|

시장보고서

상품코드

1906174

종양 분자진단 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Oncology Molecular Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

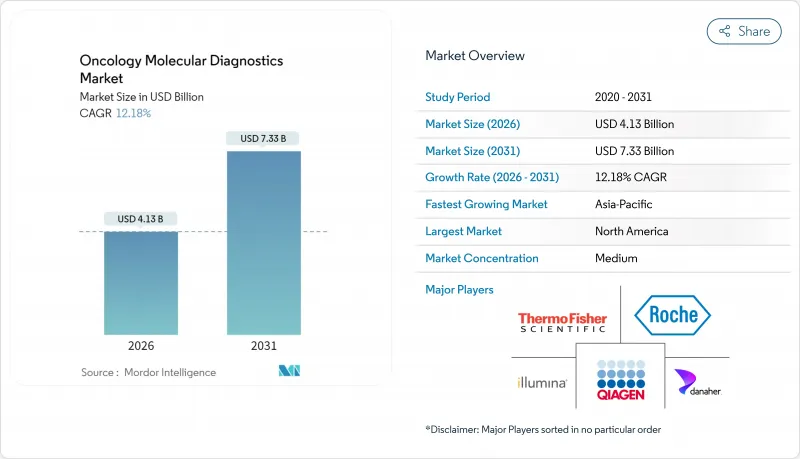

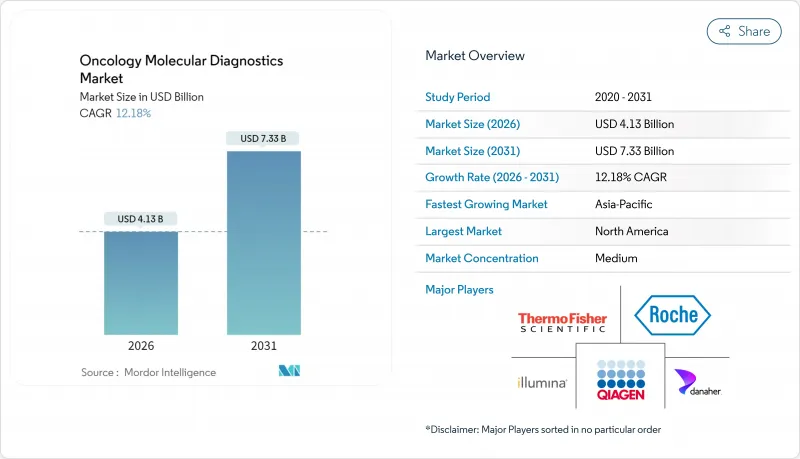

2026년 종양 분자진단 시장의 규모는 41억 3,000만 달러로 추정되며, 2025년 36억 8,000만 달러에서 성장하여, 2031년에는 73억 3,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 12.18%를 나타낼 전망입니다.

표적 요법과 연동한 동반진단, 액체 생검의 승인 확대, AI를 활용한 생물정보학이 임상 도입을 가속화하고 있습니다. 또, 환급 규정을 개선하는 국가 유전체 계획, 치료 과정에서 환자 1명당 복수의 분자 검사를 필요로 하는 암 이환율의 상승도 수요를 뒷받침하고 있습니다. 반면, 포인트 오브 케어 플랫폼은 중앙 검사실에서 첨단 검사를 분산시켜 결과 보고 시간을 단축하고 접근성을 확대하고 있습니다. 경쟁 환경은 자체 시약과 분석 소프트웨어를 결합한 수직 통합 리더 기업에 유리하게 작동합니다. 한편, 틈새 시장의 혁신기업은 AI와 액체 생검 기술을 활용하여 종양 분자진단 시장에서 미개척 영역의 기회를 파악하고 있습니다.

세계의 종양 분자진단 시장의 동향 및 인사이트

치료 경로를 변화시키는 액체 생검 동반진단

FDA의 액체 생검 동반진단제 승인은 2023년 이후 급증하여 침습적인 조직 채취를 수반하지 않는 실시간 유전체 모니터링을 가능하게 하고 있습니다. FoundationOne Liquid CDx는 현재 비소세포 폐암에 대한 MET 엑손 14 스키핑 변이 치료의 지침이 되어 조직 샘플이 한정되는 환자에 대해 정밀의료를 확대하고 있습니다. 화상에서 변화가 나타나기 전에 내성 변이를 검출할 수 있기 때문에 종양 전문의가 조기에 치료법을 변경해 치료 효과를 향상시키는 것이 가능해져 임상 도입이 진행되고 있습니다.

국가 유전체 계획이 환급 프레임워크를 가속화

호주의 PrOSPeCT 프로그램 등에서는 1억 8,500만 달러의 자금으로 2만 3,000명의 환자에게 무료 유전체 검사를 제공하고 있으며, 정책조정 및 임상시험에 대한 접근성 및 보험 적용 결정이 연계됨으로써 정밀 암 의료가 민주화되는 실례를 보이고 있습니다. 중국이나 일본에서도 같은 제도가 도입되는 가운데, 표준화된 프로토콜에 의해 지불자의 불확실성이 축소되어, 종양 분자진단 시장 전체에서 보험 적용 대상이 되는 검사가 확대되고 있습니다.

유전체 병리의 부족으로 진단 병목 현상 발생

병리 부문의 3%만이 유전체 전문의 인력이 배치된 것으로 나타났으며, 라틴아메리카가 부족 현상으로 가장 심각한 영향을 받고 있습니다. 전문 지식의 부족은 검사 결과의 해석을 제한하고 임상 판단의 지연을 초래합니다. 원격 상담 네트워크와 인공지능에 의한 의사결정 지원은 능력 부족을 완화하지만 완전한 해결책은 아니므로 가장 수요가 높은 지역에서 성장을 억제하고 있습니다.

부문 분석

시약 및 소모품은 2025년에 매출액의 61.55%를 차지하였고, 반복 수요와 저빈도 변이를 포착하는 독자 화학 기술이 반영되고 있습니다. 이 견고한 위치는 종양 분자진단 시장에서 제조업체의 안정적인 현금 흐름을 지원합니다. 소프트웨어 서비스는 현재 규모가 작지만, 클라우드 기반 해석 툴에 의한 자동 해석과 희귀한 유전체 병리에 대한 전문의의 필요성 감소에 의해 15.21%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다.

AI 기반 플랫폼이 성장함에 따라 생물정보학은 전략적 이점으로 자리매김하고 있습니다. 시약과 구독 분석 도구를 번들로 제공하는 공급업체는 엔드 투 엔드 통합을 실현하여 고객의 정착률 향상에 기여합니다. 실험실이 효율화와 표준화된 보고를 요구하는 가운데, 종양 분자진단 소프트웨어 솔루션 시장의 규모는 현저한 확대가 예상됩니다.

PCR은 2025년 34.62%의 수익을 달성했습니다. 이는 검사 기관이 PCR의 비용 효율성과 신뢰성을 높이 평가하고 있기 때문입니다. 디지털 PCR은 액체 생검에서 드문 돌연변이의 검출 감도를 더욱 향상시킵니다. 더불어 차세대 시퀀싱은 실행 비용이 낮고 임상적 유용성이 확대됨에 따라 13.5%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 하이브리드 캡처 패널은 한 번의 검사로 수백 개의 유전자를 검출할 수 있어 치료 선택을 변화시킵니다.

NGS의 채택은 종양의 이질성을 밝히는 조직과 혈장의 복합 워크플로로부터도 혜택을 받고 있습니다. 검사 기관이 액체 생검 NGS 패널의 검증을 진행하는 가운데 종합적 프로파일링의 종양 분자진단 시장 내 규모는 단일 유전자 PCR 검사를 능가하는 성장을 보이고 있지만, 신속한 단일 변이 확인에는 여전히 PCR이 필수적입니다.

지역별 분석

북미는 2025년 39.72%의 수익을 차지하였으며 종합적 유전체 프로파일링에 대한 조기 규제 승인과 광범위한 보험 적용을 활용하고 있습니다. 주요 암 센터에서 실용적인 바이오마커의 검사율은 90%에 육박합니다. 미세 잔존 병변 추적에 대한 메디케어 적용 확대는 종양 분자진단 시장을 더욱 확대하고 있습니다.

유럽에서는 비용효과의 관점에서 임상적 유용성이 증명된 이후 선택적으로 도입되면서 일관적인 환급이 이루어지고 있습니다. 유럽 의약품청에 의한 동반진단제와 의약품의 조화적인 승인은 시장 진입의 동기화를 보장하고 예산 영향 평가에 의한 억제 하에 안정된 성장을 지원하고 있습니다.

아시아태평양은 중국의 정밀의료 계획과 일본의 유전체 암 프로그램에 의해 15.89%라는 가장 높은 CAGR을 기록하고 있습니다. 국가 시퀀싱 네트워크에 대한 투자와 정부-민간 연계로 검사 단가가 하락하고 기술 이전이 가속화되고 있습니다. 지역 특유의 돌연변이에 대응한 검사법이 현지의 혁신자에 의해 개선되는 가운데, 암 발생률의 상승과 의료 인프라의 개선에 의해 아시아태평양의 종양 분자진단 시장의 규모는 급속히 확대되고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- FDA 및 EMA 승인 후 액체 생검 동반진단제의 도입

- 국가 유전체 계획에 의한 환급 촉진

- AI 구동형 생물정보학에 의한 차세대 시퀀싱(NGS)의 턴어라운드 타임 단축

- 암 이환율의 상승

- 포인트 오브 케어 검사에 대한 수요 증가

- 종합적인 암 프로파일링을 위한 멀티오믹스 통합 진전

- 억제요인

- 라틴아메리카에서 부족한 유전체 병리 전문의

- 분자진단 검사의 높은 비용

- 액체 생검 ctDNA 검사에서의 감도 및 품질 관리 과제

- 숙련 노동력 부족과 엄격한 규제 프레임워크

- 규제 상황

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측(금액)

- 제품 유형별

- 기기

- 시약 및 소모품

- 소프트웨어 및 서비스

- 기술별

- 중합효소 연쇄반응(PCR)

- 등온 NAAT

- 차세대 시퀀싱(NGS)

- 제자리 부합법(FISH/CISH)

- 질량 분석법

- 칩 및 마이크로어레이

- 전사 매개 증폭

- 암 유형별

- 유방암

- 폐암

- 대장암

- 전립선암

- 혈액 악성 종양

- 간암

- 자궁 경부암 및 부인과 암

- 기타 고형 종양

- 검체 유형별

- 조직 생검

- 액체 생검(혈액, 혈장 및 혈청)

- 세침 흡인 검체 및 세포 진단 검체

- 최종 사용자별

- 병원

- 진단센터

- 포인트 오브 케어 환경

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd

- Danaher Corporation

- Thermo Fisher Scientific Inc.

- Illumina Inc.

- Qiagen NV

- Sysmex Corporation

- bioMerieux SA

- Agilent Technologies Inc.(Dako)

- HTG Molecular Diagnostics Inc.

- Veracyte Inc.

- TBG Diagnostics Ltd.

- Guardant Health Inc.

- Foundation Medicine Inc.

- Exact Sciences Corp.

- NeoGenomics Laboratories

- BGI Genomics Co. Ltd.

- Bio-Rad Laboratories Inc.

- Natera Inc.

- Myriad Genetics Inc.

제7장 시장 기회 및 미래 전망

CSM 26.01.28Oncology Molecular Diagnostics Market size in 2026 is estimated at USD 4.13 billion, growing from 2025 value of USD 3.68 billion with 2031 projections showing USD 7.33 billion, growing at 12.18% CAGR over 2026-2031.

Companion diagnostics linked to targeted therapies, expanding liquid biopsy approvals, and AI-enabled bioinformatics are accelerating clinical uptake. Demand is also fueled by national genomics programs that improve reimbursement frameworks and by the rising prevalence of cancer, which drives multiple molecular tests per patient along the treatment continuum. Meanwhile, point-of-care platforms are moving sophisticated assays out of centralized laboratories, shrinking turnaround times and broadening access. Competitive dynamics favor vertically integrated leaders that pair proprietary reagents with analytics software, while niche innovators leverage AI and liquid biopsy technologies to capture white-space opportunities within the oncology molecular diagnostics market.

Global Oncology Molecular Diagnostics Market Trends and Insights

Liquid-biopsy companion diagnostics transforming treatment pathways

FDA approvals for liquid biopsy companion diagnostics have multiplied since 2023, enabling real-time genomic monitoring without invasive tissue sampling. FoundationOne Liquid CDx now guides MET exon 14 skipping therapy in non-small cell lung cancer, expanding precision care to patients with limited tissue. Clinical adoption is rising because the assays detect resistance mutations before imaging changes appear, letting oncologists switch therapies earlier and improving outcomes.

National genomics initiatives accelerating reimbursement frameworks

Programs such as Australia's PrOSPeCT offer 23,000 patients free genomic testing funded by USD 185 million, demonstrating how coordinated policy, clinical trial access, and coverage decisions converge to democratize precision oncology. As similar schemes roll out in China and Japan, standardized protocols lower payer uncertainty, expanding compensated testing indications across the oncology molecular diagnostics market.

Genomic pathologist shortage creating diagnostic bottlenecks

Only 3% of pathology departments report adequate staffing of genomic specialists, with Latin America most affected. Limited expertise constrains report interpretation and delays clinical decision making. Teleconsultation networks and AI decision support mitigate but do not fully resolve the capacity gap, tempering growth in regions with the greatest need.

Other drivers and restraints analyzed in the detailed report include:

- AI-driven bioinformatics slashing NGS turnaround times

- Increasing demand for point-of-care testing

- Cost barriers limiting adoption in emerging markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and consumables generated 61.55% revenue in 2025, reflecting recurrent demand and proprietary chemistries that capture low-abundance mutations. This strong position anchors steady cash flows for manufacturers within the oncology molecular diagnostics market. Software and services, although smaller today, rise at a 15.21% CAGR as cloud-hosted analytics automate interpretation and reduce the need for scarce genomic pathologists.

Growth in AI-powered platforms positions bioinformatics as a strategic moat. Vendors bundling reagents with subscription-based interpretation tools secure end-to-end integration, fostering customer stickiness. The oncology molecular diagnostics software solutions market size is projected to expand markedly as laboratories seek efficiency gains and standardized reporting.

PCR delivered 34.62% revenue in 2025 as laboratories value its cost efficiency and reliability. Digital PCR further extends sensitivity for detecting rare variants in liquid biopsy. In parallel, next-generation sequencing enjoys a 13.5% CAGR, propelled by declining run costs and broader clinical utility. Hybrid capture panels detect hundreds of genes in one assay, transforming treatment selection.

NGS adoption also benefits from combined tissue and plasma workflows that reveal tumor heterogeneity. As laboratories validate liquid biopsy NGS panels, the oncology molecular diagnostics market size for comprehensive profiling grows faster than single-gene PCR assays, yet PCR remains indispensable for rapid single-mutation confirmation.

The Oncology Molecular Diagnostics Market Report is Segmented by Product Type (Instrument, and More), Technology (Polymerase Chain Reaction, and More), Cancer Type (Breast Cancer, and More), Sample Type (Tissue Biopsy, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 39.72% revenue in 2025, leveraging early regulatory approvals and broad insurance coverage for comprehensive genomic profiling. Testing rates for actionable biomarkers approach 90% in leading cancer centers. Expanded Medicare coverage for minimal residual disease tracking further enlarges the oncology molecular diagnostics market.

Europe adopts a cost-effectiveness lens, leading to selective uptake but consistent reimbursement once clinical utility is proven. Harmonized companion diagnostic and drug approvals by the European Medicines Agency ensure synchronized market entry, supporting stable growth moderated by budget impact assessments.

Asia-Pacific posts the fastest 15.89% CAGR supported by China's precision medicine plan and Japan's genomic cancer program. Investments in national sequencing networks and public-private partnerships lower per-test costs and accelerate technology transfer. As local innovators refine assays for region-specific mutations, the oncology molecular diagnostics market size in Asia-Pacific expands rapidly with rising cancer incidence and improving healthcare infrastructure.

- Abbott Laboratories

- Roche

- Danaher

- Thermo Fisher Scientific

- Illumina

- QIAGEN

- Sysmex

- bioMerieux

- Agilent Technologies Inc. (Dako)

- HTG Molecular Diagnostics

- Veracyte

- TBG Diagnostics Ltd.

- Guardant Health

- Foundation Medicine Inc.

- Exact Sciences Corp.

- NeoGenomics Laboratories

- BGI Genomics Co. Ltd.

- Bio-Rad Laboratories

- Natera

- Myriad Genetics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Uptake of Liquid-Biopsy Companion Diagnostics Post FDA & EMA Approvals

- 4.2.2 National Genomics Initiatives Accelerating Reimbursement

- 4.2.3 AI-driven Bioinformatics Reducing NGS Turn-around Time

- 4.2.4 Rising Prevalence of Cancer

- 4.2.5 Increasing Demand for Point-of-care Testing

- 4.2.6 Growing Integration of Multi-Omics Approaches for Comprehensive Cancer Profiling

- 4.3 Market Restraints

- 4.3.1 Shortage of Genomic Pathologists in Latin America

- 4.3.2 High Cost of Molecular Diagnostic Tests

- 4.3.3 Sensitivity & QC Challenges in Liquid Biopsy ctDNA Testing

- 4.3.4 Lack of Skilled Workforce and Stringent Regulatory Framework

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Buyers

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Instruments

- 5.1.2 Reagents & Consumables

- 5.1.3 Software & Services

- 5.2 By Technology

- 5.2.1 Polymerase Chain Reaction (PCR)

- 5.2.2 Isothermal NAAT

- 5.2.3 Next-Generation Sequencing (NGS)

- 5.2.4 In-situ Hybridization (FISH/CISH)

- 5.2.5 Mass Spectrometry

- 5.2.6 Chips & Microarrays

- 5.2.7 Transcription-Mediated Amplification

- 5.3 By Cancer Type

- 5.3.1 Breast Cancer

- 5.3.2 Lung Cancer

- 5.3.3 Colorectal Cancer

- 5.3.4 Prostate Cancer

- 5.3.5 Hematological Malignancies

- 5.3.6 Liver Cancer

- 5.3.7 Cervical & Gynecologic Cancers

- 5.3.8 Other Solid Tumors

- 5.4 By Sample Type

- 5.4.1 Tissue Biopsy

- 5.4.2 Liquid Biopsy (Blood/Plasma/Serum)

- 5.4.3 Fine-Needle Aspirates & Cytology Samples

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Diagnostic Centers

- 5.5.3 Point-of-Care Settings

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 F. Hoffmann-La Roche Ltd

- 6.3.3 Danaher Corporation

- 6.3.4 Thermo Fisher Scientific Inc.

- 6.3.5 Illumina Inc.

- 6.3.6 Qiagen N.V.

- 6.3.7 Sysmex Corporation

- 6.3.8 bioMerieux SA

- 6.3.9 Agilent Technologies Inc. (Dako)

- 6.3.10 HTG Molecular Diagnostics Inc.

- 6.3.11 Veracyte Inc.

- 6.3.12 TBG Diagnostics Ltd.

- 6.3.13 Guardant Health Inc.

- 6.3.14 Foundation Medicine Inc.

- 6.3.15 Exact Sciences Corp.

- 6.3.16 NeoGenomics Laboratories

- 6.3.17 BGI Genomics Co. Ltd.

- 6.3.18 Bio-Rad Laboratories Inc.

- 6.3.19 Natera Inc.

- 6.3.20 Myriad Genetics Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment