid biofertilizers emerge as the fastest-growing technology segment with 15.1% CAGR through 2031, primarily driven by greenhouse adoption in GCC countries and precision agriculture applications. The liquid segment benefits from superior microbial viability and ease of integration with fertigation systems, though cold-chain requirements limit adoption in infrastructure-constrained markets.

The Middle East and Africa Biofertilizers Market is Segmented by Microorganism Type (Rhizobium, Azotobacter, and More), by Technology Type (Carrier-Enriched Biofertilizers, Liquid Biofertilizers, and More), by Application (Soil Treatment, and More), by Crop Type (Grains and Cereals, and More), and by Geography (Africa, and the Middle East). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Novozymes A/S

- UPL Limited

- Lallemand Inc

- Corteva, Inc.

- Rizobacter Argentina S.A.

- FMC Corporation

- Koppert B.V.

- IPL Biologicals Limited

- Groundwork BioAg Ltd.

- Biobest Group NV

- Biomax Technologies Pte. Ltd.

- Mapleton Agri Biotec Pty Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of organic-certified farmland

- 4.2.2 Subsidies and favorable organic-input policies

- 4.2.3 Synthetic-fertilizer price volatility

- 4.2.4 Salinity-mitigation programs in Gulf soils

- 4.2.5 High-tech greenhouse boom

- 4.2.6 Carbon-credit pilots for soil microbiome projects

- 4.3 Market Restraints

- 4.3.1 Dominance of subsidized synthetic fertilizers

- 4.3.2 Low farmer awareness and weak extension networks

- 4.3.3 Counterfeit / low-quality inoculants from regulatory gaps

- 4.3.4 Cold-chain logistics hurdles for liquid formulations

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Microorganism Type

- 5.1.1 Rhizobium

- 5.1.2 Azotobacter

- 5.1.3 Azospirillum

- 5.1.4 Phosphate-solubilizing Bacteria

- 5.1.5 Mycorrhiza

- 5.1.6 Other Microorganisms

- 5.2 By Technology Type

- 5.2.1 Carrier-enriched Biofertilizers

- 5.2.2 Liquid Biofertilizers

- 5.2.3 Encapsulated / Bead Technology

- 5.2.4 Other Technologies

- 5.3 By Application

- 5.3.1 Soil Treatment

- 5.3.2 Seed Treatment

- 5.3.3 Foliar / Root Dipping

- 5.3.4 Other Applications

- 5.4 By Crop Type

- 5.4.1 Grains

- 5.4.2 Pulses

- 5.4.3 Commercial Crops

- 5.4.4 Fruits and Vegetables

- 5.4.5 Other Crops

- 5.5 By Geography

- 5.5.1 Africa

- 5.5.1.1 South Africa

- 5.5.1.2 Kenya

- 5.5.1.3 Uganda

- 5.5.1.4 Tanzania

- 5.5.1.5 Nigeria

- 5.5.1.6 Rest of Africa

- 5.5.2 Middle East

- 5.5.2.1 United Arab Emirates

- 5.5.2.2 Saudi Arabia

- 5.5.2.3 Turkey

- 5.5.2.4 Egypt

- 5.5.2.5 Qatar

- 5.5.2.6 Rest of Middle East

- 5.5.1 Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Novozymes A/S

- 6.4.2 UPL Limited

- 6.4.3 Lallemand Inc

- 6.4.4 Corteva, Inc.

- 6.4.5 Rizobacter Argentina S.A.

- 6.4.6 FMC Corporation

- 6.4.7 Koppert B.V.

- 6.4.8 IPL Biologicals Limited

- 6.4.9 Groundwork BioAg Ltd.

- 6.4.10 Biobest Group NV

- 6.4.11 Biomax Technologies Pte. Ltd.

- 6.4.12 Mapleton Agri Biotec Pty Ltd

- 6.4.13 BASF SE

- 6.4.14 Bayer AG

- 6.4.15 Corteva Agriscience