|

시장보고서

상품코드

1906171

신경혈전제거 기기 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Neurothrombectomy Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

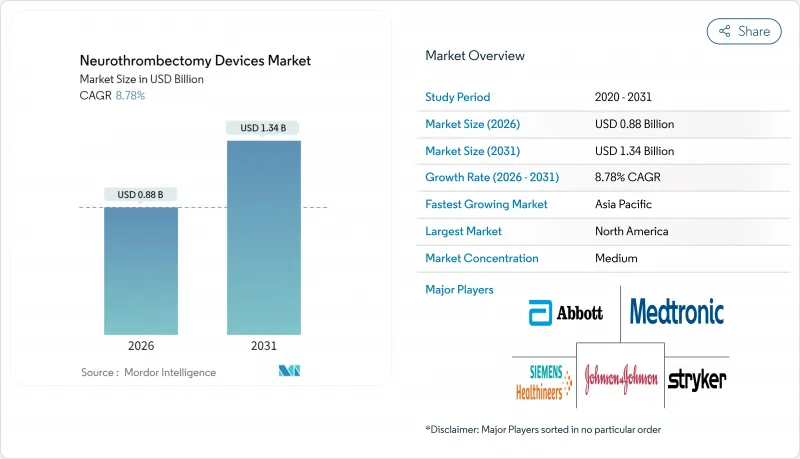

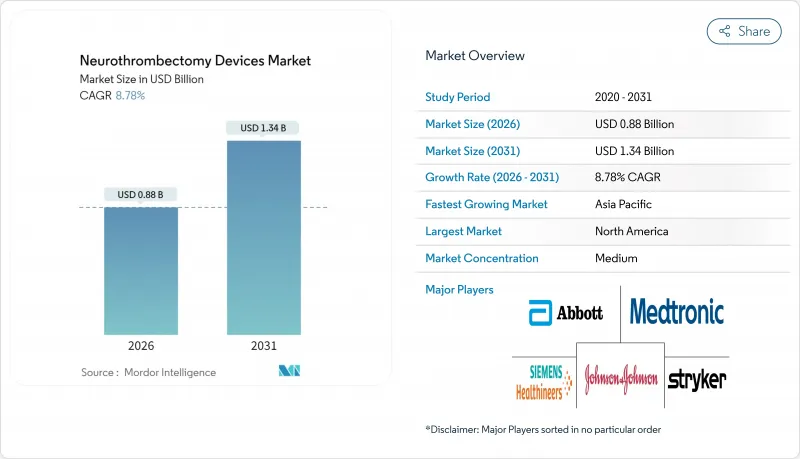

신경혈전제거 기기 시장은 2025년 8억 1,000만 달러로 평가되었으며, 2026년 8억 8,000만 달러에서 2031년까지 13억 4,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 8.78%로 예상됩니다.

DAWN 시험 및 DEFUSE-3 시험의 발견을 통해 치료 가능 시간이 24시간까지 확대되어 시장의 현재 성장 궤도의 핵심적인 촉진요인이 되고 있습니다. 미국, 독일, 일본에서의 보험 적용 범위의 확대와 환자 선택을 정밀화하는 AI 탑재의 뇌졸중 트리아지 툴의 도입이 더하여, 수기 실시 건수 증가가 계속되고 있습니다. 절차 시간을 단축하고 방사선 노출을 줄이는 대구경 흡입 카테터는 비용에 중점을 둔 의료 시스템에 영향을 미치는 경제적 이점을 제공합니다. 반면에 니티놀과 백금 이리듐 합금 공급망의 취약점은 가격 변동 요인이 되고 제조업체는 이를 완화해야 합니다. 이러한 요인들이 결합되어 신경혈전제거 기기 시장의 지속적인 성장은 임상적 증거, 환급 정책, 재료의 안정적인 공급이 조화를 이룬 균형 잡힌 전망을 형성하고 있습니다.

세계의 신경혈전제거 기기 시장의 동향 및 인사이트

DAWN/DEFUSE-3 시험 후 가이드라인 주도에 의한 도입 확대

DAWN 및 DEFUSE-3 시험은 대혈관 폐색성 뇌졸중의 치료 가능 시간을 6시간에서 24시간으로 확대하였으며, 이는 신경혈전제거 기기 시장을 직접적으로 확대시켰습니다. 국제 뇌졸중 학회는 2024년에 이러한 인사이트를 개정 가이드라인에 반영했고 종합 뇌졸중 센터에서는 그 후 수기 실시 건수가 40-60% 증가했다고 보고하고 있습니다. 관류 이미징의 보급으로 환자 선택의 표준화가 진행되고 병원 간의 편차가 감소함과 동시에 이미징 기기와 혈전 제거 기구 모두에 대한 수요가 높아지고 있습니다. FDA 절차 지침을 포함한 규제의 정합화는 미국 내 시설 간의 진료 패턴을 더욱 균일화하고 있습니다. 지역 병원으로의 도입이 진행됨에 따라 가이드 라인 준수가 계속 시술 건수를 높여 확립된 지역과 신흥 지역 모두의 성장을 강화해 나갈 것입니다.

미국, 독일, 일본에서의 환급 범위 확대

미국 의료보험서비스센터(CMS)는 2023년 경동맥 및 신경혈관 인터벤션의 진료 보상 코드를 확대하고 혈전 제거술의 병원 경제성을 즉각적으로 개선하는 정책 지원을 제시했습니다. 독일의 DRG 모델에서는 기계적 혈전제거술에 대한 특정 보상이 도입되었고 일본의 국민보험은 명확한 임상기준 하에서 선진기기의 적용 범위를 확대했습니다. 이러한 개선에도 불구하고, 미국 메디케어의 환급율은 여전히 청구액의 18-22%에 그치고, 이는 제공업체의 이익률에 압박을 가져오고 있습니다. 민간보험사는 가이드라인 변경을 반영한 사전승인 규정의 개정에 의해 이 차이를 채우면서 절차에 대한 접근성을 강화하고 있습니다. 지불자 프레임워크가 성숙하는 가운데, 신경혈전제거 기기의 추가적인 시장 확대는 후순환계 뇌졸중과 외래 진료 환경의 공식적인 인지에 달려 있습니다. 최근의 캠페인 활동은 실제 세계의 비용 절감과 환자 예후를 반영한 가치 기반 코드를 통합하는 것을 목표로 하고 있으며, 환급 주도 수요의 지속을 위한 기반을 마련하고 있습니다.

신흥 시장에서의 높은 장비 및 치료 비용

자원이 부족한 환경에서는 신경혈전제거 기기 비용이 총 치료비의 최대 80%를 차지합니다. 인도의 PRAAN 연구는 증례당 지출을 3,500-5,000달러로 추정하고 있으며 이는 월수익 중앙치의 최대 15배에 해당합니다. 존슨 매세이가 의료기기 부품 부문을 매각한 사례로 대표되는 공급망의 통합으로 니티놀과 백금 이리듐 합금의 원재료 가격에 대한 압력이 높아지고 있습니다. 공공 의료 예산은 일반적으로 전문 치료에 대한 국가 지출의 5% 미만으로 제한되며 이는 장비 조달을 방해합니다. 병원에는 현대 영상 진단 장비와 하이브리드 수술실이 부족한 경우가 많으며, 수술을 제공하려면 추가 설비 투자가 필요합니다. 자금 지원 및 가격 관리 제품의 제공 없이는 비용 장벽으로 인해 일부 신흥 경제 국가에서 신경혈전제거 기기 시장의 침투가 계속 제한될 것입니다.

부문 분석

스텐트 리트리버는 2025년 시점에서 신경혈전제거 기기 시장의 63.78%를 차지하였으며, 종합뇌졸중센터에서 수술의 주력 기기로 자리매김하고 있습니다. 스텐트 리트리버의 이점은 혈전 형태에 관계없이 높은 재관류율이 확인된 기간 시험을 포함한 수십 년간의 임상 검증을 반영한 것입니다. 또한 NeVa NET 5.5 디바이스가 다중 시설 평가에서 처음 통과했을 때 거의 완전한 재소통률 54.9%를 달성하는 등 설계 개량의 적층이 부문의 우위성을 강화하고 있습니다. 높은 가격대임에도 불구하고 의사의 숙련도가 높고 다용도성이 뛰어나기 때문에 의료기관에서는 여러 사이즈의 스텐트 리트리버를 계속 비축하고 있습니다. 한편, 흡입 카테터는 가장 급속한 확대경로를 나타내며, 2031년까지 연평균 복합 성장률(CAGR) 7.06%가 전망되고 있습니다. 이는 셋업을 효율화하고 색전 합병증을 줄이는 신형 대구경 설계가 촉진요인이 되고 있습니다. 복합기계시스템은 복잡한 혈전구조를 다루는 전문의가 지지하는 반면, 고비용과 가파른 학습곡선에 의해 보급은 한정적입니다. 풍선 가이드 카테터 및 부속 라인은 핵심 장치 채택과 연계하여 성장하여 신경혈전제거 기기 시장에서 뇌졸중 프로그램을 위한 통합 재고 솔루션을 확립합니다.

2030년까지는 스텐트 리트리버의 우위성이 경쟁에서 흔들릴 가능성은 낮지만, 흡인 우선 기술(aspiration-first)의 경제적 매력이 치료 알고리즘의 변화를 지속적으로 추진하고 있습니다. 주요 제조업체는 혈전 보유성을 높이고 원위부 색전을 최소화하는 코팅 기술에 투자하고 미국에서 신속 승인을 목적으로 한 510(k) 신청 경로를 활용하고 있습니다. 흡입 기구의 신경혈전제거 기기 시장 내 규모는 이러한 진보의 혜택을 받는 한편, 스텐트 리트리버의 벤더는 실습이나 AI 구동형 증례 계획을 포함한 번들 서비스 모델로 점유율을 유지합니다. 효능 증거, 비용 억제, 워크플로 최적화의 상호작용은 건전한 2강 체제를 지원하여 두 범주에서 지속적인 혁신을 촉진하고 있습니다.

지역별 분석

북미는 2025년 신경혈전제거 기기 시장에서 41.86%의 점유율을 차지했고, 견조한 보험 적용 범위, 밀집한 병원 네트워크, 치료 기간 연장 가이드라인의 조기 도입을 배경으로 주도적 입장을 유지했습니다. 메디케어에 의한 2023년 경동맥 인터벤션 적용 범위 확대는 지속적인 정책 지원을 나타내고 민간 보험 회사도 신속하게 승인 기준의 통일을 진행했습니다. 미국에서는 AI 구동형 트리아지 소프트웨어를 활용하여 치료 지연을 해소하는 한편, 캐나다에서는 전국민 보험 제도에 의해 주 간의 접근성 격차를 해소하고 있습니다. 멕시코에서는 의료기술의 조화에 의한 크로스보더 디바이스 인가의 원활화가 점진적인 성장을 가져오고, 대륙 규모의 에코시스템이 형성됨으로써 안정된 시술 건수가 유지되어 지역 내 신경혈전제거 기기 시장의 발전을 촉진하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 7.06%로 확대되어 신경혈전제거 기기 시장에서 가장 성장이 현저한 지역이 될 전망입니다. 중국과 인도의 정부 투자 프로그램으로 지방 도시에서 신경 집중 치료실(Neuro-ICU)의 정비가 진행되어 기존의 일류 병원에 의존하고 있던 환자층이 확대되고 있습니다. 일본에서는 전국민 보험제도 하에서 고기능 혈전제거 플랫폼의 도입이 진행되고 있으며, 한국과 호주에서는 자금력이 있는 국민건강보험제도가 하이엔드 기기 수요를 견인하고 있습니다. 다양하면서도 수렴하고 있는 이러한 환경이 아시아태평양을 전략적 성장 프론티어로 자리매김하고 있으며, 트레이닝 제휴 및 가격대별 제품 라인에 의해 세계 제조업체와 지역 제조업체 모두에게 추가적인 점유율 확대의 기회가 탄생하고 있습니다.

유럽은 성숙하면서도 안정적인 시장 상황을 보여주며, 종합적인 환급 제도와 확립된 국가 뇌졸중 치료 프로토콜이 정비되어 있습니다. 독일의 DRG 환급 제도는 예측 가능한 경제성을 제공하고 영국의 NHS는 혈전 제거술을 표준화된 품질 지표에 통합하고 있습니다. 프랑스, 이탈리아, 스페인은 학술연구를 통해 범유럽적인 임상 실천에 기여하고 있습니다. CE 마크의 통합 기준은 시장 진입을 원활하게 하지만 일부 지역에서는 재정 긴축이 절차의 성장을 억제하고 있습니다. 전반적으로 꾸준한 교체주기와 성과기반 조달에 중점을 둔 유럽은 신경혈전제거 기기 시장에 지속해서 기여하고 있지만 지역별 성장률은 아시아태평양을 밑돌고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- DAWN/DEFUSE-3 시험 후의 가이드라인에 근거한 도입 확대

- 미국, 독일, 일본에서의 환급 범위 확대

- 대구경 흡입 카테터로 처리 시간과 비용 절감

- AI를 활용한 뇌졸중 트리아지에 의해 대상 환자층 확대

- 중국 및 인도 지방도시에서의 급속한 신경집중치료실(Neuro-ICU) 병상 증가

- 억제요인

- 신흥 시장에서의 높은 의료기기 및 처치 비용

- 도시 이외에서의 숙련된 신경 전문의 부족

- 니티놀 및 백금 이리듐 합금 공급망의 취약성

- 후순환 혈전제거술의 환급 지연

- 가치 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 공급자의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 기기 유형별

- 스텐트 리트리버

- 흡입 카테터

- 복합 기계적 혈전 제거 시스템

- 풍선 가이드 카테터 및 부속 기기

- 최종 사용자별

- 병원

- 전문 신경외과 센터

- 외래수술센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Medtronic plc

- Stryker Corporation

- Penumbra Inc.

- Johnson & Johnson(CERENOVUS)

- Terumo Corporation

- MicroPort Scientific Corporation

- Rapid Medical Ltd.

- Phenox GmbH

- Acandis GmbH

- Vesalio, LLC

- Control Medical Technology, LLC

- Wallaby Medical

- Zylox-Tonbridge Medical Technology Co., Ltd.

제7장 시장 기회 및 미래 전망

CSM 26.01.28The Neurothrombectomy devices market was valued at USD 0.81 billion in 2025 and estimated to grow from USD 0.88 billion in 2026 to reach USD 1.34 billion by 2031, at a CAGR of 8.78% during the forecast period (2026-2031).

Evidence from the DAWN and DEFUSE-3 trials has enlarged the treatment window to 24 hours and is the core catalyst behind the market's current growth trajectory. Wider insurance coverage in the United States, Germany, and Japan, paired with AI-enabled stroke triage tools that sharpen patient selection, continue to expand procedure volumes. Large-bore aspiration catheters that shorten procedure times and reduce radiation exposure add an economic advantage that resonates with cost-sensitive healthcare systems. At the same time, supply-chain fragility for nitinol and platinum-iridium alloys introduces pricing volatility that manufacturers must mitigate. Collectively, these forces shape a balanced outlook in which clinical evidence, reimbursement policy, and materials security must align for sustained growth of the Neurothrombectomy devices market.

Global Neurothrombectomy Devices Market Trends and Insights

Growing Guideline-Driven Adoption After DAWN/DEFUSE-3 Trials

The DAWN and DEFUSE-3 trials extended the treatment window for large-vessel occlusion strokes from 6 hours to 24 hours, which has directly enlarged the Neurothrombectomy devices market. International stroke societies integrated these findings into updated guidelines in 2024, and comprehensive stroke centers have since reported 40-60% procedure volume increases. Wider use of perfusion imaging now standardizes patient selection, reduces inter-hospital variability, and raises demand for both imaging and thrombectomy tools. Regulatory alignment, including FDA procedural guidance, further harmonizes practice patterns across U.S. facilities. As adoption spreads into community hospitals, guideline compliance will continue to lift procedure volumes and reinforce growth across established and emerging regions.

Favorable Reimbursement Expansions in U.S., Germany & Japan

CMS broadened codes for carotid and neurovascular interventions in 2023, signaling policy support that immediately improves hospital economics for thrombectomy. Germany's DRG model has introduced specific mechanical thrombectomy reimbursements, while Japan's national payer added advanced device coverage under clearly defined clinical criteria. Despite these improvements, U.S. Medicare still reimburses only 18-22% of billed charges, creating margin pressure for providers. Private insurers are closing the gap by updating prior authorization rules to mirror guideline changes, strengthening procedure access. As payer frameworks mature, additional Neurothrombectomy devices market gains hinge on formal recognition of posterior-circulation strokes and outpatient settings. Recent advocacy efforts aim to embed value-based codes that capture real-world cost savings and patient outcomes, setting the stage for continued reimbursement-driven demand.

High Device & Procedure Cost in Emerging Markets

Neurothrombectomy device costs account for up to 80% of total procedure expenses in low-resource settings. The PRAAN study from India estimated per-case spending at USD 3,500-5,000, equal to as much as fifteen times median monthly income. Supply-chain consolidation, exemplified by Johnson Matthey's divestiture of its Medical Device Components unit, has intensified raw-material pricing pressure for nitinol and platinum-iridium alloys. Limited public healthcare budgets, typically under 5% of national spending for specialized interventions, hamper device procurement. Hospitals often lack modern imaging or hybrid operating suites, forcing additional capital outlays before procedures can be offered. Without targeted funding or price-managed offerings, cost barriers will continue to cap Neurothrombectomy devices market penetration in several emerging economies.

Other drivers and restraints analyzed in the detailed report include:

- Large-Bore Aspiration Catheters Reduce Procedure Time & Cost

- AI-Enabled Stroke Triage Broadens Eligible Patient Pool

- Shortage of Trained Neuro-Interventionists Outside Urban Centers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stent retrievers carried 63.78% of the Neurothrombectomy devices market share in 2025 and remain the procedural mainstay across comprehensive stroke centers. Their dominance reflects decades of clinical validation, including pivotal trials that confirm high reperfusion rates across clot morphologies. The segment benefits further from incremental design improvements, such as the NeVa NET 5.5 device that achieved 54.9% first-pass near-complete recanalization in multicenter evaluations. Despite premium pricing, hospitals continue to stock multiple stent retriever sizes, given high physician familiarity and versatile performance. In parallel, aspiration catheters command the fastest expansion path, with a 7.06% CAGR forecast through 2031, propelled by newer large-bore designs that streamline setup and reduce embolic complications. Combined mechanical systems appeal to specialists handling complex clot architectures but face moderate uptake due to higher cost and steeper learning curves. Balloon guide catheters and accessory lines grow in lockstep with core device adoption, ensuring integrated shelf solutions for stroke programs within the Neurothrombectomy devices market.

Price competition is unlikely to erode stent retriever dominance before 2030, yet the economic appeal of aspiration-first techniques continues to reshape procedural algorithms. Key manufacturers invest in coating technologies that enhance clot grip and minimize distal embolization, leveraging 510(k) pathways for accelerated U.S. clearance. The Neurothrombectomy devices market size for aspiration tools is set to benefit from these advances, while stent retriever vendors protect share through bundled service models, including hands-on training and AI-driven case planning. The interplay of efficacy evidence, cost containment, and workflow optimization underpins a healthy two-horse race that fuels continuous innovation in both categories.

The Neurothrombectomy Devices Market Report is Segmented by Device Type (Stent Retrievers, Aspiration Catheters, Combined Mechanical Thrombectomy Systems, Balloon Guide Catheters & Accessory Devices), End User (Hospitals, Specialty Neurosurgery Centers, Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the Neurothrombectomy devices market with 41.86% share in 2025, underpinned by robust payer coverage, dense hospital networks, and early adoption of extended-window guidelines. Medicare's 2023 coverage expansion for carotid interventions signaled ongoing policy support, while private insurers moved quickly to harmonize authorizations. U.S. centers capitalize on AI-driven triage software to reduce treatment delays, whereas Canada leverages universal healthcare to equalize access across provinces. Mexico adds incremental growth through medical technology harmonization that eases cross-border device clearance, culminating in a continental ecosystem that sustains steady procedure volumes and advances the regional Neurothrombectomy devices market.

Asia-Pacific is projected to post a 7.06% CAGR to 2031, making it the fastest-growing region for Neurothrombectomy devices. Government investment programs in China and India are building neuro-ICU capacity in secondary cities, expanding the addressable patient pool beyond traditional tier-one hospitals. Japan continues to adopt premium thrombectomy platforms under its universal insurance, while South Korea and Australia drive high-end device demand through well-funded national health systems. This diverse yet converging environment elevates Asia-Pacific as a strategic growth frontier, where training partnerships and price-tiered product lines can unlock additional share for global and regional manufacturers.

Europe presents a mature but stable market landscape, with comprehensive reimbursement coverage and established national stroke pathways. Germany's DRG reimbursement specificity delivers predictable economics, and the United Kingdom's NHS integrates thrombectomy into standardized quality metrics. France, Italy, and Spain contribute through academic research that informs pan-European clinical practice. Harmonized CE-mark standards streamline market entry, but economic austerity in certain jurisdictions moderates procedural growth. Overall, steady replacement cycles and an emphasis on outcome-based procurement preserve Europe's contribution to the Neurothrombectomy devices market, even as regional growth rates trail those of Asia-Pacific.

- Medtronic

- Stryker

- Penumbra

- Johnson & Johnson (CERENOVUS)

- Terumo

- MicroPort

- Rapid Medical Ltd.

- Phenox

- Acandis

- Vesalio, LLC

- Control Medical Technology, LLC

- Wallaby Medical

- Zylox-Tonbridge Medical Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing guideline-driven adoption after DAWN/DEFUSE-3 trials

- 4.2.2 Favorable reimbursement expansions in U.S., Germany & Japan

- 4.2.3 Large-bore aspiration catheters reduce procedure time & cost

- 4.2.4 AI-enabled stroke triage broadens eligible patient pool

- 4.2.5 Rapid growth of neuro-ICU beds in tier-2 Chinese & Indian cities

- 4.3 Market Restraints

- 4.3.1 High device & procedure cost in emerging markets

- 4.3.2 Shortage of trained neuro-interventionists outside urban centers

- 4.3.3 Supply-chain vulnerability for nitinol & platinum-iridium alloys

- 4.3.4 Reimbursement delays for posterior-circulation thrombectomies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Device Type (Value)

- 5.1.1 Stent Retrievers

- 5.1.2 Aspiration Catheters

- 5.1.3 Combined Mechanical Thrombectomy Systems

- 5.1.4 Balloon Guide Catheters & Accessory Devices

- 5.2 By End User (Value)

- 5.2.1 Hospitals

- 5.2.2 Specialty Neurosurgery Centers

- 5.2.3 Ambulatory Surgical Centers

- 5.3 By Geography (Value)

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 GCC

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Medtronic plc

- 6.3.2 Stryker Corporation

- 6.3.3 Penumbra Inc.

- 6.3.4 Johnson & Johnson (CERENOVUS)

- 6.3.5 Terumo Corporation

- 6.3.6 MicroPort Scientific Corporation

- 6.3.7 Rapid Medical Ltd.

- 6.3.8 Phenox GmbH

- 6.3.9 Acandis GmbH

- 6.3.10 Vesalio, LLC

- 6.3.11 Control Medical Technology, LLC

- 6.3.12 Wallaby Medical

- 6.3.13 Zylox-Tonbridge Medical Technology Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment