|

시장보고서

상품코드

1906179

유럽의 건축 및 건축용 시트 시장 : 시장 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Europe Building And Construction Sheets - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

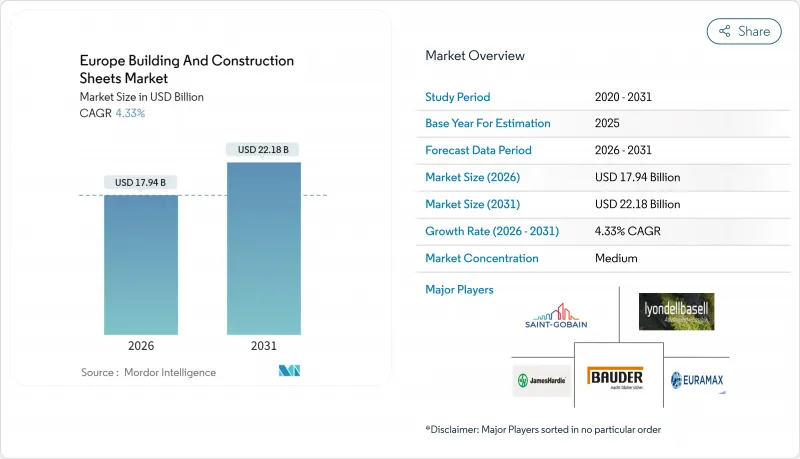

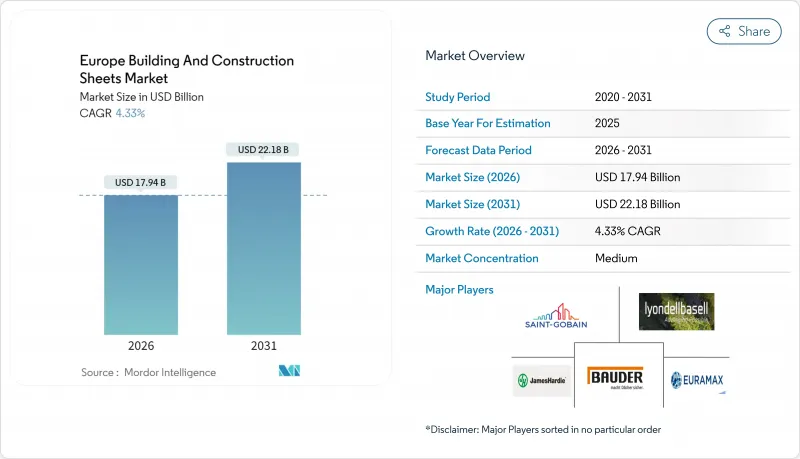

유럽의 건축 및 건축용 시트 시장 규모는 2026년에 179억 4,000만 달러에 달할 것으로 예측되고 있습니다. 2025년 172억 달러로 평가되었고, 성장해 2031년에는 221억 8,000만 달러에 이를 것으로 보이며, 2026-2031년에 걸쳐 연평균 복합 성장률(CAGR) 4.33%로 성장할 전망입니다.

이러한 전망은 변동성이 큰 거시경제 환경 속에서도 시장의 지속 가능성을 강조하며, 2030년까지 탄소 중립 건물을 의무화하는 유럽연합 기후 지침과의 부합성을 보여줍니다. 규제 압박으로 인해 구조적 성능과 태양광 발전 또는 향상된 단열 기능을 결합한 시트 사양이 주목받고 있습니다. 동시에 연간 1,562억 3천만 달러 규모의 공공 자금이 리모델링 중심 시트 시스템 수요를 촉진하고 있으며, 급성장하는 데이터센터 부문과 모듈식 건설 방식이 상업적 기회를 확대하고 있습니다. 특히 디지털 모니터링과 저탄소 생산을 융합하는 공급업체 간 통합이 심화되면서 유럽의 건축 및 건축용 시트 시장의 경쟁 구도가 재편되고 있습니다.

유럽의 건축 및 건축용 시트 시장 동향 및 인사이트

건축 외피에 대한 엄격한 에너지 절약 규제

유럽의 건축 및 건설 시트 시장은 엄격한 규정과 지속가능성 목표에 힘입어 중대한 변혁을 겪고 있습니다. 개정된 '건물 에너지 성능 지침(EPBD)'에 따라 회원국들은 2030년까지 제로 배출 건물 상태를 달성해야 합니다. 이 의무는 설계자들이 구조적 강도와 높은 열 저항 또는 태양광 패널을 결합한 시트를 우선적으로 선택하도록 유도합니다. 또한 2030년까지 완료해야 하는 수명주기 온난화 잠재력 평가로 인해 재활용 원료와 저탄소 제조 수요가 증가하고 있습니다. 독일은 5,207억 8천만 달러 규모의 기후 기금을 통해 건설 분야의 탈탄소화에 최소 1,041억 5천만 달러를 할당하는 등 상당한 움직임을 보이고 있으며, 이는 수요량을 더욱 확대시키고 있습니다. 이러한 입법적 추진력은 시장 내 프리미엄 가격 형성을 촉진하고 연구개발(R&D) 노력을 강화하고 있습니다. 인증된 저탄소 발자국을 보유한 공급업체들은 이제 공공 프로젝트에서 우선 입찰자 지위를 확보하며 장기 성장 기회를 선점하고 있습니다.

리노벨링 프로그램을위한 공적 자금 확대

유럽의 건축용 시트 시장은 에너지 효율 개조에 대한 투자 증가로 상당한 성장을 보이고 있습니다. 연간 1,562억 3천만 달러 규모의 EU 보조금이 에너지 개조를 주도하며, 주요 구조 변경 없이 외벽, 지붕, 외장 시스템을 업그레이드하고 있습니다. 스페인 국가 에너지 효율 기금은 취약 계층 가구와 에너지 효율이 낮은 건물을 우선 대상으로 연간 3억 8천만 달러를 배정합니다. 이 정책은 실질적인 킬로와트시 절감 효과를 보장하는 비용 효율적인 폴리머 및 하이브리드 시트 사용을 유도합니다. 프랑스는 에너지 효율 개선을 위한 무이자 대출과 세금 감면 제도를 재도입하여 신축 활동이 둔화되는 상황에서도 수요를 촉진하고 있습니다. 금융 지침은 검증 가능한 성능을 요구하여 건설사들이 실시간 열 데이터를 제공하는 통합 센서가 장착된 스마트 시트를 선택하도록 유도하고 있습니다. 이러한 요소들이 종합적으로 해당 지역의 전문적인 리모델링 등급 제품에 대한 수요를 유지하고 있습니다.

변동성 높은 에너지 가격, 생산 비용 상승

유럽의 건축 및 건축용 시트 시장은 현재 에너지 가격 변동성과 규제 압박으로 인한 어려움을 겪고 있습니다. 도매 가스 요금은 2023년 최고점에서 하락했으나 제조업체의 전기 요금은 여전히 역사적 평균을 상회하여 철강, 알루미늄, 폴리머 시트 생산자의 이익 마진을 압박하고 있습니다. EU 배출권 거래제(EU ETS)의 잠재적 연장은 특히 고로 운영에 대한 탄소 비용을 더욱 상승시키고 있습니다. 기업들은 이러한 어려움을 완화하기 위해 현장 태양광 솔루션과 전력 구매 계약(PPA)을 도입하고 있으나, 이는 상당한 자본 투자와 긴 허가 절차를 필요로 합니다. 비용 인플레이션은 프로젝트 입찰에도 영향을 미쳐 수주 주기 지연이나 자재 대체를 초래하고 있습니다. 이러한 장애물에도 불구하고 기업들이 변화하는 에너지 및 규제 환경에 적응함에 따라 시장은 안정화될 것으로 예상됩니다.

부문 분석

금속 시트는 2025년 매출의 32.65%를 차지하며 유럽의 건축 시트 시장의 구조적 핵심 지위를 공고히 했습니다. 수요는 강철의 하중 지지 능력과 알루미늄의 내식성에 의존하며, 이 두 재료는 재생 에너지로 구동되는 전기로(Electric Arc Furnace)와 같은 저탄소 공정으로 점점 더 많이 생산되고 있습니다. 아르셀로미탈과 타타 스틸 유럽은 내재 배출량을 최대 40%까지 절감하는 재활용 함유 등급을 적극 추진 중입니다. 동시에 건물 일체형 태양광(BIPV)은 박막 셀의 프레임리스 캐리어로 알루미늄 외피를 채택하여 금속 수요를 녹색 에너지 목표와 직접 연계합니다.

폴리머 시트는 구조 보강을 피하는 리모델링에 경량 패널을 선호하는 계약업체로 인해 2031년까지 5.29%의 가장 빠른 부문 연평균 성장률(CAGR)을 기록할 전망입니다. 난연제 및 자외선 안정제를 포함한 배합은 수명을 연장하는 반면, 바이오 기반 수지는 저탄소 대안을 제시합니다. 하이브리드 시스템은 다층 폴리머 막 내에 유연한 태양광 라미네이트 또는 상변화 물질을 내장하여 기능적 범위를 확장합니다. 역청과 고무는 방수 및 진동 감쇠 분야에서 역할을 유지하지만, 휘발성 화합물에 대한 지속적인 규제 강화로 시장 입지가 위협받고 있습니다. 전반적으로 소재 혁신은 유럽의 건축 시트 시장의 공급 측면 차별화를 강화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 동향과 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 건물 외피에 대한 에너지 효율 규제의 강화

- 리모델링 프로그램에 대한 공공 자금 지원 확대

- 데이터 센터 건설 증가로 인한 구조용 데킹 수요 증가

- 모듈식 및 현장 외 건설 방식의 채택 증가

- 태양광 기술 지붕 및 외벽 시스템에의 통합

- 지역 조달 저탄소 시트 재료로의 전환

- 시장 성장 억제요인

- 생산 비용 상승을 초래하는 변동성 높은 에너지 가격

- 저비용 수입품의 접근을 제한하는 무역조치

- 숙련 설치 작업원의 부족

- 신용 조건의 계약이 신규 건설 파이프라인을 억제

- 가치/공급망 분석

- 규제 상황(EU 그린딜 및 에너지 성능 지령)

- 기술의 전망

- 지속가능성과 순환형 경제에 대한 노력

- 디지털화와 오프사이트 건설의 영향

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 소재별

- 아스팔트

- 고무

- 금속

- 폴리머

- 기타

- 건설 유형별

- 신축

- 리노벨링

- 최종 사용자별

- 주거용

- 상업용

- 인프라

- 국가별

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Saint-Gobain

- LyondellBasell

- James Hardie Industries plc

- Paul Bauder GmbH

- Euramax International

- Celotex Limited

- Rauch Spanplattenwerk GmbH

- Rizolin LLC

- Icopal(BMI Group)

- CBG Composites GmbH

- Kingspan Group plc

- Tata Steel Europe

- ArcelorMittal Construction

- Sika AG

- Soprema Group

- Firestone Building Products(Holcim Elevate)

- IKO Industries

- Owens Corning

- BASF SE

- Knauf Insulation

- Coroplast Fritz Muller GmbH

제7장 시장 기회와 장래의 전망

HBR 26.01.26The Europe Building & Construction Sheets Market size in 2026 is estimated at USD 17.94 billion, growing from 2025 value of USD 17.2 billion with 2031 projections showing USD 22.18 billion, growing at 4.33% CAGR over 2026-2031.

This outlook underscores the market's durability in a volatile macro environment and its alignment with European Union climate directives that mandate zero-emission buildings by 2030. Regulatory pressure is redirecting specifications toward sheets that combine structural performance with solar harvesting or enhanced thermal insulation. Simultaneously, USD 156.23 billion in annual public funding is stimulating demand for renovation-focused sheet systems, while the fast-rising data-centre sector and modular construction practices are widening commercial opportunities. Intensifying consolidation, particularly among suppliers that fuse digital monitoring with low-carbon production, is reshaping competitive dynamics across the Europe building construction sheets market.

Europe Building And Construction Sheets Market Trends and Insights

Stricter Energy-Efficiency Regulations for Building Envelopes

The European building and construction sheets market is undergoing a significant transformation driven by stringent regulations and sustainability goals. Under the revised Energy Performance of Buildings Directive, member states must achieve zero-emission building status by 2030. This mandate pushes specifiers to prioritize sheets that combine structural strength with high thermal resistance or photovoltaic layers. Additionally, life-cycle warming potential assessments, also due by 2030, are driving up the demand for recycled inputs and low-carbon manufacturing. Germany is making a significant move with its USD 520.78 billion climate fund, dedicating at least USD 104.15 billion to decarbonizing construction, which in turn amplifies volume requirements. This legislative momentum is boosting premium pricing and intensifying R&D efforts in the market. Suppliers with certified low embodied-carbon footprints are now securing preferred-bidder status on public projects, positioning themselves for long-term growth opportunities.

Expanded Public Funding for Renovation Programmes

The Europe building construction sheets market is witnessing significant growth, driven by increasing investments in energy-efficient retrofits. Annual EU grants of USD 156.23 billion are driving energy retrofits, upgrading facades, roofs, and cladding systems without major structural changes. Spain's National Energy Efficiency Fund allocates USD 380 million annually, prioritising vulnerable households and underperforming buildings. This focus leans towards cost-effective polymer and hybrid sheets, ensuring tangible kilowatt-hour savings. France has reintroduced zero-interest loans and tax breaks for energy-efficient upgrades, boosting demand even as new construction activity slows. Financing guidelines mandate verifiable performance, leading builders to opt for smart sheets with integrated sensors that provide real-time thermal data. These factors collectively sustain the demand for specialised renovation-grade products in the region.

Volatile Energy Prices Elevating Production Costs

The Europe building and construction sheets market is currently navigating challenges stemming from energy price volatility and regulatory pressures. While wholesale gas rates have retreated from their 2023 highs, electricity tariffs for manufacturers remain above historical averages, squeezing profit margins for steel, aluminium, and polymer sheet producers. The potential extension of the EU Emissions Trading System is further elevating carbon costs, particularly for blast-furnace operations. Companies are adopting on-site solar solutions and power-purchase agreements to mitigate these challenges, but these require significant capital investments and lengthy permitting processes. Cost inflation is also impacting project bids, causing delays in award cycles or material substitutions. Despite these hurdles, the market is expected to stabilize as firms adapt to evolving energy and regulatory landscapes.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Data-Centre Construction Increasing Demand for Structural Decking

- Rising Adoption of Modular and Off-Site Construction Methods

- Shortage of Skilled Installation Labour

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal sheets secured 32.65% of 2025 revenue, reinforcing their status as the structural backbone of the Europe building construction sheets market. Demand leans on steel's load-bearing capacity and aluminium's corrosion resistance, both increasingly produced through low-carbon pathways such as electric arc furnaces powered by renewable electricity. ArcelorMittal and Tata Steel Europe actively promote recycled-content grades that cut embodied emissions by up to 40%. In parallel, building-integrated photovoltaics adopt aluminium skins as frameless carriers for thin-film cells, linking metal demand directly to green-energy targets.

Polymer sheets deliver the fastest segment CAGR of 5.29% toward 2031 as contractors favour lightweight panels for retrofits that avoid structural reinforcement. Formulations incorporating fire retardants and UV stabilisers extend service life, while bio-based resins open a lower-carbon alternative. Hybrid systems embed flexible solar laminates or phase-change materials within multilayer polymer membranes, broadening functional scope. Bitumen and rubber maintain roles in waterproofing and vibration damping, yet continual regulatory tightening on volatile compounds challenges their market presence. Overall, material innovation strengthens supply-side differentiation across the Europe building construction sheets market.

The Europe Building and Construction Sheets Market Report is Segmented by Material (Bitumen, Rubber, Metal, Polymer and Others), by Construction Type (New Construction and Renovation), by End-User (Residential, Commercial and Infrastructure), and by Country (United Kingdom, Germany, France, Italy, Spain and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Saint-Gobain

- LyondellBasell

- James Hardie Industries plc

- Paul Bauder GmbH

- Euramax International

- Celotex Limited

- Rauch Spanplattenwerk GmbH

- Rizolin LLC

- Icopal (BMI Group)

- CBG Composites GmbH

- Kingspan Group plc

- Tata Steel Europe

- ArcelorMittal Construction

- Sika AG

- Soprema Group

- Firestone Building Products (Holcim Elevate)

- IKO Industries

- Owens Corning

- BASF SE

- Knauf Insulation

- Coroplast Fritz Muller GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter energy-efficiency regulations for building envelopes

- 4.2.2 Expanded public funding for renovation programmes

- 4.2.3 Growth in data-centre construction increasing demand for structural decking

- 4.2.4 Rising adoption of modular and off-site construction methods

- 4.2.5 Integration of solar technologies into roofing and cladding systems

- 4.2.6 Shift toward locally sourced, low-carbon sheet materials

- 4.3 Market Restraints

- 4.3.1 Volatile energy prices elevating production costs

- 4.3.2 Trade measures limiting access to low-cost imports

- 4.3.3 Shortage of skilled installation labour

- 4.3.4 Tighter credit conditions damping new-build pipelines

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape (EU Green Deal & EPBD)

- 4.6 Technological Outlook

- 4.7 Sustainability & Circularity Initiatives

- 4.8 Digitalisation & Off-site Construction Impact

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Bitumen

- 5.1.2 Rubber

- 5.1.3 Metal

- 5.1.4 Polymer

- 5.1.5 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Renovation

- 5.3 By End-user

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Saint-Gobain

- 6.4.2 LyondellBasell

- 6.4.3 James Hardie Industries plc

- 6.4.4 Paul Bauder GmbH

- 6.4.5 Euramax International

- 6.4.6 Celotex Limited

- 6.4.7 Rauch Spanplattenwerk GmbH

- 6.4.8 Rizolin LLC

- 6.4.9 Icopal (BMI Group)

- 6.4.10 CBG Composites GmbH

- 6.4.11 Kingspan Group plc

- 6.4.12 Tata Steel Europe

- 6.4.13 ArcelorMittal Construction

- 6.4.14 Sika AG

- 6.4.15 Soprema Group

- 6.4.16 Firestone Building Products (Holcim Elevate)

- 6.4.17 IKO Industries

- 6.4.18 Owens Corning

- 6.4.19 BASF SE

- 6.4.20 Knauf Insulation

- 6.4.21 Coroplast Fritz Muller GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment